Street Calls of the Week

Introduction & Market Context

Upwork Inc. (NASDAQ:UPWK) released its Q1 2025 investor presentation on May 5, highlighting record profitability metrics despite modest revenue growth. The freelance marketplace platform’s stock surged 11.26% in after-hours trading to $14.82, following the announcement of strong financial results that exceeded analyst expectations.

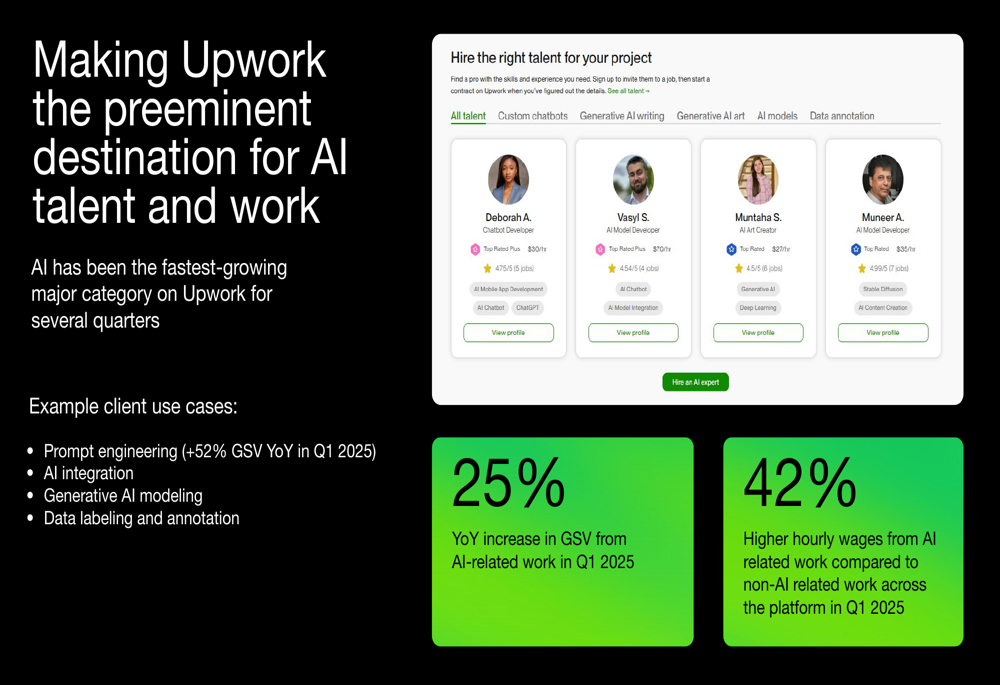

The presentation emphasized how artificial intelligence is reshaping the work landscape, with Upwork positioning itself as the premier destination for AI talent. The company outlined how traditional hiring models lack flexibility and speed, while most organizations struggle with acquiring critical AI talent in-house amid ongoing budget pressures.

Quarterly Performance Highlights

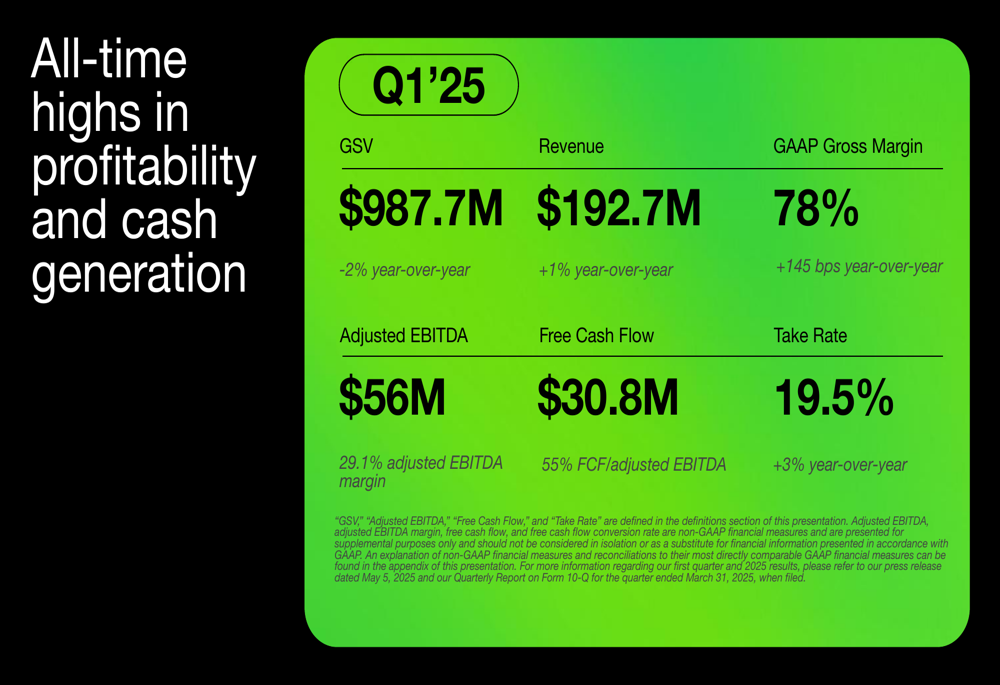

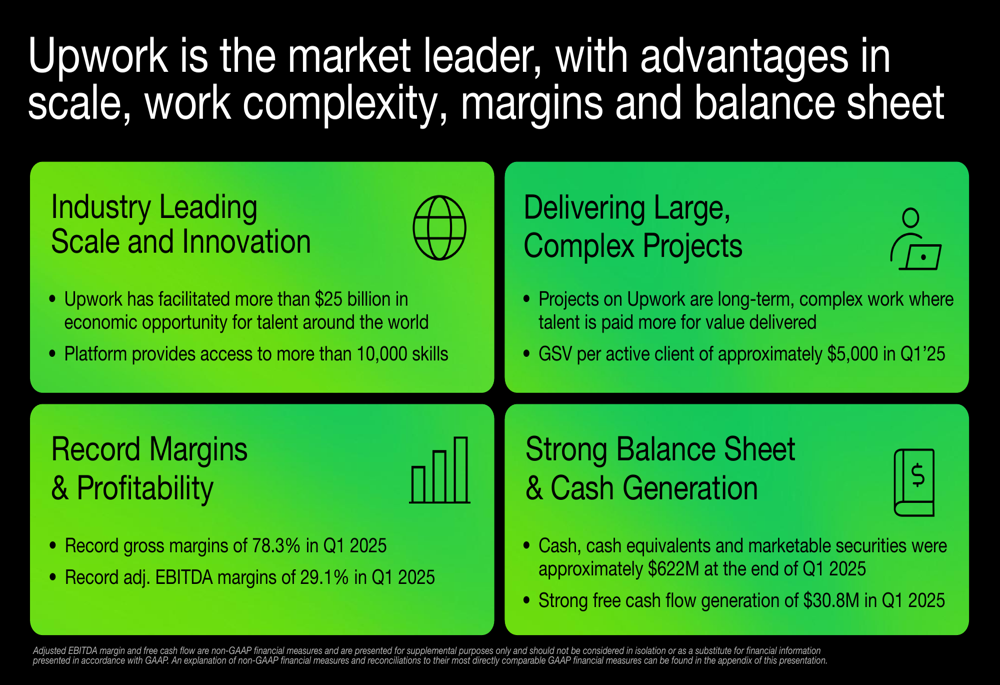

Upwork reported Q1 2025 revenue of $192.7 million, representing a 1% year-over-year increase, while achieving all-time highs in profitability metrics. The company’s gross margin reached a record 78.3%, expanding 145 basis points compared to the same period last year.

As shown in the following financial performance summary:

Adjusted EBITDA reached $56 million with a 29.1% margin, while free cash flow generation more than doubled year-over-year to $30.8 million. The company’s take rate improved to 19.5%, a 3% increase from Q1 2024, though Gross Services Volume (GSV) declined slightly by 2% to $987.7 million.

"Upwork is becoming the critical infrastructure for enabling the combination of humans and AI to work together," said CEO Hayden Brown, according to the earnings call transcript.

AI Strategy and Growth

Upwork’s presentation highlighted AI as its fastest-growing major category, with AI-related work increasing 25% year-over-year in Q1 2025. The company noted that AI roles command a 42% premium in hourly wages compared to non-AI work across the platform, with prompt engineering specifically growing 52% in GSV year-over-year.

The following slide illustrates Upwork’s positioning in the AI talent market:

In April 2024, Upwork launched Uma™, its "Mindful AI" conversational work companion designed to improve customer productivity. The company reported that Uma-powered features have significantly boosted engagement, with the Uma Proposal Writer increasing engagement by 58% and Uma on Upwork’s homepage driving a 340% increase in user engagement.

Upwork also strengthened its AI capabilities through strategic acquisitions, including Objective in Q4 2024, which brought AI-native search technology to enhance core search, match, and discovery performance across both marketplace and enterprise offerings.

Enterprise and Monetization Initiatives

Beyond AI, Upwork outlined two additional growth catalysts: Enterprise expansion and Ads & Monetization. The company is targeting the global enterprise staffing market, which it estimates at over $650 billion, through a targeted approach with custom solutions for large clients.

The company introduced its Business Plus plan in Q4 2024, providing an enterprise-like value proposition at a premium price point. Enterprise revenues reached $26.4 million in Q1 2025, benefiting from increased spend per contract.

Upwork’s monetization strategy has become one of its fastest-growing revenue streams, contributing to the company’s take rate expansion. Products in this category include Boosted Profiles, Featured Jobs, Boosted Proposals, Connects Purchases, and Client & Talent Subscriptions.

Financial Outlook and Shareholder Returns

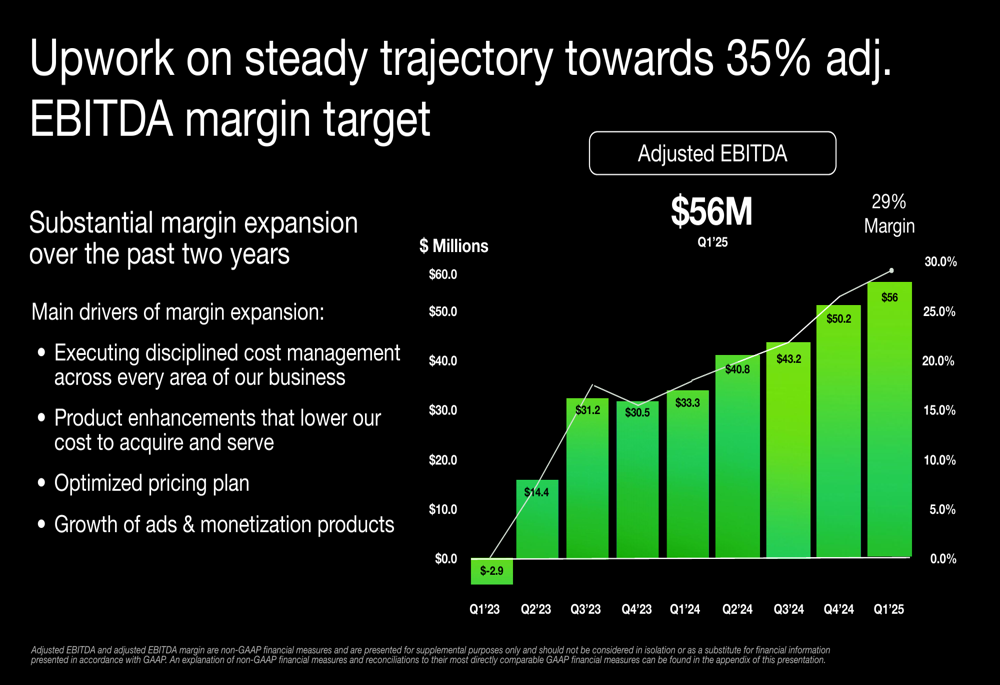

Upwork’s presentation highlighted its trajectory toward a 35% adjusted EBITDA margin target, showing substantial progress over the past two years as illustrated in this chart:

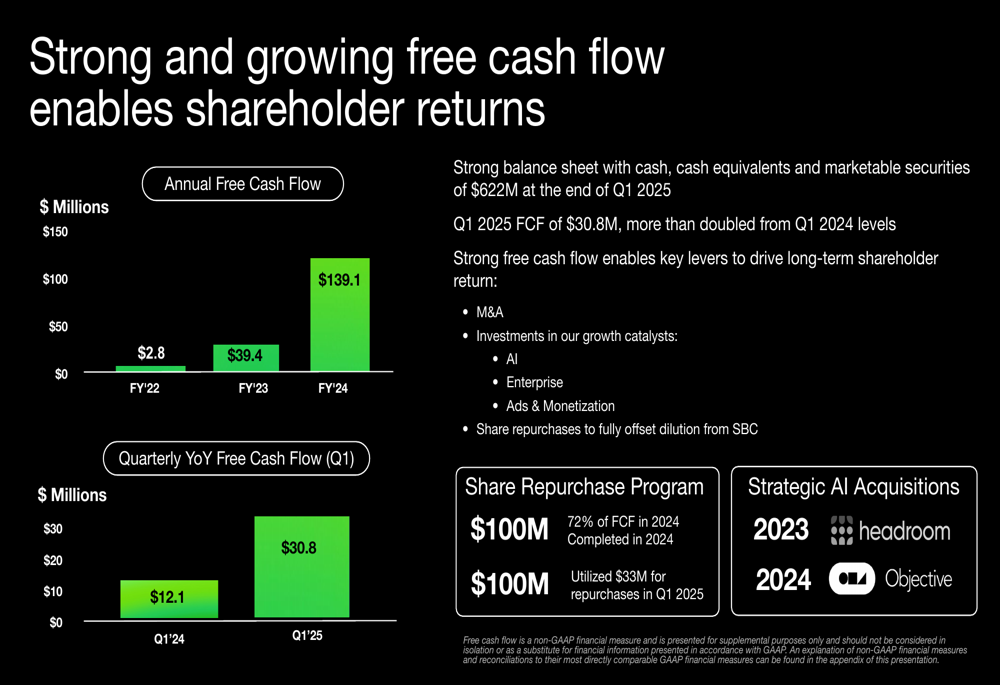

The company maintains a strong balance sheet with $622 million in cash, cash equivalents, and marketable securities at the end of Q1 2025. This financial position enables strategic investments in growth catalysts while returning value to shareholders through share repurchases.

As shown in the following slide on cash flow and shareholder returns:

Upwork completed 72% of its share repurchase program in 2024 using $100 million and utilized an additional $33 million for repurchases in Q1 2025. For the full year 2025, the company has set its revenue guidance between $740 and $760 million, with adjusted EBITDA expected to range from $190 to $200 million.

"It’s in times like these that the strongest, most resilient businesses stand out," noted CFO Erica Gessert during the earnings call, emphasizing the company’s focus on profitable growth despite macroeconomic pressures in the contingent labor market.

Upwork’s leadership advantages in scale, work complexity, margins, and balance sheet strength are summarized in this comprehensive overview:

While the company faces challenges including macro pressures in the labor market and competitive pressures in the freelance marketplace, its strategic focus on AI talent acquisition, enterprise expansion, and monetization initiatives positions it for potential growth reacceleration in 2026, according to management guidance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.