Gold prices edge up amid Fed rate cut hopes; US-Russia talks awaited

Introduction & Market Context

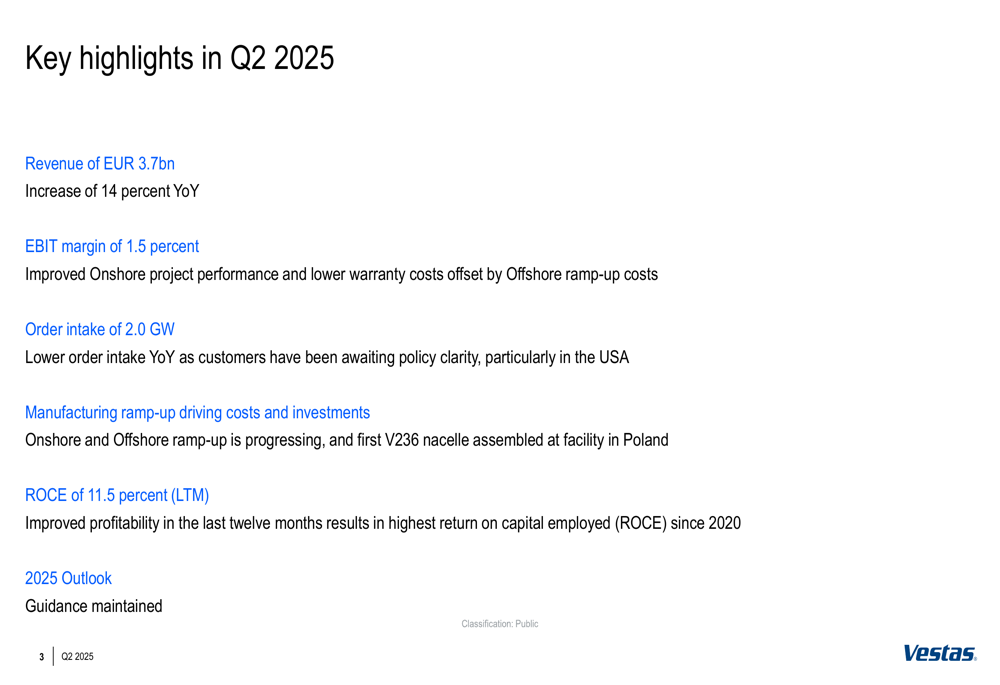

Vestas Wind Systems A/S (ETR:VWSB) (CPH:VWS) reported second-quarter 2025 financial results showing revenue growth of 14% year-over-year, reaching €3.7 billion, despite facing significant challenges in order intake. The Danish wind turbine manufacturer continues to navigate a complex market environment characterized by stable raw material costs but increasing tariffs and ongoing geopolitical volatility.

The company highlighted that while inflation and transport costs have stabilized, the wind energy sector continues to face challenges related to permitting processes, auction designs, and market structures. However, there is an increasing focus on energy security and affordability across global markets, which presents opportunities for renewable energy providers like Vestas.

Quarterly Performance Highlights

Vestas achieved an EBIT margin of 1.5% in Q2 2025, showing improvement from the 0.4% reported in Q1 2025. This progress was primarily driven by better performance in onshore projects. The company’s return on capital employed (ROCE) reached 11.5% on a last-twelve-months basis, reflecting strengthened operational efficiency.

As shown in the following financial highlights slide, the company maintained its full-year guidance despite the mixed quarterly results:

Order intake declined significantly to 2.0 GW, representing a 44% decrease year-over-year. This drop was primarily attributed to customers in the Americas, particularly in the United States, awaiting greater policy clarity before committing to new projects. The average selling price (ASP) also declined to €1.11 million per MW in Q2, down from €1.24 million per MW in the previous quarter.

However, the company noted a positive start to Q3 with several orders announced, including in the USA, as the policy landscape has begun to provide more certainty to customers.

Segment Analysis

Power Solutions

The Power Solutions segment, which encompasses Vestas’ turbine sales and installation business, saw revenue increase by 7% year-over-year. However, the segment reported an EBIT margin before special items of -0.4%, representing a decline of 1.1 percentage points compared to the same period last year.

The following chart illustrates the Power Solutions performance trends:

A significant development for the segment was the commencement of serial manufacturing at the company’s nacelle facility in Poland, with the first V236 nacelle leaving the factory in June. This manufacturing ramp-up, while driving costs and investments in the short term, represents an important step in Vestas’ product strategy.

Service

The Service segment continues to be a bright spot for Vestas, with the order backlog increasing to €36 billion from €35 billion a year ago. The company now has 159 GW under service contracts, up from 151 GW in the comparable period.

The following slide shows the geographic distribution of Vestas’ service business:

Service generated an EBIT of €163 million in Q2 2025, corresponding to a robust EBIT margin of 17.2%. The company is two quarters into its Service recovery plan, which is expected to run until the end of 2026, with a long-term ambition of achieving a 25% EBIT margin for this segment.

Financial Position and Cash Flow

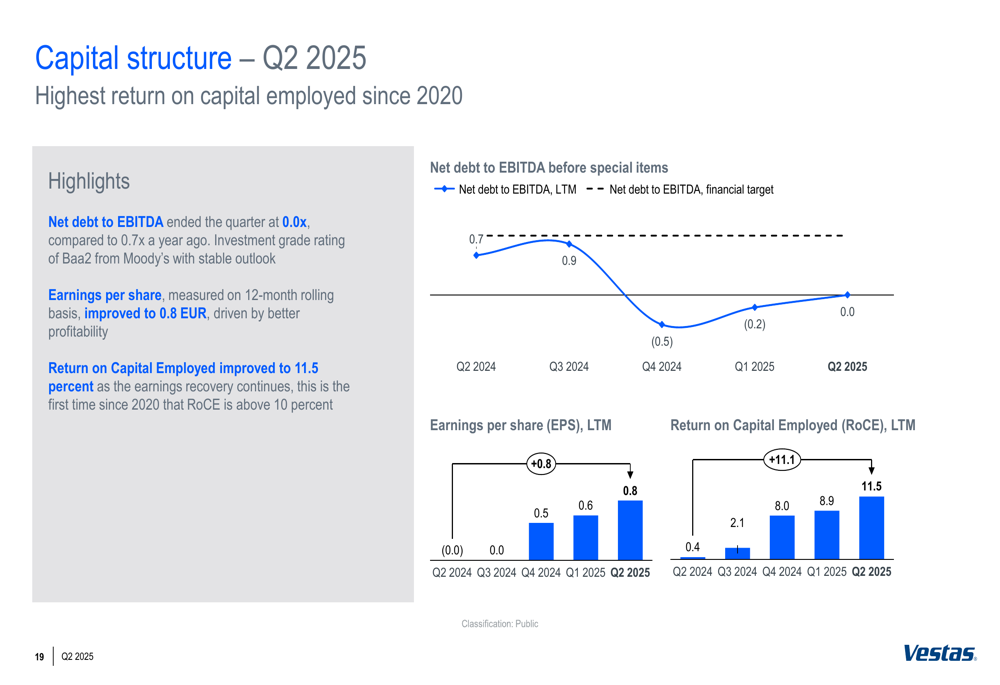

Vestas maintained a strong financial position in Q2 2025, with net debt to EBITDA ending the quarter at 0.0x. Earnings per share improved to €0.8, reflecting the company’s enhanced profitability.

The following chart illustrates key capital structure metrics:

Operating cash flow was positive at €120 million for the quarter, while adjusted free cash flow amounted to negative €227 million. Total (EPA:TTEF) investments for the period reached €288 million, primarily related to tangible investments supporting the company’s manufacturing capabilities.

Warranty costs amounted to €115 million in the quarter, corresponding to 3.1% of revenue, while warranty provisions consumed were €188 million.

Sustainability Performance

Vestas continues to emphasize its sustainability credentials, reporting that turbines produced and shipped in the last twelve months are expected to avoid 480 million tonnes of greenhouse gas emissions over their lifetime. However, carbon emissions from the company’s own operations increased by 8,000 tonnes year-over-year due to increased activity.

The company’s safety performance showed a slight deterioration, with the number of recordable injuries per million working hours (TRIR) increasing from 2.8 to 3.0 year-over-year.

Outlook and Guidance

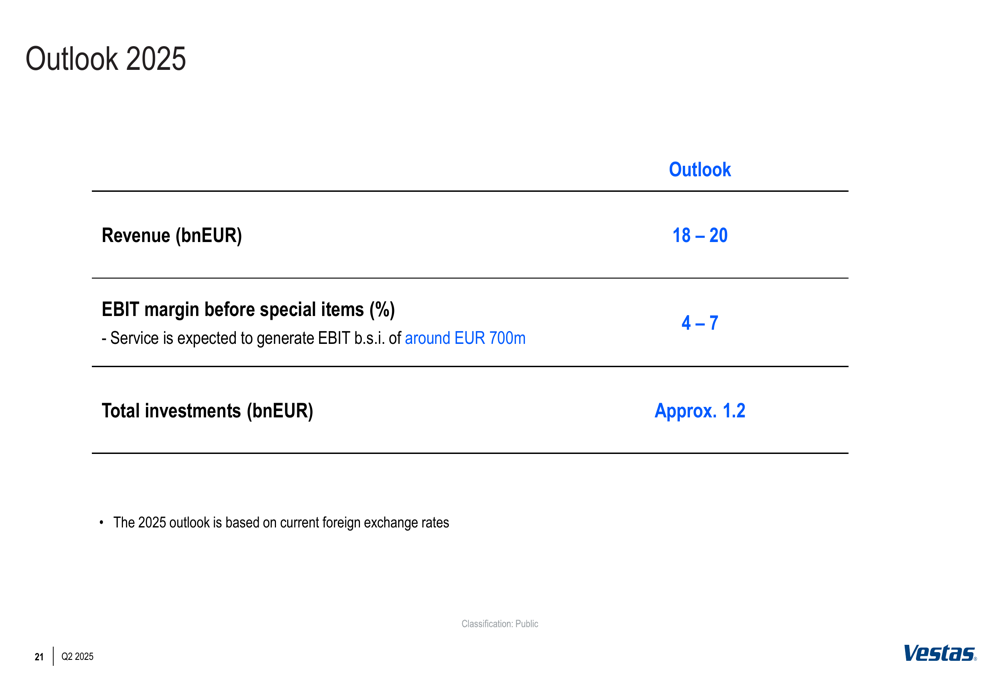

Vestas maintained its full-year 2025 guidance, projecting revenue between €18-20 billion and an EBIT margin before special items of 4-7%. The company expects total investments of approximately €1.2 billion for the year.

The following slide outlines the company’s outlook for 2025:

This outlook suggests that Vestas anticipates stronger performance in the second half of 2025, as the current EBIT margin of 1.5% would need to improve significantly to reach the full-year target range of 4-7%.

Building on the momentum from Q1 2025, when the company reported a 29% revenue increase, Vestas appears to be maintaining its growth trajectory despite the challenging order environment. The continued strength of the Service segment provides a stable foundation, while the company works to improve margins in its Power Solutions business amid ongoing manufacturing ramp-up activities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.