TSX futures subdued as gold rally takes a breather

Introduction & Market Context

Viscofan (BME:VIS) shares rose 1.05% to €67.10 following the release of its first quarter 2025 results on April 28, which showed strong operational performance across all business segments and regions, despite currency headwinds impacting the bottom line. The food casings manufacturer reported solid volume growth in all product families, with particularly strong performance in its New Business division and South American markets.

Quarterly Performance Highlights

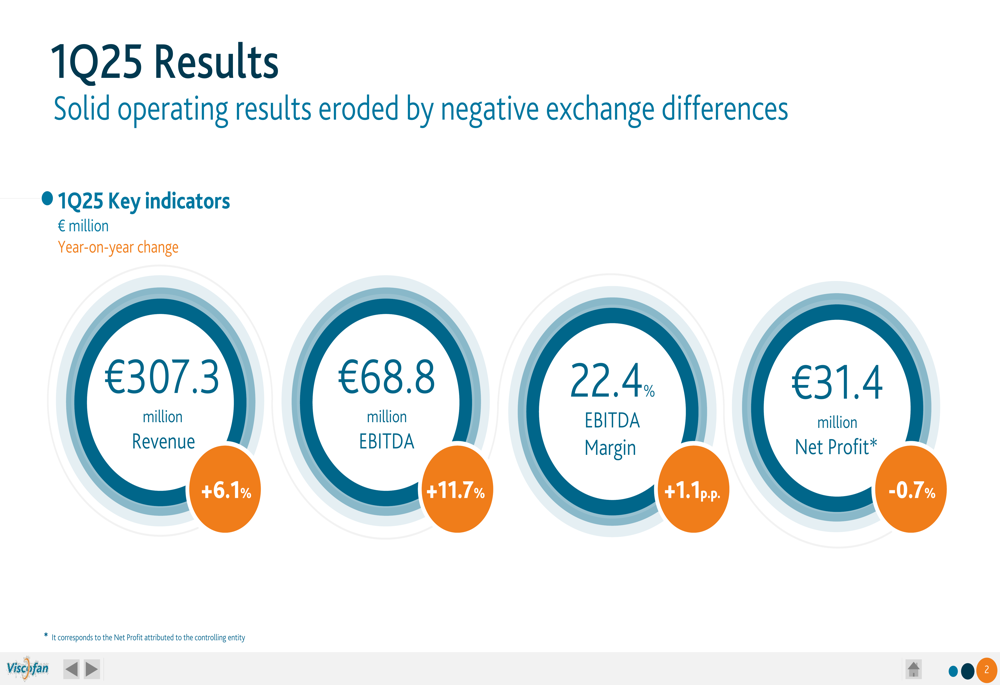

Viscofan reported revenue of €307.3 million for Q1 2025, representing a 6.1% year-on-year increase from the €289.7 million recorded in Q1 2024. The company’s EBITDA grew at an even faster pace, rising 11.7% to €68.8 million, while EBITDA margin expanded by 1.1 percentage points to 22.4%.

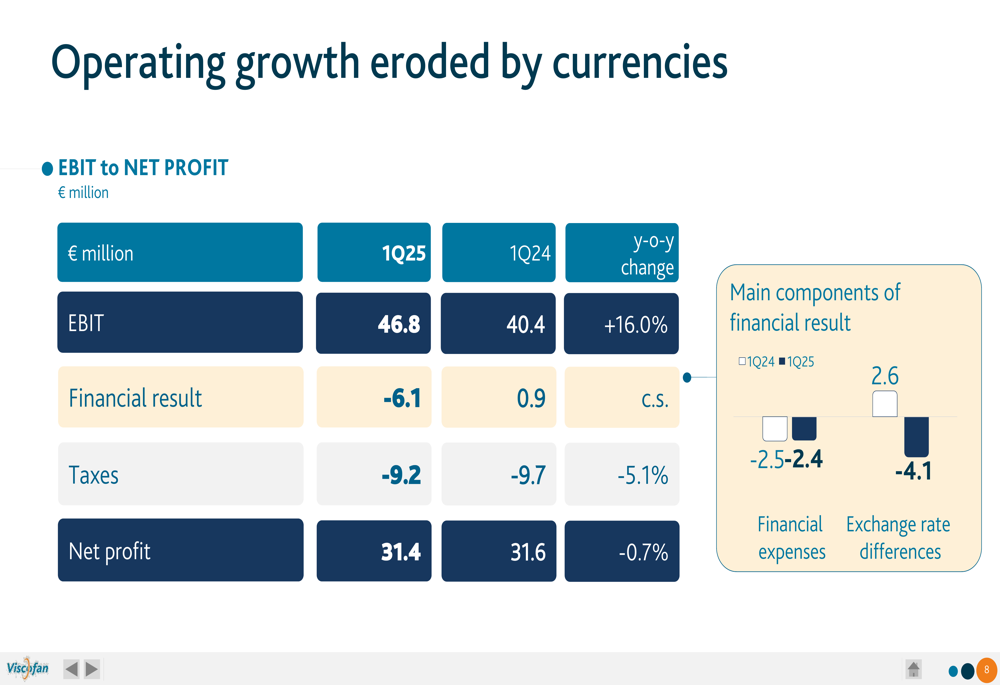

As shown in the following key indicators chart, despite the strong operational performance, net profit decreased slightly by 0.7% to €31.4 million:

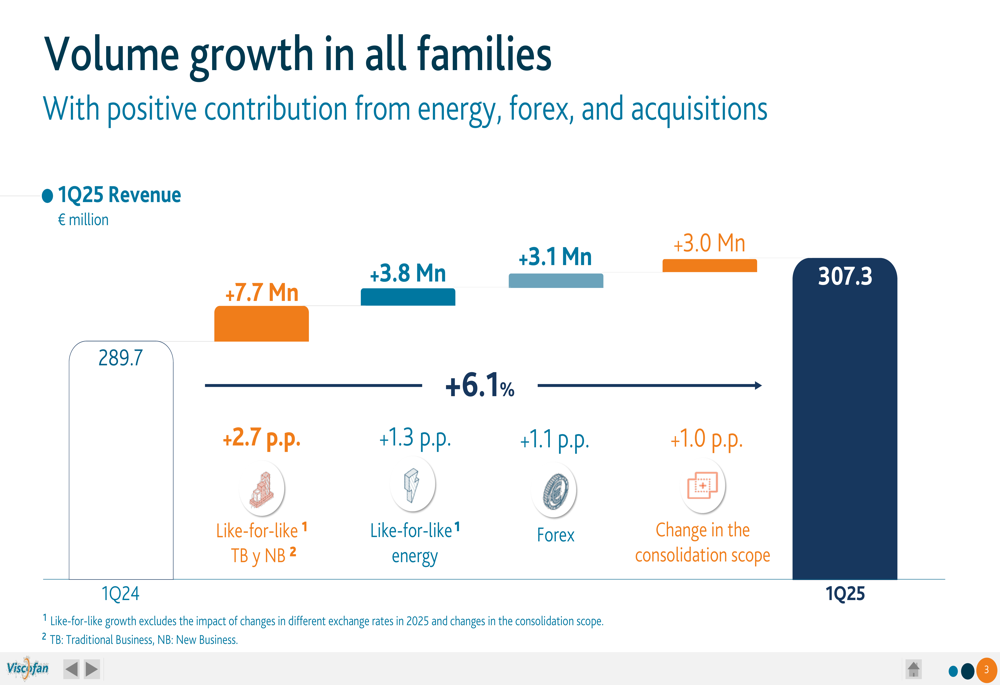

The revenue growth was driven by multiple factors, with like-for-like growth contributing 2.7 percentage points, energy sales adding 1.3 percentage points, favorable foreign exchange movements contributing 1.1 percentage points, and changes in consolidation scope adding another 1.0 percentage point.

The following chart breaks down these revenue growth components:

Detailed Financial Analysis

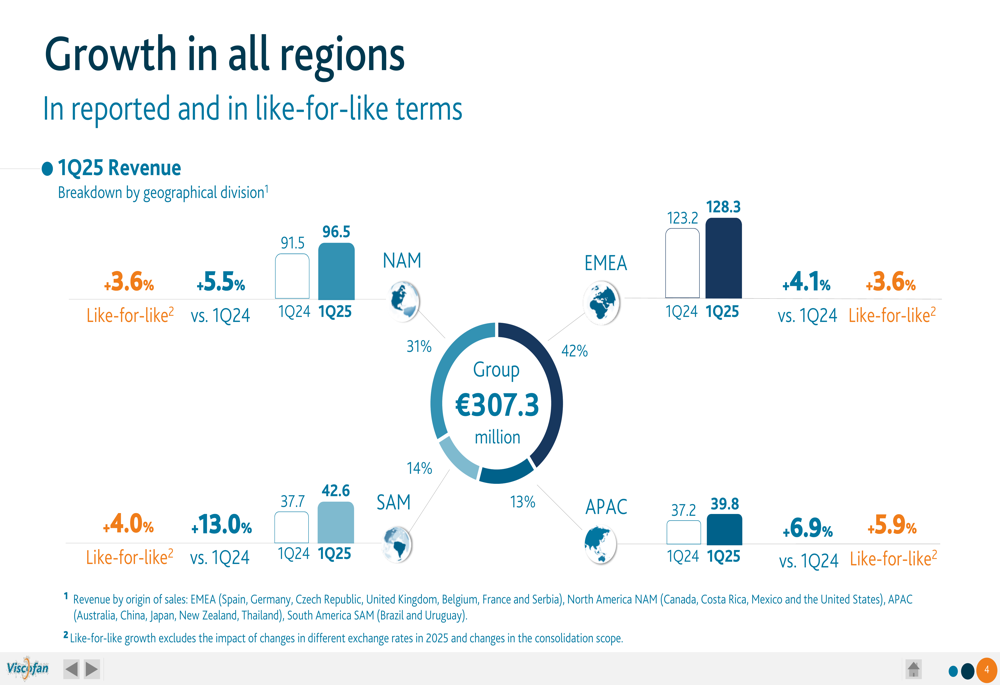

Viscofan’s growth was geographically balanced, with all regions showing positive performance. South America led with 13.0% year-on-year growth, followed by Asia-Pacific at 6.9%, North America at 5.5%, and Europe, Middle East, and Africa at 4.1%.

This regional growth distribution is illustrated in the following map:

When analyzed by business division, Viscofan’s Traditional Business, which represents 82% of total revenue, grew by 4.1% to €250.9 million. The New Business division, accounting for 13% of revenue, showed the strongest relative growth at 10.9%, reaching €39.1 million. Energy sales, making up the remaining 5%, surged by 27.8% to €17.2 million.

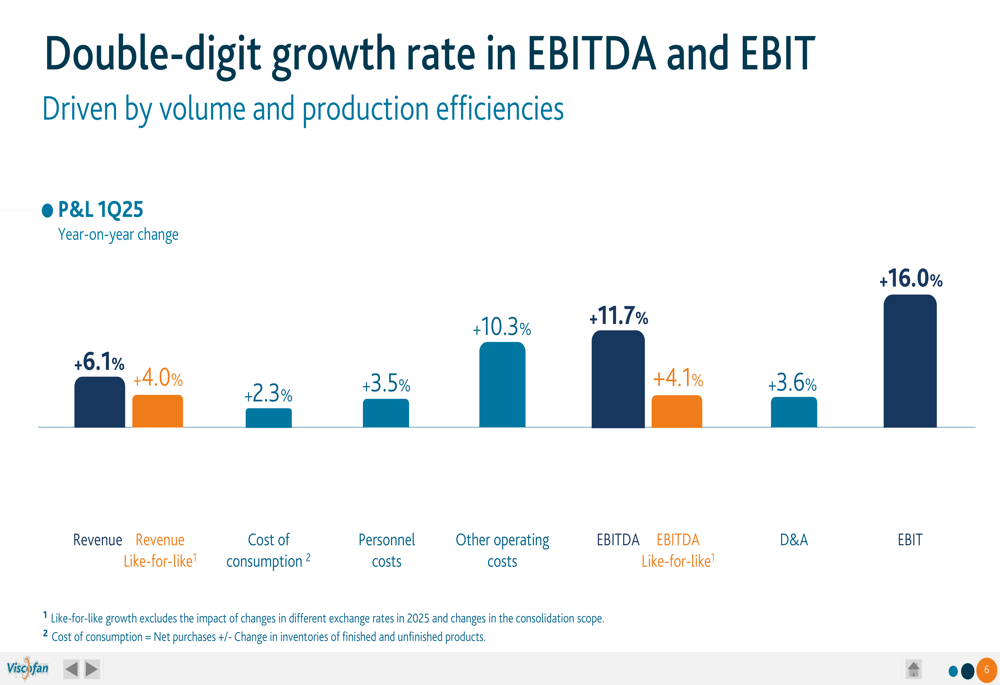

The company’s cost structure showed disciplined management, with cost of consumption increasing by only 2.3% and personnel costs by 3.5%, both below the revenue growth rate. This cost control, combined with operational efficiencies, contributed to the double-digit growth in EBITDA and EBIT, which increased by 11.7% and 16.0% respectively.

The following chart illustrates these growth rates:

Despite the strong operational performance, Viscofan’s net profit decreased slightly by 0.7% to €31.4 million. This decline was primarily due to negative currency effects, with exchange rate differences swinging from a positive €2.6 million in Q1 2024 to a negative €4.1 million in Q1 2025, as shown in this breakdown:

Strategic Initiatives & Investment Plans

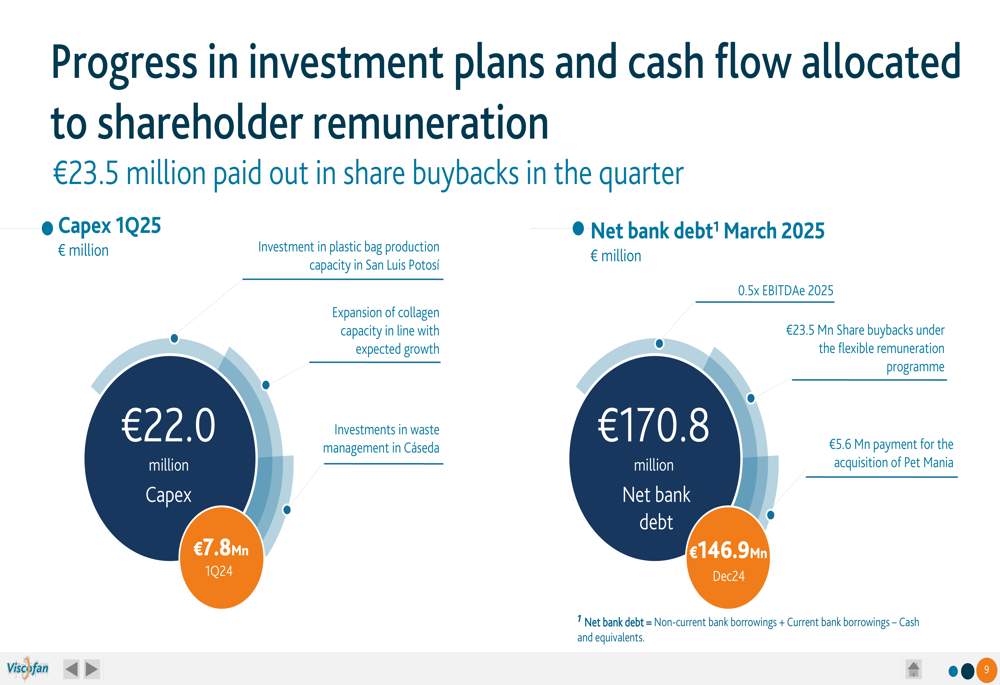

Viscofan significantly ramped up its capital expenditure in Q1 2025, investing €22.0 million compared to €7.8 million in the same period last year. These investments focused on three key areas: expanding plastic bag production capacity in San Luis Potosí, increasing collagen capacity to meet expected growth, and improving waste management in Cáseda.

The company’s net bank debt increased to €170.8 million by the end of March 2025, up from €146.9 million in December 2024. This increase reflects not only the higher capital expenditure but also €23.5 million in share buybacks under the company’s flexible remuneration program and €5.6 million for the acquisition of Pet Mania.

The following slide details these investment initiatives and financial position:

Forward-Looking Statements

Viscofan’s management indicated that the Q1 2025 results are in line with the company’s full-year guidance in operational terms. The company highlighted four key takeaways from the quarter:

1. Revenue growth across all reporting regions, driven by higher volumes in all main casing families

2. Improved operating profitability due to production efficiencies, cost control, and favorable foreign exchange impact on operations

3. Negative impact of exchange differences caused by a weak US dollar

4. Results aligned with 2025 guidance in operational terms

The company continues to execute its strategic plan, focusing on capacity expansion and operational efficiency while maintaining a commitment to shareholder remuneration through its flexible dividend program and share buybacks.

With strong volume growth across all product families and regions, Viscofan appears well-positioned to continue its operational momentum through 2025, though currency fluctuations remain a potential challenge to bottom-line results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.