IonQ CRO Alameddine Rima sells $4.6m in shares

Introduction & Market Context

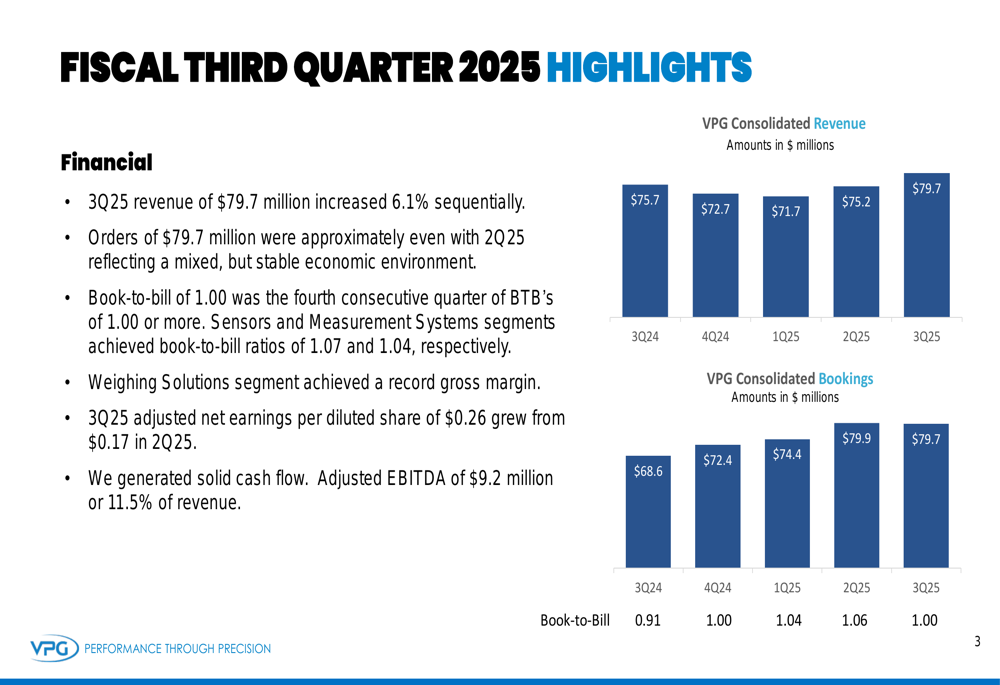

Vishay Precision Group (NYSE:VPG) presented its third quarter 2025 earnings results on November 4, 2025, highlighting revenue growth and improved profitability despite a mixed economic environment. The company reported revenue of $79.7 million, up 6.1% sequentially and 5.3% year-over-year, with adjusted earnings per share of $0.26, exceeding analyst expectations of $0.20.

Despite the positive results, VPG's stock declined 3.64% to $36.62 in regular trading following the announcement, after dropping 0.29% in pre-market activity. The stock remains well above its 52-week low of $18.57 but has pulled back from its recent high of $38.90.

The company's presentation painted a picture of stable but uneven market conditions, with strong performance in the Sensors segment offsetting challenges in other areas.

Quarterly Performance Highlights

VPG's consolidated revenue showed consistent improvement over the past year, culminating in the $79.7 million reported for Q3 2025. Orders remained steady at $79.7 million, approximately even with the previous quarter, resulting in a book-to-bill ratio of 1.00 – the fourth consecutive quarter at or above this important threshold.

As shown in the following consolidated revenue and bookings charts:

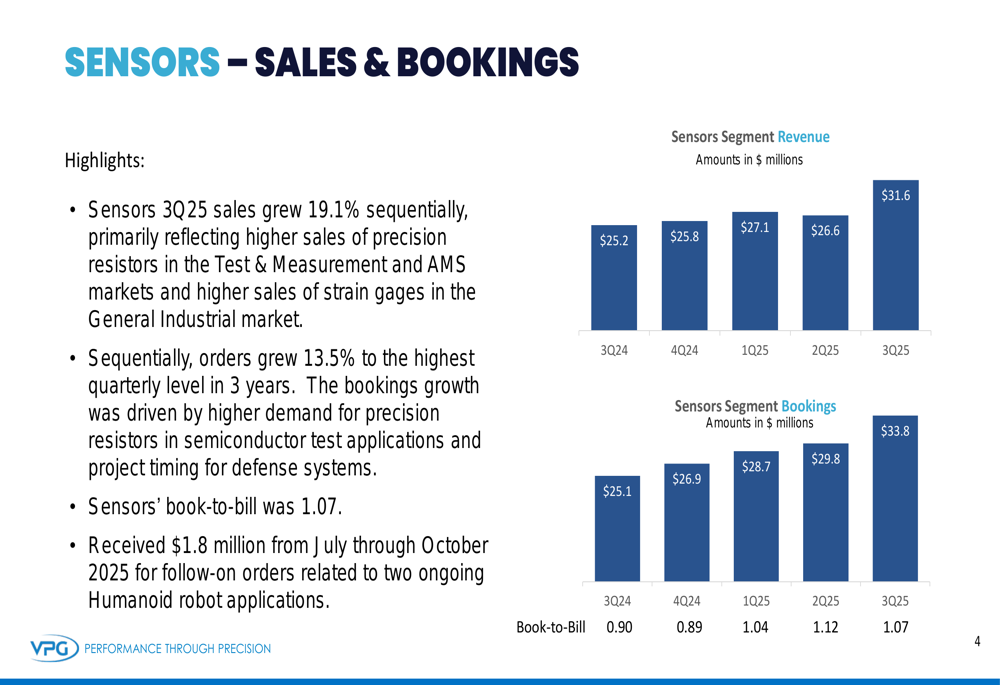

The Sensors segment emerged as the standout performer, with sales growing 19.1% sequentially to $31.6 million. This growth was primarily driven by higher sales of precision resistors in Test & Measurement and Advanced Manufacturing Systems (AMS) markets, along with increased strain gage sales in the General Industrial market. The segment achieved a book-to-bill ratio of 1.07, indicating continued growth potential.

The Sensors segment performance is illustrated in these charts:

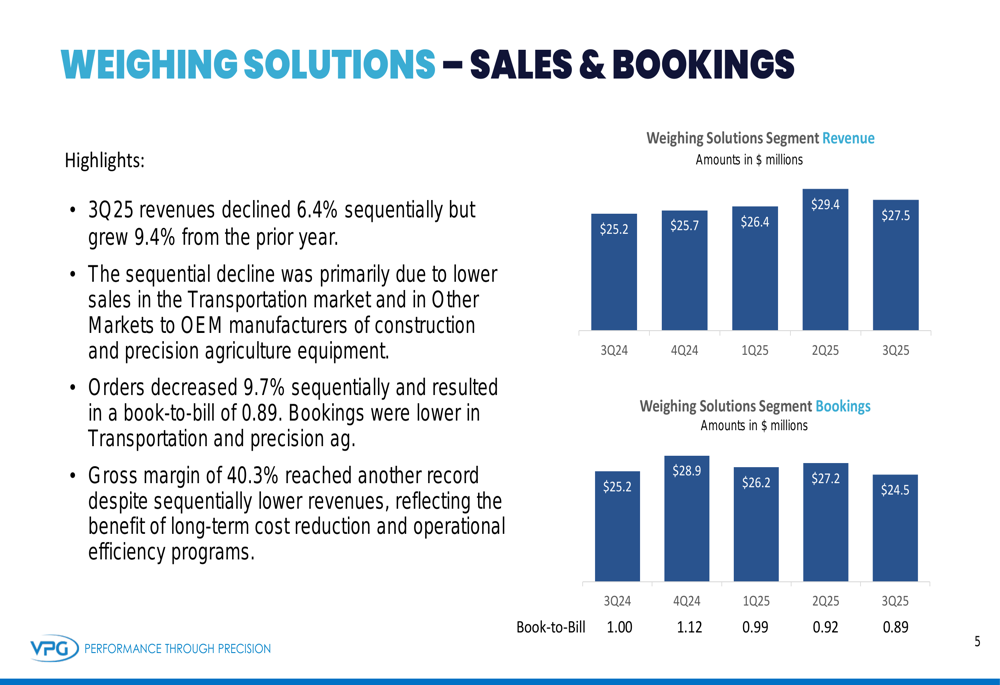

In contrast, the Weighing Solutions segment saw revenue decline 6.4% sequentially to $27.5 million, though it remained 9.4% higher than the prior year. Despite the revenue decrease, the segment achieved a record gross margin of 40.3%, reflecting successful cost reduction and operational efficiency initiatives. The sequential decline was primarily attributed to lower sales in the Transportation market and to OEM manufacturers of construction and precision agriculture equipment.

The following charts show the Weighing Solutions segment's performance:

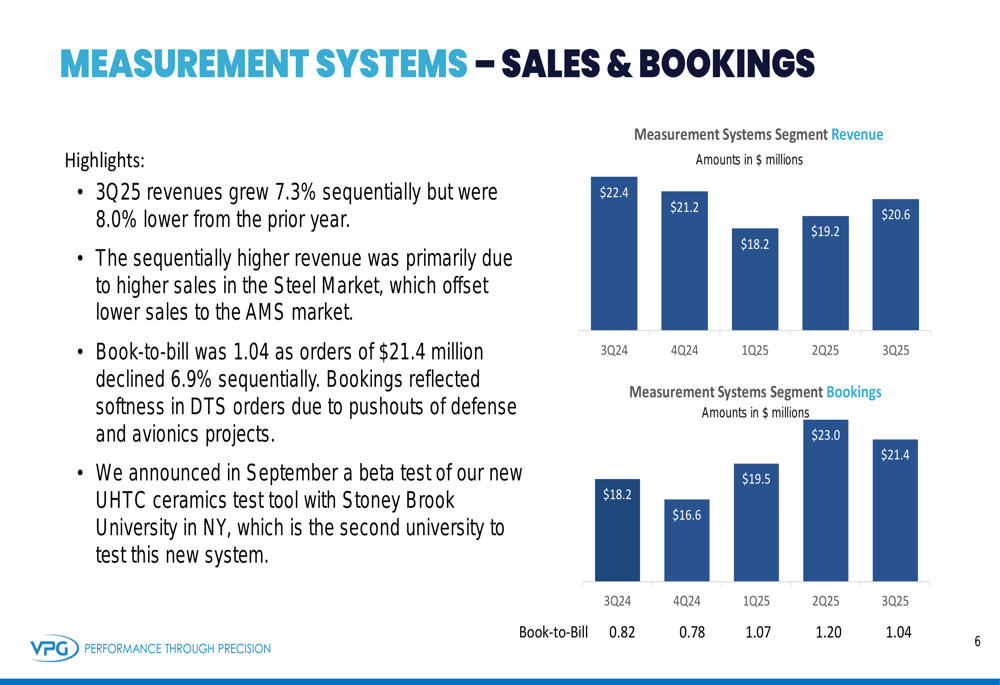

The Measurement Systems segment showed signs of recovery with 7.3% sequential revenue growth to $20.6 million, though still 8.0% below the prior year. The improvement was driven by higher sales in the Steel Market, which offset lower sales to the AMS market. The segment maintained a positive book-to-bill ratio of 1.04, despite some softness in Dynamic Test Systems (DTS) orders due to pushouts of defense and avionics projects.

Measurement Systems segment performance is detailed in these charts:

Detailed Financial Analysis

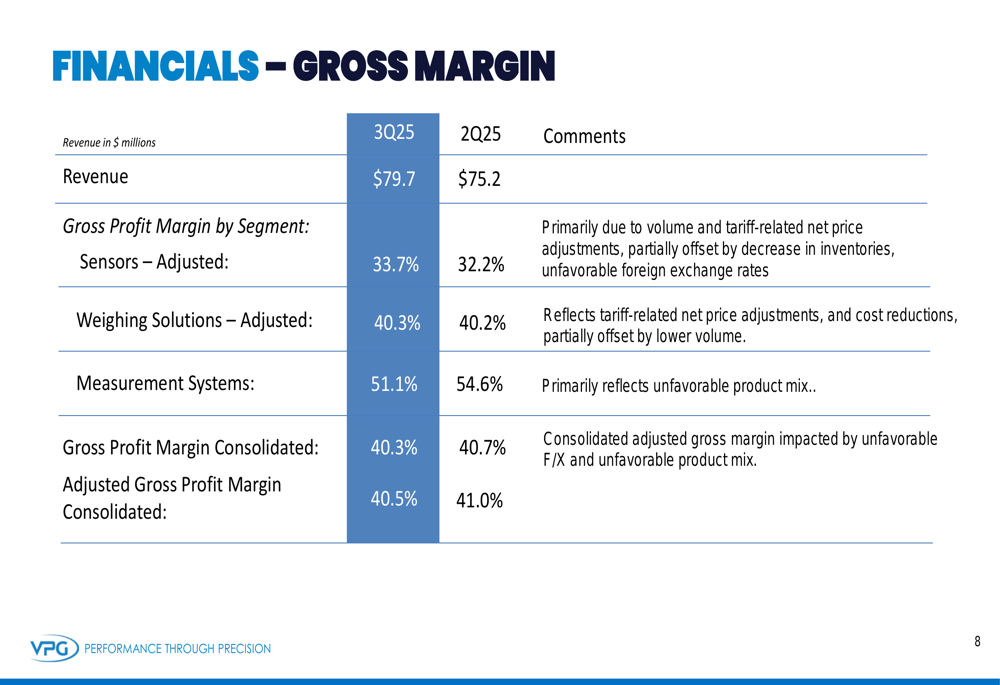

VPG's gross profit margin remained strong at 40.3% in Q3 2025, slightly below the 40.7% reported in Q2. On an adjusted basis, the gross margin was 40.5%, compared to 41.0% in the previous quarter. The marginal decline was attributed to unfavorable foreign exchange rates and product mix, partially offset by tariff-related net price adjustments and cost reductions.

The gross margin breakdown by segment reveals:

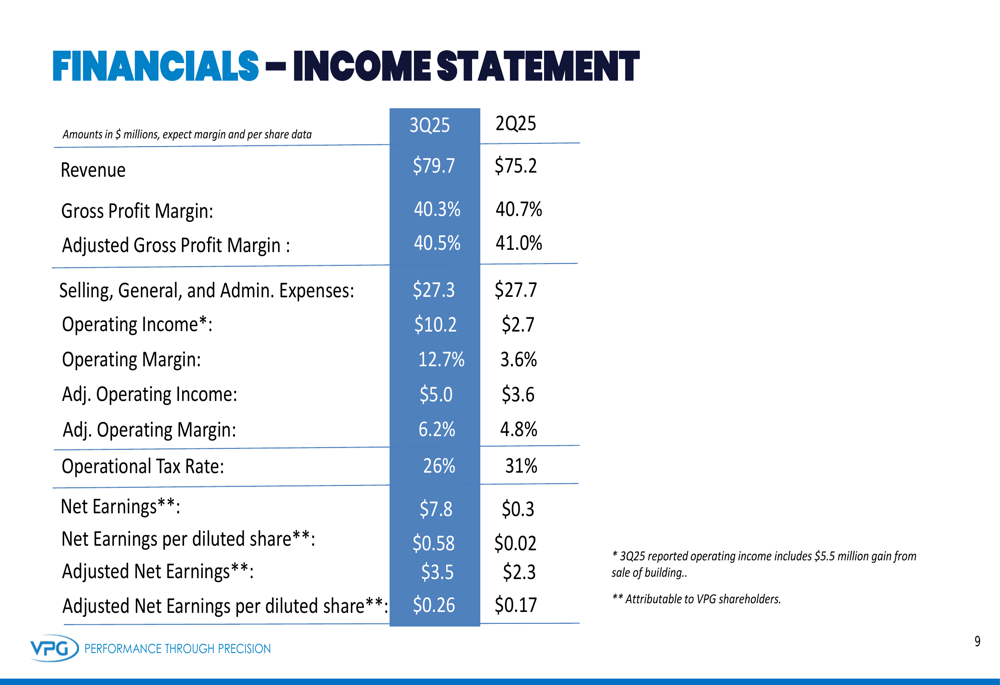

Operating income increased significantly to $10.2 million (12.7% margin) from $2.7 million (3.6% margin) in Q2, though this included a $5.5 million gain from the sale of a building. Adjusted operating income, which excludes this one-time gain, improved to $5.0 million (6.2% margin) from $3.6 million (4.8% margin), reflecting the company's operational improvements.

Net earnings attributable to VPG shareholders reached $7.8 million or $0.58 per diluted share, compared to $0.3 million or $0.02 per diluted share in Q2. On an adjusted basis, excluding the building sale gain and other one-time items, net earnings were $3.5 million or $0.26 per diluted share, up from $2.3 million or $0.17 per diluted share.

The comprehensive income statement comparison is shown here:

VPG generated adjusted EBITDA of $9.2 million or 11.5% of revenue in Q3. While cash from operations was negative at -$1.3 million compared to $6.0 million in Q2, adjusted free cash flow remained positive at $7.4 million, up from $4.7 million in the previous quarter, benefiting from the building sale proceeds.

The company maintained a strong balance sheet with $86.3 million in cash and cash equivalents. Total long-term debt decreased significantly to $20.6 million from $31.5 million, as the company used the $10.8 million in proceeds from the building sale to pay down its outstanding bank revolver balance, which is expected to save approximately $660,000 in annual interest expense.

The cash flow and balance sheet highlights are detailed here:

Strategic Initiatives

VPG continues to execute on its three strategic priorities for 2025: business development, cost controls and operational excellence, and M&A.

The company reported that orders for business development initiatives totaled approximately $26 million year-to-date, keeping it on track to meet its full-year goal. Notably, VPG received $1.8 million in follow-on orders from July through October 2025 for two ongoing humanoid robot applications, highlighting its growing presence in this emerging market.

On the cost control front, VPG completed the sale of a building for $10.8 million as part of its ongoing manufacturing consolidations and relocations. The company reported that its targeted annual fixed cost reductions of $5 million remain on track, with approximately $4 million already realized according to the earnings call.

To support future growth, VPG added two new C-Suite positions: Chief Business and Product Officer and Chief Operating Officer. These additions are intended to enable accelerated growth and operational improvements.

The company's strategic priorities and progress are summarized here:

Market Trends and Forward Outlook

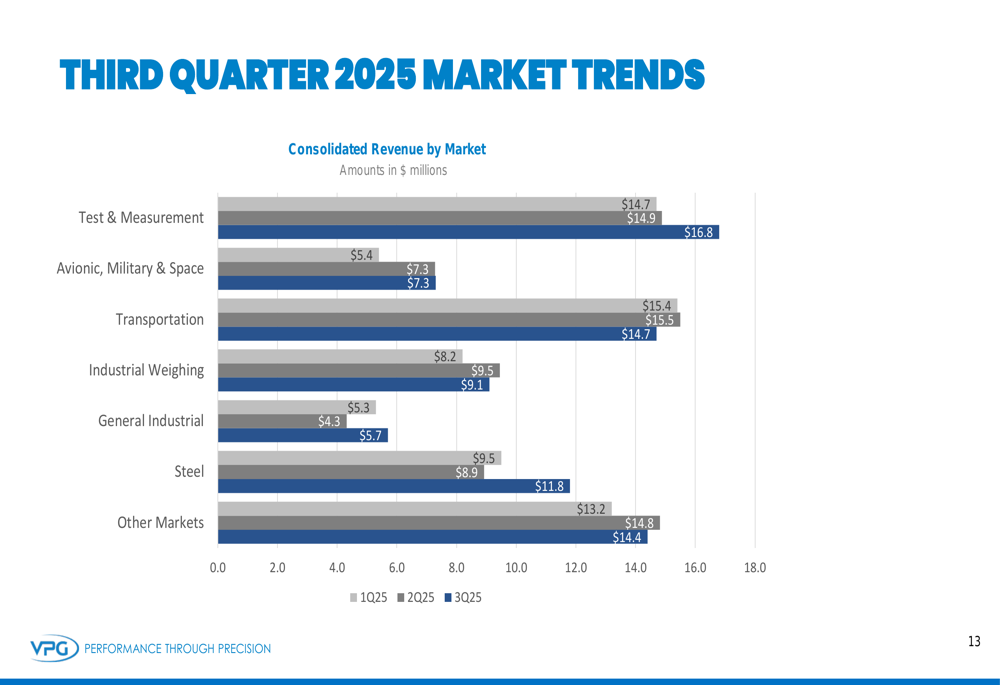

VPG's presentation included a breakdown of revenue by market segment, showing mixed performance across different sectors. Test & Measurement and Steel markets showed the strongest sequential growth, while Transportation experienced a decline.

The market trends are illustrated in this chart:

During the earnings call, CEO Zeev Shashani expressed satisfaction with the quarter's results, stating, "We are pleased with the solid quarter. We see a stable, moderately improved business environment." CFO Bill Clancy highlighted the company's focus on humanoid robotics, noting, "We remain excited about the potential of our business development initiatives."

Looking ahead, VPG forecasts Q4 2025 revenue between $75 million and $81 million, suggesting a potentially flat to slightly higher sequential performance. The company faces ongoing challenges in the transportation, construction, and precision agriculture markets, as well as delays in defense and space projects attributed partly to the U.S. government shutdown.

On a positive note, VPG is making progress on its sustainability initiatives, having recently published its first Sustainability Report. The company is currently undertaking a Climate Risk Assessment and setting Greenhouse Gas Goals and Targets.

Overall, VPG's Q3 2025 results demonstrate the company's ability to navigate a mixed market environment while improving profitability through operational efficiency and strategic initiatives. The strong performance in the Sensors segment, combined with record margins in Weighing Solutions despite lower volumes, highlights the effectiveness of the company's business strategy and cost control measures.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.