Oil prices rebound sharply on smaller-than-feared OPEC+ output hike

Introduction & Market Context

Unum Group (NYSE:UNM) shares plunged over 10% in regular trading on Wednesday after the release of its second quarter 2025 statistical supplement, with premarket trading showing an even steeper decline of 13.49%. The significant market reaction follows a quarter that delivered mixed results, continuing a challenging trend after the company missed analyst expectations in Q1 2025.

The insurance provider’s stock traded at $72.51, well below its 52-week high of $84.48, as investors responded to financial results that showed premium growth but declining profits. This marks the second consecutive quarter of disappointing performance, with the company having missed both revenue and EPS forecasts in the first quarter.

Quarterly Performance Highlights

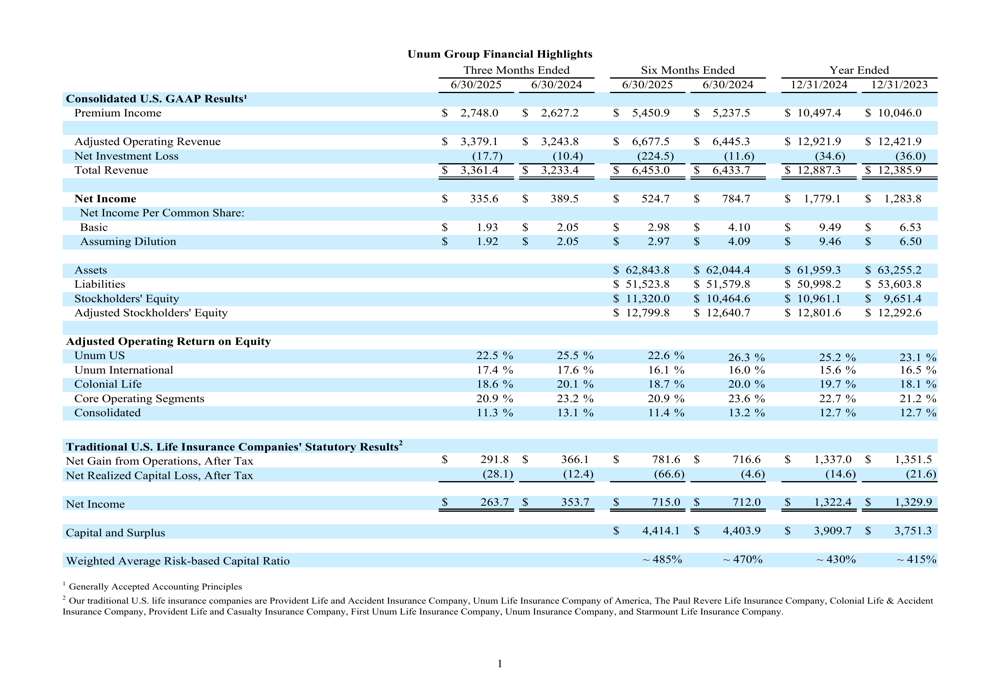

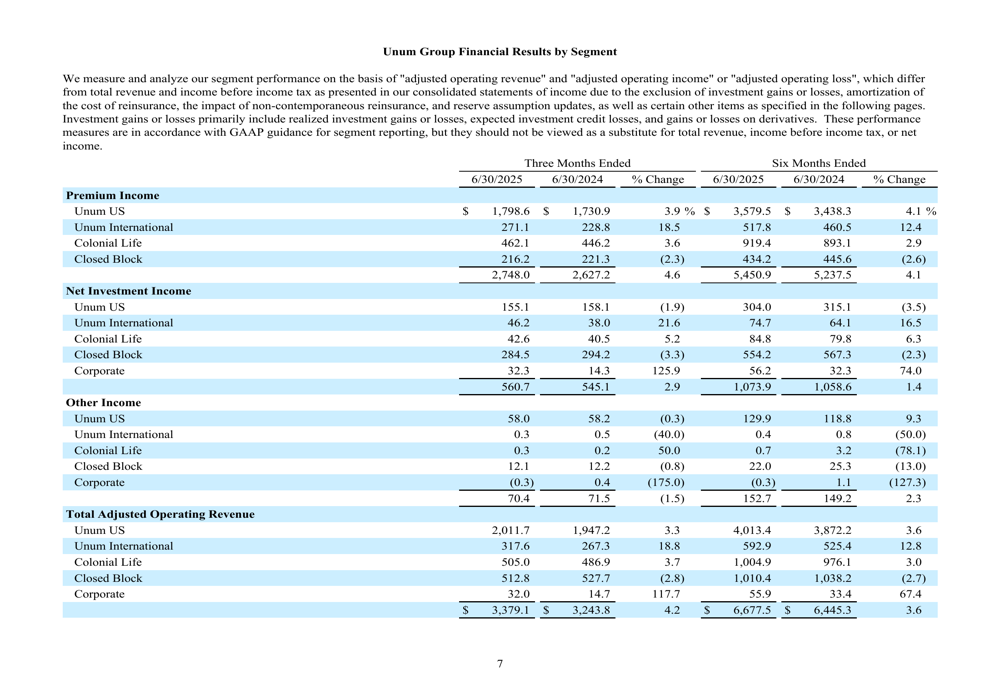

According to Unum’s Q2 2025 statistical supplement, the company reported premium income of $2,748.0 million for the three months ended June 30, 2025, representing a 4.6% increase from $2,627.2 million in the same period of 2024. However, net income declined to $335.6 million, down 13.8% from $389.5 million in Q2 2024.

As shown in the following financial highlights table:

The company maintained a solid capital position with total stockholders’ equity of $11,320.0 million as of June 30, 2025, compared to $10,961.1 million at the end of 2024. Total (EPA:TTEF) assets grew modestly to $62,843.8 million from $61,959.3 million over the same period.

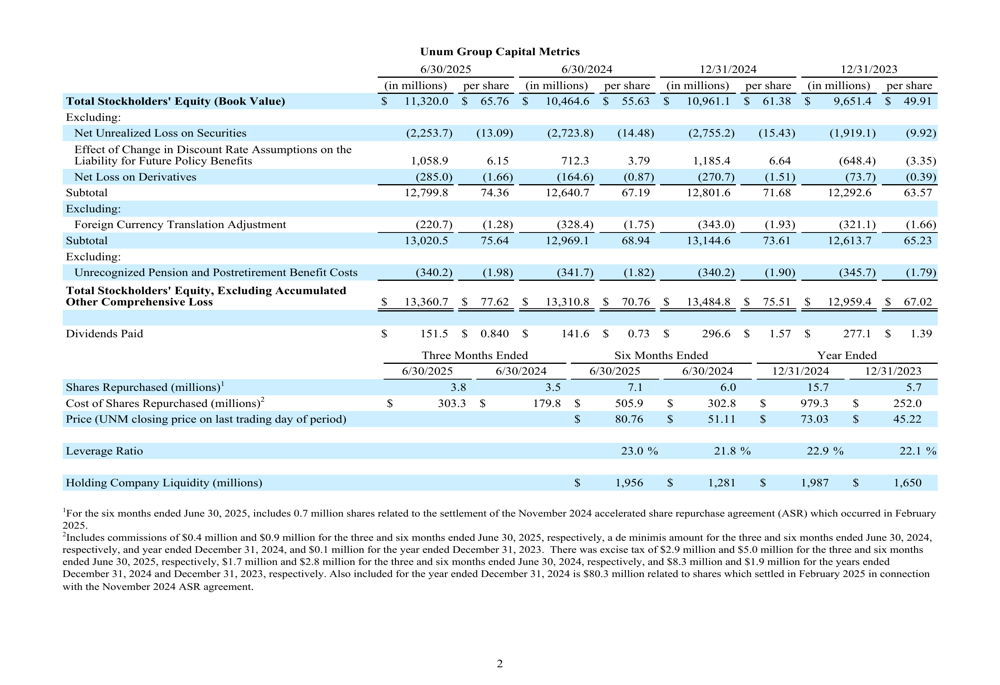

Unum’s capital metrics reveal a closing stock price of $80.76 on the last trading day of the period, though this figure has since declined substantially following the earnings release:

Segment Analysis

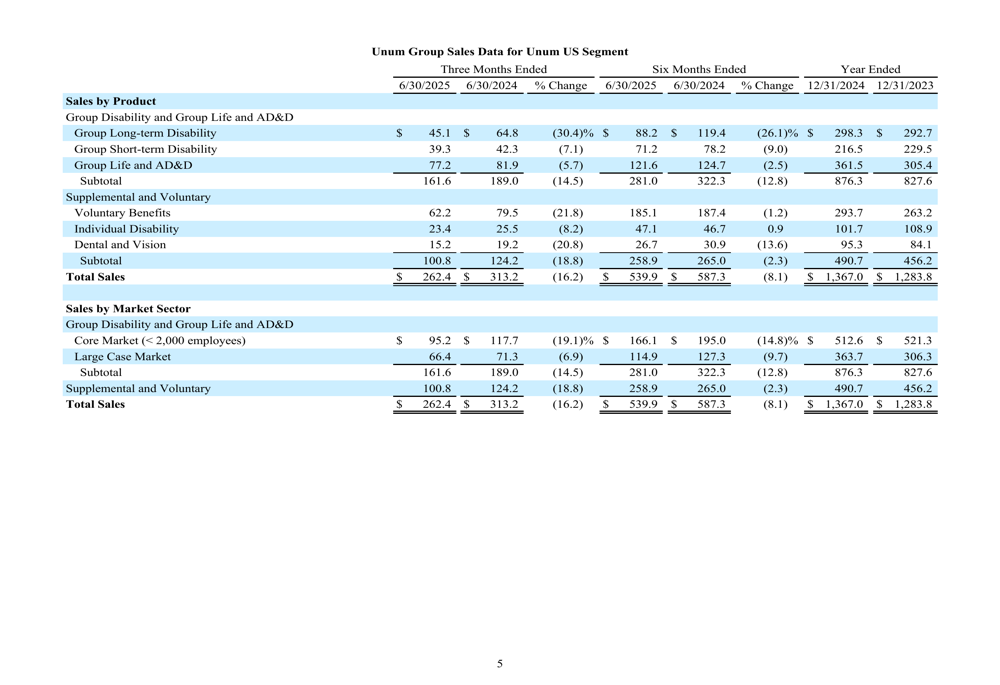

Performance across Unum’s business segments showed considerable variation. The Unum US segment, which represents the company’s largest business unit, reported total sales of $262.4 million for Q2 2025, a significant 16.2% decline from $313.2 million in Q2 2024. This weakness was particularly evident in the group disability and life insurance products.

The following table details the sales performance across Unum US products and market sectors:

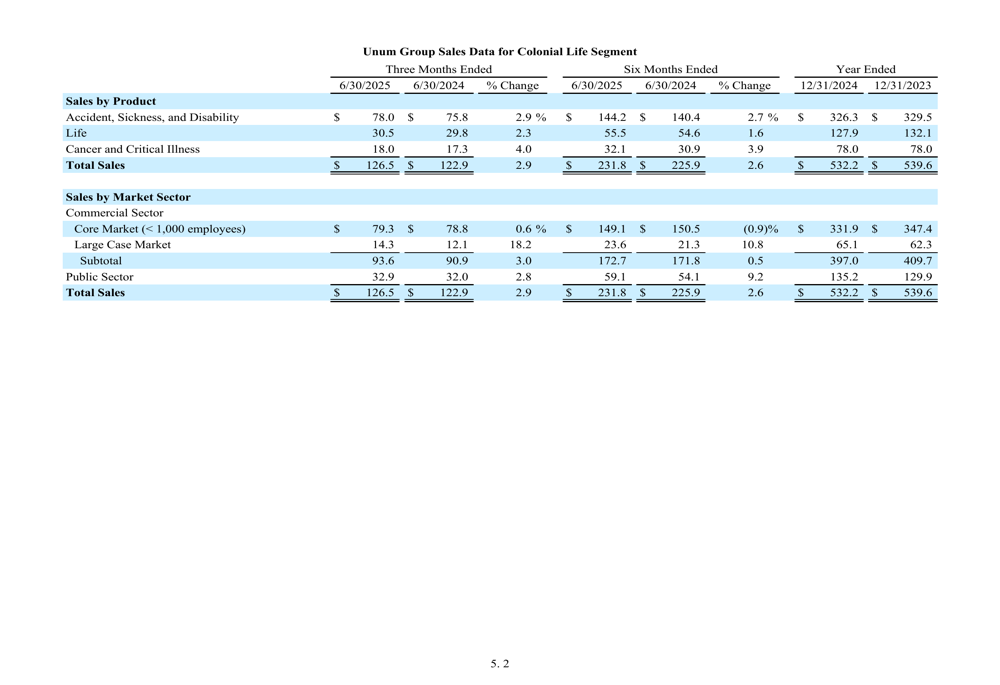

In contrast, the Colonial Life segment demonstrated modest growth, with total sales reaching $126.5 million in Q2 2025, up 2.9% from $122.9 million in the same period last year. This segment’s resilience provided some offset to the weakness in the core Unum US business.

The Colonial Life segment’s sales breakdown by product and market sector shows:

The Unum International segment, which includes operations in the UK and Poland, showed mixed results. While the earnings article from Q1 had highlighted growth in Poland as a bright spot, the overall international segment appears to have delivered inconsistent performance across markets and products.

Investment Portfolio & Capital Position

Unum maintained a diversified investment portfolio with a focus on fixed maturity securities, which comprised the majority of its investments. The company reported an earned book yield of 4.47% and an average duration of 8.17 years, reflecting a conservative investment approach designed to match long-term liabilities.

The investment portfolio composition as of June 30, 2025, is illustrated below:

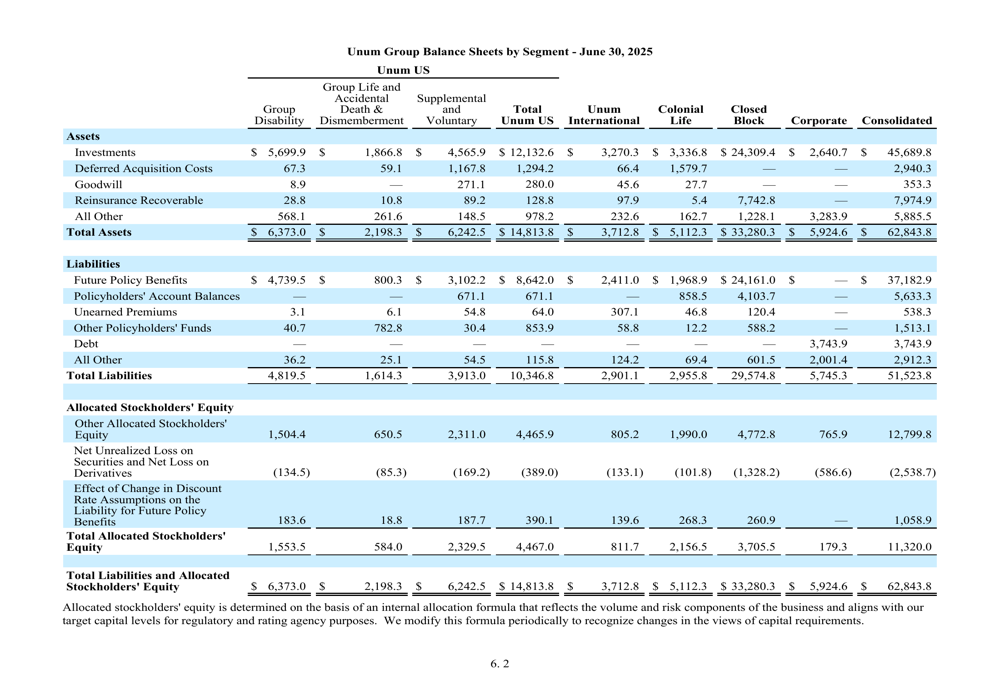

The company’s balance sheet by segment shows how assets, liabilities, and allocated stockholders’ equity are distributed across business units:

Unum continues to maintain strong ratings from major agencies, with financial strength ratings of A (Excellent) from AM Best, A (Strong) from Fitch, A2 (Good) from Moody’s, and A (Strong) from S&P for its major insurance subsidiaries. These ratings reflect the company’s solid capital position despite recent earnings challenges.

Forward Outlook

The significant stock price decline following the Q2 2025 results suggests investors are concerned about Unum’s near-term growth prospects. This reaction follows a challenging first quarter, where the company missed analyst expectations with an EPS of $2.04 against a forecast of $2.18 and revenue of $3.09 billion versus an expected $3.34 billion.

The consecutive quarters of underperformance raise questions about the company’s previously stated full-year guidance of 5-10% sales growth. While premium income has grown, the decline in net income and mixed sales performance across segments may indicate ongoing operational challenges.

Unum’s balance sheet remains strong, with total stockholders’ equity growing to $11,320.0 million as of June 30, 2025. This solid capital foundation, combined with the company’s track record of 16 consecutive years of dividend increases (as noted in the Q1 earnings report), may provide some reassurance to long-term investors despite the current volatility.

However, with the stock now trading significantly below its 52-week high, market sentiment appears cautious as investors await more clarity on whether the company can reverse the trend of declining profits and uneven segment performance in the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.