Tonix Pharmaceuticals stock halted ahead of FDA approval news

Introduction & Market Context

Utz Brands Inc. (NYSE:UTZ) presented its second quarter 2025 earnings results on July 31, 2025, highlighting continued momentum in its volume-led growth strategy. The company reported a 2.9% increase in net sales, driven primarily by strong performance in its branded salty snacks segment.

Despite meeting growth expectations, Utz shares have faced pressure in recent trading, with the stock closing at $13.93 on July 30, down 1.9% for the day and continuing to trade near its 52-week low of $11.53. The stock remains significantly below its 52-week high of $18.89, reflecting ongoing investor concerns about profitability despite solid top-line growth.

Quarterly Performance Highlights

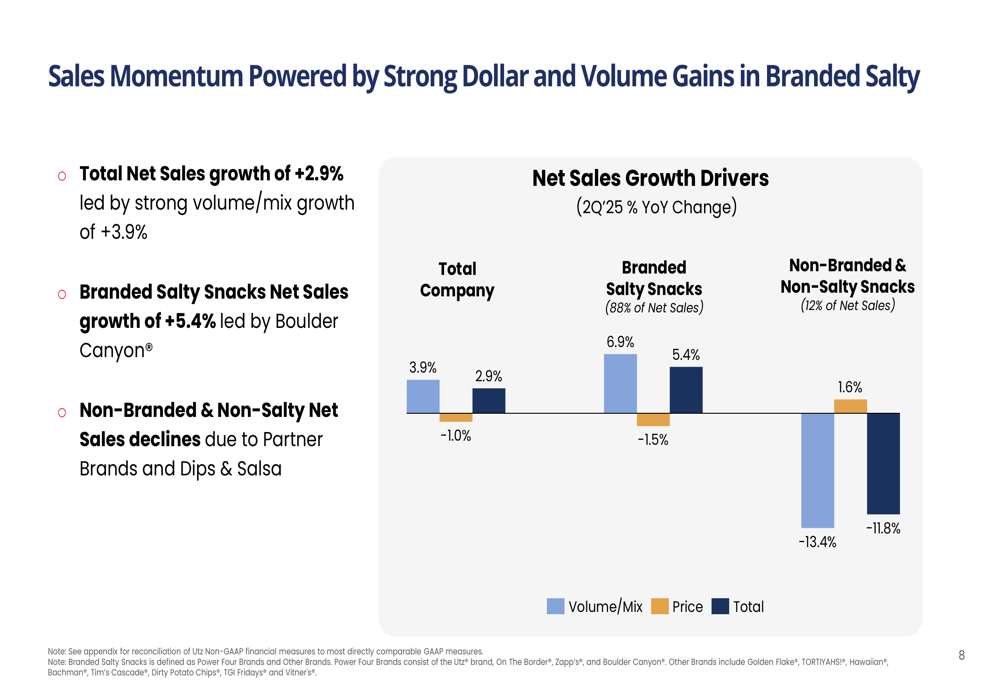

Utz reported net sales of $366.7 million for Q2 2025, representing a 2.9% increase year-over-year. This growth was primarily volume-driven, with volume/mix contributing a robust 3.9% increase, partially offset by a 1.0% decrease in pricing.

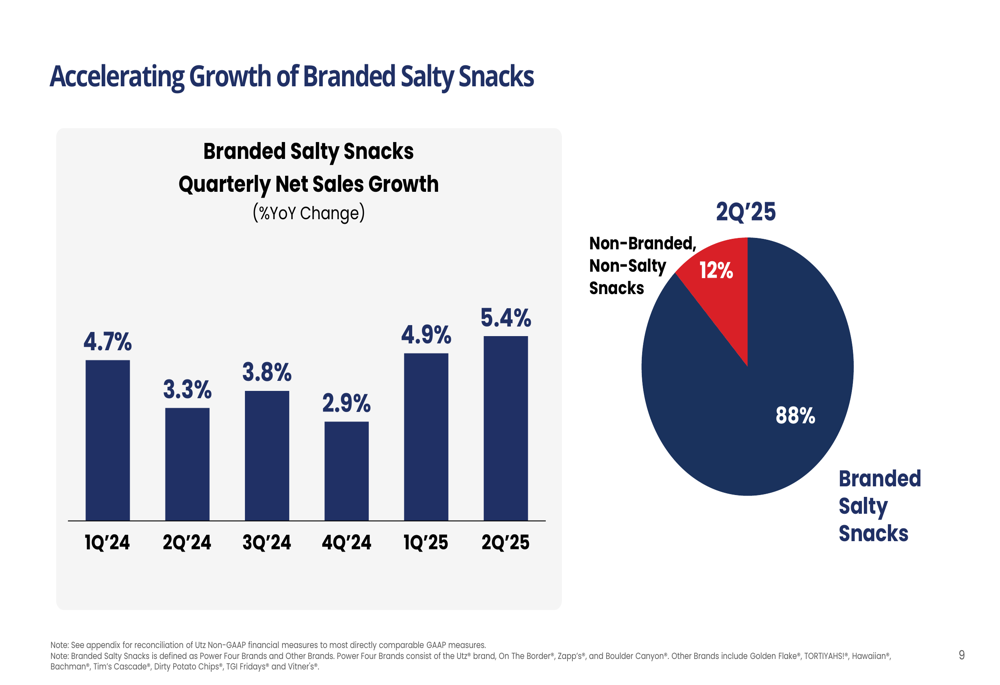

The company’s branded salty snacks segment, which comprises 88% of total sales, showed particularly strong performance with 5.4% growth compared to the same period last year. This growth was led by the Boulder Canyon brand, continuing the momentum seen in previous quarters.

As shown in the following chart of quarterly branded salty snacks growth, Utz has demonstrated accelerating momentum in its core business:

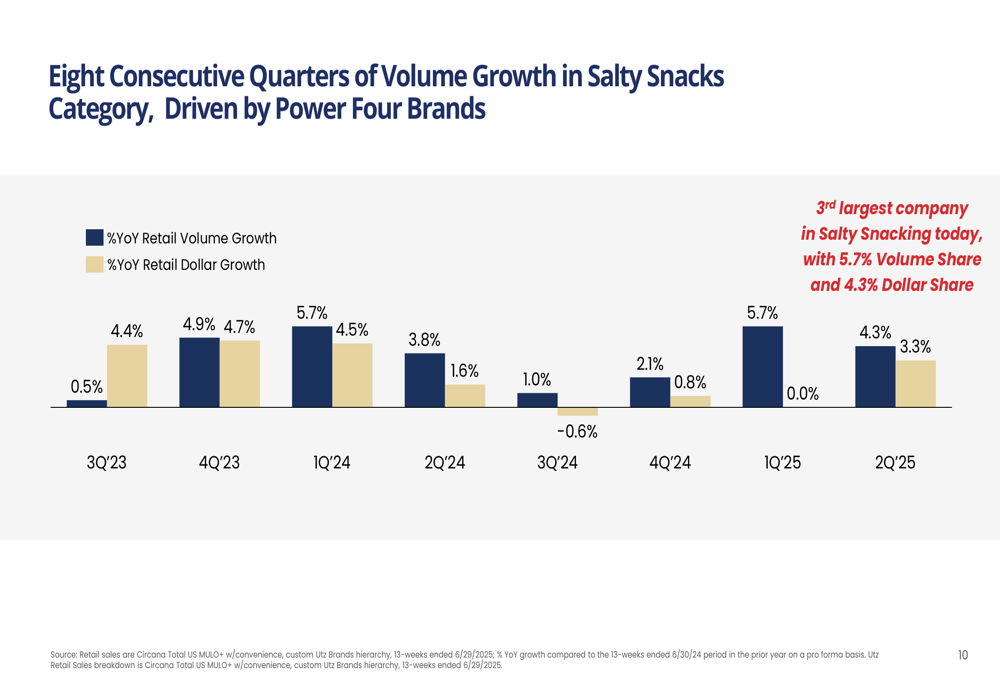

Notably, Utz achieved its eighth consecutive quarter of volume share growth in the salty snacks category. The company now holds a 5.7% volume share and 4.3% dollar share, maintaining its position as the third-largest company in the salty snacking category.

The following chart illustrates Utz’s consistent volume and dollar growth over the past eight quarters:

Supply Chain Transformation

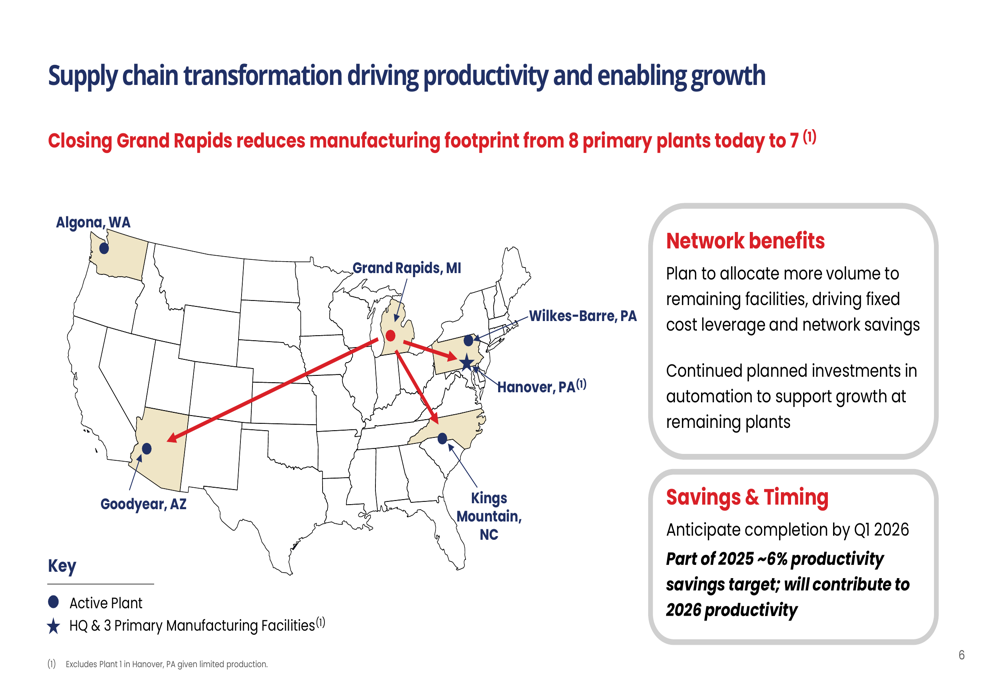

A key strategic announcement in the Q2 presentation was Utz’s plan to further optimize its manufacturing network. The company revealed it will close its Grand Rapids facility, reducing its manufacturing footprint from eight primary plants to seven. This move is part of Utz’s ongoing productivity initiatives.

The company’s manufacturing network optimization strategy is illustrated in this map:

According to the presentation, this consolidation will allow Utz to allocate more volume to its remaining facilities, driving fixed cost leverage and network savings. The company plans to complete this transition by Q1 2026 and expects it to contribute to both its 2025 productivity savings target of approximately 6% and to 2026 productivity.

This supply chain transformation follows similar efficiency initiatives mentioned in previous earnings calls, as the company continues to balance growth investments with operational efficiency.

Detailed Financial Analysis

While Utz delivered solid top-line growth, profitability metrics showed a slight year-over-year decline as the company continued to reinvest in capabilities and distribution expansion to support long-term growth.

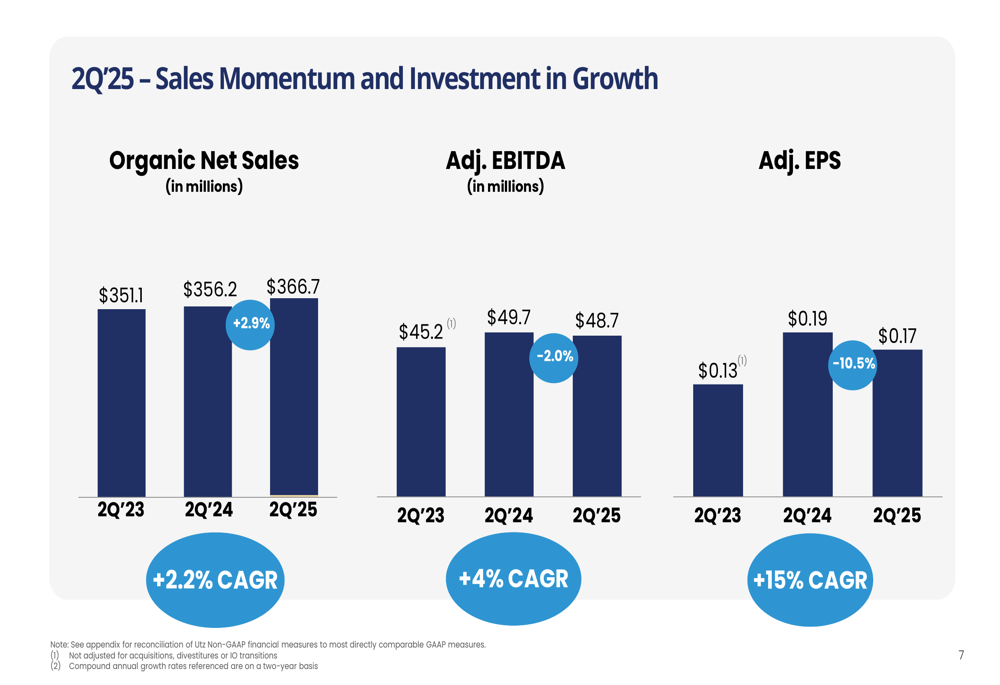

The following chart illustrates the three-year trend in key financial metrics:

Adjusted EBITDA for Q2 2025 was $48.7 million, down 2.0% from $49.7 million in Q2 2024, though still representing a two-year CAGR of 4%. Adjusted EPS came in at $0.17, a 10.5% decrease from $0.19 in the same quarter last year, but maintaining a strong two-year CAGR of 15%.

The company noted that productivity cost savings helped fuel adjusted gross profit margin expansion, but these benefits were partially offset by investments in capabilities and distribution expansion. Management indicated that productivity initiatives are expected to be more second-half weighted.

The drivers of net sales growth are broken down in the following chart:

Forward-Looking Statements

Based on Q2 results, Utz has updated its fiscal year 2025 guidance. The company is now projecting stronger top-line trends while tightening its adjusted EBITDA forecast. However, it has lowered adjusted EPS guidance to account for higher interest expenses and increased depreciation and amortization linked to accelerated capital expenditures.

This guidance update follows the Q1 2025 results, where the company had maintained a focus on distribution gains and innovation within its Boulder Canyon and On the Border brands. The continued emphasis on volume growth rather than price increases aligns with CEO Howard Friedman’s previous statement that "We’ve never been a price-driven business. Consumers come down the aisle because they like the brands, they like the innovation, and they like the marketing."

The company’s focus on productivity initiatives, including the newly announced manufacturing network optimization, suggests a balanced approach to driving both top-line growth and margin improvement in the coming quarters. However, investors will likely continue to monitor the impact of these investments on near-term profitability metrics as Utz positions itself for sustainable long-term growth in the competitive salty snacks category.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.