Goldman Sachs reiterates Buy on Xiaomi stock as 17 Pro Max drives sales

Introduction & Market Context

Veidekke ASA (OB:VEI), one of Scandinavia’s largest construction and civil engineering companies, presented its second quarter 2025 results on August 14, 2025. The company reported solid growth figures amid what appears to be improving market conditions across its Nordic operations. Veidekke’s stock closed at NOK 170 on August 13, 2025, showing a modest 0.24% increase ahead of the earnings announcement.

The presentation, delivered by Group CEO Jimmy Bengtsson and CFO Jørgen Wiese Porsmyr, highlighted Veidekke’s continued focus on project selectivity and execution quality, which has contributed to both revenue growth and margin improvement during the quarter.

Quarterly Performance Highlights

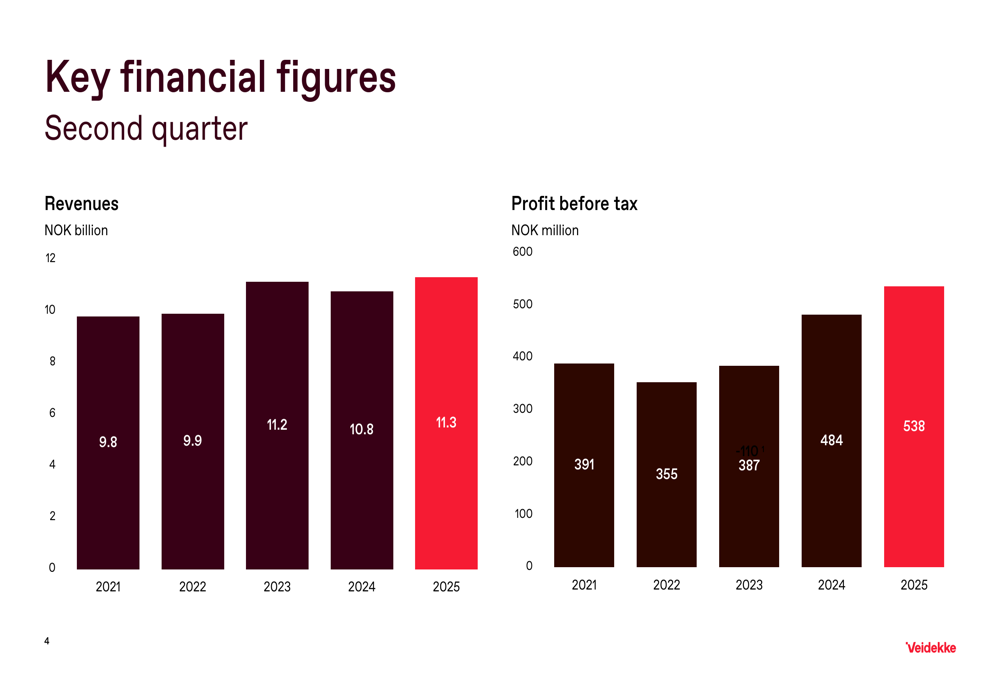

Veidekke reported revenues of NOK 11.3 billion for Q2 2025, representing a 5% increase compared to Q2 2024. Profit before tax reached NOK 538 million, up from NOK 484 million in the same period last year, while the profit margin improved to 4.7% from 4.5%.

As shown in the following chart of key financial figures, Veidekke has demonstrated consistent revenue growth over the past five years, with profits reaching their highest level in the current quarter:

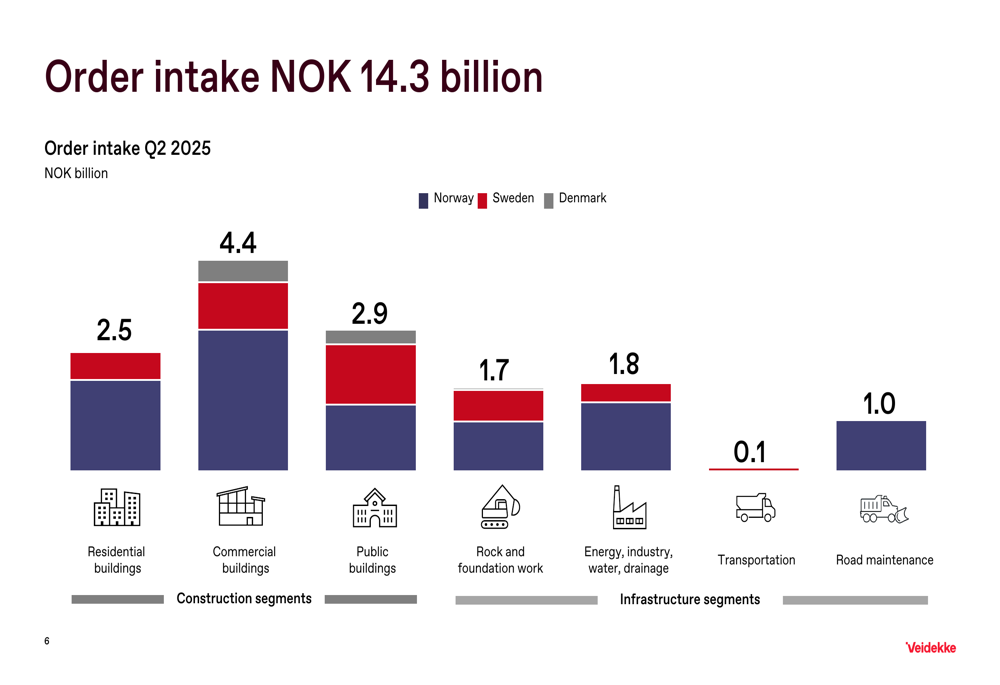

A particularly notable achievement was the strong order intake of NOK 14.3 billion during the quarter, which helped boost the company’s order book to NOK 49.2 billion – a 20% increase year-to-date. This robust order intake spans multiple segments, with commercial buildings representing the largest portion at NOK 4.4 billion.

The following breakdown illustrates the composition of Veidekke’s Q2 2025 order intake across different construction segments:

Detailed Financial Analysis

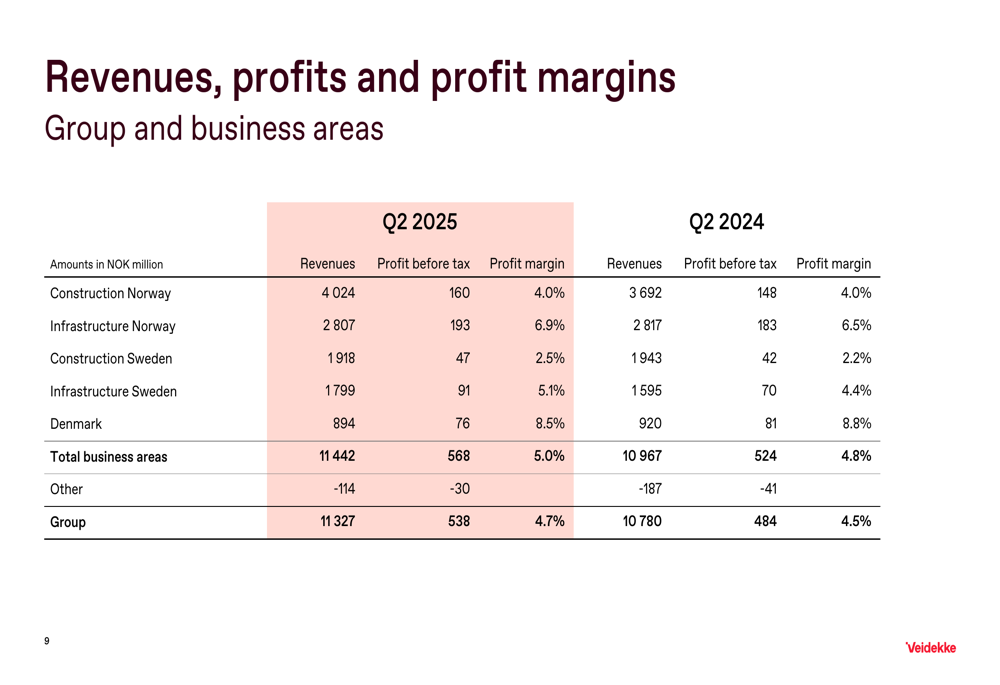

When examining performance by business segment, Construction Norway emerged as the strongest performer with revenues up 9% compared to Q2 2024 and a significant 28% increase in its order book during the quarter. Several major projects contributed to this growth, including a NOK 2.3 billion contract with Kongsberg and a NOK 1.3 billion project with Statnett.

The following table provides a comprehensive breakdown of revenues, profits, and profit margins across all business segments:

Results were more mixed in other regions. Construction Sweden reported a 7% revenue decline in local currency but managed to increase profits by 8%. Meanwhile, Denmark operations saw both revenue (down 4%) and profits decrease compared to Q2 2024.

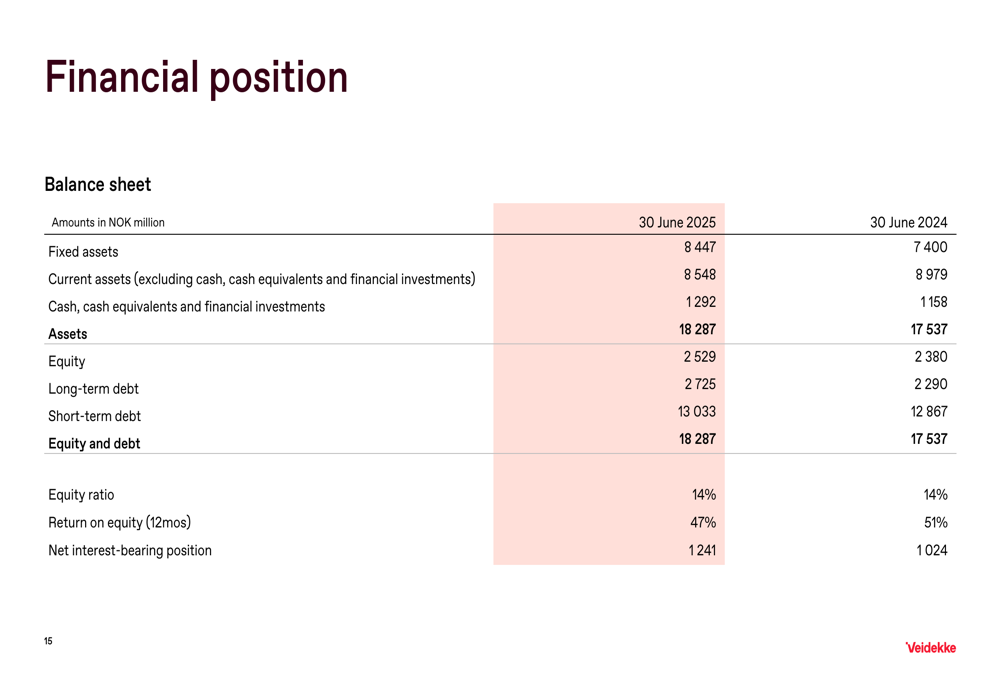

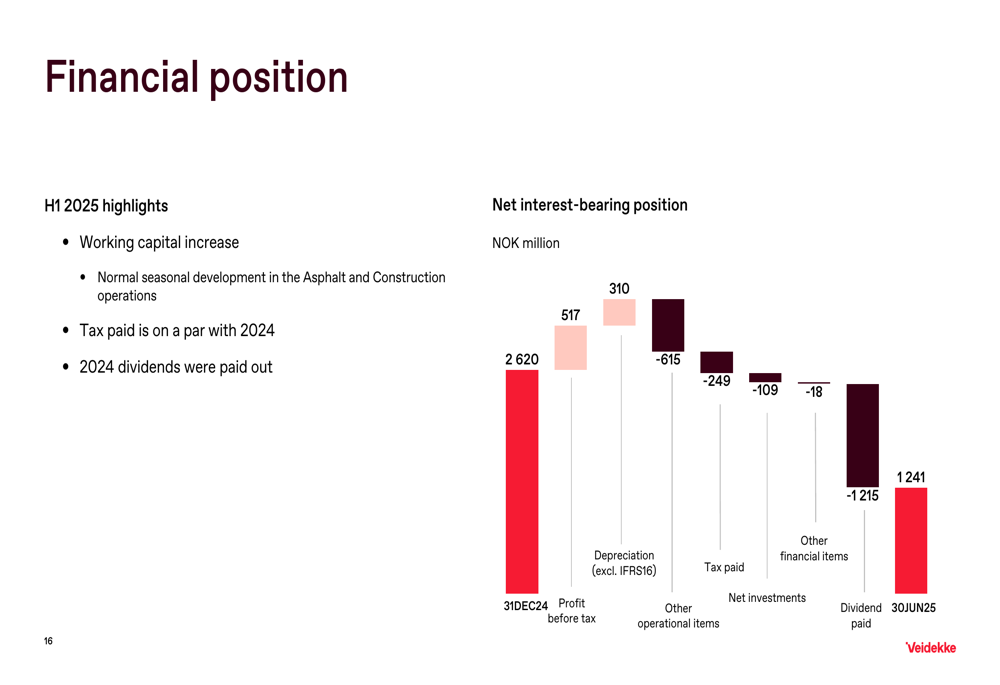

From a balance sheet perspective, Veidekke maintained a solid financial position with total assets of NOK 18.3 billion as of June 30, 2025, compared to NOK 17.5 billion a year earlier. The company’s equity ratio stood at 13.8%.

The detailed balance sheet figures show Veidekke’s financial position remains strong:

The company’s net interest-bearing position amounted to NOK 1,241 million, reflecting working capital increases, tax payments, and dividends paid during the first half of 2025:

Strategic Initiatives

Veidekke’s management emphasized several strategic priorities during the presentation. These include maintaining selectivity in project selection, ensuring proper risk management, and improving capacity utilization across the organization.

The company specifically highlighted its intention to increase civil engineering activities in Norway and implement improvement measures in underperforming units. Management noted that uncertainty management during project execution remains a vital factor in reducing project risk and potential losses.

Forward-Looking Statements

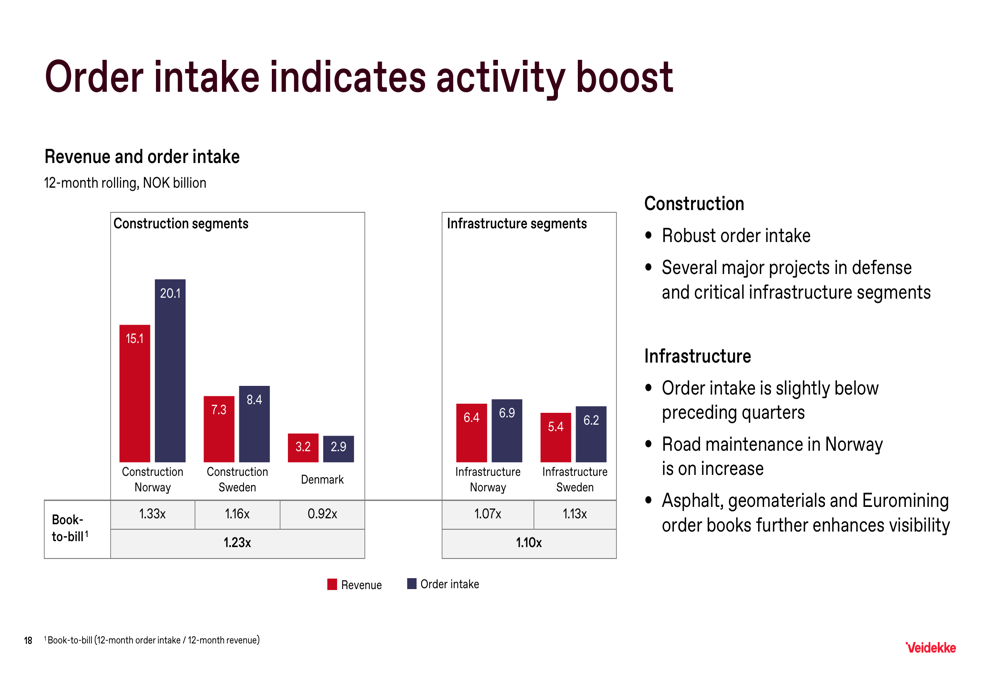

Looking ahead, Veidekke’s order intake suggests an upcoming boost in activity levels. The company reported favorable order-to-bill ratios across most segments, with Construction Norway leading at 1.33x, followed by Construction Sweden at 1.16x and Infrastructure Sweden at 1.13x.

The following chart illustrates how current order intake positions Veidekke for future growth:

Management expressed confidence in the company’s positioning for market improvement, citing its solid order book and quality project portfolio. The presentation concluded with a summary of key takeaways, emphasizing both the 5% revenue growth and the substantial 20% year-to-date increase in the order book to NOK 49 billion.

Veidekke’s focus on quality projects and risk management appears to be yielding results, though management acknowledged there is still potential for improvement, particularly in underperforming units.

With its strong order book and improving profit margins, Veidekke appears well-positioned to capitalize on construction and infrastructure opportunities across the Nordic region through the remainder of 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.