Street Calls of the Week

Introduction & Market Context

Veolia Environnement VE SA (EPA:VIE) presented its H1 2025 results on July 31, 2025, reporting solid performance across all business segments despite challenging macroeconomic conditions. The environmental services giant delivered results in line with its annual guidance, showcasing the resilience of its business model.

The company’s stock closed at €30.25 on July 30, down 1.01% ahead of the results announcement, reflecting broader market caution. Year-to-date, Veolia’s shares have shown strong momentum with a 19.62% gain, according to previous earnings data.

CEO Estelle Brachlianoff emphasized the company’s resilient business model during the presentation, stating that Veolia is "85% macro-immune" due to its diversified geographic footprint and long-term contract structure.

Quarterly Performance Highlights

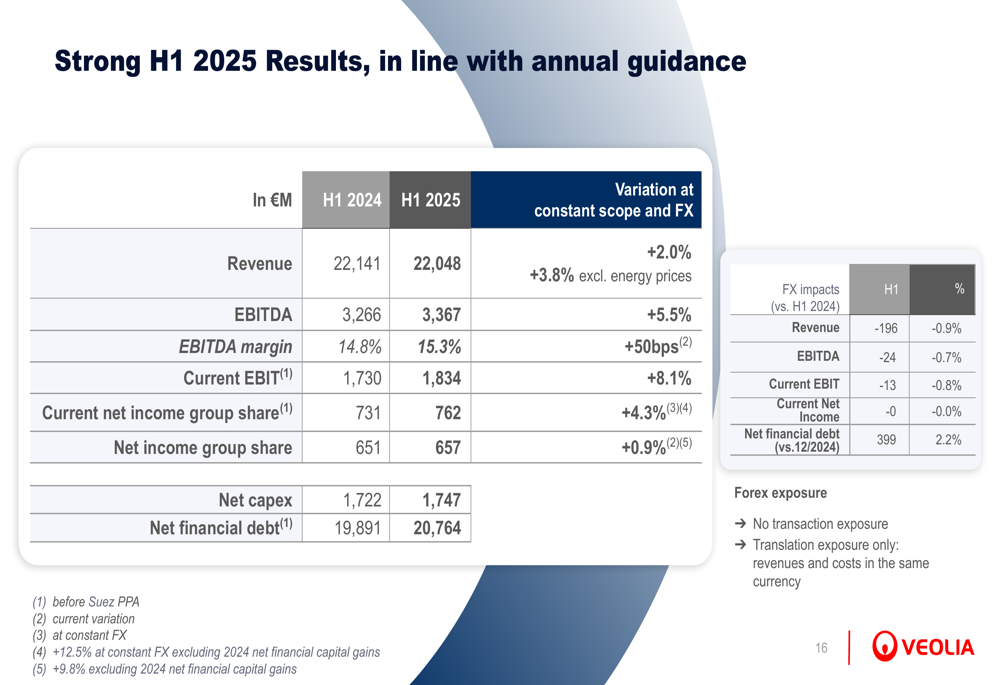

Veolia reported H1 2025 revenue of €22,048 million, up 3.8% excluding energy prices at constant scope and forex. EBITDA reached €3,367 million, increasing 5.5% with an improved margin of 15.3% (up 50 basis points year-over-year). Current EBIT grew 8.1% to €1,834 million, while current net income rose 4.3% to €762 million.

As shown in the following comprehensive financial overview from the presentation:

Performance was driven by solid organic growth across all segments, with particularly strong results in the company’s strategic "booster" businesses, which grew 8.9% including targeted M&A. The company’s efficiency program delivered €191 million in gains during H1, while synergies from the Suez merger contributed an additional €47 million.

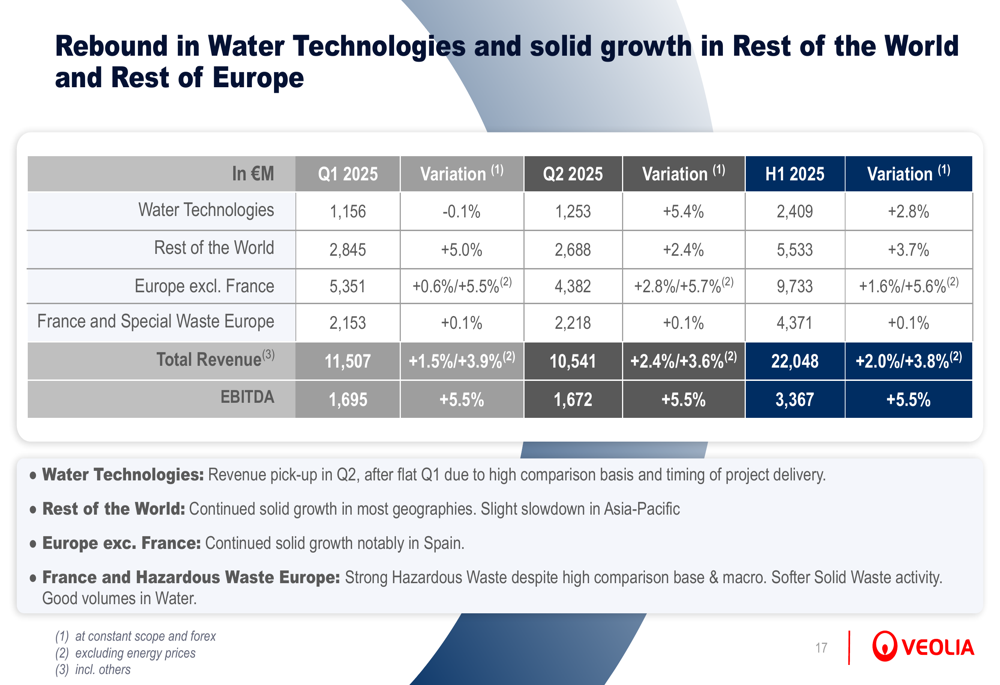

The geographic breakdown of revenue and EBITDA shows balanced growth across regions:

Veolia’s core "stronghold" activities showed consistent growth, with Water Operations revenue up 3.6% to €6,135 million, Solid Waste revenue increasing 1.5% to €5,597 million, and District Heating Networks revenue growing 5.1% to €3,770 million (excluding energy prices).

The company’s strategic "booster" businesses demonstrated even stronger performance, as illustrated in the presentation:

Strategic Initiatives

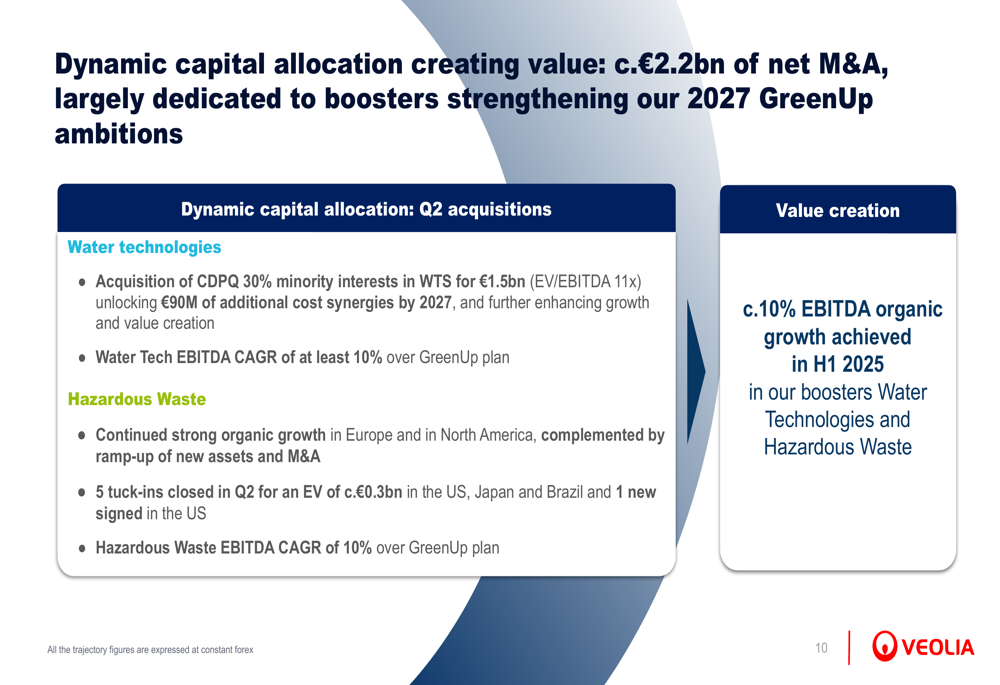

A key highlight of the H1 2025 results was Veolia’s dynamic capital allocation strategy, with approximately €2.2 billion dedicated to net M&A activities primarily focused on strengthening the company’s "booster" businesses under its GreenUp strategic plan.

The most significant transaction was the acquisition of CDPQ’s 30% minority interest in Water Technologies Services (WTS), which aligns with the Q1 announcement and strengthens Veolia’s position in this high-growth segment. This strategic move is expected to unlock additional synergies and accelerate growth in the water technology sector.

As shown in the capital allocation slide:

The company has ambitious plans for its Water Tech business, targeting 6-10% CAGR in revenues and ≥10% CAGR in EBITDA through 2027, with the goal of increasing water tech revenues by 50% by 2030. A particular focus is on PFAS treatment, where Veolia aims to generate approximately €1 billion in revenues by 2030.

Similarly, in Hazardous Waste, Veolia is targeting mid to high single-digit revenue growth and approximately 10% EBITDA growth through 2027, with plans to increase capacity by 285 kilotons and grow hazardous waste revenues by 50% by 2030.

Detailed Financial Analysis

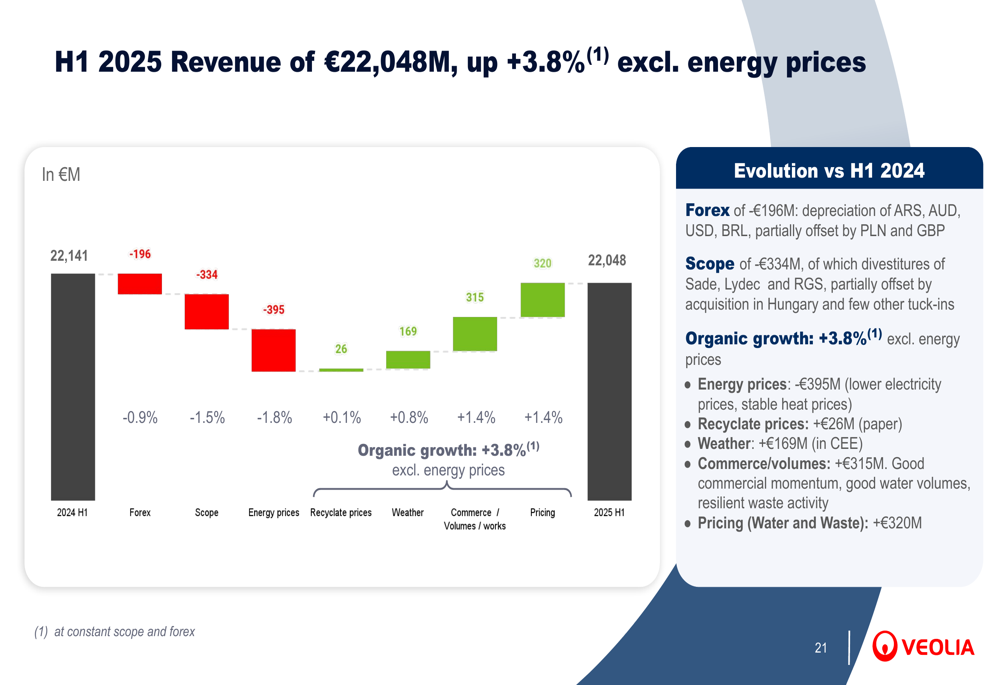

A deeper analysis of Veolia’s H1 2025 revenue shows the various factors contributing to the 3.8% growth (excluding energy prices):

The positive impact from commerce/volumes/works (+1.4%), pricing (+2.0%), and weather (+0.7%) more than offset the negative impact from energy prices (-1.7%). This demonstrates the company’s ability to grow organically despite volatile energy markets.

Similarly, EBITDA growth of 5.5% was driven by multiple factors:

Efficiency gains and synergies contributed €191 million and €47 million respectively, while commerce/volumes/works added €151 million. These positive factors more than compensated for the negative impact from energy and recycled prices (-€38 million).

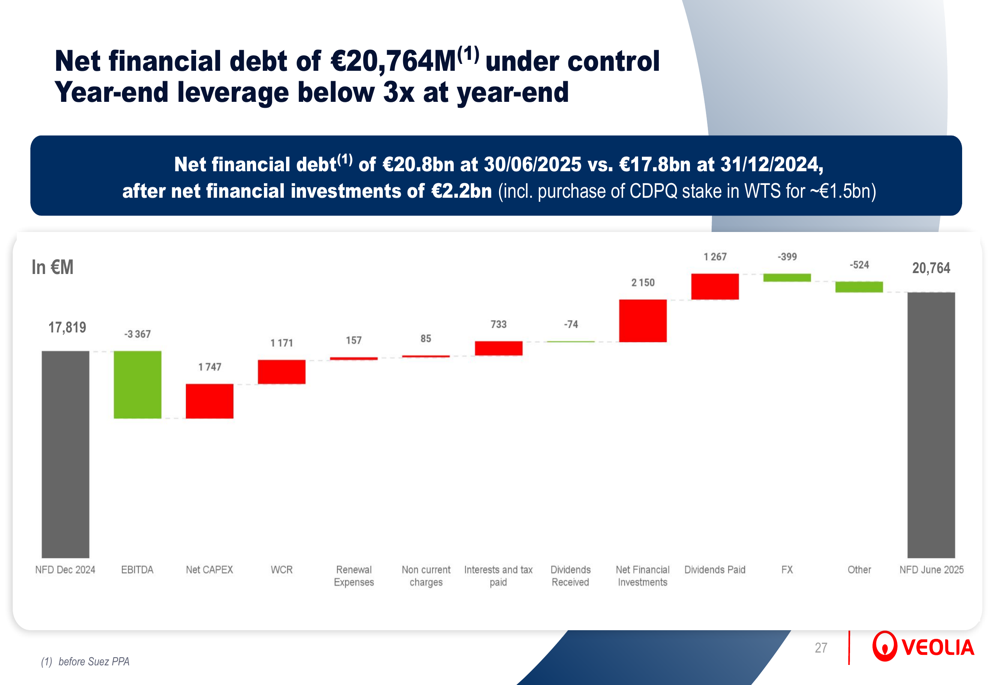

Net financial debt stood at €20,764 million, reflecting the significant M&A activity during the period:

Despite the substantial investments, Veolia maintained its leverage ratio below 3x, in line with its financial policy. The company also successfully refinanced its debt, with 90% at fixed rates, and maintained its strong investment grade ratings from both Moody’s and Standard & Poor’s.

Forward-Looking Statements

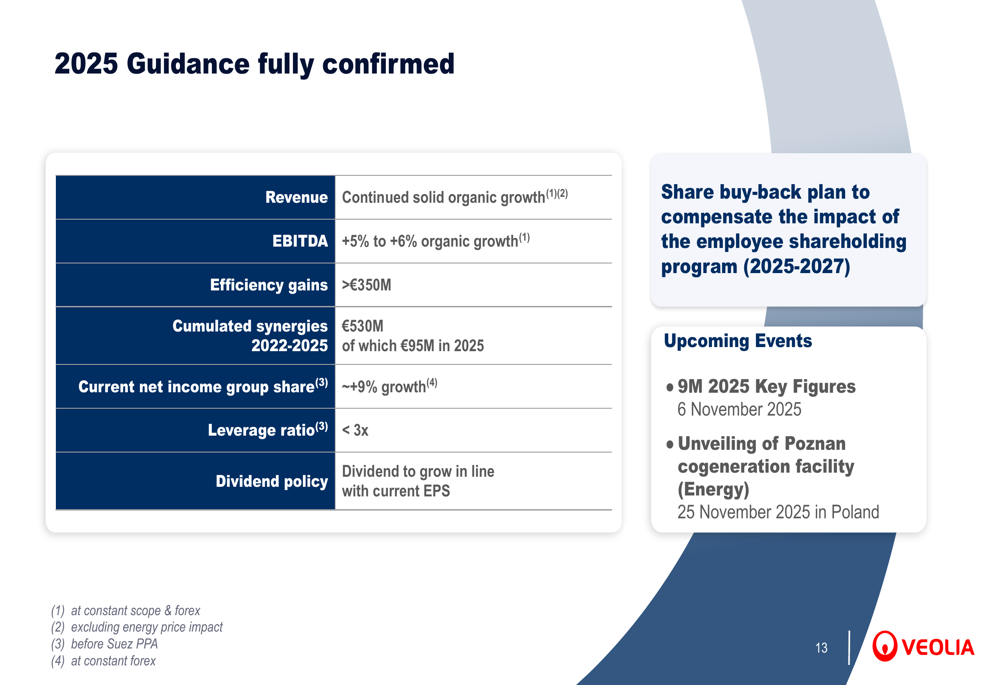

Veolia confidently reaffirmed its 2025 guidance and long-term GreenUp targets, demonstrating management’s confidence in the company’s strategy and execution capabilities.

For 2025, Veolia expects:

- Continued solid organic revenue growth

- EBITDA organic growth of 5-6%

- Efficiency gains exceeding €350 million

- Cumulated synergies of €530 million by year-end (including €95 million in 2025)

- Current net income growth of approximately 9%

- Leverage ratio below 3x

- Dividend growth in line with current EPS

As illustrated in the guidance slide:

Looking further ahead, Veolia confirmed its GreenUp targets through 2027, including:

- EBITDA of at least €8 billion by 2027

- Leverage ratio maintained at or below 3x

- Current net income growth of approximately 10% CAGR over 2023-2027

The company’s value creation strategy combines growth in both boosters and strongholds, operational performance improvements through efficiency and synergies, and disciplined capital allocation:

"Our resilient and growth business model enables us to fully confirm our guidance," stated CEO Estelle Brachlianoff during the presentation, echoing similar comments from the Q1 earnings call where she emphasized the company’s resilience against macroeconomic challenges.

With its strategic focus on high-growth boosters, continued operational improvements, and disciplined financial management, Veolia appears well-positioned to deliver on its short and long-term targets despite the uncertain global economic environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.