Intel stock extends gains after report of possible U.S. government stake

USA Compression Partners LP (NYSE:USAC) released its first quarter 2025 earnings presentation on May 6, highlighting continued revenue growth and strong operational performance as the company positions itself to capitalize on expanding natural gas demand in the United States.

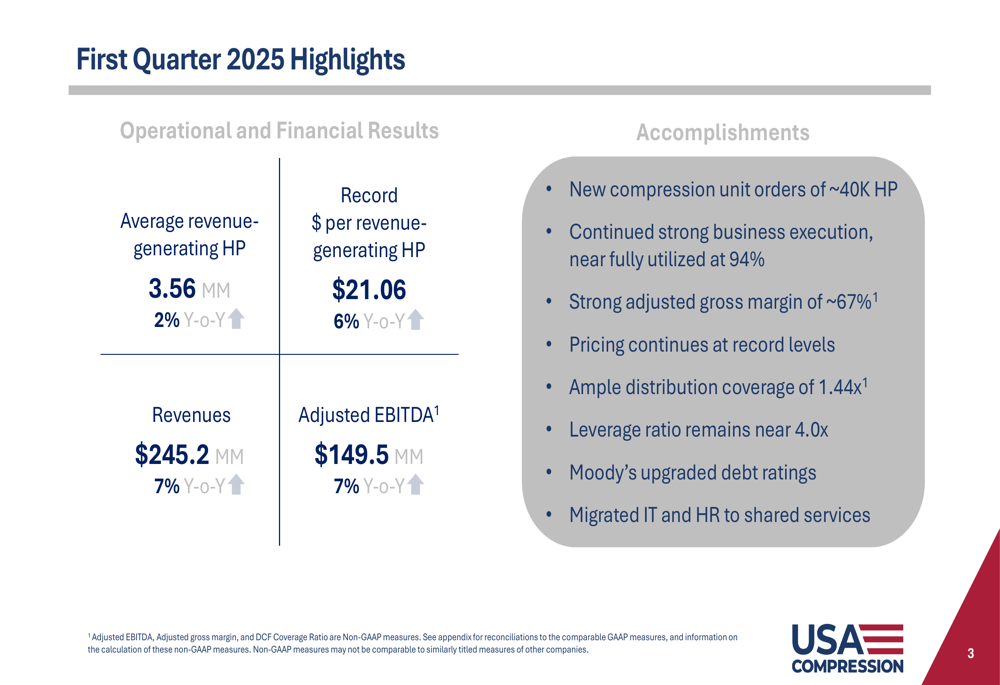

Quarterly Performance Highlights

USA Compression reported solid financial and operational results for Q1 2025, demonstrating consistent growth across key metrics. The company achieved revenues of $245.2 million, representing a 7% increase year-over-year, while adjusted EBITDA also grew 7% to $149.5 million compared to the same period last year.

The company maintained near-full utilization of its compression fleet at 94%, while achieving a strong adjusted gross margin of approximately 67%. Average revenue-generating horsepower reached 3.56 million, up 2% year-over-year, and the company set a record for revenue per horsepower at $21.06, a 6% increase from Q1 2024.

As shown in the following quarterly highlights slide, USA Compression continued to execute well across its business while maintaining solid financial metrics:

"Our first quarter results demonstrate the continued strength of our business model and our ability to execute in a dynamic market environment," said Clint Green, CEO of USA Compression Partners. The company also reported ample distribution coverage of 1.44x and maintained its leverage ratio near 4.0x, reflecting disciplined financial management.

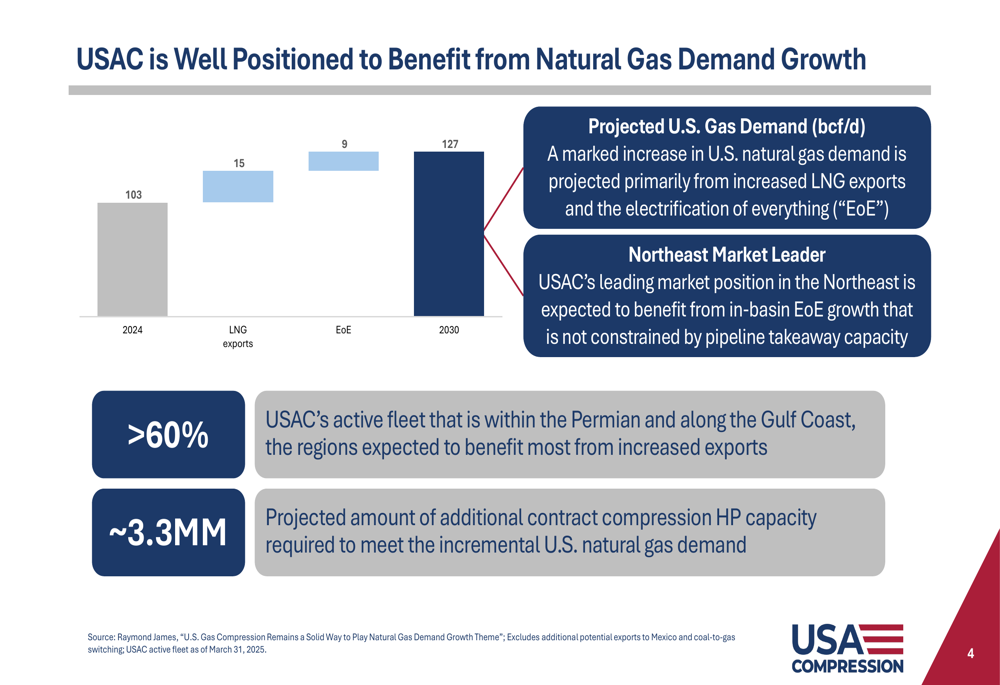

Strategic Positioning for Natural Gas Growth

A key focus of USA Compression’s presentation was the company’s strategic positioning to benefit from projected growth in U.S. natural gas demand. According to the company’s analysis, U.S. gas demand is expected to increase from 103 bcf/d in 2024 to 127 bcf/d by 2030, driven primarily by increased LNG exports and electrification.

The following slide illustrates how USA Compression is positioned to capitalize on this growth trend:

More than 60% of USAC’s active compression fleet is strategically located within the Permian Basin and along the Gulf Coast, areas expected to see significant production growth. Additionally, the company highlighted its leading market position in the Northeast, which is expected to benefit from in-basin end-of-life growth that is not constrained by pipeline takeaway capacity.

The company estimates that approximately 3.3 million horsepower of additional contract compression capacity will be required to meet the projected incremental U.S. natural gas demand, creating substantial growth opportunities for USA Compression.

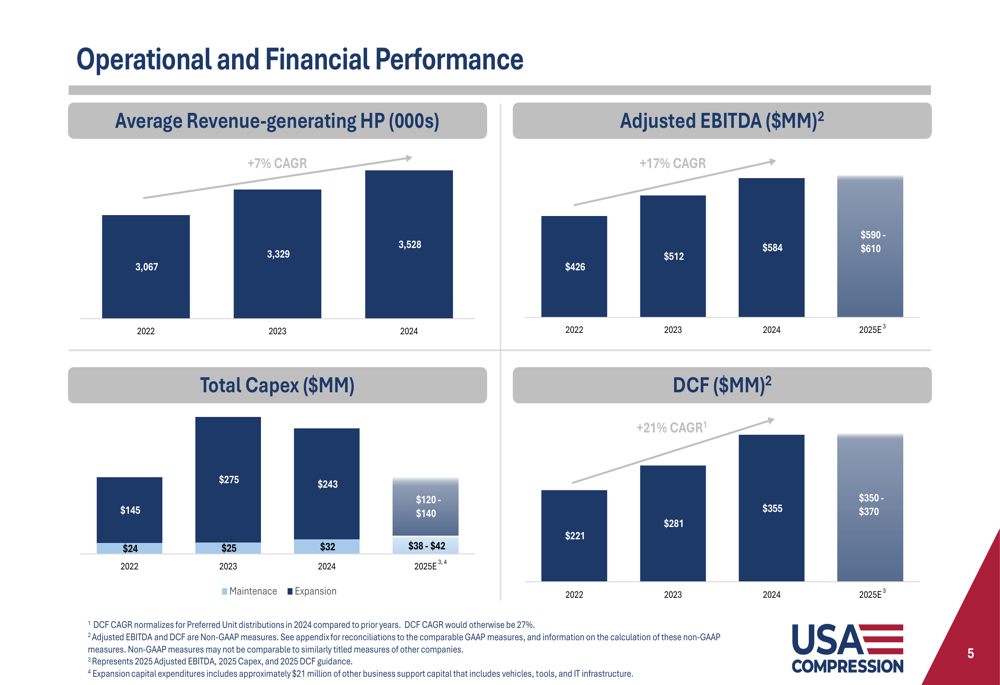

Financial Performance and Outlook

USA Compression has demonstrated consistent financial improvement over the past three years. The company’s operational and financial performance slide shows impressive compound annual growth rates (CAGR) across key metrics from 2022 to 2024:

Average revenue-generating horsepower has grown at a 7% CAGR, while adjusted EBITDA has increased at a 17% CAGR, reaching $584 million in 2024. Most notably, distributable cash flow (DCF) has grown at a 21% CAGR over the same period, reaching $355 million in 2024.

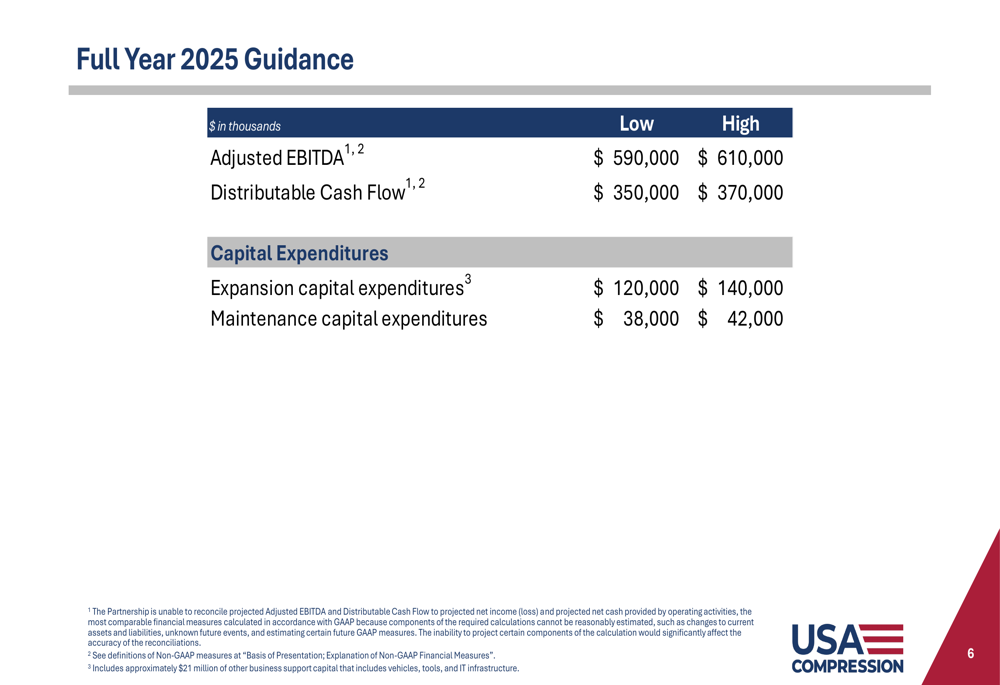

Looking ahead, USA Compression provided guidance for full-year 2025, projecting continued growth:

The company expects adjusted EBITDA to range between $590 million and $610 million for 2025, representing approximately 3% growth at the midpoint compared to 2024. Distributable cash flow is projected between $350 million and $370 million. Capital expenditures are expected to be lower than in 2024, with expansion capital ranging from $120 million to $140 million and maintenance capital between $38 million and $42 million.

This guidance aligns with the company’s strategy of disciplined growth while maintaining strong returns for unitholders. The reduced capital expenditure forecast for 2025 follows higher spending in 2024, when the company reported expansion and maintenance capital expenditures totaling $243 million.

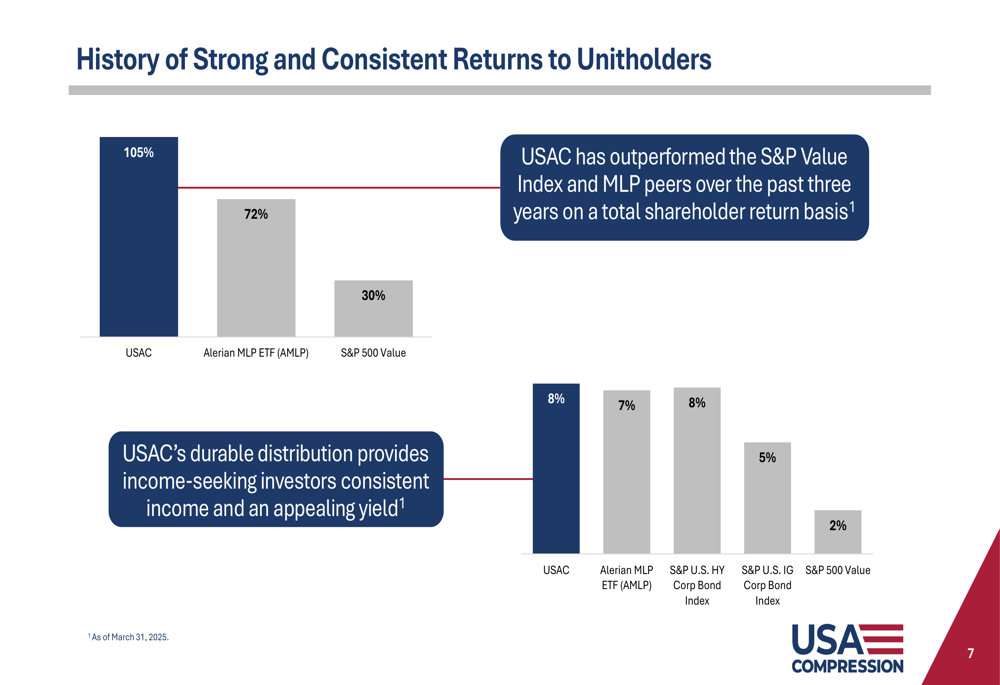

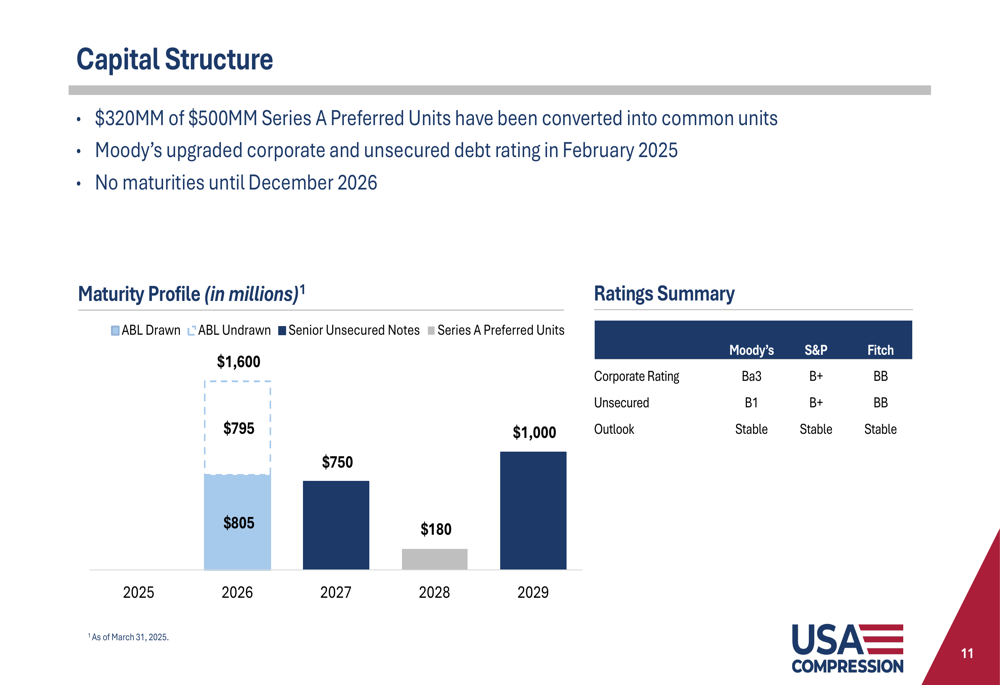

Shareholder Returns and Capital Structure

USA Compression highlighted its track record of delivering strong returns to unitholders. The company has outperformed both the broader market and its MLP peers over the past three years:

The presentation showed that USAC delivered a total shareholder return of 105% over the three-year period, significantly outpacing the Alerian MLP ETF (AMLP) at 72% and the S&P 500 Value Index at 30%. Additionally, the company’s current yield of 8% remains competitive with high-yield corporate bonds while exceeding the yields offered by investment-grade corporate bonds and the broader market.

On the capital structure front, USA Compression reported that $320 million of its $500 million Series A Preferred Units have been converted into common units, simplifying the company’s capital structure. In February 2025, Moody’s upgraded the company’s corporate and unsecured debt ratings, reflecting improved financial stability.

The company has no debt maturities until December 2026, providing financial flexibility for the next 18 months. This improved debt profile, combined with strong operational performance, positions USA Compression well for continued growth as natural gas demand expands in the coming years.

Conclusion

USA Compression’s Q1 2025 presentation portrays a company with solid financial performance, strategic market positioning, and a clear growth trajectory aligned with expanding natural gas demand. With consistent revenue and EBITDA growth, high fleet utilization, and strong shareholder returns, the company appears well-positioned to capitalize on the projected increase in U.S. natural gas demand through 2030.

The company’s shares closed at $24.30 on May 5, 2025, down 2.64% for the day, but showed signs of recovery in after-hours trading, up 0.99% to $24.54. Over the past year, the stock has traded between $21.06 and $30.10, reflecting both the volatility in the energy sector and the company’s overall positive trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.