Gold prices edge higher on raised Fed rate cut hopes

Introduction & Market Context

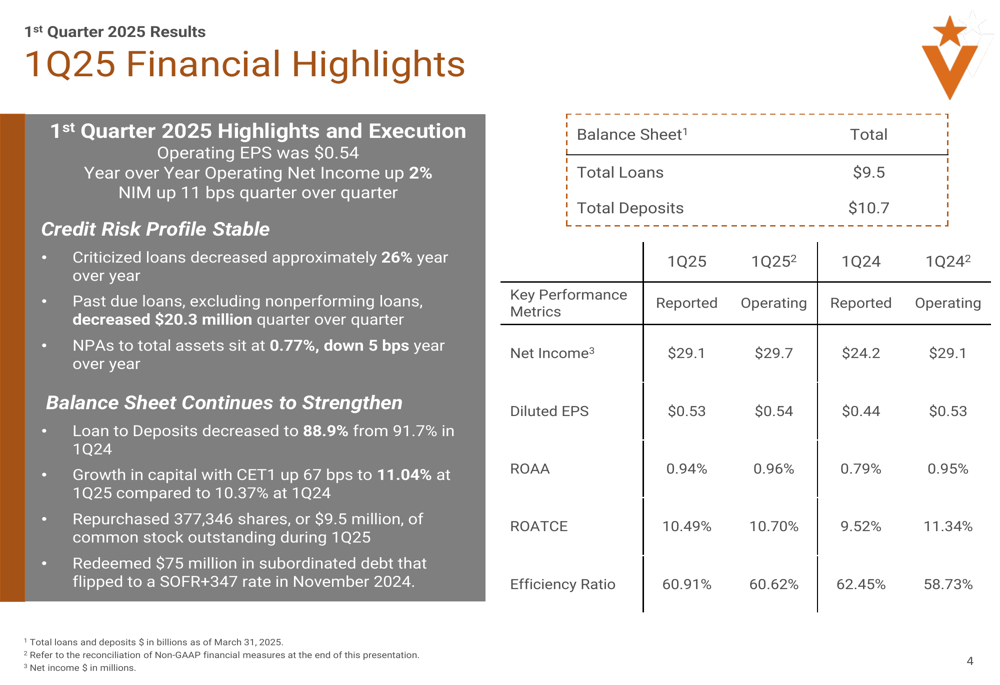

Veritex Holdings Inc (NASDAQ:VBTX) released its first quarter 2025 earnings presentation on April 23, 2025, highlighting continued balance sheet strengthening, credit quality improvement, and net interest margin expansion. The Texas-based regional bank reported operating EPS of $0.54, with operating net income up 2% year-over-year, as the company maintains its strategic focus on achieving a 1% return on assets in 2025.

Trading at $22.78 in the aftermarket session, up 2.98% following the release, Veritex continues to execute on its transformation strategy that began in 2024, when the company prioritized balance sheet restructuring over earnings growth.

Quarterly Performance Highlights

Veritex reported stable operating earnings with Q1 2025 operating EPS at $0.54, matching the previous quarter’s performance but representing a 2% year-over-year increase in operating net income. The company’s net interest margin expanded by 11 basis points quarter-over-quarter to 3.31%, reflecting improved asset yields and deposit cost management.

As shown in the following financial highlights table, the company improved key profitability metrics compared to the same period last year:

The bank’s efficiency ratio improved to 60.91% from 62.45% in Q1 2024, while return on average tangible common equity (ROATCE) increased to 10.49% from 9.52% a year earlier. These improvements align with management’s previous guidance from Q4 2024, when they emphasized their focus on returning to a 1% ROA in 2025.

Credit Quality and Balance Sheet Strength

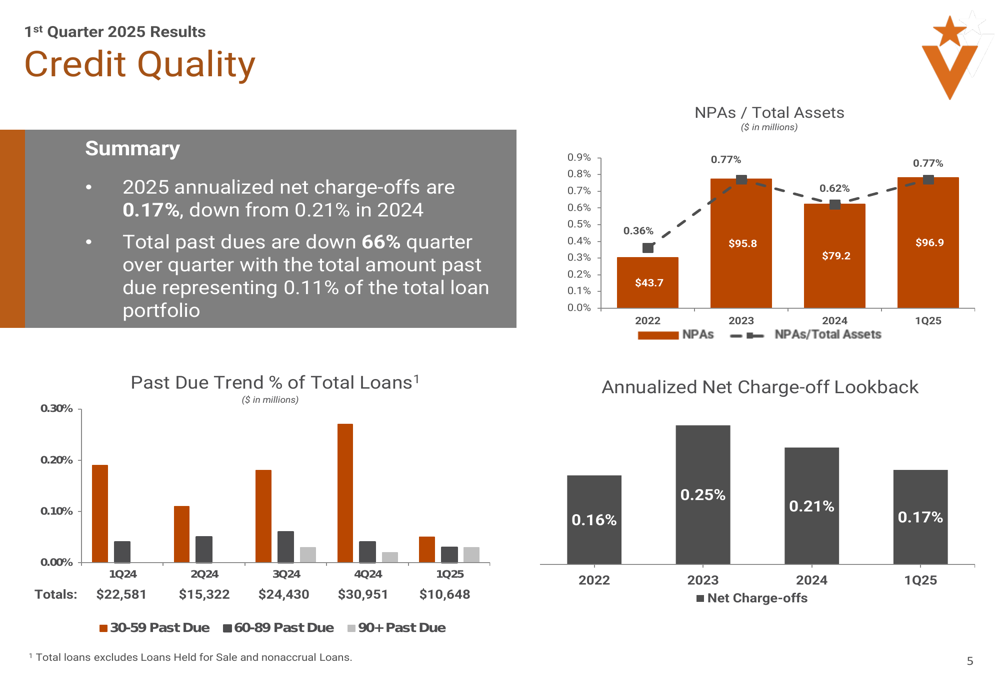

A significant highlight of Veritex’s Q1 2025 presentation was the continued improvement in credit quality metrics. Annualized net charge-offs decreased to 0.17% from 0.21% in 2024, while total past due loans declined by 66% quarter-over-quarter, representing just 0.11% of the total loan portfolio.

The following chart illustrates the bank’s improving credit quality trends:

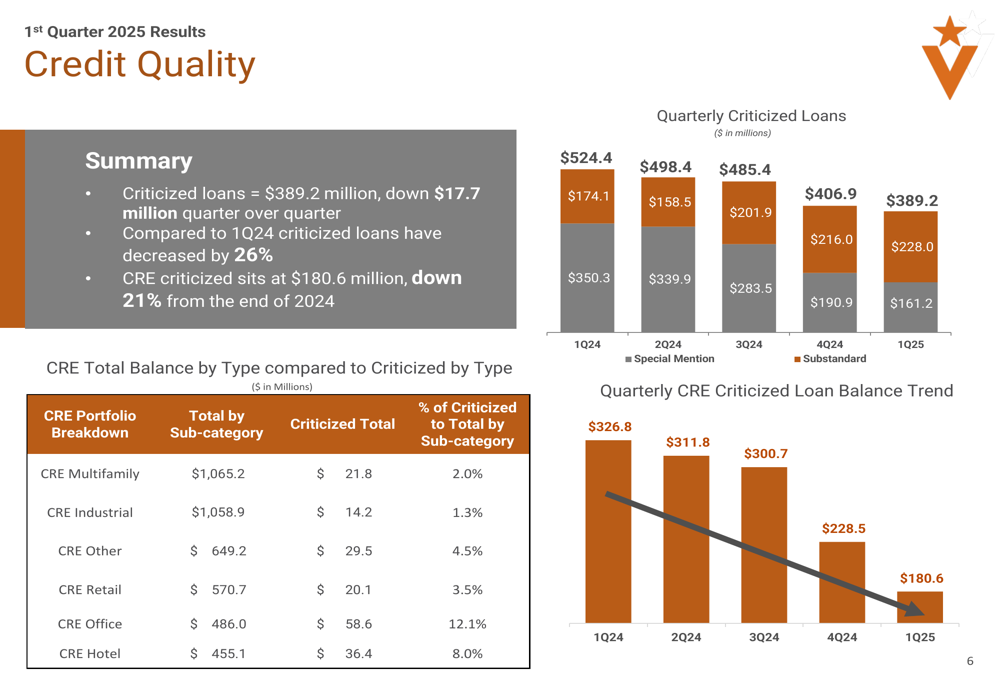

Criticized loans, a key indicator of potential problem assets, totaled $389.2 million, down $17.7 million quarter-over-quarter and a substantial 26% decrease from Q1 2024. The commercial real estate (CRE) portfolio, which has been an area of focus for many regional banks, showed particular improvement:

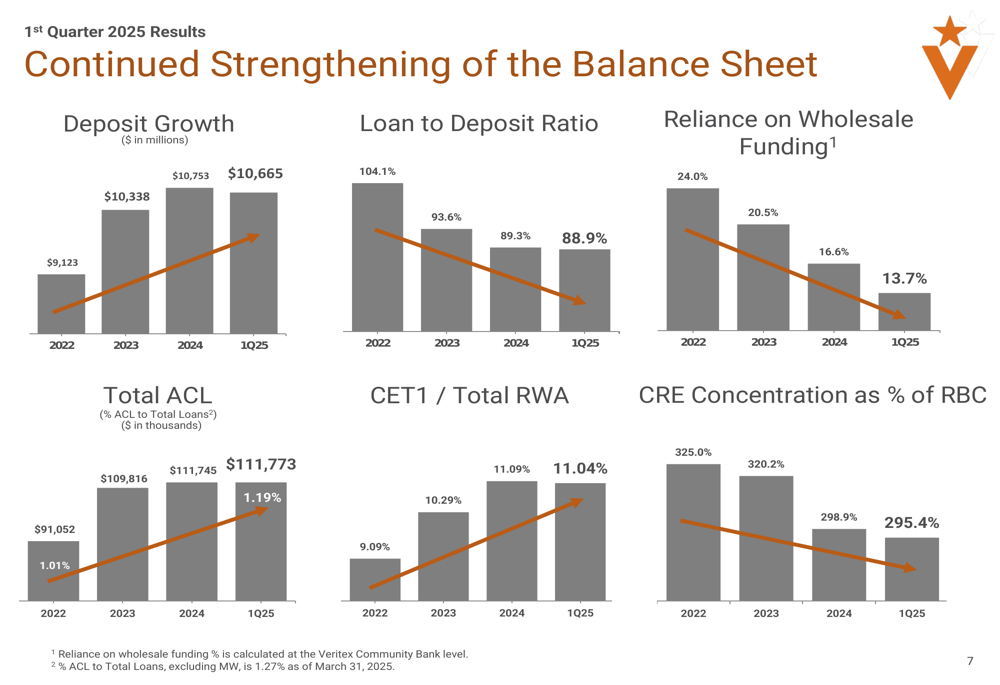

Veritex has also made significant progress in strengthening its balance sheet, with deposit growth increasing from $9.1 billion to $10.7 billion and the loan-to-deposit ratio decreasing from 104.1% to a more conservative 88.9%. This improvement reduces the bank’s reliance on wholesale funding, which declined from 24% to 13.7%.

The following chart demonstrates these balance sheet improvements:

Capital Management and Strategic Initiatives

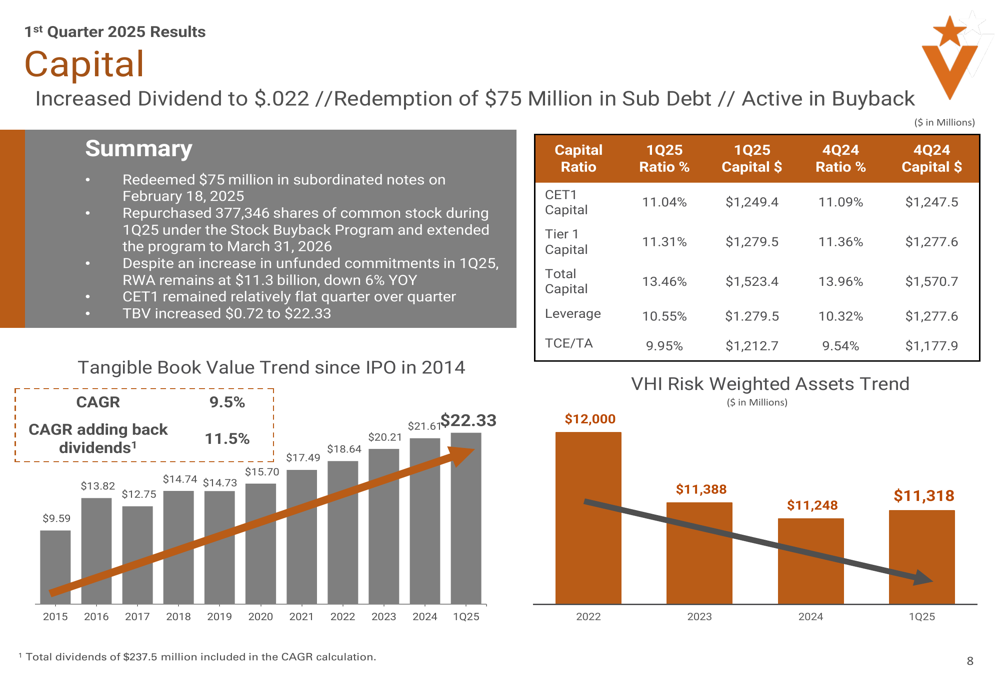

During Q1 2025, Veritex continued to enhance its capital position while returning value to shareholders. The company increased its dividend to $0.022 per share, repurchased 377,346 shares totaling $9.5 million, and redeemed $75 million in subordinated debt. The CET1 ratio improved to 11.04%, up 67 basis points from the previous year.

The following chart shows the company’s tangible book value growth trend since its IPO:

Veritex maintained a disciplined approach to loan growth, with total loans decreasing approximately $104 million in Q1 2025 due to strong paydowns in CRE and ADC (Acquisition, Development, and Construction) loans. This aligns with management’s guidance from previous quarters about anticipated paydowns and their focus on quality over quantity in loan growth.

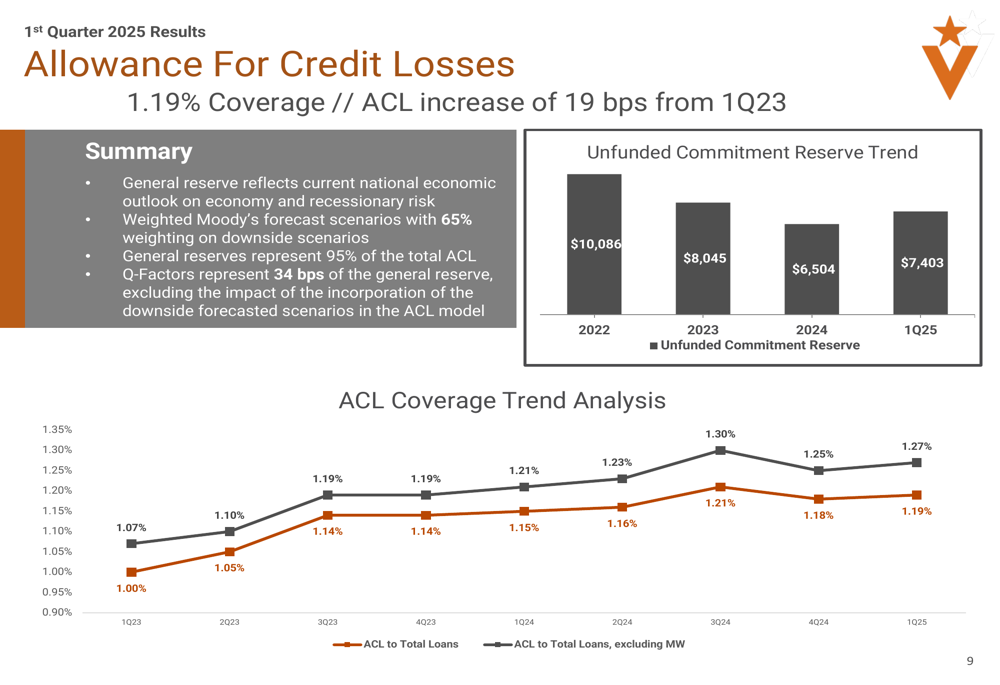

The bank’s allowance for credit losses (ACL) stands at 1.19%, representing a 19 basis point increase from Q1 2023, reflecting a conservative approach to potential economic uncertainties:

Liquidity and Investment Portfolio

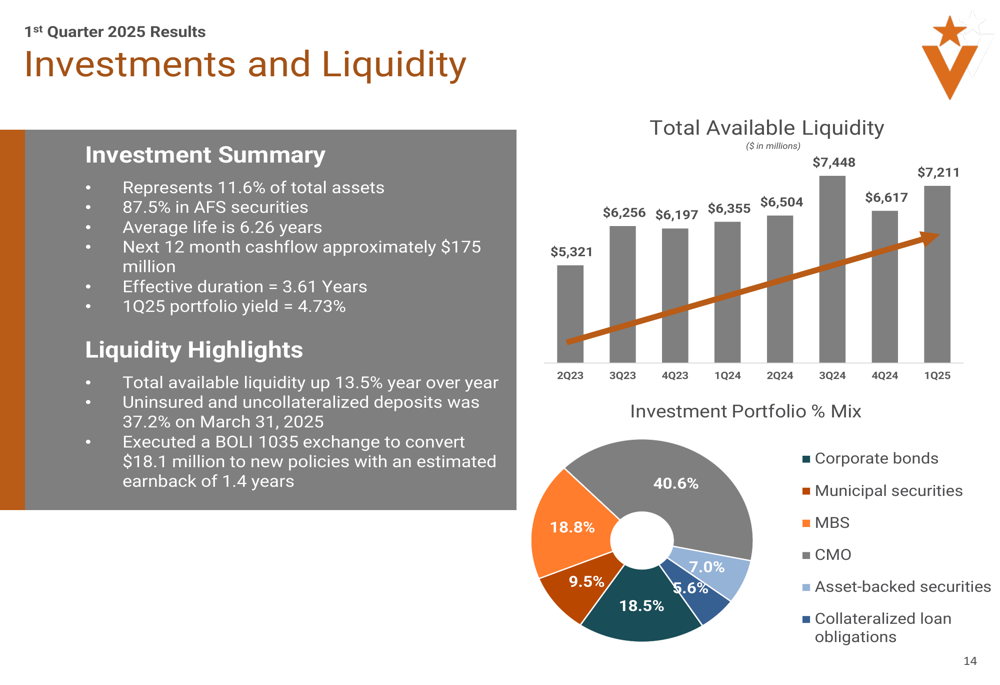

Veritex’s investment portfolio accounts for 11.6% of total assets, with 87.5% classified as available for sale (AFS). The company maintains strong liquidity, positioning it well for potential growth opportunities while providing a buffer against market uncertainties.

As shown in the following chart, the bank has a diversified investment portfolio and substantial available liquidity:

Forward-Looking Statements

Looking ahead, Veritex appears well-positioned to achieve its target of a 1% ROA in 2025, building on the foundation established through its balance sheet transformation in 2024. The company’s focus on disciplined loan growth, deposit cost management, and fee income expansion aligns with the strategy outlined in previous quarters.

This outlook is consistent with management’s comments from the Q4 2024 earnings call, where CEO Malcolm Holland emphasized, "We are laser focused and committed to return on average asset levels in excess of 1% in 2025 and beyond." The Q1 2025 results show progress toward this goal, with improved NIM, strengthened capital ratios, and enhanced credit quality.

While loan paydowns continue to present a challenge for growth, the company’s strong deposit franchise and improved balance sheet position it well to capitalize on opportunities in its Texas markets. The bank’s reduced reliance on wholesale funding and improved loan-to-deposit ratio provide flexibility as it navigates the evolving interest rate environment.

Investors will likely focus on Veritex’s ability to maintain NIM expansion, generate fee income growth, and achieve positive operating leverage in the coming quarters as key indicators of progress toward its 1% ROA target.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.