Gold prices hold sharp gains as soft US jobs data fuels Fed rate cut bets

USCB Financial Holdings (NASDAQ:USCB) reported strong second quarter 2025 results, with significant growth in earnings, loans, and deposits, according to the company’s latest earnings presentation. The Miami-based bank delivered net income of $8.1 million or $0.40 per diluted share, representing a 31.1% increase compared to the second quarter of 2024.

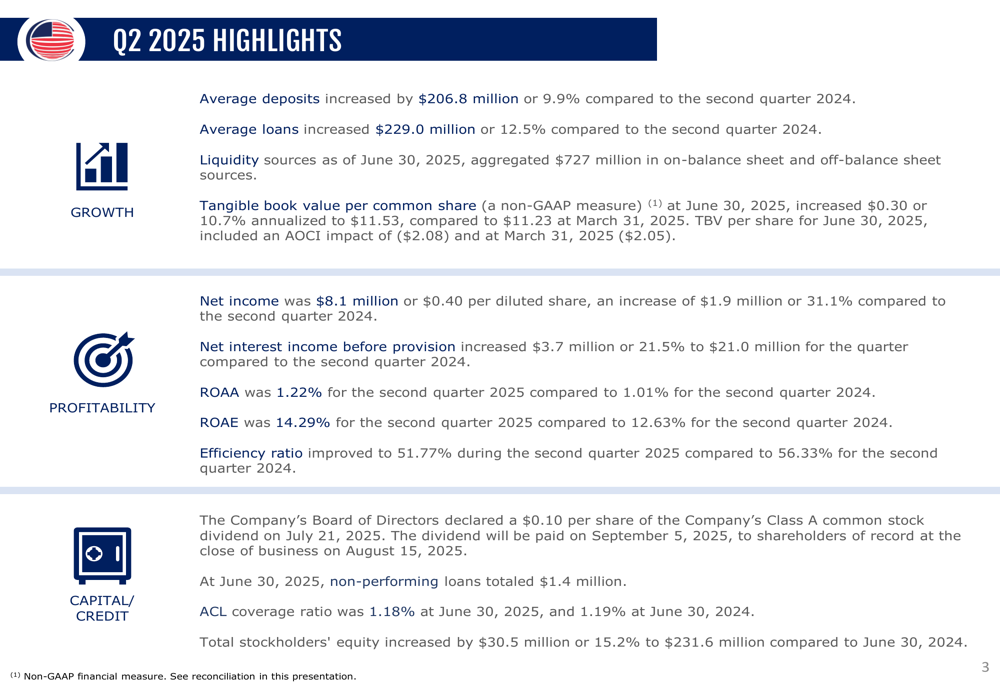

Quarterly Performance Highlights

USCB Financial demonstrated robust performance across key metrics in Q2 2025. Net income increased to $8.1 million from $6.2 million in the same period last year. The bank’s return on average assets (ROAA) improved to 1.22% from 1.01% in Q2 2024, while return on average equity (ROAE) rose to 14.29% from 12.63%.

The company’s efficiency ratio, a key measure of operational effectiveness, improved to 51.77% from 56.33% in the prior-year quarter, indicating better cost management. The bank also declared a quarterly dividend of $0.10 per share.

As shown in the following summary of quarterly highlights:

USCB’s tangible book value per share increased to $11.53 as of June 30, 2025, representing a 10.7% annualized increase from $11.23 at the end of the previous quarter. This growth reflects the company’s continued focus on building shareholder value.

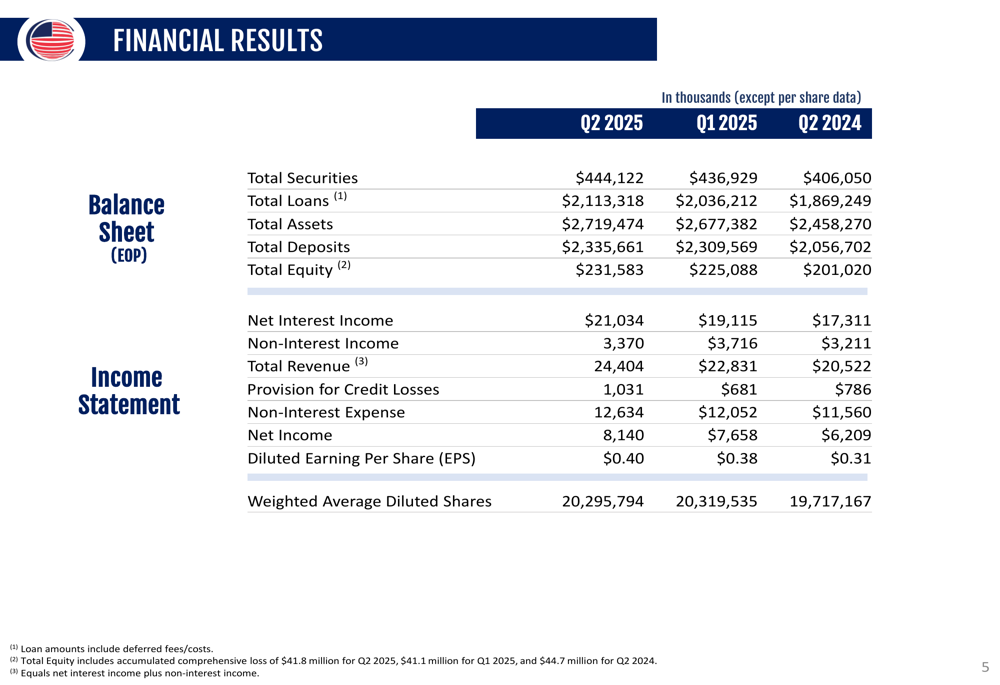

Detailed Financial Analysis

The bank reported total assets of $2.72 billion as of June 30, 2025, up from $2.46 billion a year earlier. Total (EPA:TTEF) loans increased to $2.11 billion from $1.87 billion in Q2 2024, while deposits grew to $2.34 billion from $2.06 billion.

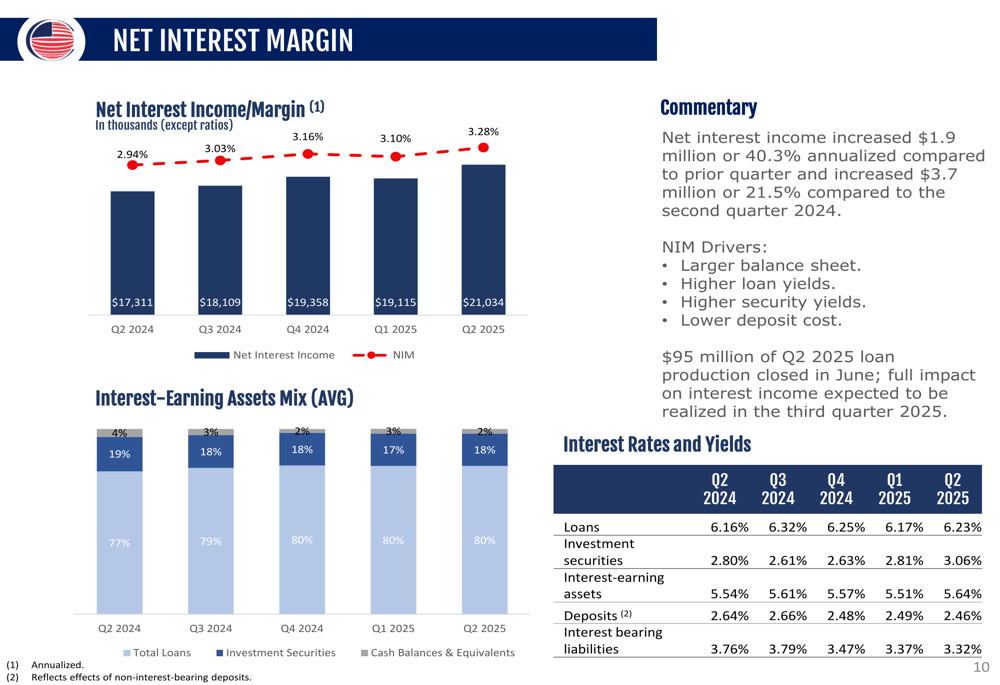

Net interest income before provision for credit losses increased by 21.5% year-over-year to $21.0 million, driven by loan growth and improved net interest margin. The net interest margin expanded to 3.28% in Q2 2025 from 2.94% in Q2 2024, reflecting higher loan yields and lower deposit costs.

The detailed financial results are presented in the following table:

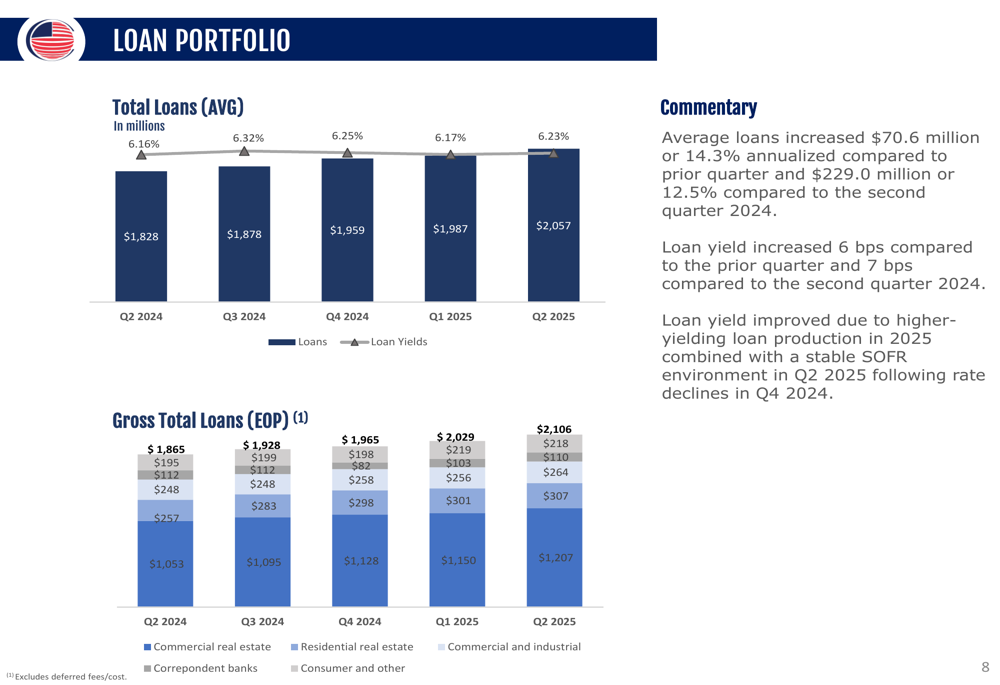

USCB’s loan portfolio continues to show strong growth, with average loans increasing by $229.0 million or 12.5% compared to Q2 2024. Loan yields improved to 6.32% in Q2 2025 from 6.25% in Q2 2024, contributing to the enhanced net interest margin.

The bank’s loan production has been robust, with gross loan production for 2025 amounting to $369 million. Notably, $95 million of Q2 2025 loan production closed in June, with the full impact on interest income expected to be realized in the third quarter.

The following chart illustrates the growth in the loan portfolio and yield trends:

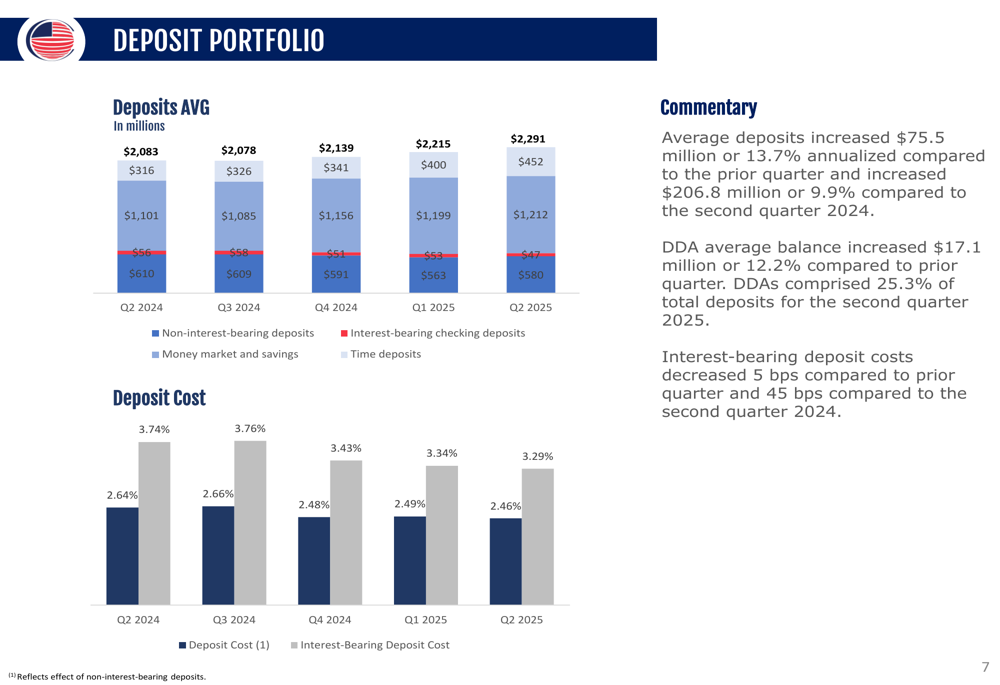

On the funding side, average deposits increased by $206.8 million or 9.9% compared to Q2 2024. Non-interest-bearing deposits comprised 25.3% of total deposits for Q2 2025, providing a stable and low-cost funding base. Interest-bearing deposit costs decreased by 45 basis points compared to Q2 2024, further supporting the improvement in net interest margin.

The deposit portfolio composition and cost trends are shown below:

Net interest margin improvement was driven by a combination of factors including a larger balance sheet, higher loan yields, higher security yields, and lower deposit costs. The bank’s interest-earning asset mix continues to be dominated by loans, which generally provide higher yields than securities.

The following chart illustrates the net interest income and margin trends:

Asset Quality & Capital Position

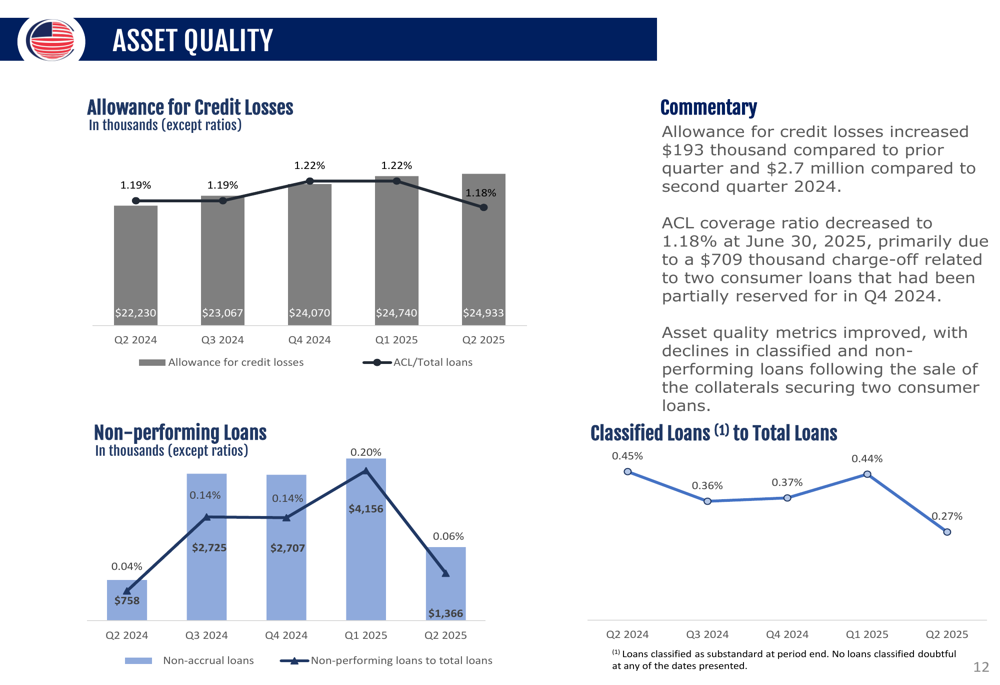

USCB maintained strong asset quality metrics in Q2 2025. Non-performing loans totaled just $1.4 million, representing a minimal portion of the total loan portfolio. The allowance for credit losses to loans ratio stood at 1.18%, providing adequate coverage for potential loan losses.

The bank’s asset quality trends are illustrated in the following chart:

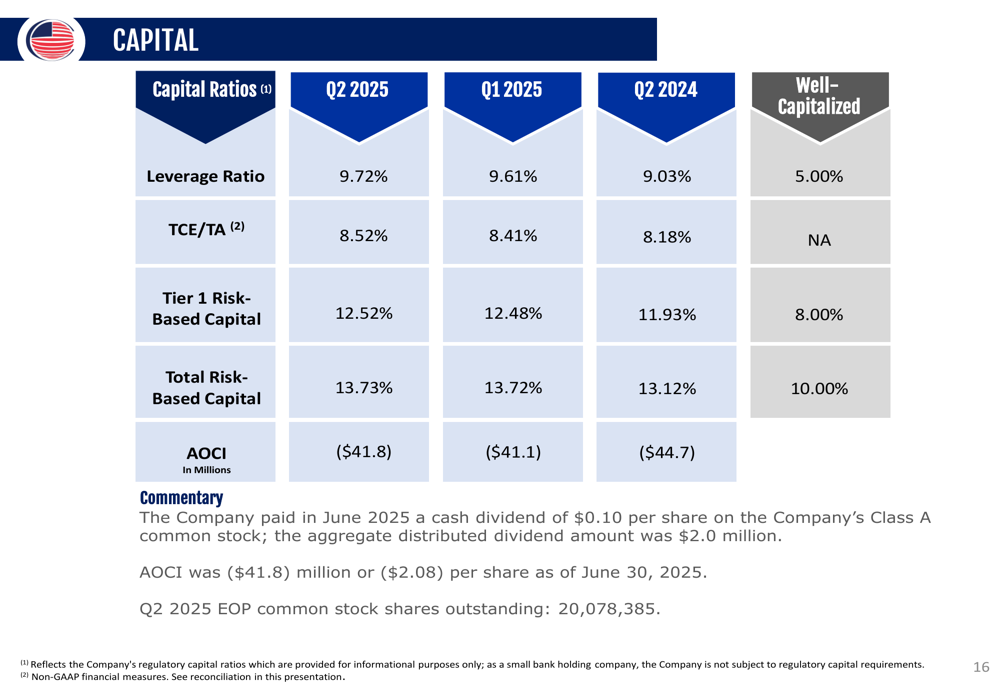

USCB’s capital position remains robust, with all regulatory capital ratios exceeding "well-capitalized" benchmarks. As of June 30, 2025, the bank reported a leverage ratio of 9.72%, a Tier 1 risk-based capital ratio of 12.52%, and a total risk-based capital ratio of 13.73%.

Total stockholders’ equity increased by $30.5 million or 15.2% to $231.6 million compared to June 30, 2024, further strengthening the bank’s financial foundation.

The capital ratios and benchmarks are presented in the following table:

Strategic Outlook

USCB Financial Holdings continues to position itself as a leading franchise in one of the most attractive banking markets in Florida and the U.S. The bank’s strategy focuses on robust organic growth, maintaining strong asset quality, and enhancing profitability.

Management highlighted several key strengths and strategic priorities in the presentation, including the bank’s experienced leadership team, strong profitability metrics, and core-funded deposit base. The bank’s commercial real estate loan portfolio remains diversified and granular, with retail non-owner occupied properties making up 27% of total CRE or $327.4 million.

The key strategic takeaways are summarized in the following slide:

This performance represents a continuation of the positive trends observed in Q1 2025, when the bank reported EPS of $0.38 and ROAE of 14.15%. The Q2 results show further improvement in these metrics, with EPS increasing to $0.40 and ROAE rising to 14.29%.

While the stock experienced some volatility following the Q1 earnings announcement, dropping 8.98% to $16.26 in after-hours trading at that time, the fundamentals of the bank continue to strengthen. According to the latest data, USCB’s stock closed at $17.18 on July 25, 2025, up 0.76% on the day, suggesting improved investor sentiment about the bank’s performance and prospects.

With its strong capital position, improving profitability metrics, and continued loan and deposit growth, USCB Financial Holdings appears well-positioned to capitalize on opportunities in the Florida banking market while navigating potential challenges such as interest rate fluctuations and economic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.