Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

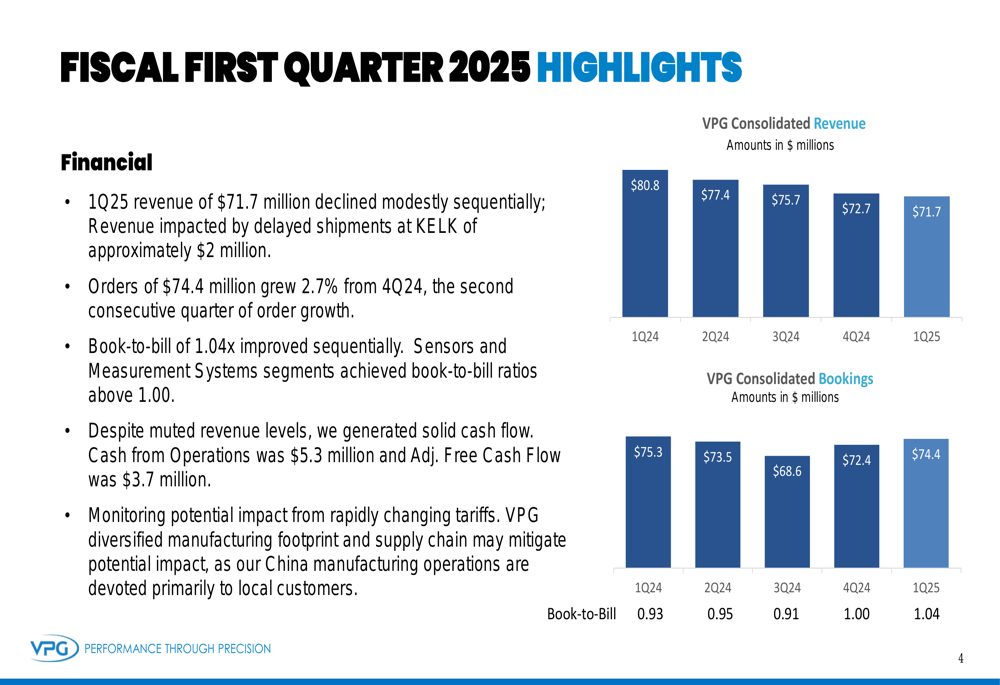

Vishay Precision Group Inc (NYSE:VPG) presented its first quarter 2025 earnings results on May 6, 2025, revealing a complex picture of sequential revenue decline offset by improving order trends. The precision measurement technology company reported quarterly revenue of $71.7 million, missing analyst expectations of $75.18 million and continuing a five-quarter downward trend from the $80.8 million reported in Q1 2024.

The earnings miss triggered a negative market reaction, with VPG shares declining 3.54% in pre-market trading following the announcement. The company is currently trading at a P/E ratio of 29.8x, according to available market data, with analysts recently revising earnings expectations downward.

Quarterly Performance Highlights

VPG’s Q1 2025 performance showed modest sequential revenue decline, but the company highlighted several positive indicators, including improved order intake and book-to-bill ratio.

As shown in the following chart of consolidated revenue and bookings trends:

Orders reached $74.4 million, growing 2.7% from Q4 2024, while the book-to-bill ratio improved to 1.04x from 1.00x in the previous quarter. This suggests potential revenue stabilization in upcoming quarters, despite the current downward trend.

The company reported a net loss of $0.9 million, or -$0.07 per diluted share, compared to net earnings of $0.8 million, or $0.06 per share, in Q4 2024. On an adjusted basis, earnings were $0.04 per share, falling significantly short of analyst expectations of $0.18 per share.

Despite these challenges, VPG improved its adjusted operating margin to 1.1% from 0.8% in the previous quarter, demonstrating some progress in operational efficiency.

Segment Analysis

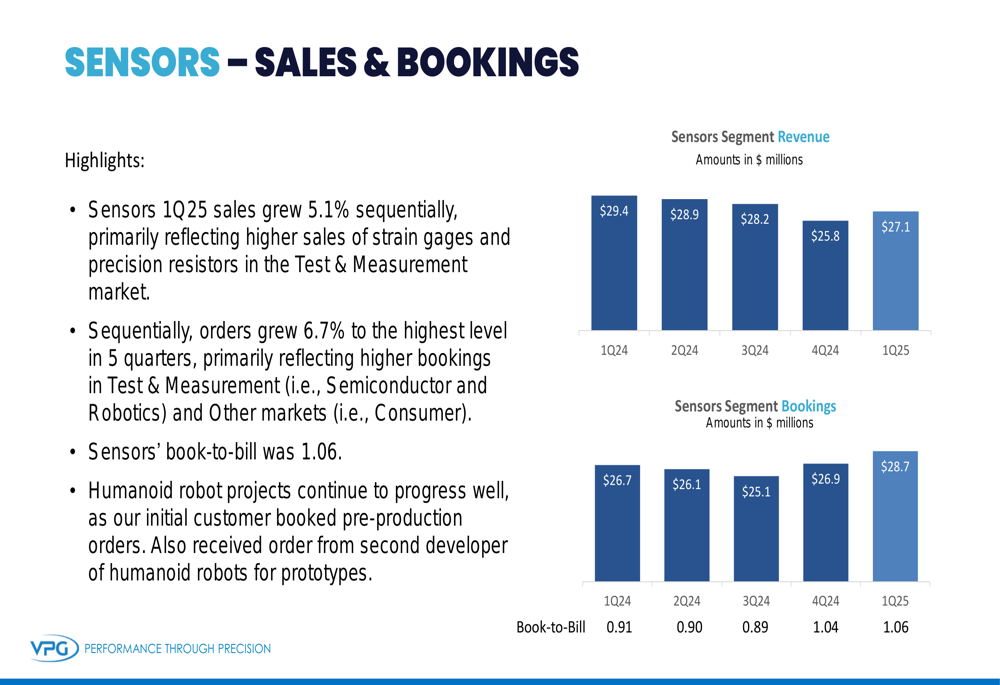

VPG’s three business segments showed divergent performance, with Sensors emerging as the bright spot while Measurement Systems faced significant headwinds.

The Sensors segment demonstrated strong growth, with sales increasing 5.1% sequentially and orders growing 6.7% to reach the highest level in five quarters:

The company noted that humanoid robot projects continue to progress well in this segment, representing a key growth opportunity.

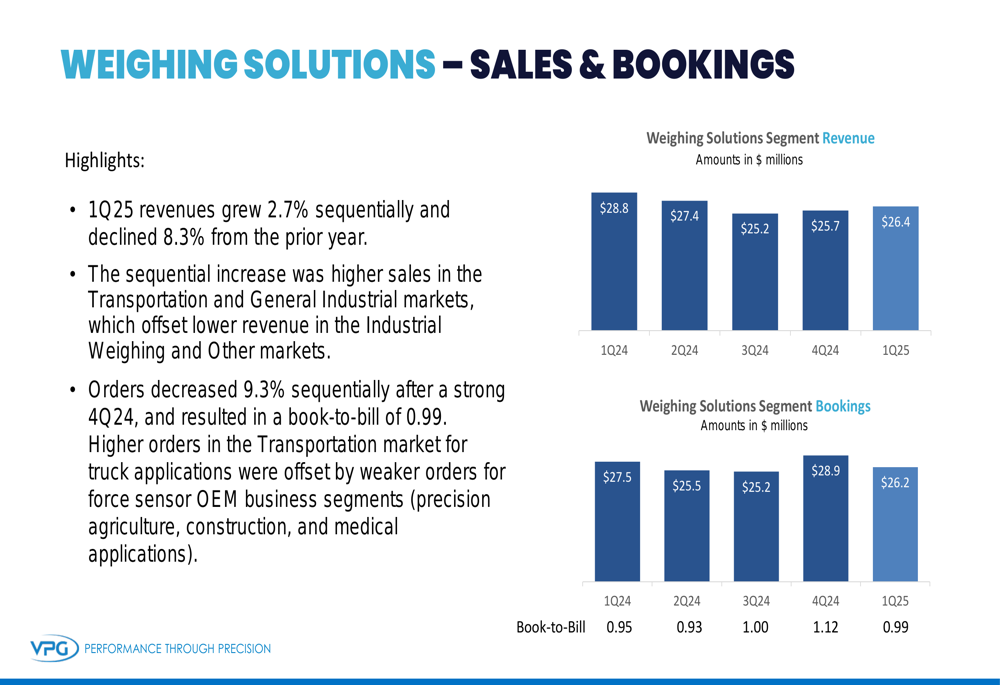

In contrast, the Weighing Solutions segment showed mixed results with modest sequential growth but year-over-year decline:

Weighing Solutions revenue increased 2.7% sequentially to $26.4 million but declined 8.3% compared to the prior year. The sequential improvement was driven by higher sales in Transportation and General Industrial markets, while orders decreased 9.3% sequentially after a strong Q4 2024.

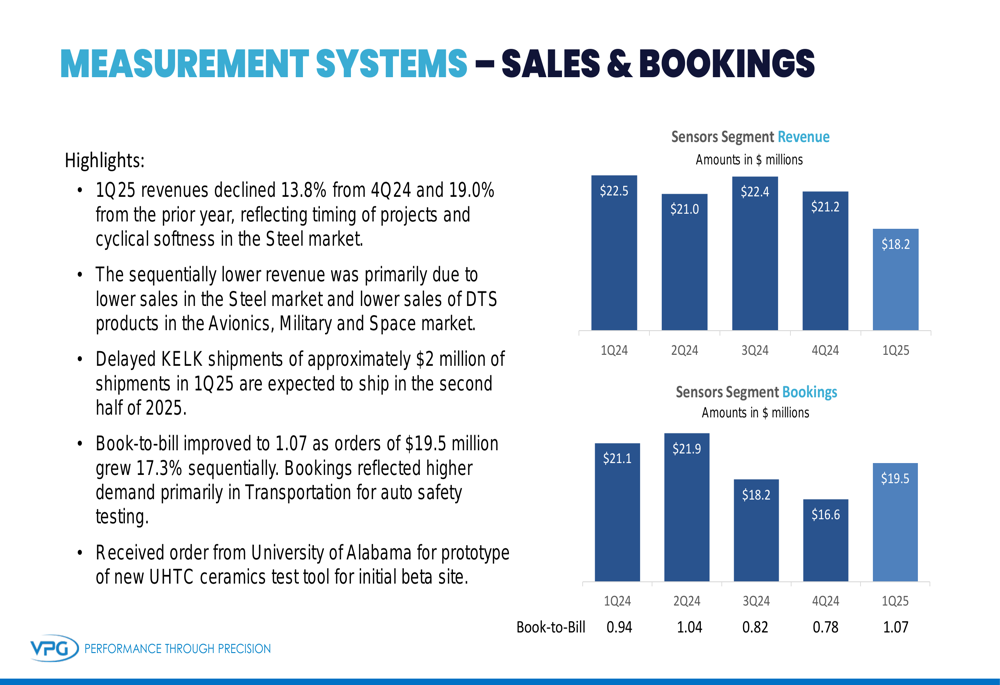

The Measurement Systems segment faced the most significant challenges:

Revenue declined 13.8% sequentially to $18.2 million, primarily due to lower sales in the Steel market and reduced sales of DTS products in the Avionics, Military and Space market. However, orders improved 17.3% sequentially, resulting in a book-to-bill ratio of 1.07.

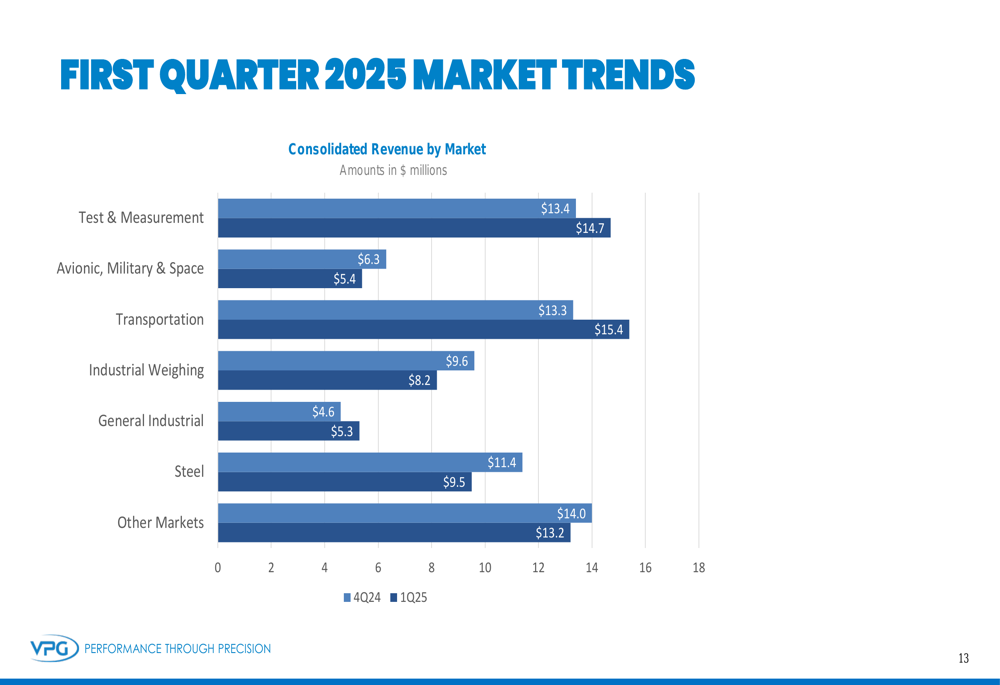

Market Trends Analysis

VPG’s performance varied significantly across different market segments, as illustrated in the following revenue breakdown:

The Transportation market showed the strongest performance, increasing from $13.3 million in Q4 2024 to $15.4 million in Q1 2025. Test & Measurement also improved from $13.4 million to $14.7 million. However, these gains were offset by declines in the Steel market (from $11.4 million to $9.5 million) and Avionics, Military & Space (from $6.3 million to $5.4 million).

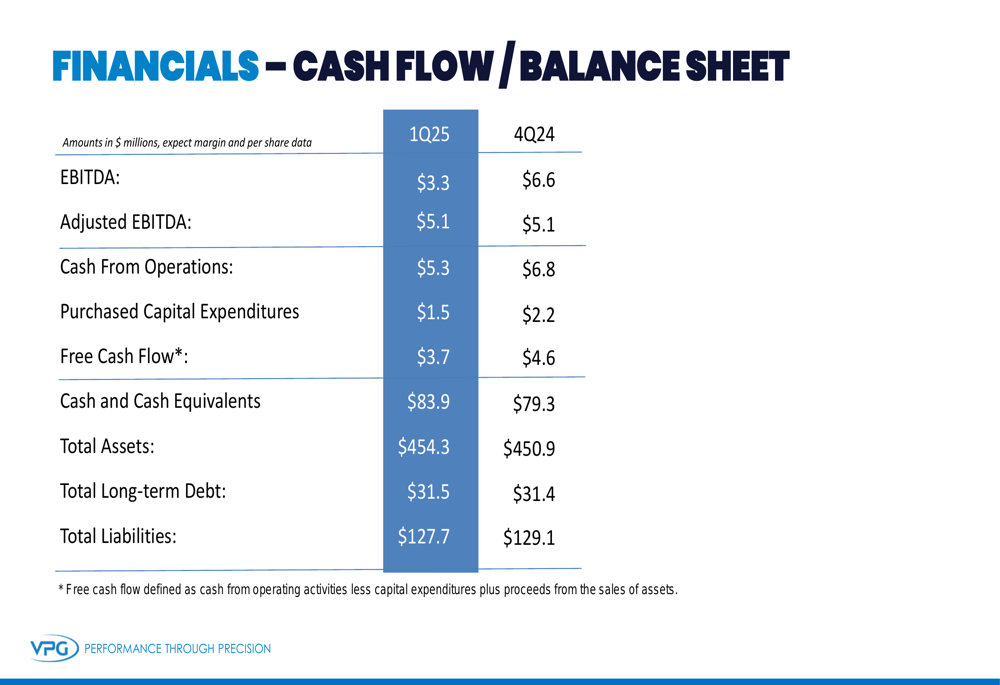

Financial Position & Outlook

Despite the earnings challenges, VPG maintained a strong financial position with improving cash flow metrics:

Cash from operations was $5.3 million, while adjusted free cash flow reached $3.7 million. The company’s cash and cash equivalents increased to $83.9 million from $79.3 million in the previous quarter, significantly exceeding its total long-term debt of $31.5 million.

VPG provided a revenue forecast for Q2 2025 between $70 million and $76 million, indicating potential stabilization. The company expects gradual revenue recovery and is targeting $5 million in annual operational cost reductions by year-end, with capital expenditures for 2025 projected between $10 million and $12 million.

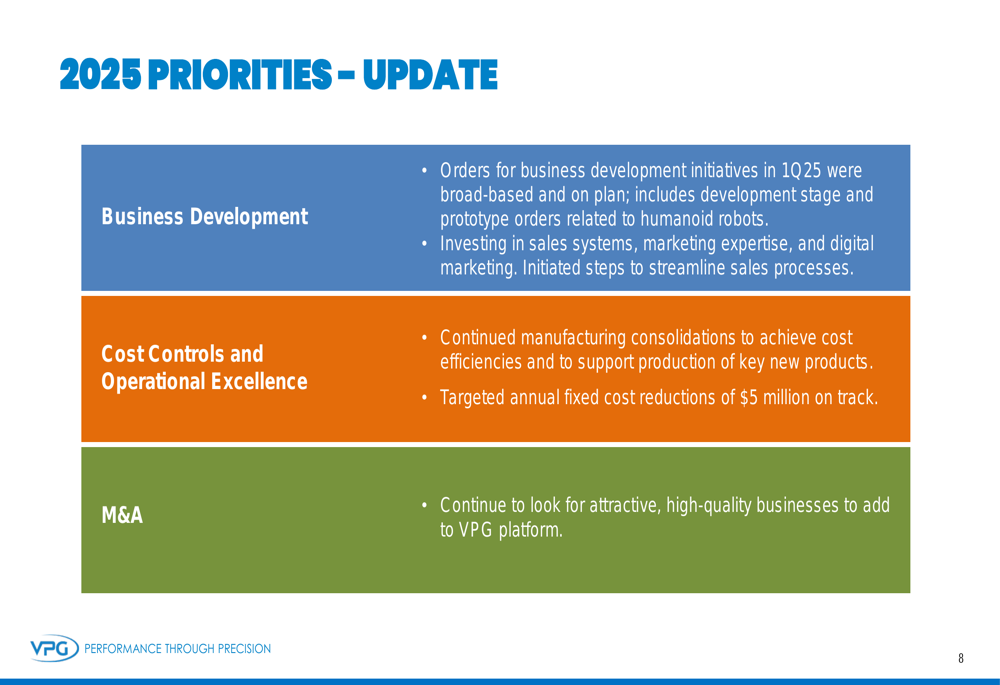

Strategic Initiatives

VPG outlined three key strategic priorities for 2025, focusing on business development, operational excellence, and potential acquisitions:

The company reported broad-based orders for business development initiatives in Q1, including development stage and prototype orders related to humanoid robots. VPG is also investing in sales systems, marketing expertise, and digital marketing to drive future growth.

On the operational front, manufacturing consolidations are continuing to achieve cost efficiencies, with the company on track to achieve its targeted annual fixed cost reductions of $5 million.

The company also emphasized its commitment to sustainability, highlighting several 2024 milestones including increased board diversity, updated code of conduct, and the publication of energy management and water use reduction targets.

During the earnings call Q&A session, management confirmed that approximately $2 million in KELK product shipments have been delayed to Q3-Q4, which impacted the current quarter’s results. They also reiterated their focus on strategic acquisitions to enhance growth opportunities.

While VPG faces near-term challenges with revenue declines and earnings pressure, the improving order trends and book-to-bill ratio suggest potential stabilization in coming quarters as the company continues to execute on its cost reduction and growth initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.