Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

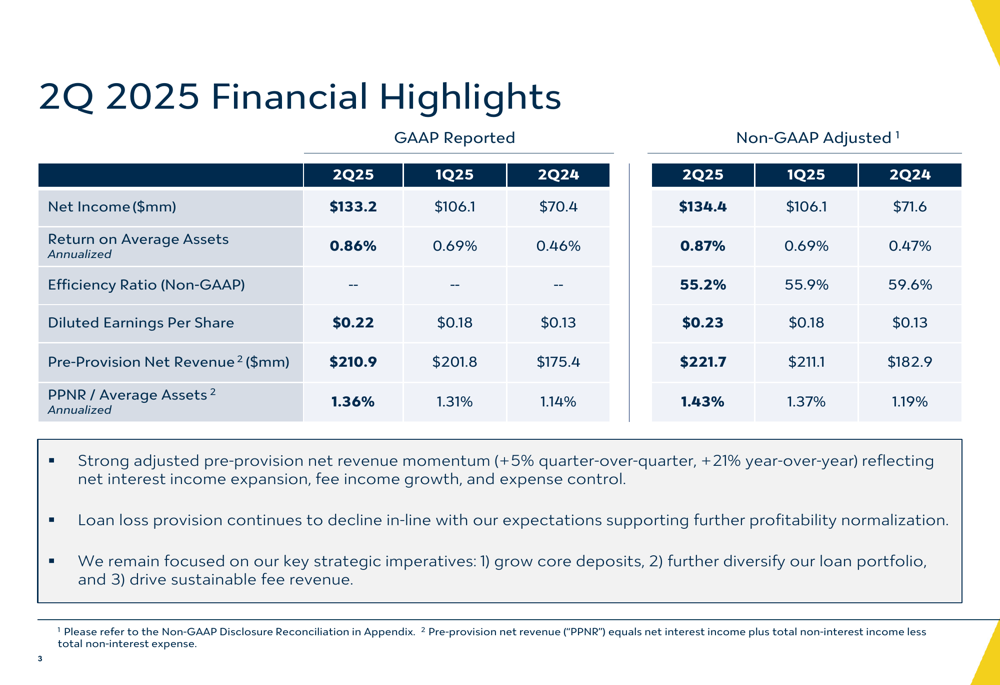

Valley National Bancorp (NASDAQ:VLY) released its second quarter 2025 earnings presentation on July 24, 2025, revealing substantial year-over-year growth in profitability metrics despite a challenging banking environment. The company reported GAAP net income of $133.2 million, representing an 89% increase from the $70.4 million reported in the same quarter last year. Despite the positive results, Valley’s stock saw a 1.9% decline in premarket trading to $10.35, according to market data.

The regional bank has been executing a multi-year strategy focused on deposit growth, loan portfolio diversification, and enhanced fee income generation, which appears to be yielding significant results as reflected in the Q2 performance.

Quarterly Performance Highlights

Valley National reported diluted earnings per share of $0.22 on a GAAP basis and $0.23 on an adjusted basis for Q2 2025, compared to $0.13 per share in Q2 2024. The company’s efficiency ratio improved to 55.2%, down from 59.6% a year ago, indicating better operational efficiency.

As shown in the following comprehensive financial highlights chart, Valley demonstrated improvement across multiple key performance indicators:

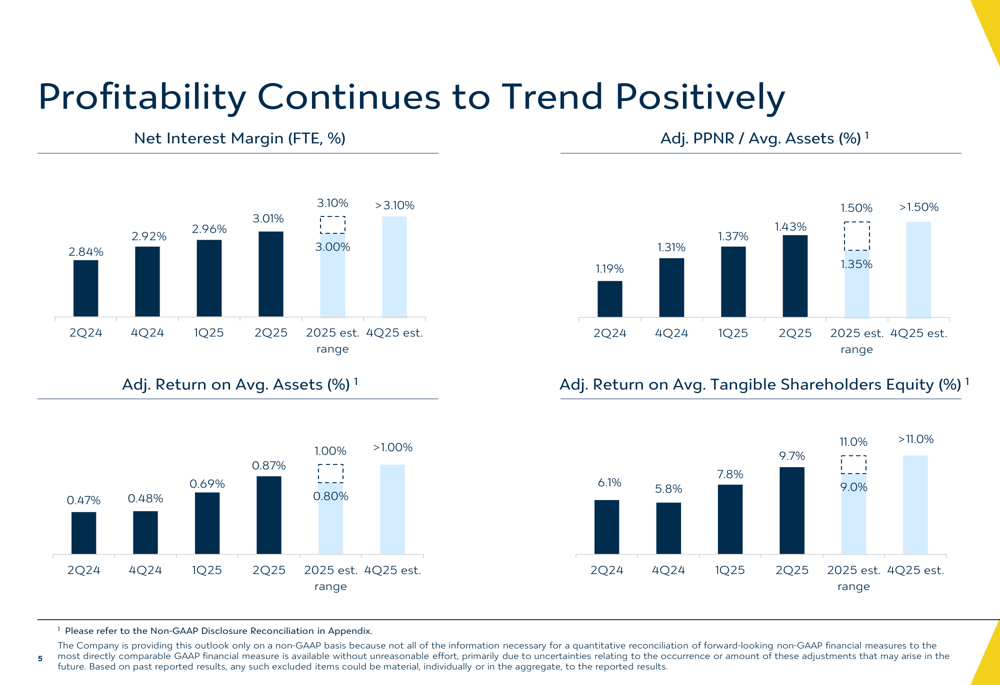

The bank’s net interest margin (NIM) expanded for the fifth consecutive quarter to 3.01%, up from 2.84% in Q2 2024. This improvement in NIM has contributed to stronger net interest income despite a challenging rate environment.

The following chart illustrates Valley’s consistent profitability improvement trends:

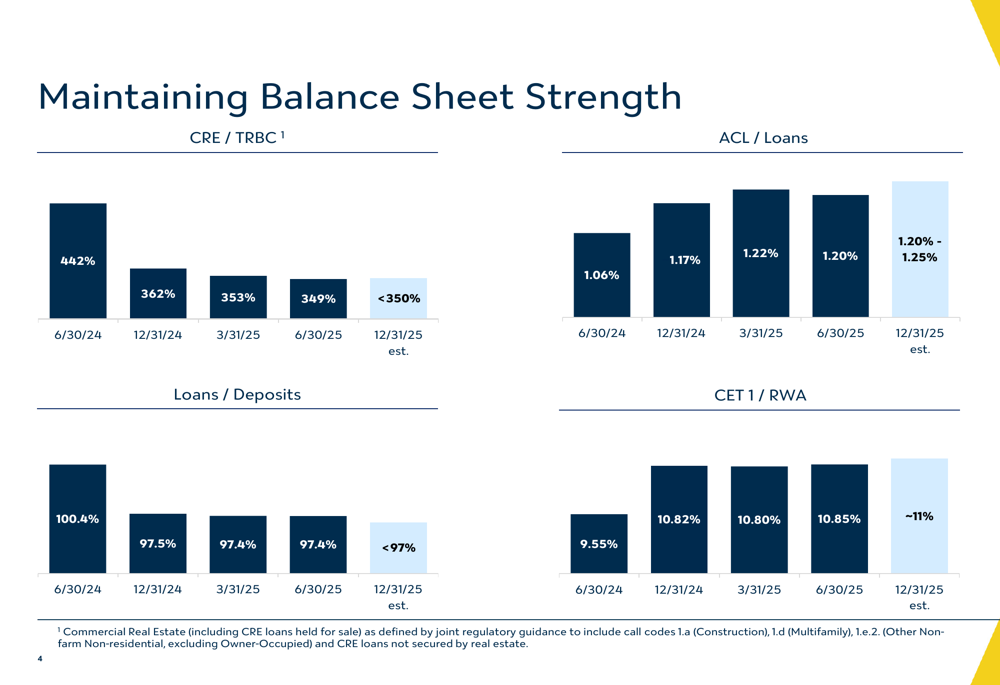

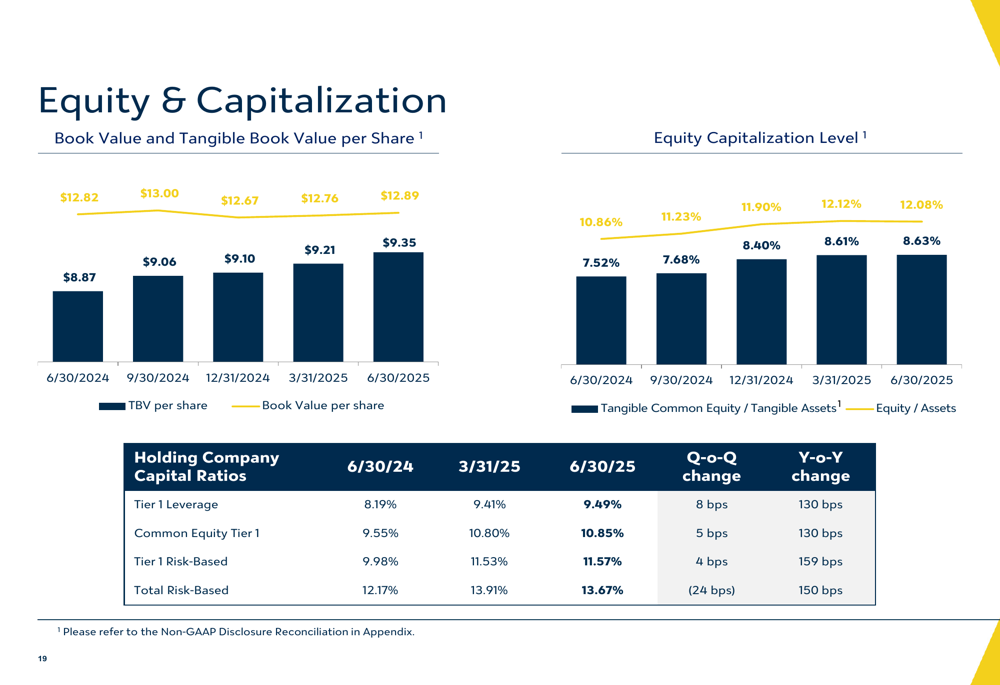

Valley’s balance sheet metrics also showed notable strengthening, with the CET1/RWA ratio improving to 10.85% from 9.55% a year ago, and the loans-to-deposits ratio improving to 97.4% from 100.4% in Q2 2024. The allowance for credit losses (ACL) to loans ratio increased to 1.20% from 1.06% a year earlier, reflecting a prudent approach to potential credit risks.

The following chart demonstrates Valley’s balance sheet strength across key metrics:

Strategic Initiatives

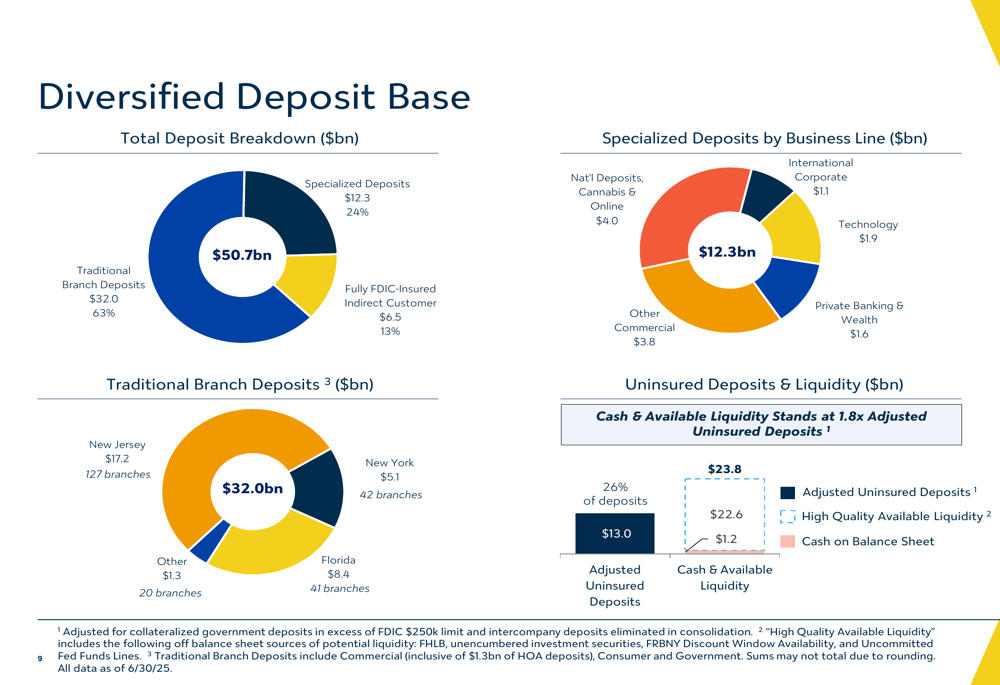

Valley National has been actively diversifying its deposit base, with total deposits reaching $50.7 billion as of June 30, 2025. The bank has significantly reduced its reliance on Northeast branches, which now account for 44% of deposits compared to 78% in 2017, while increasing its presence in the Southeast and through specialty deposit verticals.

As illustrated in the following deposit base breakdown, the bank has created a well-diversified funding structure:

The company has achieved impressive growth in commercial deposit accounts, which increased by 116% since 2017, while consumer deposit accounts grew by 24% during the same period. Direct deposits now represent 87% of total deposits, up from 82% a year ago, reflecting the bank’s focus on building stable core funding.

Valley has also made significant progress in diversifying its loan portfolio, with C&I loans growing at a 19% CAGR since 2017 and now representing 34% of commercial loans, up from 24% in 2017. The geographical distribution of loans has shifted as well, with Florida and other regions now accounting for 48% of commercial loans compared to 21% in 2017.

Non-interest income has been another area of focus, with fee income reaching $62.6 million in Q2 2025. Wealth, trust, and insurance services contributed 28% of this total, while capital markets and deposit service charges represented 16% and 23%, respectively. The bank has achieved a 12% CAGR in non-interest income since 2017, significantly outpacing the peer median of 5%.

Forward-Looking Statements

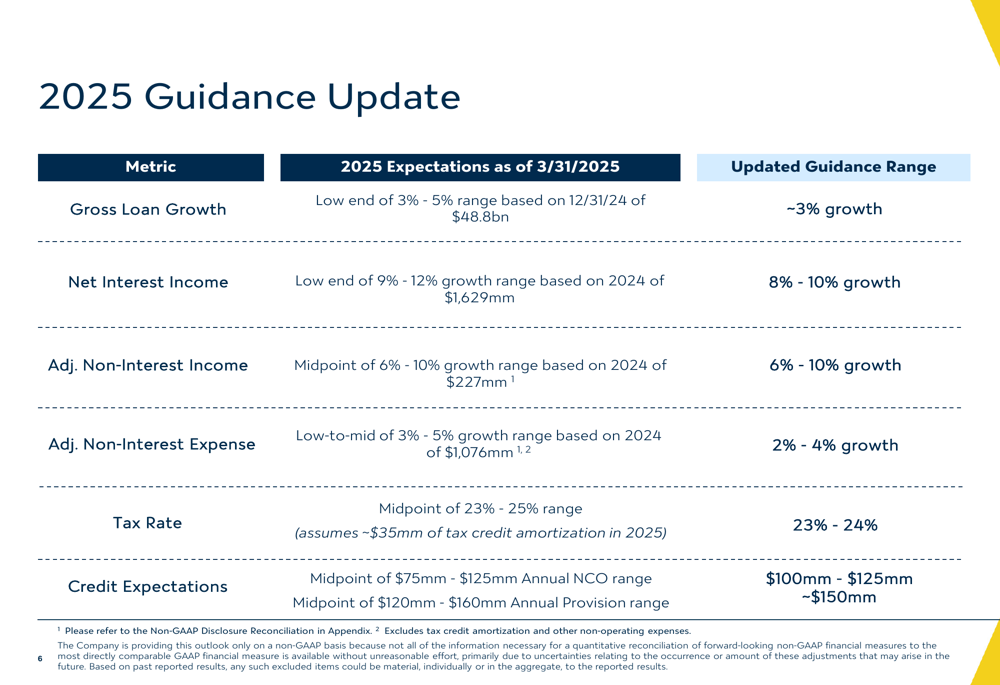

Valley National provided updated guidance for 2025, adjusting some of its previous projections while maintaining an optimistic outlook for continued improvement. The following chart details the updated guidance:

The bank now expects gross loan growth of approximately 3% for 2025, at the low end of its previous 3-5% range. Net interest income growth is projected at 8-10%, slightly below the previous 9-12% forecast. Non-interest expense growth has been revised downward to 2-4% from 3-5%, reflecting improved cost control.

Looking further ahead, Valley is targeting a return on average assets exceeding 1.00% by the fourth quarter of 2025, up from 0.87% in Q2 2025. The bank also aims to achieve a net interest margin above 3.10% and an adjusted pre-provision net revenue to average assets ratio exceeding 1.50% by year-end.

"We think we’ll definitely get our fair share of the technology market," CEO Ira Robbins stated during the earnings call, highlighting the company’s strong position in technology and healthcare sectors. He also noted the company’s historical success in healthcare lending, saying, "We have never taken a loss on any Valley-originated healthcare C&I loans over this 20-year period."

Valley’s equity position continues to strengthen, with tangible book value per share showing consistent growth and tangible common equity to tangible assets improving to 8.63% as of June 30, 2025, up from 7.52% a year earlier.

The following chart illustrates Valley’s improving equity and capitalization metrics:

While Valley National’s presentation paints a positive picture of its performance and outlook, the bank still faces potential challenges from macroeconomic pressures, intense competition in the technology banking sector, and potential interest rate volatility. However, the significant improvements in profitability metrics and balance sheet strength position the company well to navigate these challenges while continuing to execute its strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.