Lisa Cook sues Trump over firing attempt, emergency hearing set

Introduction & Market Context

United Rentals , Inc. (NYSE:URI) released its second quarter 2025 investor presentation on July 24, 2025, highlighting the company’s continued market leadership and strategic initiatives. As the largest equipment rental company in North America with a 15% market share, United Rentals has maintained its growth trajectory through a combination of organic expansion, strategic acquisitions, and digital transformation.

The company’s presentation comes after a strong first quarter, where URI reported total revenue of $3.72 billion (up 6.7% year-over-year) and rental revenue of $3.1 billion (up 7.4% year-over-year). The stock has shown volatility over the past year, trading within a 52-week range of $525.91 to $896.98, with recent trading at approximately $791.04.

Quarterly Performance Highlights

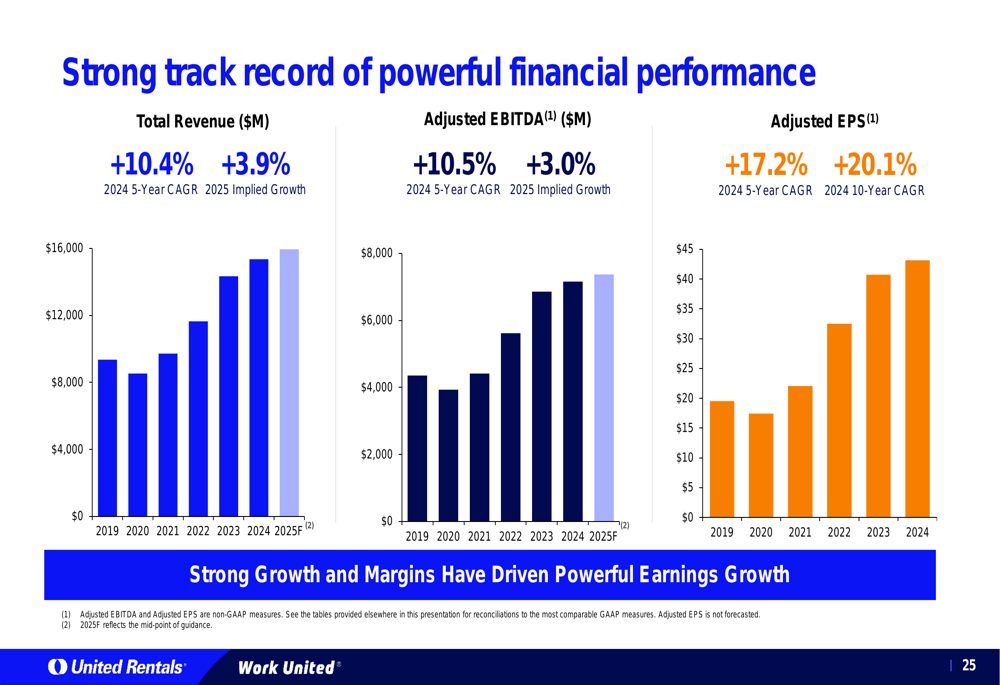

United Rentals continues to demonstrate solid financial performance, building on its 2024 results when the company achieved $15.3 billion in total revenue (a 7.1% year-over-year increase) and $7.2 billion in adjusted EBITDA (up 4.4% year-over-year).

The company’s presentation highlights its impressive long-term growth trajectory, with a five-year CAGR (2019-2024) of 10.4% for total revenue, 10.5% for adjusted EBITDA, and 17.2% for adjusted EPS. Over a ten-year period, adjusted EPS has grown at a remarkable 20.1% CAGR.

As shown in the following chart of the company’s financial performance track record:

The company has maintained strong adjusted EBITDA margins, reaching 46.7% in 2024. This financial discipline has translated into robust earnings growth, positioning URI well for continued success in 2025.

Strategic Initiatives

A key driver of United Rentals’ growth has been its specialty business, which represented approximately 33.4% of total revenue in 2024. The specialty segment has grown at an impressive 20.1% CAGR over the past decade, significantly outpacing the company’s overall growth rate.

The following chart illustrates the consistent growth of URI’s specialty business:

United Rentals is continuing its specialty expansion, targeting at least 50 new specialty cold-starts in 2025, compared to 72 in 2024. This focus on specialty solutions aligns with the company’s strategy to provide higher-margin services and create additional value for customers.

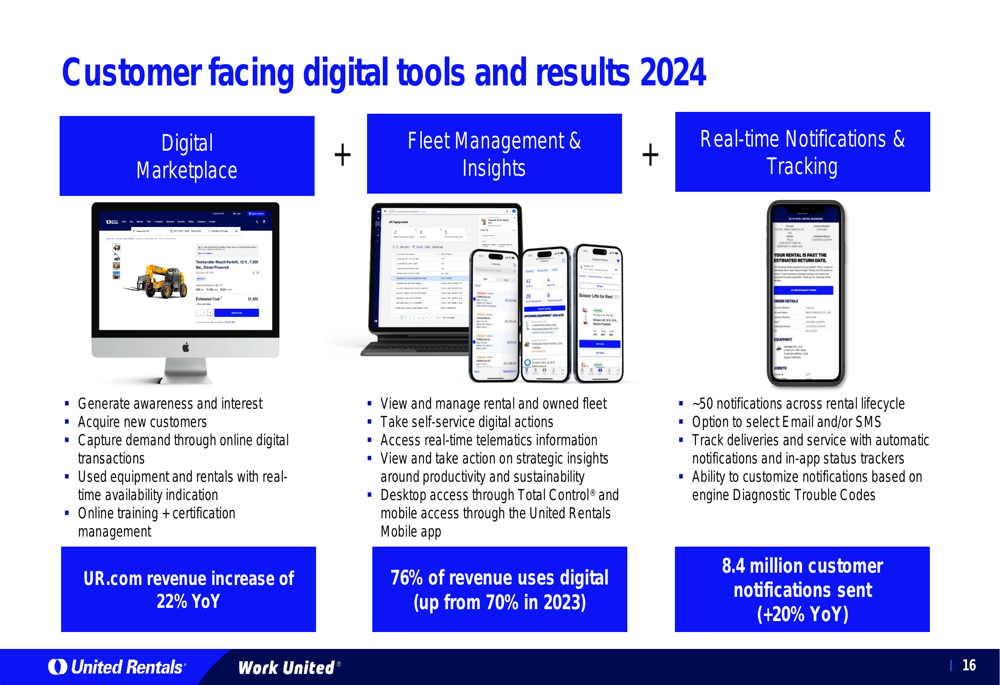

Digital transformation represents another critical strategic initiative for URI. The company has invested heavily in customer-facing digital tools, resulting in significant improvements in online engagement and operational efficiency.

The company’s digital marketplace and fleet management tools have yielded impressive results, as shown in the following slide:

These digital initiatives have driven a 22% year-over-year increase in online revenue, a 31% growth in online payments, and a 23% increase in online field service requests. Additionally, 76% of revenue now comes from customers using digital tools, up from 70% in 2023.

Competitive Industry Position

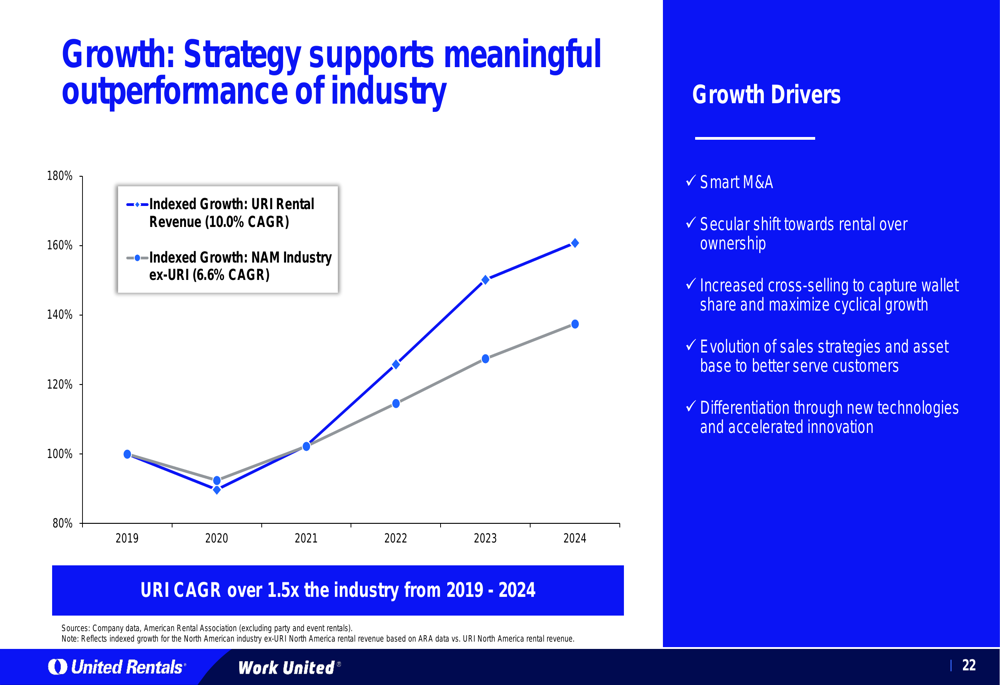

United Rentals has consistently outperformed the broader equipment rental industry, with its rental revenue growing at a 10.0% CAGR compared to the North American industry (excluding URI) growth of 6.6% CAGR from 2019 to 2024.

The following chart illustrates URI’s outperformance relative to the industry:

This outperformance is attributed to several factors, including strategic M&A, the secular shift toward rental over ownership, increased cross-selling to capture wallet share, evolution of sales strategies, and differentiation through technology and innovation.

The company benefits from a diverse end-market exposure, with only 5% of rental revenue coming from residential construction, while industrial and other segments account for 49% and verticals represent 46%. This diversification helps reduce cyclical volatility and provides stability across various economic conditions.

Financial Strength & Capital Allocation

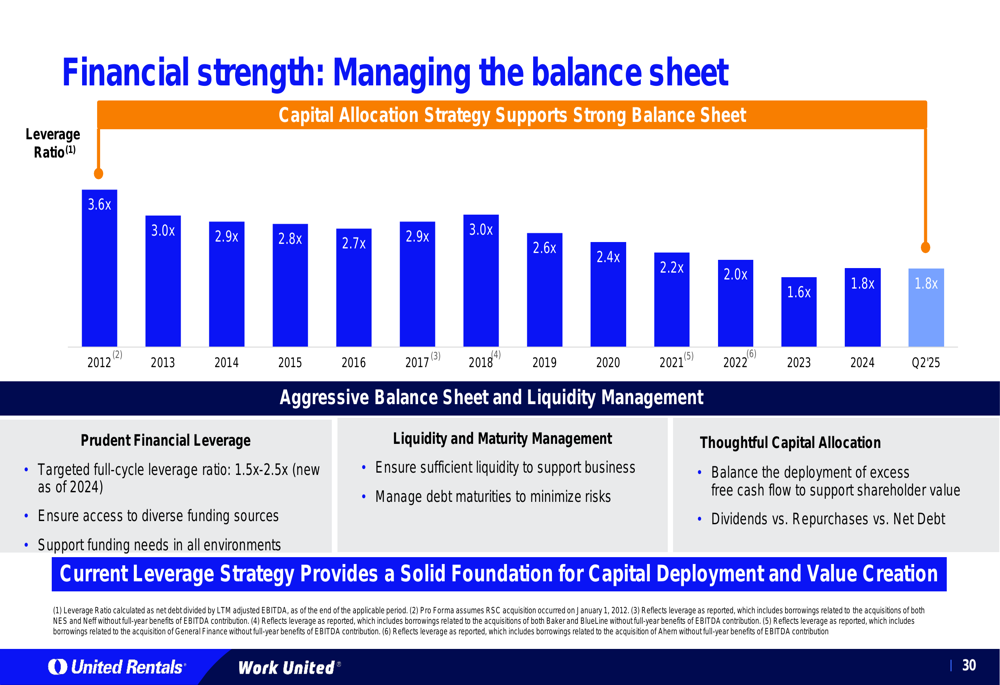

United Rentals has maintained a strong balance sheet, with a current leverage ratio of 1.8x as of Q2 2025, well within its targeted full-cycle leverage ratio of 1.5x-2.5x. The company has steadily reduced its leverage from 3.6x in 2012, as shown in the following chart:

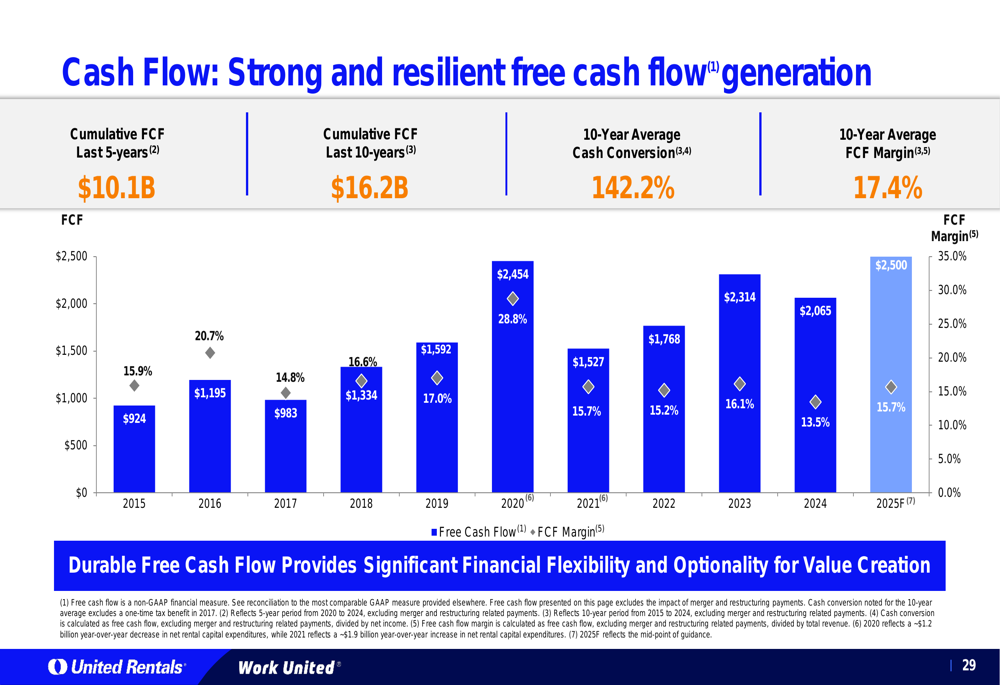

This financial discipline has enabled URI to generate substantial free cash flow, with cumulative FCF of $10.1 billion over the past five years and $16.2 billion over the past decade. The company forecasts $2.5 billion in free cash flow for 2025, representing a 15.7% FCF margin.

The strong cash flow generation is illustrated in the following chart:

United Rentals has maintained a balanced approach to capital allocation, focusing on organic growth investments, strategic M&A, dividends, and share repurchases. The company initiated a dividend program in 2023 and has increased its quarterly dividend to $1.79 per share in 2025, a 10% increase from 2024.

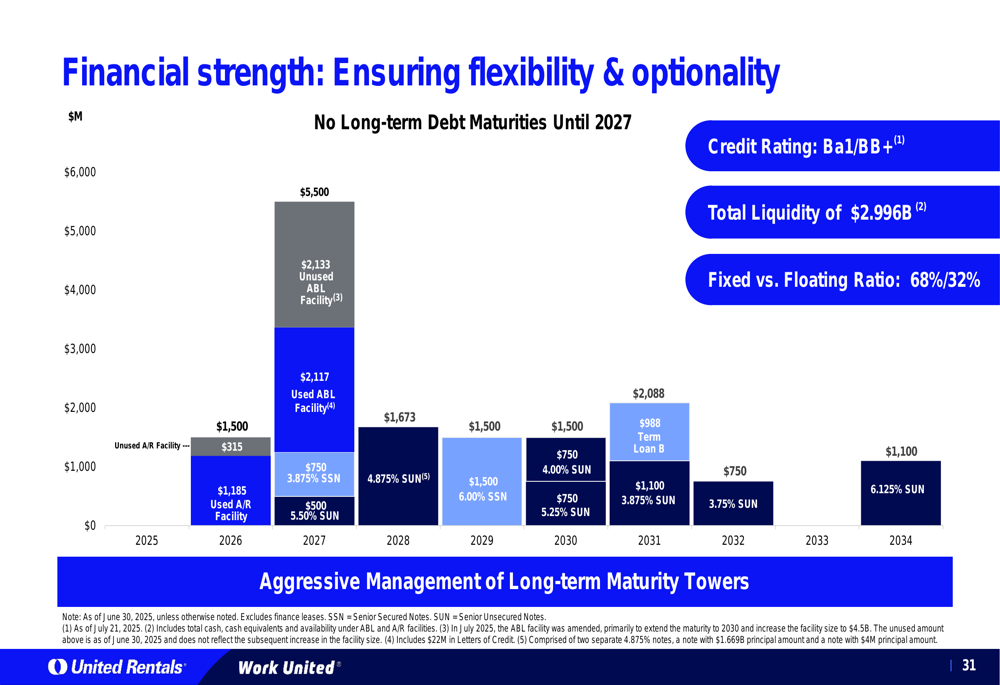

The company’s debt maturity schedule is well-managed, with no long-term debt maturities until 2027, providing financial flexibility for future investments and capital returns:

Forward-Looking Statements

Looking ahead, United Rentals remains focused on leveraging its competitive advantages to drive long-term value creation. The company reaffirmed its full-year 2025 guidance during its Q1 earnings call, anticipating continued double-digit growth in specialty rentals and steady fleet productivity.

URI’s strategy centers on balancing top-line growth, margin improvement, and prudent capital allocation. The company plans to continue investing in its specialty business, digital capabilities, and operational efficiency to maintain its market leadership position.

During the Q1 earnings call, CEO Matt Flannery emphasized the company’s commitment to being a reliable partner for its customers, while CFO Ted Grace highlighted URI’s strong financial position, noting that the balance sheet "remains in great shape, providing strong optionality for the business."

Despite its strong position, United Rentals faces potential challenges, including tariff impacts on equipment and parts, margin compression due to competitive pricing, local market softness in certain regions, and broader macroeconomic uncertainties that could impact overall demand.

Nevertheless, the company’s diverse end-market exposure, strong financial position, and strategic focus on high-growth specialty segments and digital transformation position it well to navigate these challenges and continue delivering value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.