Oil prices rise on talk of Russia sanctions; bouncing off recent lows

United Therapeutics Corporation (NASDAQ:UTHR) reported strong second-quarter 2025 financial results on July 30, with total revenue reaching $799 million, a 12% increase year-over-year. However, the stock was down 4.85% in premarket trading to $283.14, suggesting investors may have expected even stronger results or were concerned about specific aspects of the presentation.

Quarterly Performance Highlights

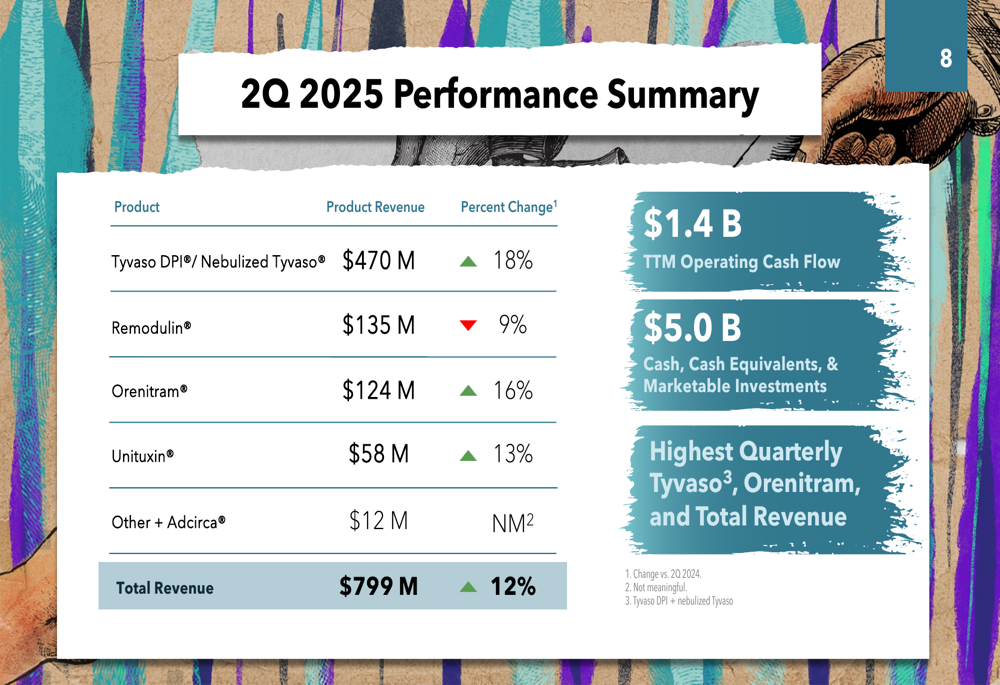

United Therapeutics delivered its highest-ever quarterly revenue, driven primarily by continued strong performance of its Tyvaso franchise. The company’s flagship product, Tyvaso DPI/Nebulized Tyvaso, generated $470 million in revenue, representing an 18% increase compared to the same period last year.

As shown in the following financial performance summary:

Other products in the portfolio showed mixed results. Orenitram posted $124 million in revenue (up 16% year-over-year) and Unituxin contributed $58 million (up 13%). However, Remodulin revenue declined by 9% to $135 million. The company highlighted its strong financial position with $5.0 billion in cash, cash equivalents, and marketable investments, and trailing twelve-month operating cash flow of $1.4 billion.

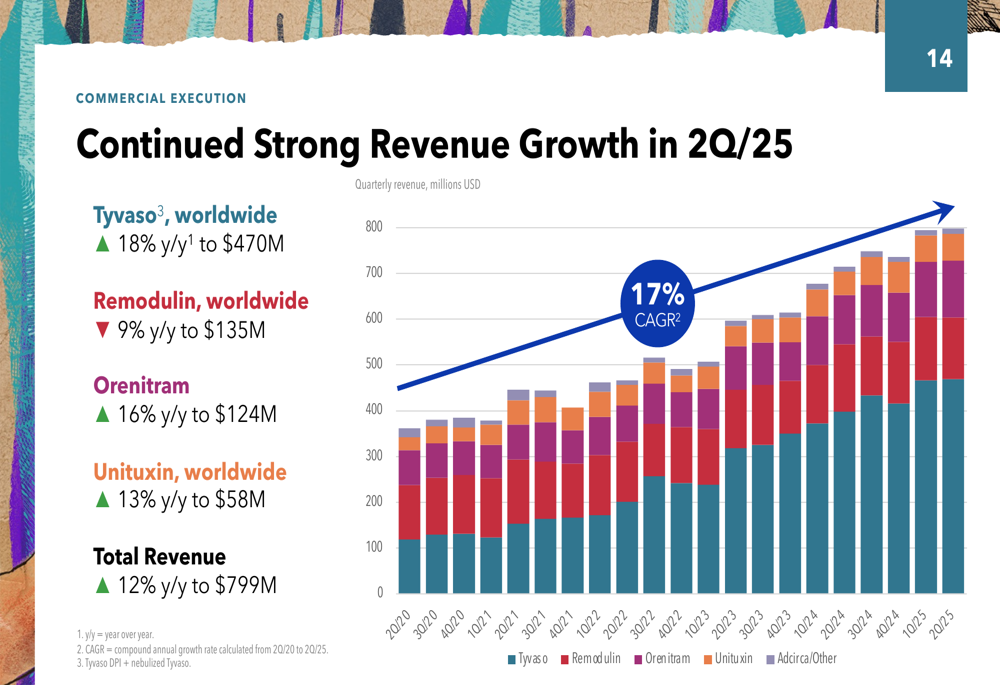

The quarterly revenue trend demonstrates consistent growth over time, particularly for the Tyvaso product line:

During the presentation, the company announced a $1.0 billion share repurchase authorization through March 31, 2026, citing its strong financial position, confidence in upcoming catalysts, and continued belief in its core business.

Strategic Growth Initiatives

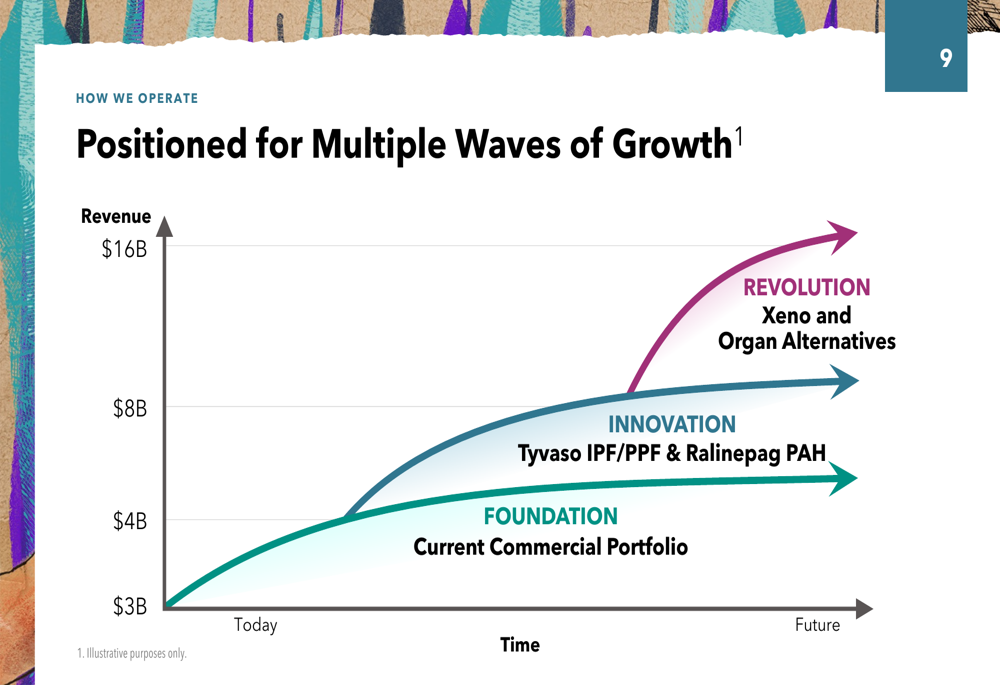

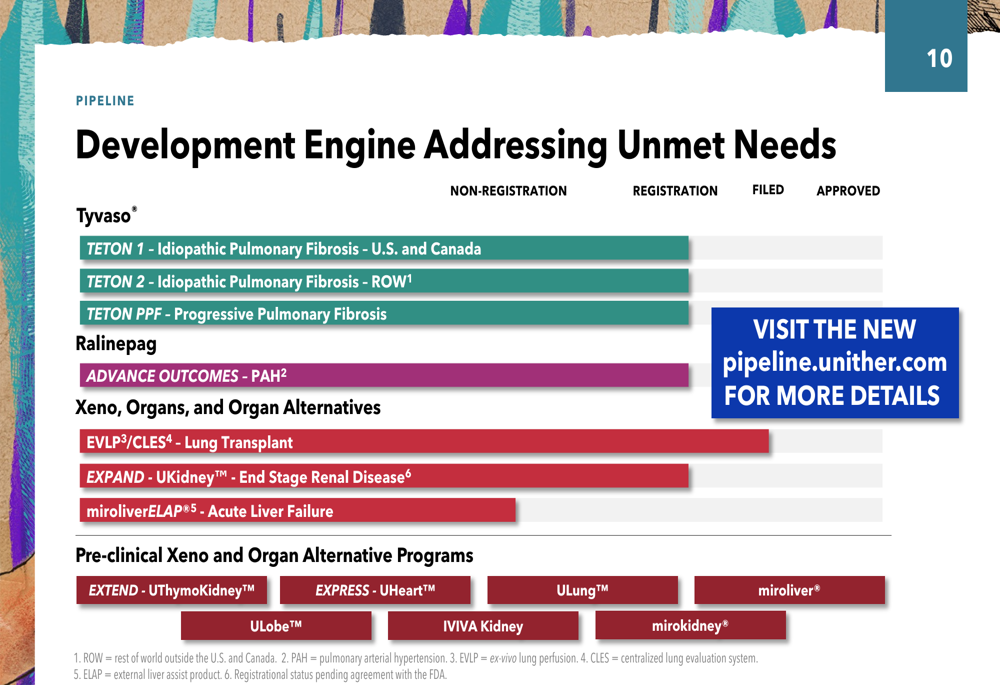

United Therapeutics outlined its growth strategy, which is divided into three distinct waves: Foundation (current commercial portfolio), Innovation (new indications including IPF/PPF), and Revolution (xenotransplantation and organ alternatives).

The company’s strategic roadmap illustrates how these initiatives are expected to drive future growth:

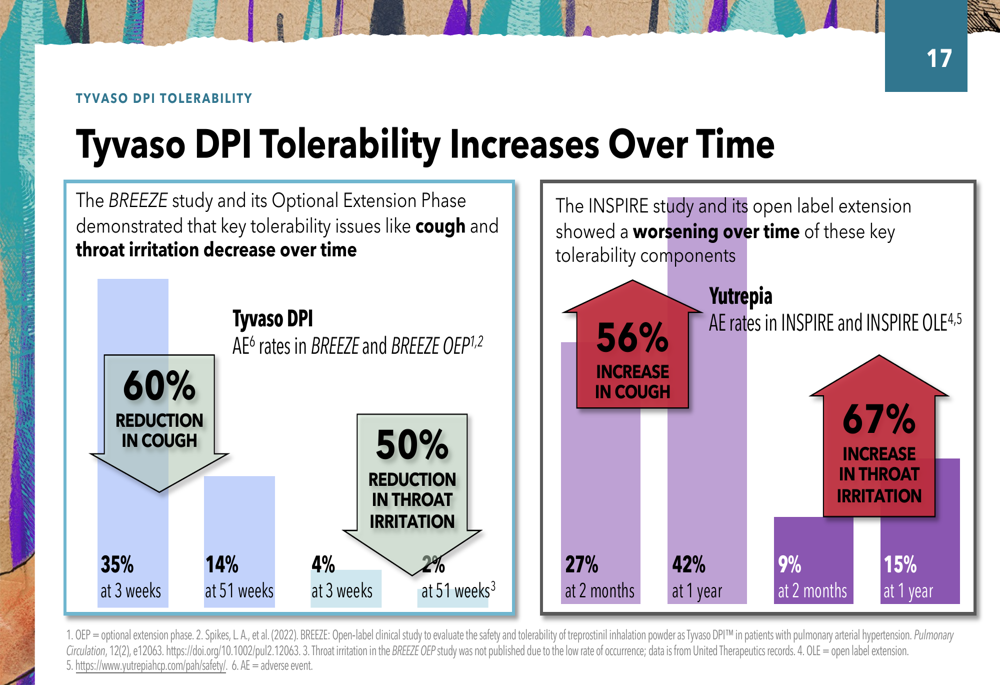

A key focus of the presentation was positioning Tyvaso DPI as superior to competing products, particularly Yutrepia. The company emphasized several advantages, including no maximum labeled dose, improved tolerability over time, optimal particle size for lung deposition, and ease of use.

The following chart demonstrates how Tyvaso DPI’s tolerability improves over time, in contrast to competing products:

Pipeline Development and IPF Opportunity (SO:FTCE11B)

United Therapeutics highlighted its robust development pipeline addressing multiple unmet needs across various therapeutic areas:

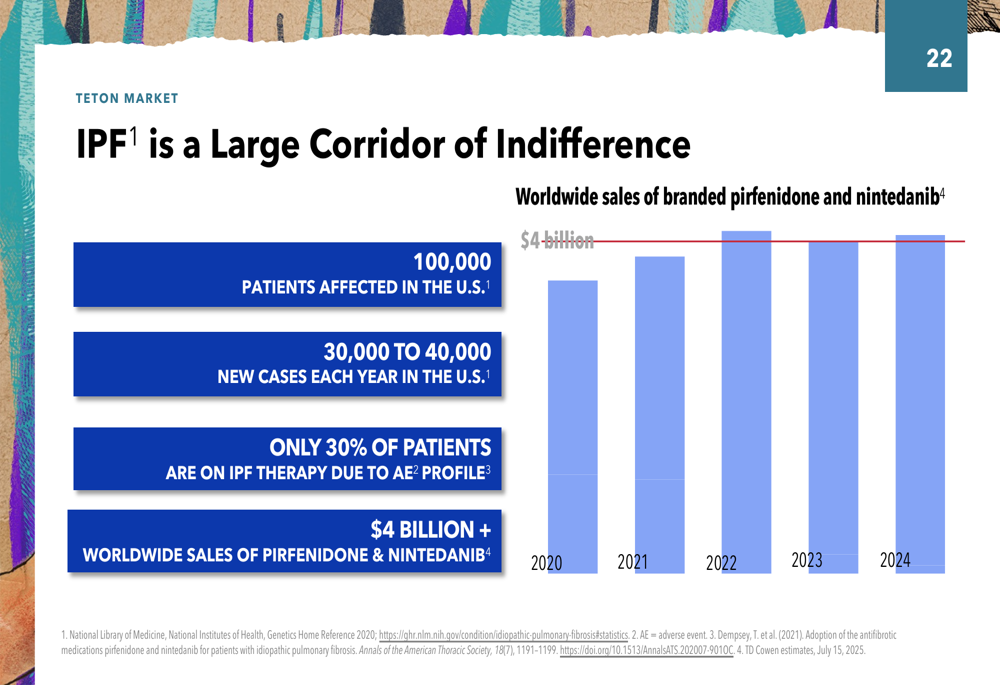

A significant focus of the presentation was the company’s pursuit of idiopathic pulmonary fibrosis (IPF) as a new indication for Tyvaso. Management characterized IPF as a "large corridor of indifference" with substantial market potential:

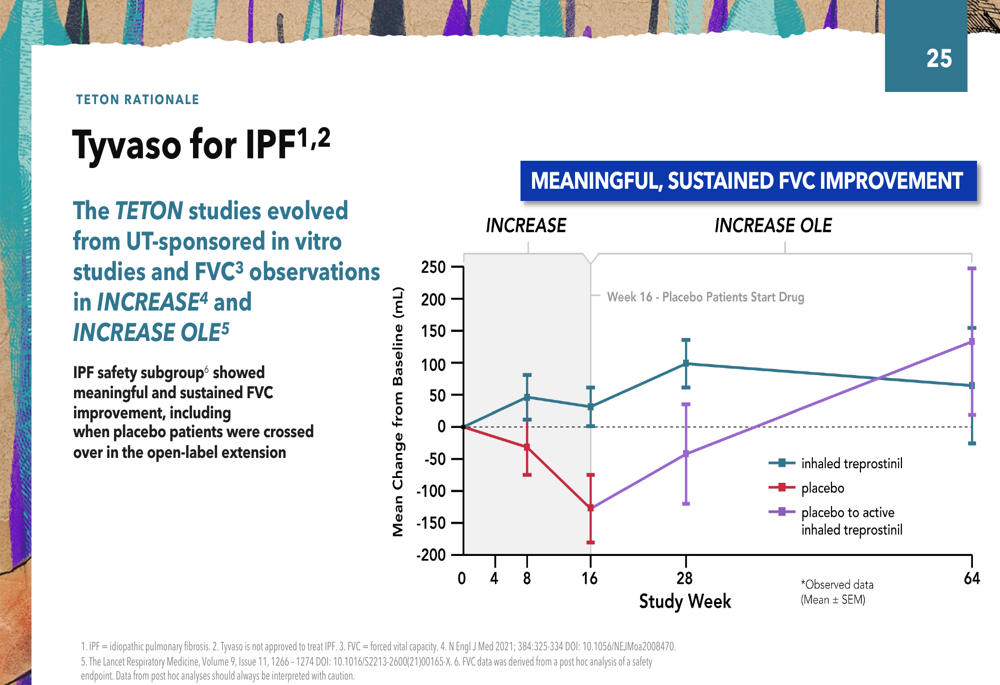

The company presented data suggesting that treprostinil, the active ingredient in Tyvaso, has antifibrotic properties that could provide meaningful benefits for IPF patients. Clinical observations from the INCREASE study showed sustained FVC (forced vital capacity) improvement, which is the basis for the ongoing TETON clinical program:

Development Timeline and Competitive Positioning

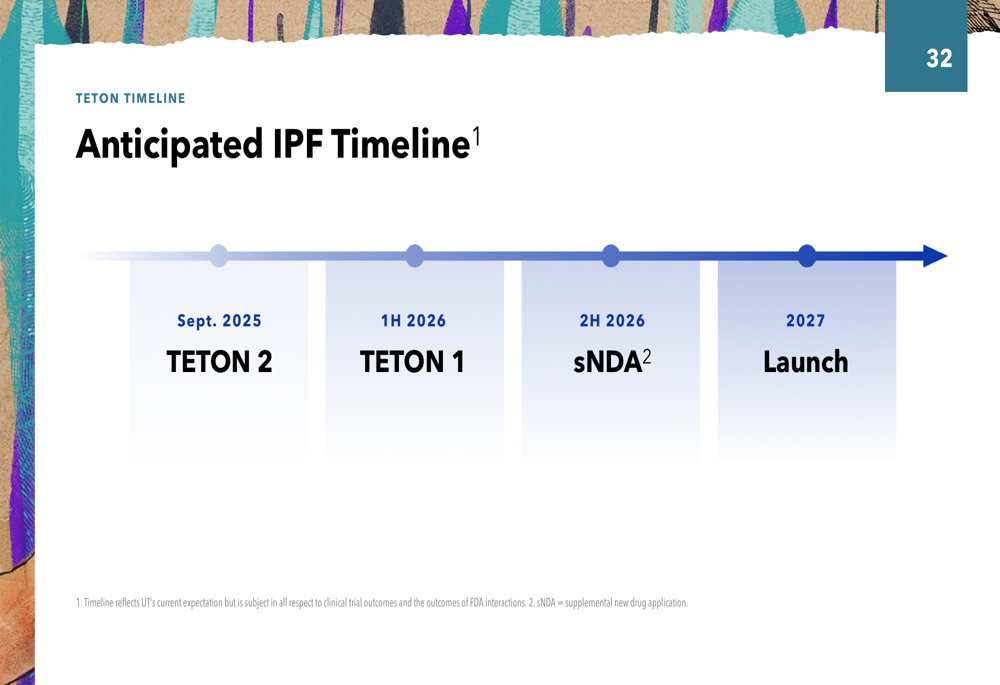

United Therapeutics outlined the anticipated timeline for its IPF program, with TETON 2 study results expected in September 2025, followed by TETON 1 results in the first half of 2026. The company plans to submit a supplemental new drug application (SNDA) in the second half of 2026, with potential launch in 2027:

The presentation included a critical assessment of competitor TPIP (treprostinil palmitil inhalation powder), suggesting its data may overstate its true potential due to imbalanced patient populations, aggressive statistical analysis, and lack of clarity in PH-ILD results. The company estimated that TPIP would not reach the market until 2029-2030, giving Tyvaso a potential first-mover advantage in the IPF indication.

Market Context and Outlook

The stock’s premarket decline of 4.85% contrasts with the positive financial results presented, suggesting investors may have concerns about specific aspects of the company’s strategy or competitive positioning. This reaction comes despite United Therapeutics trading at an attractive P/E ratio of 13x and maintaining gross profit margins of 89.24%, according to previous earnings reports.

Looking ahead, United Therapeutics expects to maintain its growth trajectory through continued expansion of its Tyvaso franchise, advancement of its pipeline candidates, and long-term development of its revolutionary organ manufacturing technologies. The company’s strong cash position provides significant flexibility for both internal development and potential strategic acquisitions.

The presentation reinforced United Therapeutics’ disciplined financial approach, consistent with CEO Martine Rothblatt’s previously stated philosophy: "We never spend more than 50% of prior year revenue on cash operating expenses." This strategy has enabled the company to invest in innovation while maintaining financial stability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.