FTSE 100 today: The index and GBP slide; Ocado plunges

Viavi Solutions Inc. (NASDAQ:VIAV) reported strong fourth-quarter results for fiscal year 2025, with double-digit revenue growth across both business segments and significant margin expansion. The company presented its quarterly earnings on August 7, 2025, highlighting its continued momentum in data center and aerospace markets while advancing strategic acquisitions.

Quarterly Performance Highlights

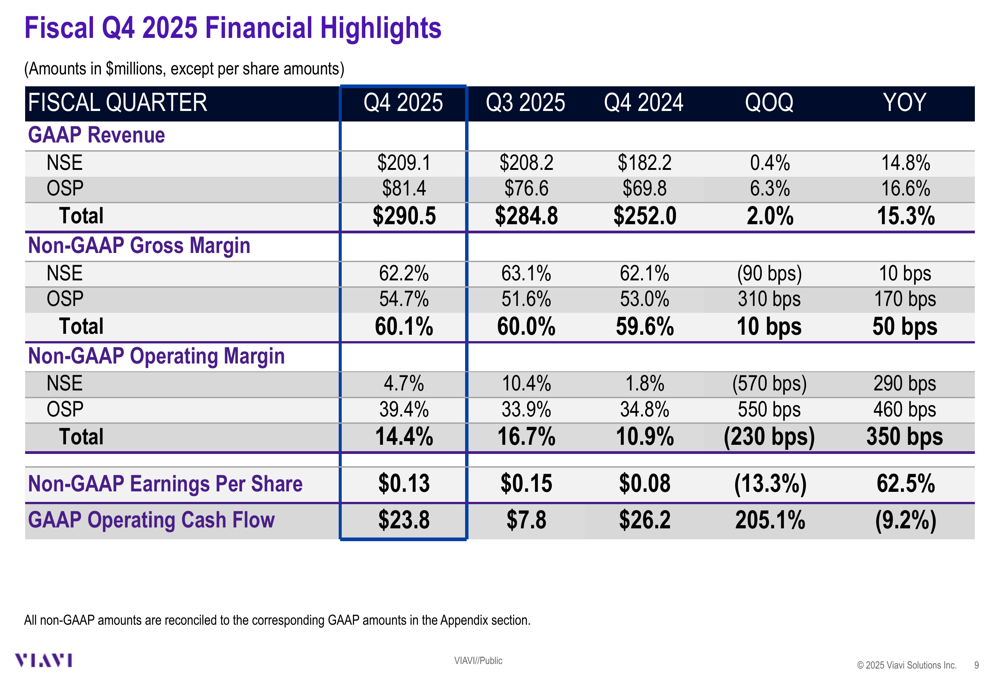

Viavi delivered robust financial performance in the fourth quarter, with results at or above the high end of guidance. Revenue reached $290.5 million, representing a 15.3% year-over-year increase and 2.0% sequential growth from the previous quarter.

"Revenue was at the high end of the guidance range," the company noted in its presentation, attributing the growth to strong demand for fiber lab and production products from the data center ecosystem, as well as growth in aerospace and defense products.

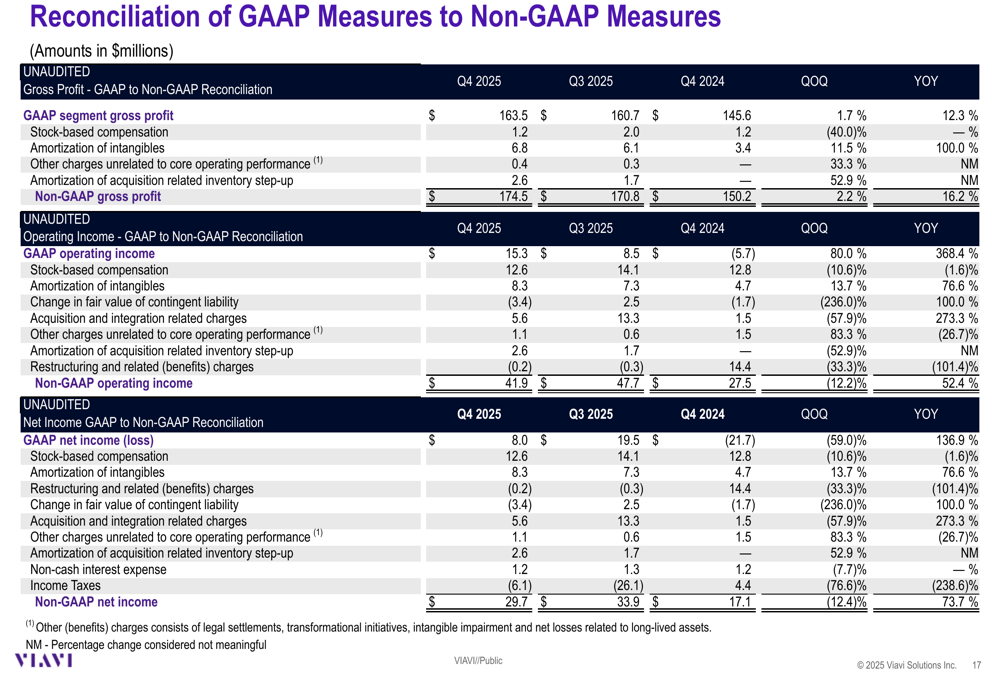

The company’s profitability metrics showed substantial improvement, with non-GAAP operating income of $41.9 million, up 52.4% year-over-year, and non-GAAP operating margin of 14.4%, representing a 350 basis point improvement from the prior year. Non-GAAP earnings per share reached $0.13, a 62.5% increase compared to Q4 2024.

As shown in the following comprehensive financial overview:

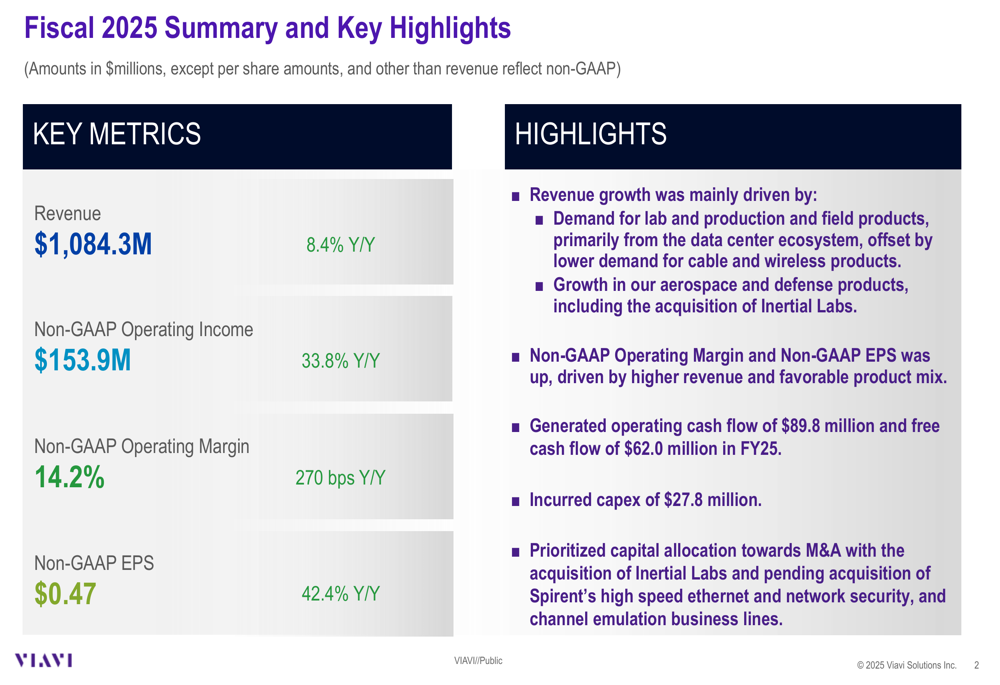

The company generated $23.8 million in operating cash flow and $18.3 million in free cash flow during the quarter, while incurring $5.5 million in capital expenditures. This performance caps a strong fiscal year 2025, in which Viavi achieved total revenue of $1,084.3 million, up 8.4% year-over-year, with non-GAAP EPS of $0.47, representing a 42.4% increase from fiscal 2024.

The full fiscal year summary highlights the company’s consistent growth trajectory:

Segment Performance Analysis

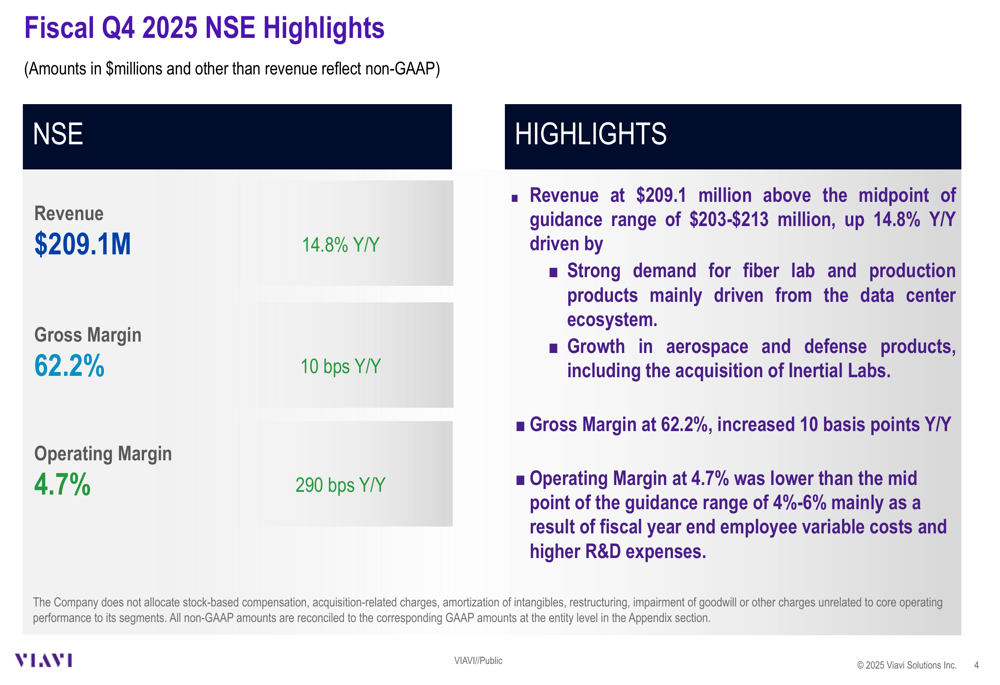

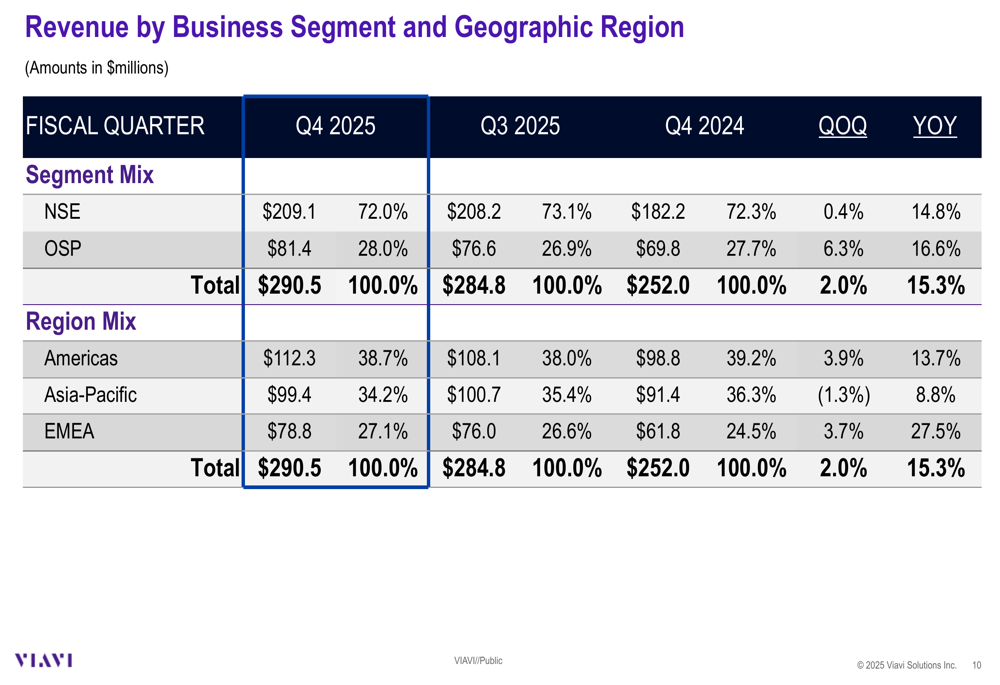

Both of Viavi’s business segments contributed to the quarter’s strong performance. The Network and Service Enablement (NSE) segment, which represents 72% of total revenue, generated $209.1 million in the fourth quarter, a 14.8% increase year-over-year. This segment’s performance was driven by strong demand for fiber lab and production products from data center customers.

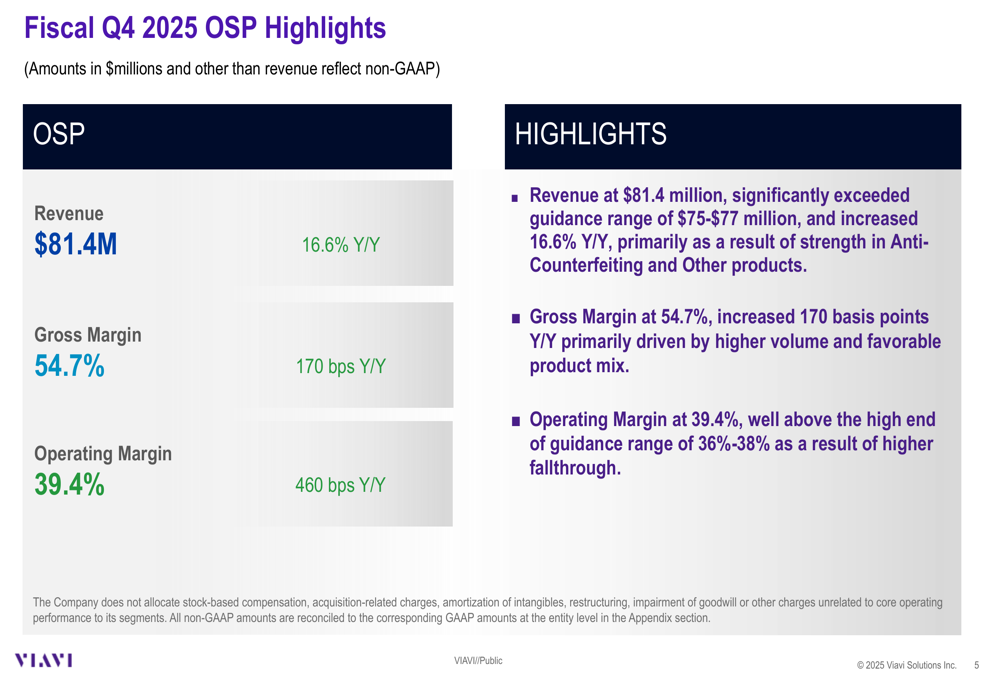

The Optical Security and Performance Products (OSP) segment delivered even stronger growth, with revenue of $81.4 million, up 16.6% year-over-year. This segment significantly exceeded the guidance range of $75-$77 million due to strength in anti-counterfeiting and other products.

The detailed segment performance is illustrated below:

Profitability also improved across both segments. The NSE segment achieved an operating margin of 4.7%, up 290 basis points year-over-year, while the OSP segment reached an impressive 39.4% operating margin, up 460 basis points from the prior year.

The following slides provide more detailed insights into each segment’s performance:

From a geographic perspective, Viavi saw growth across all regions, with particularly strong performance in EMEA, which grew 27.5% year-over-year to $78.8 million. The Americas region, which accounts for the largest share of revenue at 38.7%, grew 13.7% to $112.3 million, while the Asia-Pacific region increased 8.8% to $99.4 million.

The geographic breakdown of revenue is shown here:

Strategic Initiatives and Acquisitions

Viavi continues to execute its growth strategy through both organic expansion and strategic acquisitions. The company completed the acquisition of Inertial Labs during fiscal 2025, strengthening its position in the aerospace and defense market.

Additionally, Viavi has made significant progress on its pending acquisition of Spirent (LON:SPT)’s high-speed ethernet and network security, and channel emulation business lines. The company successfully priced and allocated a $600 million Term Loan B to fund this acquisition, which will close concurrently with the transaction.

"The Term Loan B will close concurrently with the transaction," the company stated in its presentation, indicating that preparations for integrating these new business lines are well underway.

The company maintains a solid financial position to support these strategic initiatives, with a total cash balance of $429.0 million as of the end of fiscal Q4 2025. Short-term debt stands at $246.2 million, while long-term debt is $396.3 million.

Forward-Looking Guidance

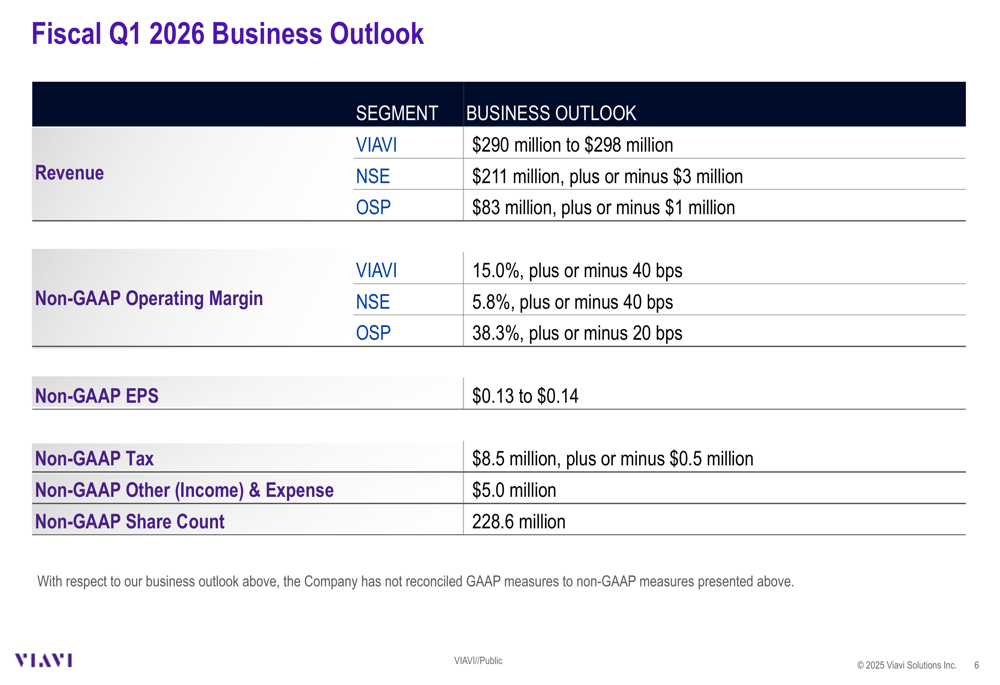

Looking ahead to the first quarter of fiscal 2026, Viavi expects continued growth momentum. The company projects revenue between $290 million and $298 million, with non-GAAP operating margin of 15.0% (plus or minus 40 basis points) and non-GAAP EPS between $0.13 and $0.14.

The NSE segment is expected to generate approximately $211 million in revenue (plus or minus $3 million) with an operating margin of 5.8% (plus or minus 40 basis points). The OSP segment is projected to deliver around $83 million in revenue (plus or minus $1 million) with an operating margin of 38.3% (plus or minus 20 basis points).

The detailed Q1 2026 outlook is presented here:

This guidance suggests that Viavi expects to maintain its growth trajectory in the coming quarter, building on the momentum established throughout fiscal 2025. The company’s focus on high-growth markets such as data centers and aerospace, combined with strategic acquisitions, positions it well for continued expansion.

While the previous quarter’s earnings call had mentioned concerns about potential tariff-related shipment delays, these do not appear to have materially impacted the company’s Q4 performance or its outlook for Q1 2026, indicating effective management of these challenges.

As Viavi continues to execute its growth strategy, investors will be watching closely to see if the company can maintain its strong performance in both revenue growth and margin expansion while successfully integrating its recent and pending acquisitions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.