Stock market today: S&P 500 drops for fifth day as focus shifts to Powell’s speech

Introduction & Market Context

U.S. Bancorp (NYSE:USB) presented its second quarter 2025 earnings on July 17, revealing solid performance despite net interest income headwinds. The bank reported earnings per share of $1.11, representing a 13% year-over-year increase, driven by strong fee revenue growth and disciplined expense management. Despite these positive results, U.S. Bancorp’s stock was down 2.25% in premarket trading to $44.65, suggesting investors may have had higher expectations.

The company’s quarterly performance demonstrates its strategic shift toward a more balanced revenue mix, with fee income now representing 42% of total net revenue. This diversification has helped U.S. Bancorp navigate the challenging interest rate environment while making progress toward its medium-term financial targets.

Quarterly Performance Highlights

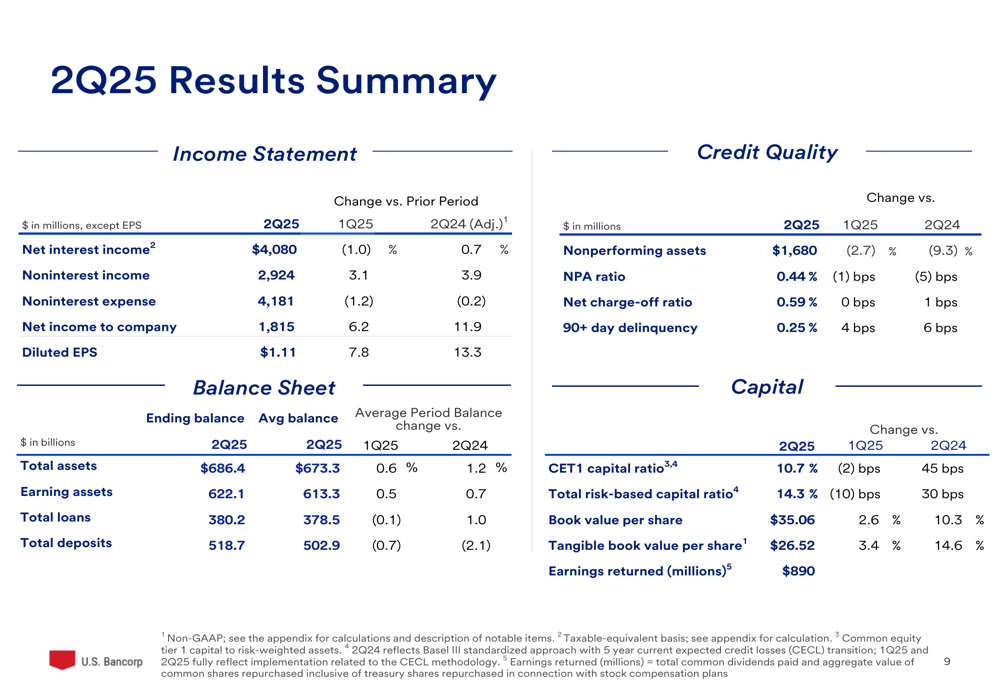

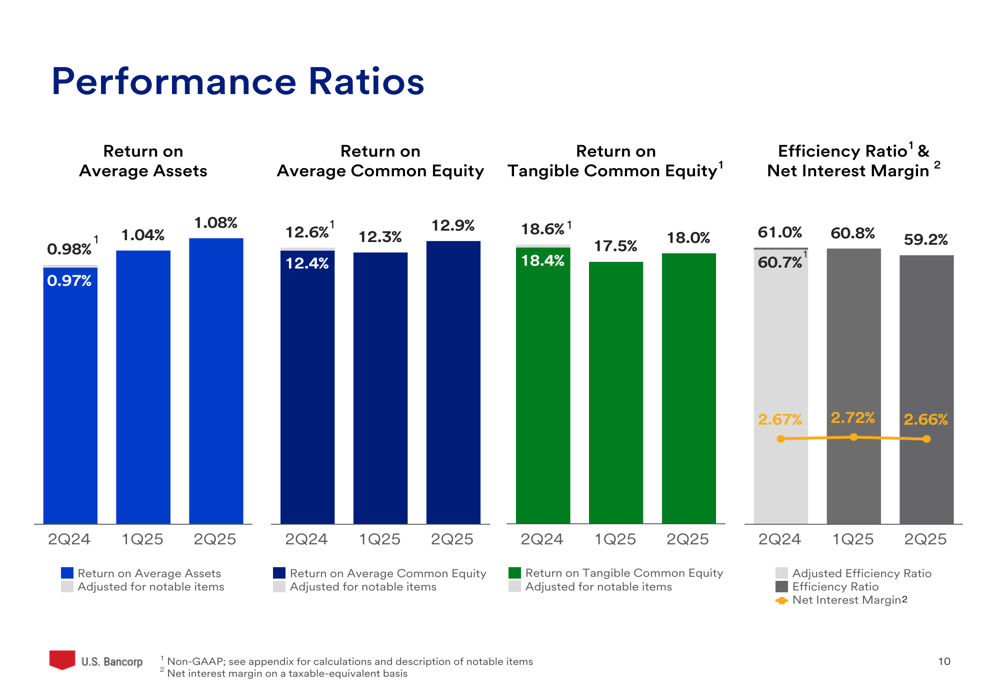

U.S. Bancorp reported net income of $1.815 billion for Q2 2025, up 11.9% from the same period last year and 6.2% higher than the previous quarter. The bank achieved a return on tangible common equity of 18.0% and demonstrated positive operating leverage of 250 basis points year-over-year.

As shown in the following comprehensive results summary, the bank maintained stable credit quality while improving its efficiency ratio to 59.2%:

Net interest income was $4.08 billion, down 1.0% from the previous quarter but up 0.7% year-over-year on an adjusted basis. The slight decline was primarily attributed to competitive deposit pricing pressure and customer rotation into higher-rate products. Meanwhile, noninterest income rose to $2.92 billion, up 3.1% quarter-over-quarter and 3.9% year-over-year, reflecting growth across most fee income categories.

The bank’s performance ratios showed improvement across multiple metrics compared to both the previous quarter and the same period last year:

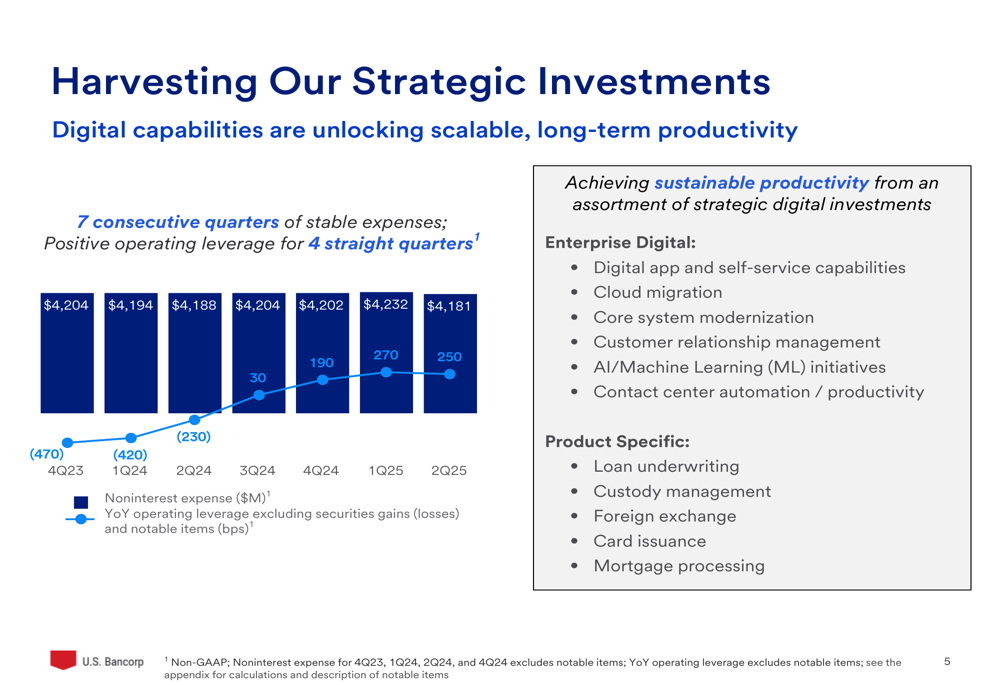

On the expense front, U.S. Bancorp maintained its disciplined approach, with noninterest expenses decreasing 1.2% from the previous quarter to $4.18 billion. This marks the seventh consecutive quarter of stable expenses, contributing to four straight quarters of positive operating leverage.

Strategic Initiatives

U.S. Bancorp’s presentation highlighted its strategic focus on harvesting investments in digital capabilities to drive long-term productivity. The bank has maintained stable expenses while investing in enterprise digital initiatives and product-specific enhancements.

As illustrated in the following chart, the company’s strategic investments are yielding results in terms of expense management:

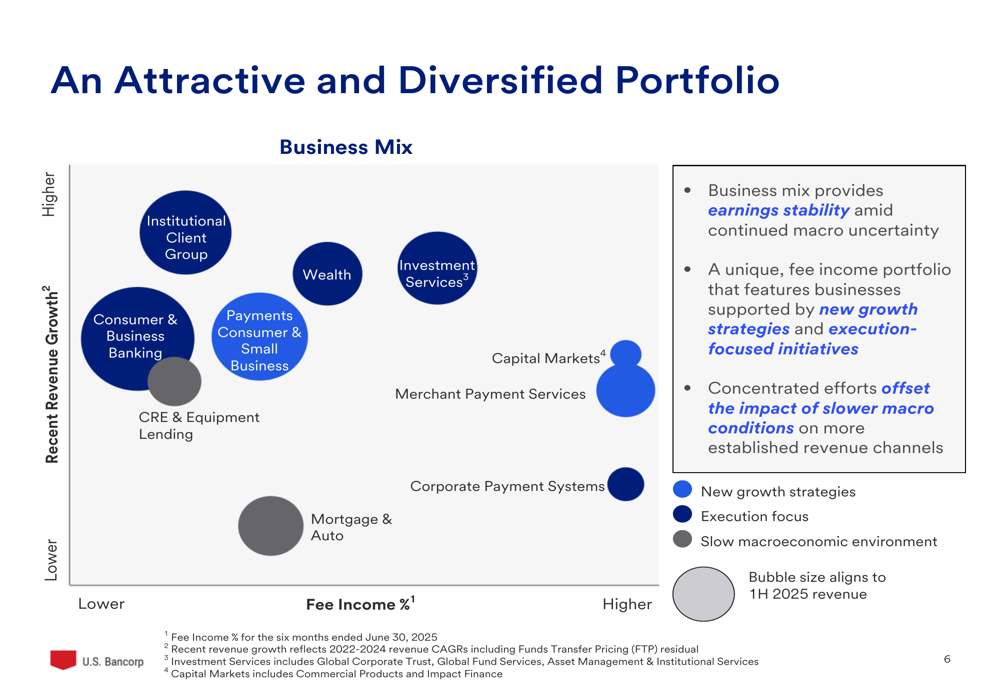

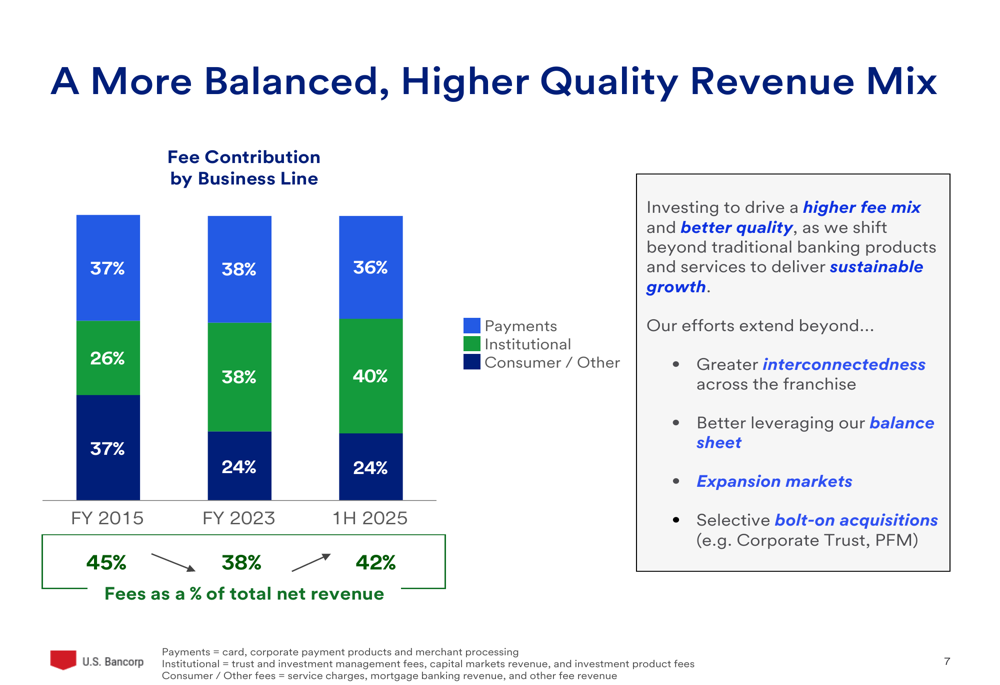

The bank is also actively repositioning its portfolio to focus on higher-quality, fee-generating business lines. This diversified approach provides earnings stability amid macroeconomic uncertainty while creating opportunities for growth.

The following visualization demonstrates how U.S. Bancorp’s business mix is distributed across various sectors, with bubble size representing revenue contribution:

Over time, U.S. Bancorp has strategically shifted toward a more balanced revenue mix with higher fee contributions. The bank’s institutional business has grown from 26% of fee revenue in 2015 to 40% in the first half of 2025, while payments remain a significant contributor at 36%.

Detailed Financial Analysis

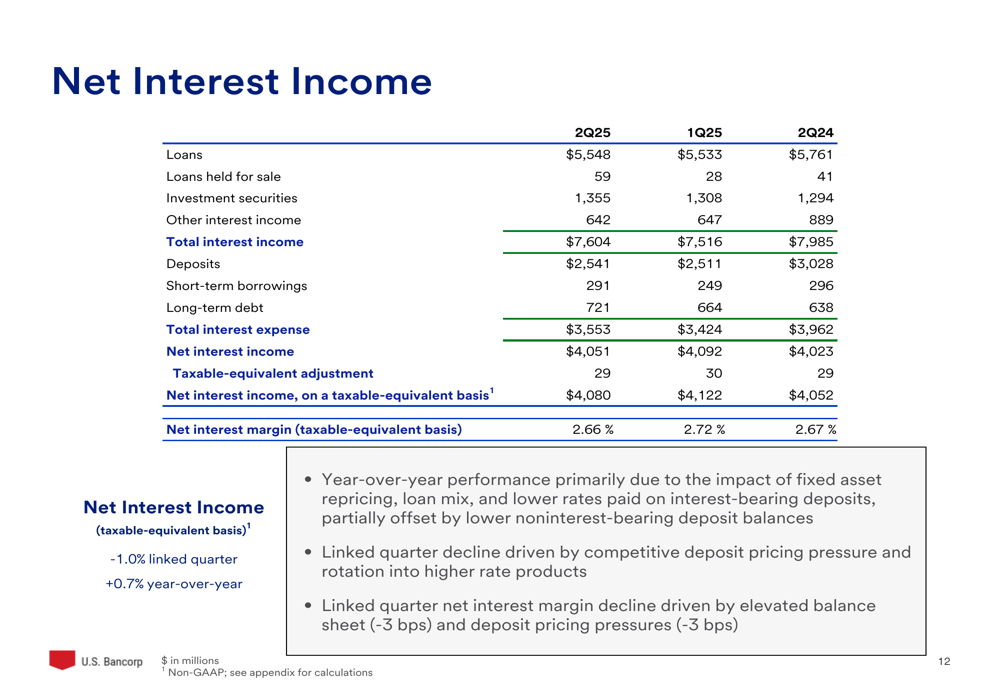

U.S. Bancorp’s net interest income performance reflects the challenging rate environment, with net interest margin at 2.66% for Q2 2025, down from 2.72% in the previous quarter. The year-over-year performance was primarily supported by fixed asset repricing, loan mix improvements, and lower rates paid on interest-bearing deposits, partially offset by lower noninterest-bearing deposit balances.

The following breakdown provides a detailed view of the components affecting net interest income:

On the fee income side, U.S. Bancorp saw growth across most categories, with particularly strong performance in payments, trust and investment management, and capital markets revenue. Total (EPA:TTEF) fee revenue reached $2.98 billion in Q2 2025, representing 4.6% year-over-year growth.

Credit quality remained stable, with nonperforming assets decreasing 2.7% from the previous quarter to $1.68 billion. The bank reported a net charge-off ratio of 0.59%, unchanged from the previous quarter and up just 1 basis point year-over-year. A $53 million reserve release was driven by strategic loan sales, while the reserve coverage ratio held steady at 2.07%.

Forward-Looking Statements

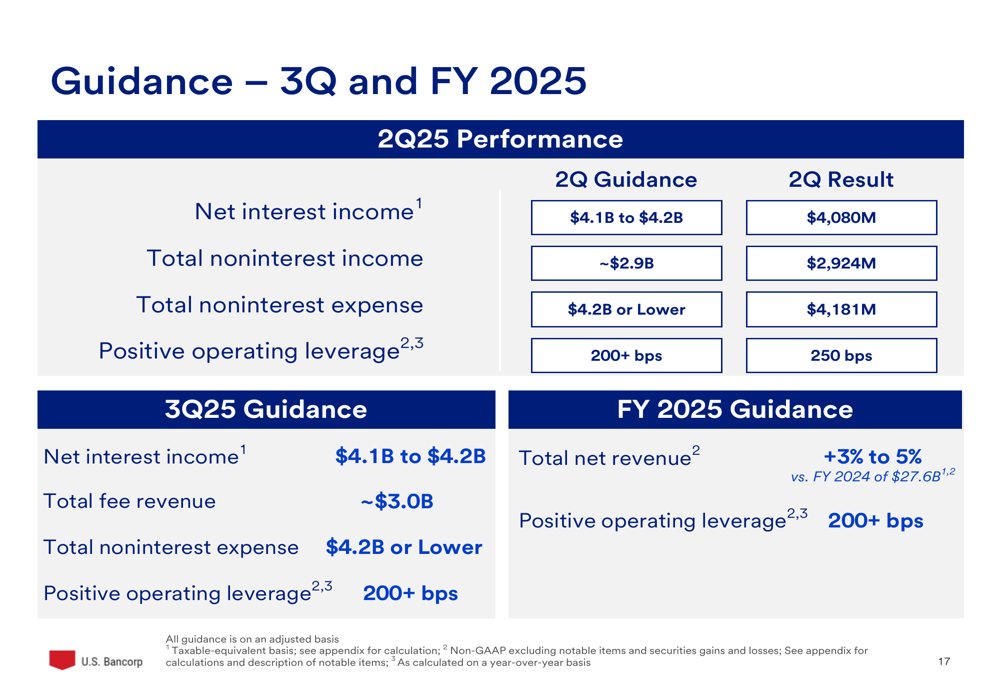

For the third quarter of 2025, U.S. Bancorp expects net interest income between $4.1 billion and $4.2 billion, total fee revenue of approximately $3.0 billion, and noninterest expenses of $4.2 billion or lower. The bank anticipates maintaining positive operating leverage of over 200 basis points.

For the full year 2025, the company projects total net revenue growth of 3% to 5% compared to the $27.6 billion reported in fiscal year 2024, with positive operating leverage exceeding 200 basis points.

The following guidance summary outlines the bank’s expectations for both Q3 and full-year 2025:

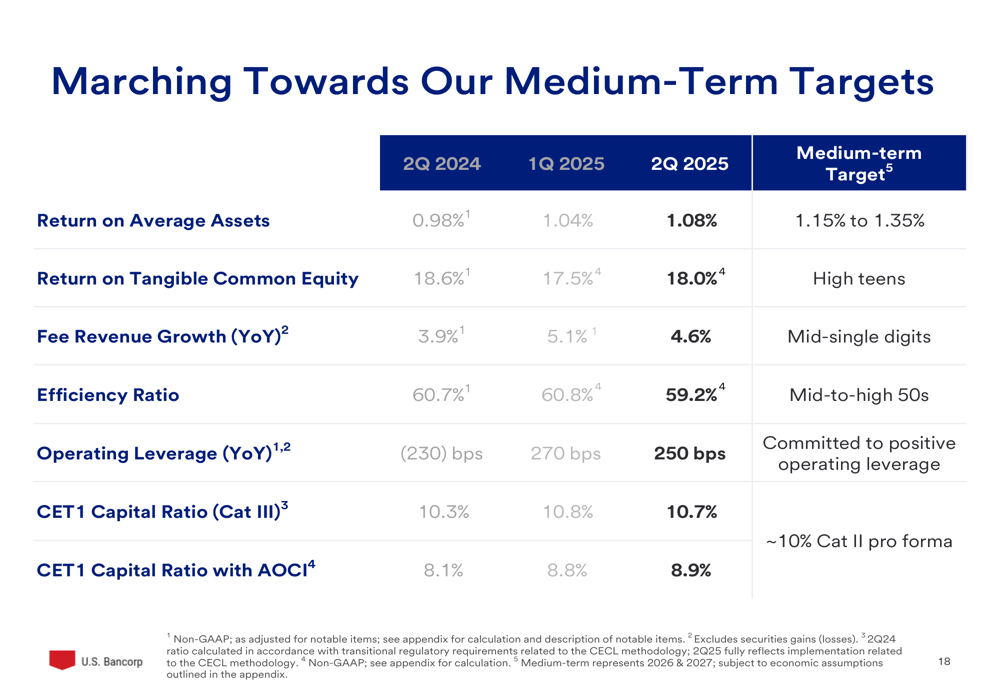

U.S. Bancorp also provided an update on its progress toward medium-term financial targets. The bank’s return on average assets of 1.08% in Q2 2025 shows improvement from 1.04% in Q1 2025 but remains below the medium-term target of 1.15% to 1.35%. Similarly, the efficiency ratio of 59.2% represents progress toward the medium-term goal of mid-to-high 50s.

Market Reaction & Conclusion

Despite reporting solid financial results with 13% EPS growth and improved efficiency, U.S. Bancorp’s stock was down 2.25% in premarket trading. This negative reaction may reflect broader market concerns about the banking sector or investor expectations for more substantial improvements in net interest income.

U.S. Bancorp’s Q2 2025 presentation demonstrates the bank’s strategic shift toward a more balanced revenue mix, with fee income now representing 42% of total net revenue. This diversification strategy, combined with disciplined expense management and balance sheet optimization, positions the bank to navigate the current interest rate environment while making progress toward its medium-term financial targets.

The bank’s focus on deepening client relationships, particularly targeting multi-service clients who generate significantly higher revenue, should support continued growth in fee income. Meanwhile, ongoing investments in digital capabilities and payments transformation are expected to drive further operational efficiencies and enhance the customer experience.

As U.S. Bancorp continues to execute its strategy, investors will be watching closely for signs of accelerating progress toward medium-term targets and the impact of potential Federal Reserve rate cuts on the bank’s net interest margin.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.