Street Calls of the Week

Introduction & Market Context

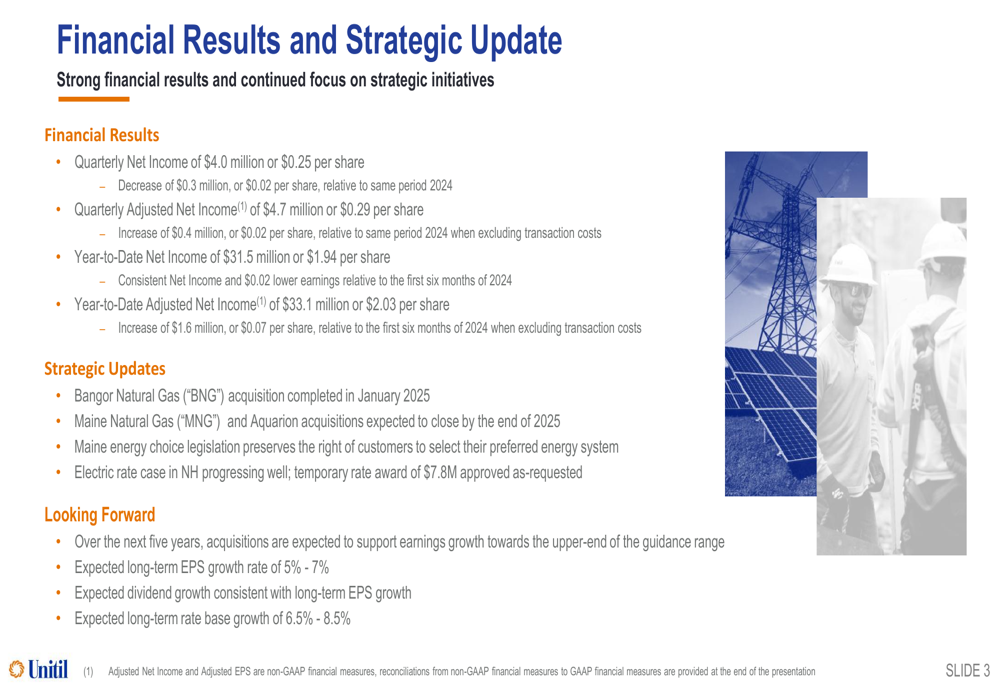

Unitil Corporation (NYSE:UTL) presented its Q2 2025 financial results and strategic update on August 5, 2025, highlighting its acquisition-driven growth strategy amid mixed quarterly performance. The utility company reported quarterly net income of $4.0 million ($0.25 per share), representing a slight decrease from the prior year, while maintaining its full-year earnings guidance.

The presentation comes after Unitil’s stock has experienced some volatility following its Q1 2025 results, when shares dropped 4.14% after slightly missing earnings expectations. The stock has since stabilized, closing at $52.13 on August 4, 2025, up 0.62% for the day, but still trading well below its 52-week high of $63.52.

As shown in the following comprehensive overview of Unitil’s financial results and strategic initiatives:

Quarterly Performance Highlights

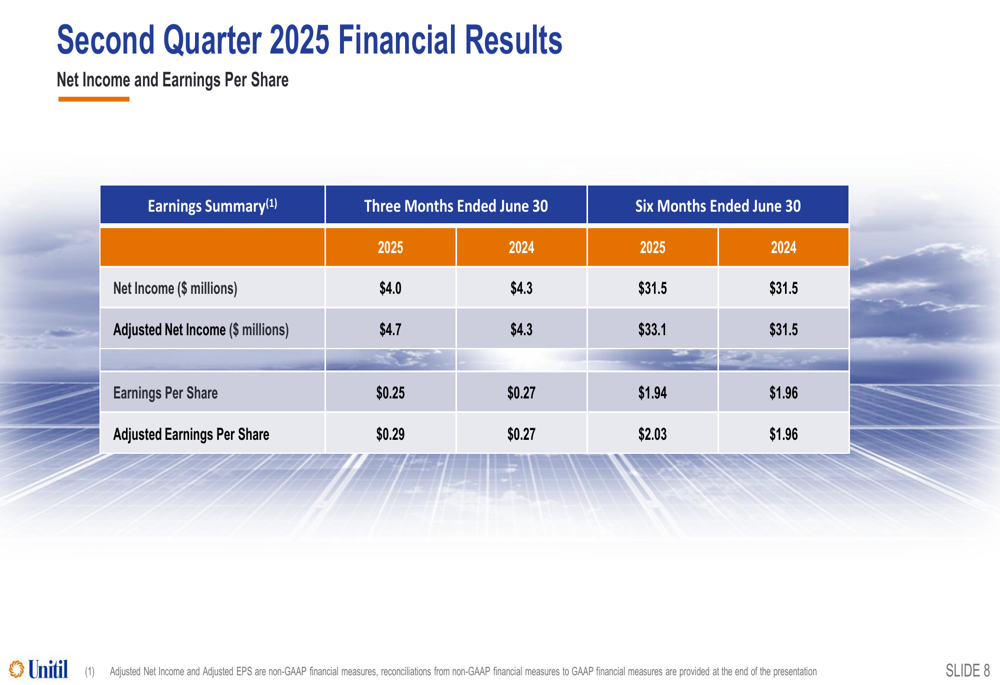

Unitil reported Q2 2025 net income of $4.0 million ($0.25 per share), down $0.3 million ($0.02 per share) compared to the same period last year. However, when excluding transaction costs related to acquisitions, adjusted net income reached $4.7 million ($0.29 per share), representing a $0.4 million ($0.02 per share) increase year-over-year.

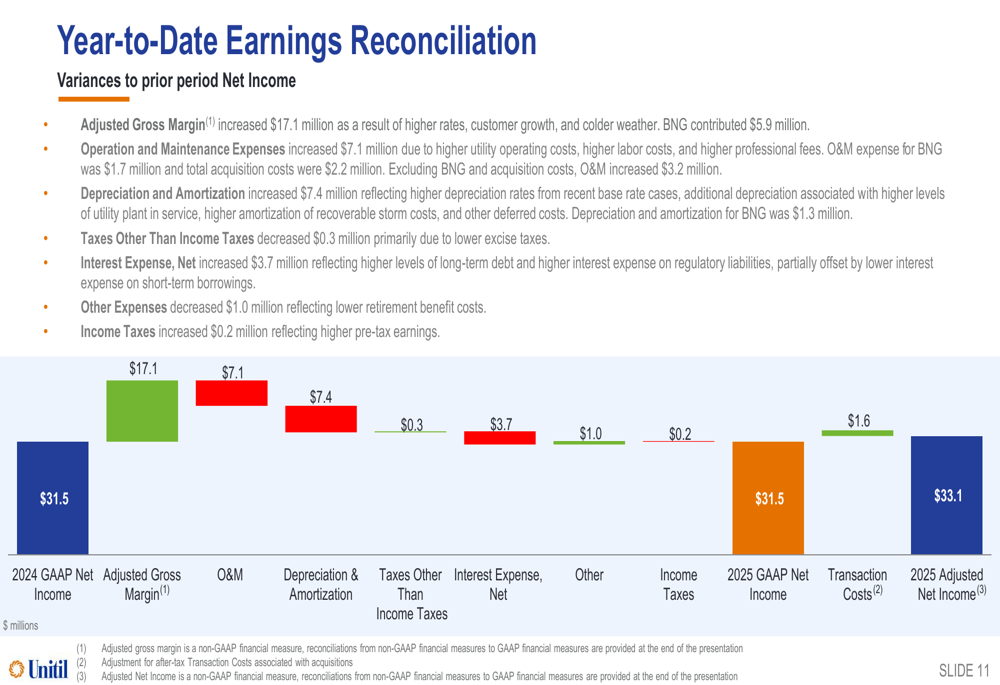

Year-to-date performance has been stronger, with net income of $31.5 million ($1.94 per share) and adjusted net income of $33.1 million ($2.03 per share), reflecting a $1.6 million ($0.07 per share) increase compared to the first half of 2024 when excluding transaction costs.

The detailed quarterly financial results are presented in the following table:

Strategic Initiatives

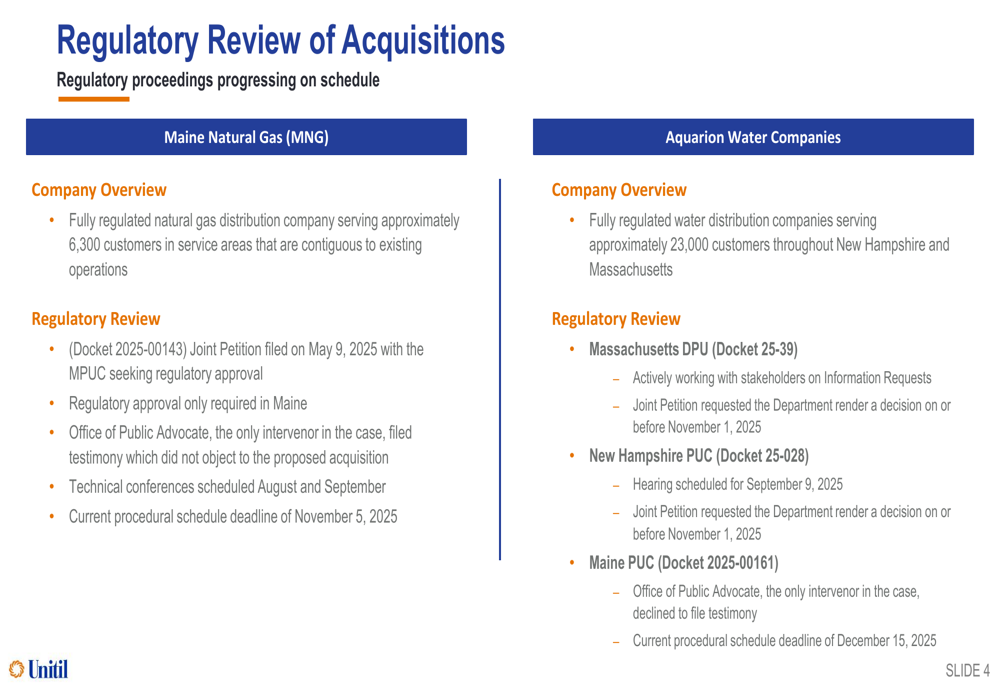

Unitil’s growth strategy centers on strategic acquisitions and infrastructure investments. The company completed the acquisition of Bangor Natural Gas (BNG) in January 2025 and expects to close the acquisitions of Maine Natural Gas (MNG) and Aquarion Water Companies by the end of 2025.

The regulatory review process for these acquisitions is progressing as planned. For Maine Natural Gas, a joint petition was filed with the Maine Public Utilities Commission in May 2025, with a procedural schedule deadline of November 5, 2025. The Aquarion Water Companies acquisition, which will add approximately 23,000 customers across New Hampshire and Massachusetts, is undergoing regulatory review in three states, with decisions expected by the end of 2025.

The following slide details the regulatory review process for these pending acquisitions:

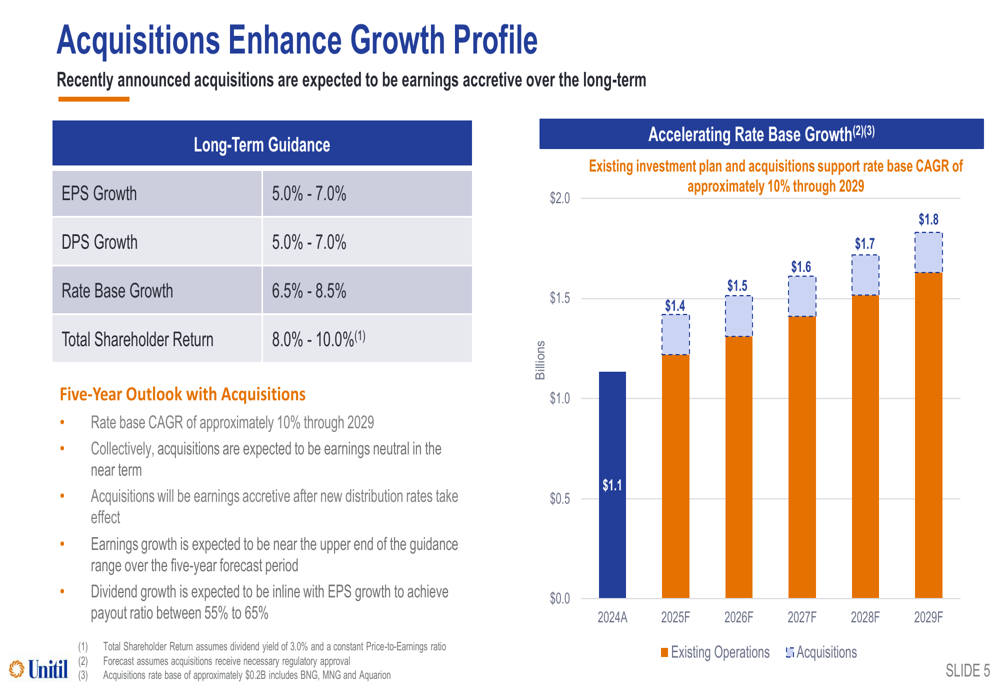

These acquisitions are expected to significantly enhance Unitil’s growth profile, with the company projecting a rate base CAGR of approximately 10% through 2029, substantially higher than its previous guidance of 6.5%-8.5%. While the acquisitions are expected to be earnings neutral in the near term, they should become accretive after new distribution rates take effect.

The accelerating rate base growth resulting from these acquisitions is illustrated in the following chart:

Detailed Financial Analysis

Unitil’s financial performance varied by segment. Electric operations showed modest growth, with adjusted gross margin increasing by 2.5%, weather-normalized unit sales up 0.9%, and customer count rising by 0.7%. The company noted that 100% of electric customers are now decoupled, providing revenue stability regardless of consumption patterns.

Gas operations demonstrated stronger performance, with adjusted gross margin increasing by 17.1%, weather-normalized unit sales up 19.9%, and customer count growing by 10.7%, including 8,800 customers from the BNG acquisition. The company highlighted that 55% of gas customers are now decoupled.

The following waterfall chart breaks down the year-to-date earnings reconciliation, showing the key factors affecting performance:

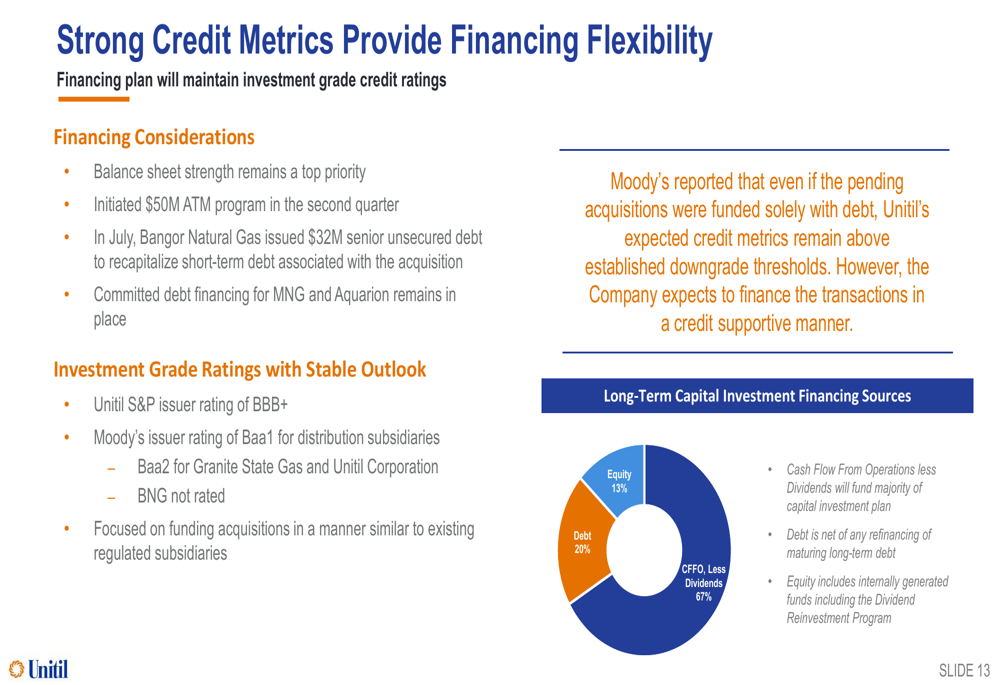

Unitil has maintained strong credit metrics despite its acquisition activity. The company initiated a $50 million ATM program in the second quarter and secured $32 million in senior unsecured debt for Bangor Natural Gas in July. Committed debt financing for the MNG and Aquarion acquisitions remains in place. Moody’s has indicated that even if the pending acquisitions were funded solely with debt, Unitil’s expected credit metrics would remain above established downgrade thresholds.

The following slide details the company’s credit metrics and financing flexibility:

Forward-Looking Statements

Unitil reaffirmed its 2025 earnings guidance range of $3.01 to $3.17 per share, with a midpoint of $3.09, representing a 6.1% annual growth rate since 2022. The company expects a net loss in the third quarter of 2025, consistent with its typical seasonal earnings pattern, with more than 50% of annual earnings typically occurring in the first quarter.

Looking beyond 2025, Unitil projects long-term EPS growth of 5%-7%, dividend growth consistent with EPS growth, and rate base growth of 6.5%-8.5% before accounting for acquisitions. With acquisitions included, the rate base CAGR is expected to reach approximately 10% through 2029.

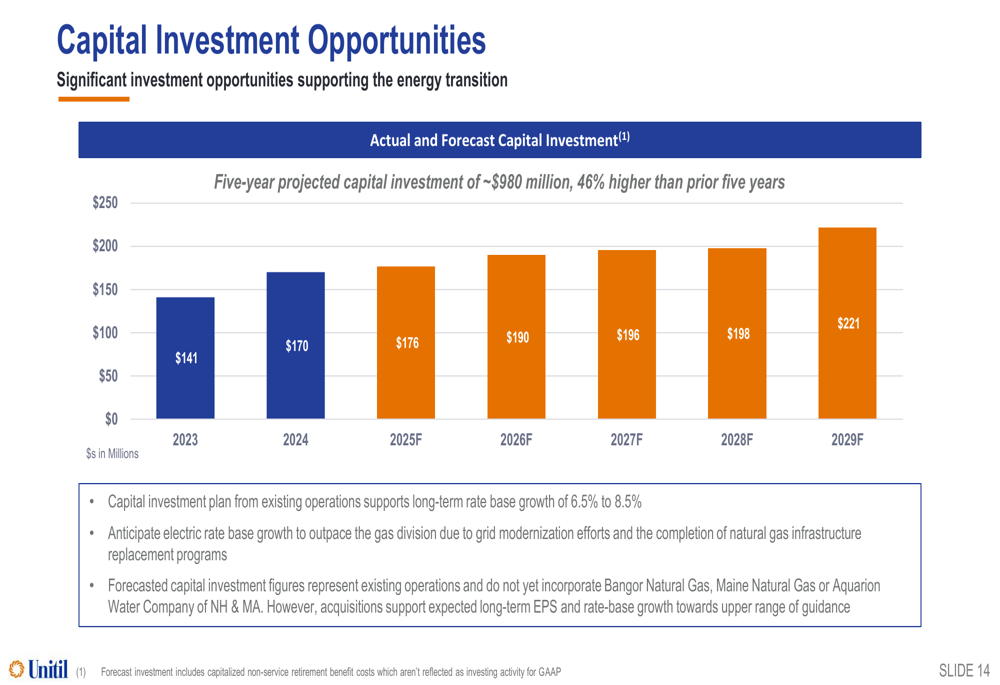

The company’s five-year capital investment plan totals approximately $980 million, 46% higher than the previous five-year period. This plan supports grid modernization efforts and clean energy transition initiatives, including the recently completed 5 MW Kingston Solar Project in New Hampshire.

The following chart illustrates Unitil’s projected capital investments through 2029:

Unitil’s growth strategy is supported by favorable regulatory environments in its service territories. Maine recently became the 27th state to pass fuel choice legislation, preserving consumers’ rights to select their preferred energy systems. This legislation, combined with the cost advantage of natural gas over competing fuels like oil and propane, provides long-term growth opportunities for Unitil’s gas operations, particularly given the low penetration rates in Maine and New Hampshire.

In conclusion, while Unitil’s Q2 2025 results showed modest quarterly performance, the company’s strategic acquisitions and capital investment plans position it for accelerated growth in the coming years. The successful integration of these acquisitions and favorable regulatory outcomes will be critical factors in achieving the projected 10% rate base growth through 2029 and the associated earnings growth targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.