Intel stock extends gains after report of possible U.S. government stake

Introduction & Market Context

Urban Outfitters, Inc. (NASDAQ:URBN) delivered exceptional first-quarter results for fiscal year 2026, significantly exceeding analyst expectations with record earnings. The company’s diverse brand portfolio and multi-channel strategy continue to drive growth despite broader retail sector challenges. Following the earnings announcement on May 21, 2025, URBN’s stock surged 17.45% in after-hours trading, reaching $70.00, well above its 52-week high of $63.21.

The company’s presentation revealed strong performance across all business segments, with particularly impressive growth in its Nuuly subscription service, highlighting the success of URBN’s diversified business model in capturing evolving consumer preferences.

Quarterly Performance Highlights

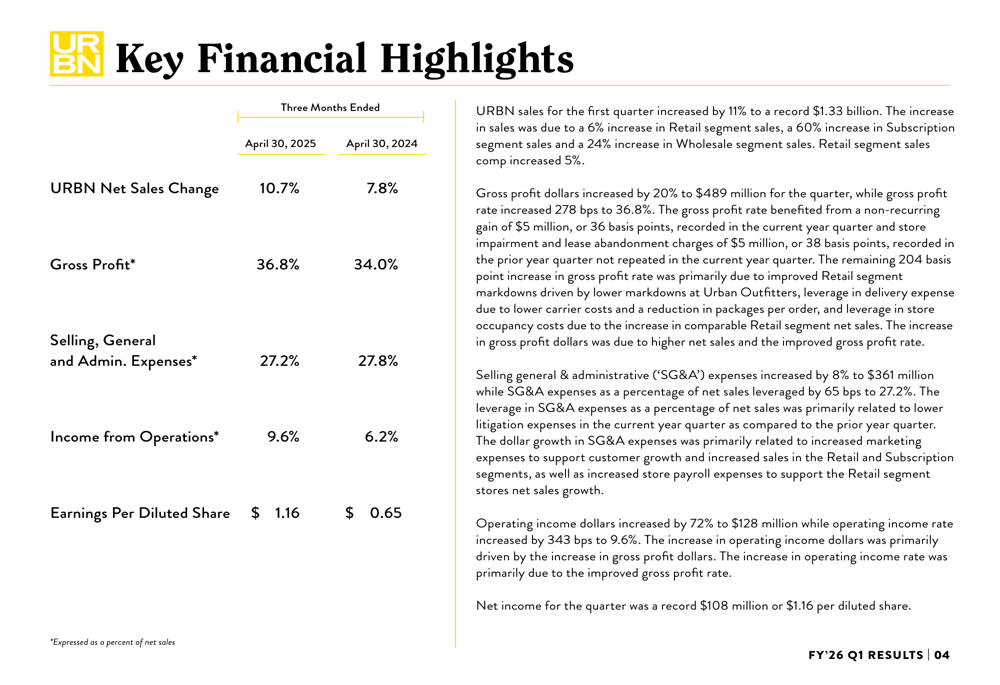

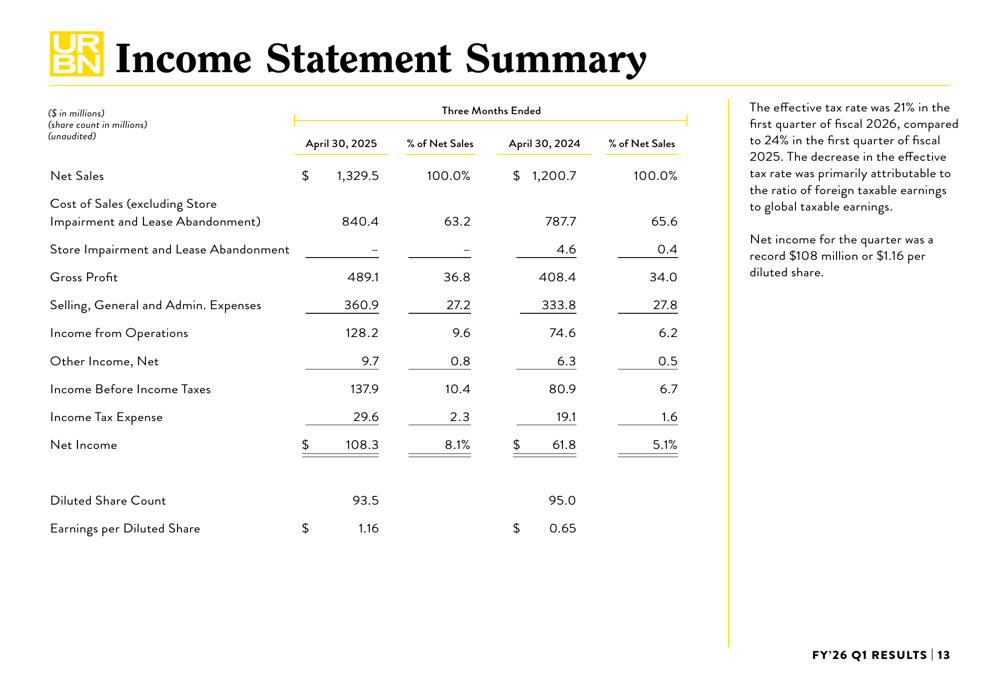

Urban Outfitters reported substantial growth in key financial metrics for Q1 FY’26, with total sales increasing 10.7% year-over-year to $1.33 billion. The company achieved a record earnings per diluted share of $1.16, representing a 78% increase from $0.65 in the prior year period.

As shown in the following key financial highlights:

The company’s gross profit margin expanded significantly to 36.8% from 34.0% in the prior year, driven primarily by reduced markdowns at Urban Outfitters and leveraged expenses. Operating income saw an even more dramatic improvement, increasing to 9.6% of net sales from 6.2% in the prior year quarter.

SG&A expenses as a percentage of sales decreased to 27.2% from 27.8%, despite an 8% increase in dollar terms to $360.9 million. This improvement was primarily related to lower litigation expenses compared to the prior year quarter, demonstrating effective cost management while supporting growth initiatives.

Segment Analysis

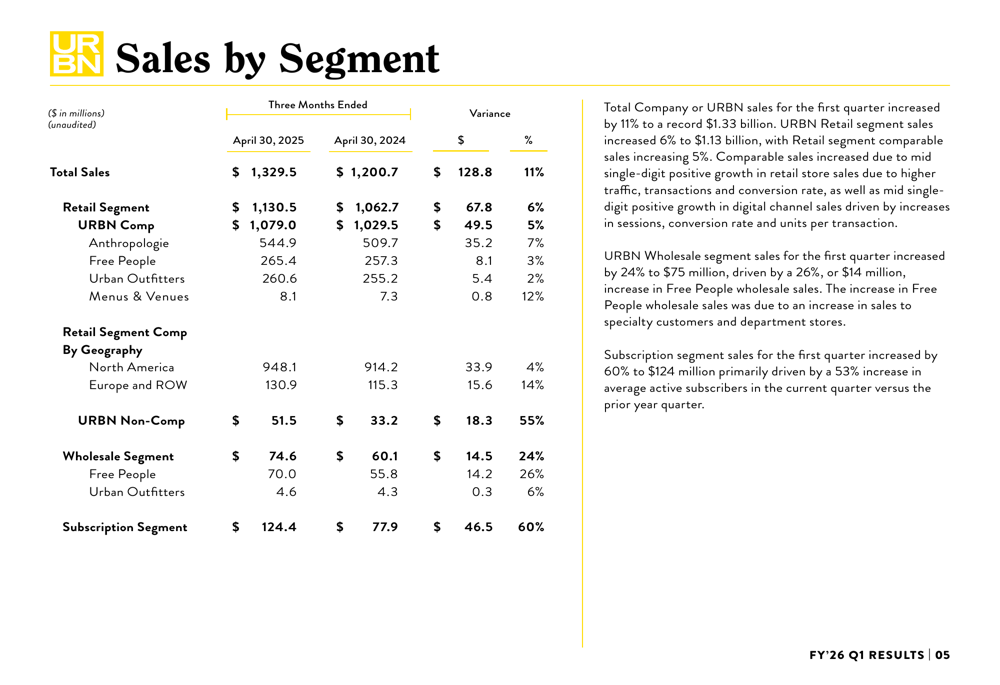

Urban Outfitters’ performance was strong across all three business segments – retail, wholesale, and subscription. The retail segment, which represents the largest portion of the business, grew by 6% to $1.13 billion with comparable sales increasing 5%.

The breakdown of sales by segment reveals the diverse growth drivers within the company:

The wholesale segment, primarily driven by Free People, increased by 24% to $74.6 million. Most notably, the subscription segment (Nuuly) showed exceptional growth, increasing by 60% to $124.4 million, reflecting the company’s successful expansion into the rental apparel market.

Geographic performance varied significantly, with retail segment comparable sales in Europe and ROW (Rest of World) increasing by 14%, substantially outpacing North America’s 4% growth. This indicates strong international momentum and potential for further global expansion.

Brand Performance

Each of URBN’s brands contributed to the overall growth, though with varying degrees of strength. Anthropologie, the company’s largest brand, increased sales by 8% to $569.9 million, with comparable sales up 7% driven by both digital and retail store growth.

Free People continued its strong performance with an 11% sales increase to $353.1 million. Particularly noteworthy was the performance of FP Movement, which grew by 29% to $80.1 million, significantly outpacing the 6% growth of the core Free People brand.

The Urban Outfitters brand showed more modest growth of 1% to $273.5 million, with stronger performance in Europe offsetting weakness in North America. The brand saw positive results in home goods, women’s apparel, and women’s accessories.

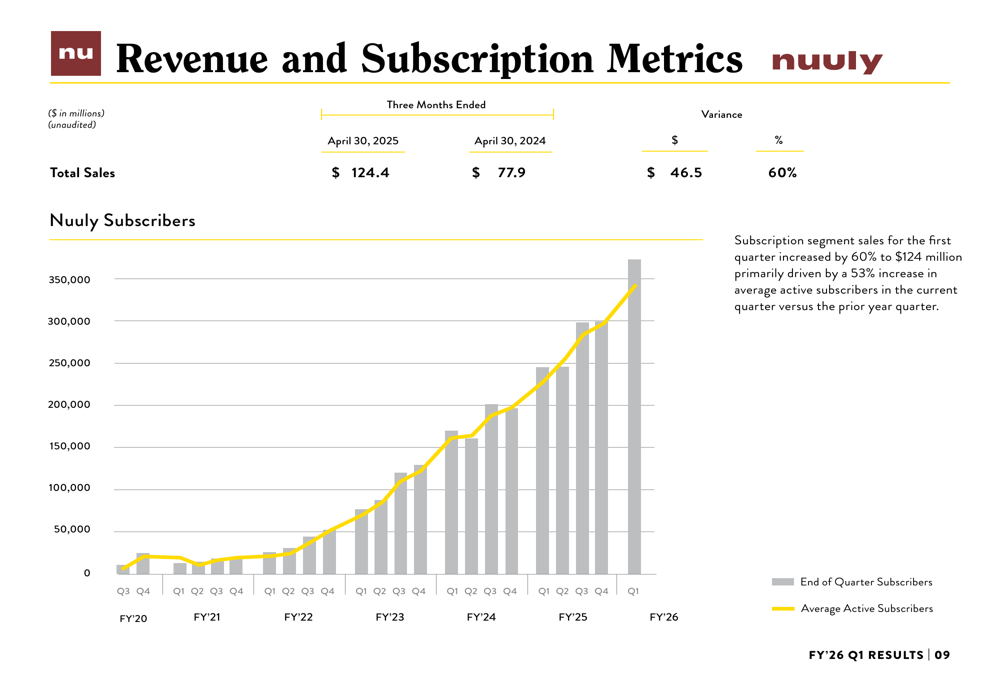

Nuuly, the company’s subscription rental service, demonstrated remarkable growth and increasing scale:

With over 350,000 subscribers and 60% revenue growth, Nuuly has quickly established itself as a significant contributor to URBN’s business. The 53% increase in average active subscribers highlights strong consumer adoption of this innovative retail model.

Profitability and Financial Position

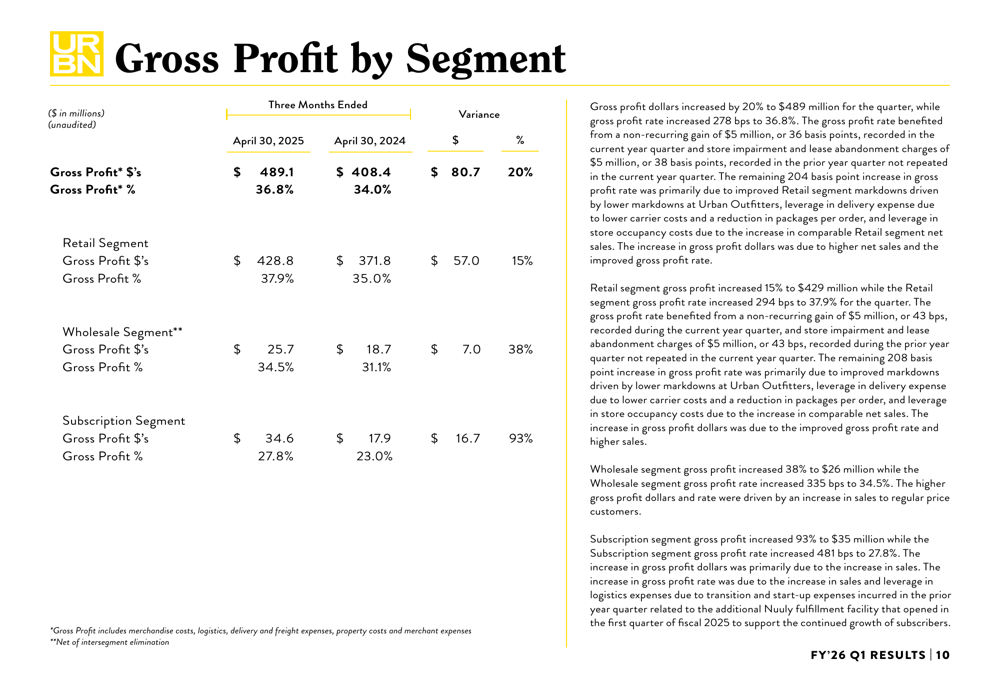

The improvement in profitability was evident across all business segments. Gross profit increased by 20% to $489.1 million, with the gross profit rate expanding by 278 basis points to 36.8%.

The detailed breakdown of gross profit by segment shows improvements across all business lines:

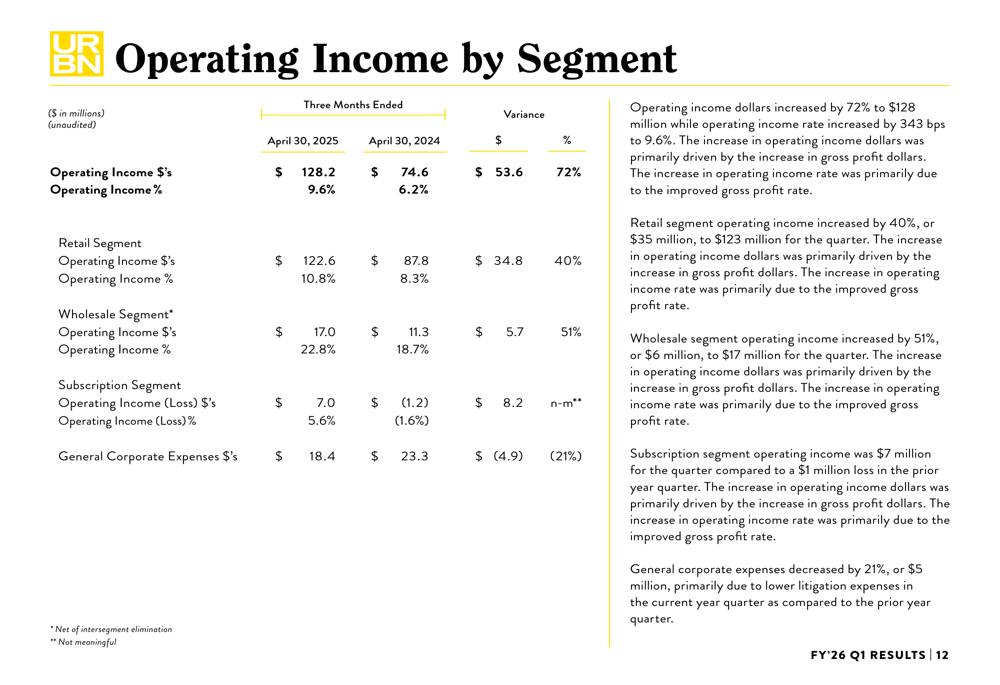

Operating income saw an even more dramatic improvement, increasing by 72% to $128.2 million. All segments contributed to this growth, with the subscription segment achieving a particularly notable turnaround from an operating loss of $1.2 million in the prior year to operating income of $7.0 million.

The company’s operating income performance by segment demonstrates the improving economics across all business lines:

Urban Outfitters maintains a strong financial position with $841 million in cash and marketable securities and no borrowings against its $350 million credit facility. During the quarter, the company repurchased 3.3 million shares for $152 million at an average price of $46.40, reflecting management’s confidence in the business outlook.

The company’s comprehensive income statement shows the significant improvement in profitability:

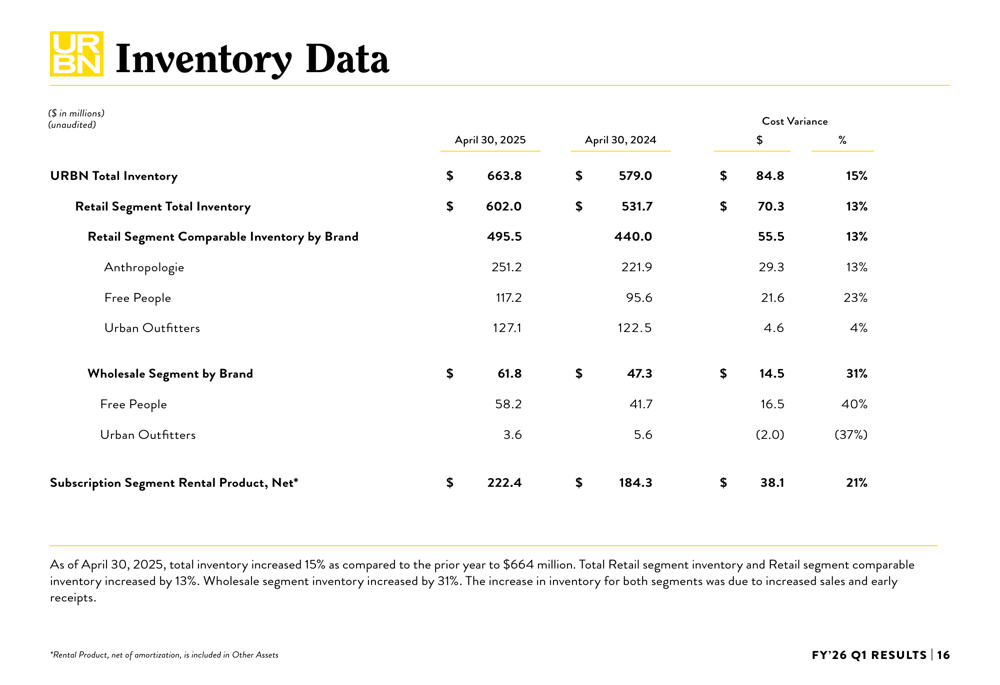

Inventory levels increased by 15% year-over-year to $663.8 million, slightly outpacing sales growth. Management attributed this to increased sales and early receipts, indicating confidence in future demand.

Store Expansion and Capital Allocation

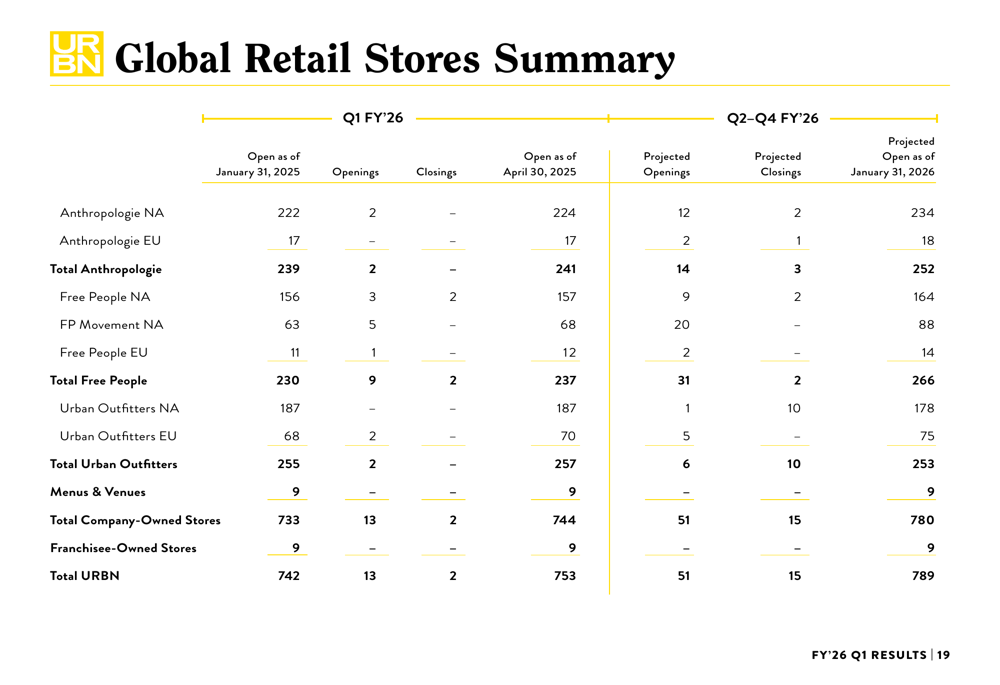

Urban Outfitters continues to expand its physical retail presence selectively, with a net increase of 11 stores during Q1 FY’26. The company’s store expansion strategy varies by brand, with significant growth planned for Free People (projected to add 36 stores in FY’26) and more modest growth for Anthropologie (projected to add 13 stores).

The company’s global store summary highlights these expansion plans:

Notably, Urban Outfitters plans to reduce its namesake brand store count slightly by the end of FY’26, focusing instead on optimizing its existing store base and growing in more profitable locations, particularly in Europe where the brand is showing stronger performance.

Forward-Looking Statements

Looking ahead, Urban Outfitters expects continued growth across all segments. Management projects total company sales to grow in the high single digits for Q2, with retail segment comparable sales increasing in the mid-single digits and wholesale segment achieving low double-digit growth.

The company anticipates gross margin improvement of 50-100 basis points for the fiscal year, with minimal negative impact expected from potential tariffs. This outlook reflects management’s confidence in the company’s strategic positioning and operational execution.

The strong Q1 results and positive outlook position Urban Outfitters favorably in the competitive retail landscape, with its diversified brand portfolio, multi-channel strategy, and innovative business models like Nuuly providing multiple avenues for continued growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.