Aspire Biopharma faces potential Nasdaq delisting after compliance shortfall

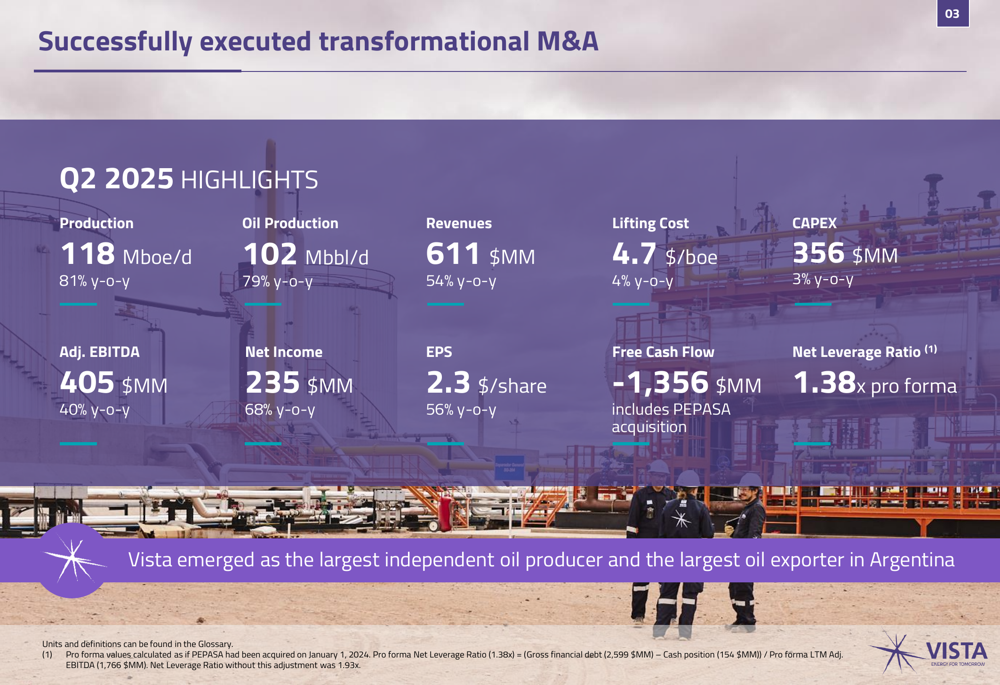

Vista Energy (BMV:VISTA), Argentina’s largest independent oil producer, presented its second quarter 2025 results on July 11, highlighting a transformational period marked by significant growth following its strategic acquisition of PEPASA. The company reported substantial increases across key operational and financial metrics, cementing its position as the leading oil exporter in Argentina.

Quarterly Performance Highlights

Vista Energy delivered exceptional growth in Q2 2025, with total production reaching 118 Mboe/d, representing an 81% increase year-over-year. Oil production, which constitutes the majority of Vista’s output, grew by 79% to 102.2 Mbbl/d. Natural gas production saw even stronger growth, increasing 93% year-over-year to 2.44 MMm3/d.

This production surge translated into revenues of $611 million, a 54% increase compared to Q2 2024, despite lower realized oil prices. The company’s adjusted EBITDA reached $405 million, up 40% year-over-year, while net income grew 68% to $235 million.

As shown in the following comprehensive overview of Vista’s Q2 2025 performance:

"Vista emerged as the largest independent oil producer and the largest oil exporter in Argentina," the company stated in its presentation, highlighting the transformative impact of its recent acquisition activities. The company’s earnings per share increased 56% year-over-year to $2.3/share.

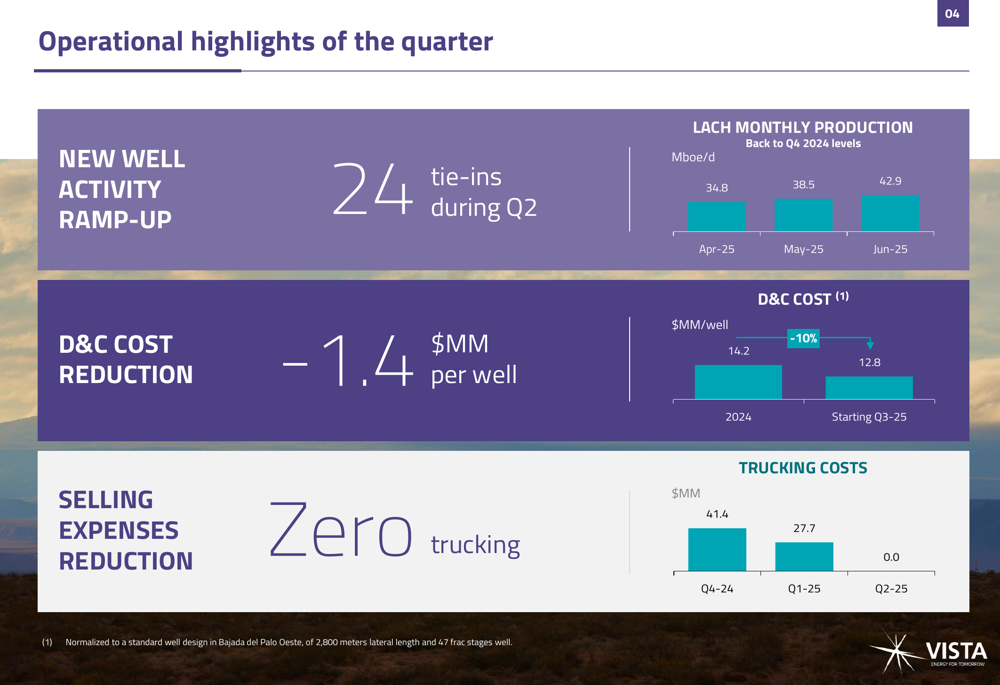

Operational Improvements

The quarter was marked by significant operational enhancements that contributed to Vista’s strong performance. The company tied in 24 new wells during Q2 and achieved a $1.4 million reduction in drilling and completion (D&C) costs per well, representing a 10% improvement.

A major operational milestone was the complete elimination of trucking costs, as the Oldelval pipeline expansion came online by the end of Q1 2025. This operational improvement led to savings of $28 million compared to Q1 2025 and $41 million compared to Q4 2024.

The following chart illustrates these key operational improvements:

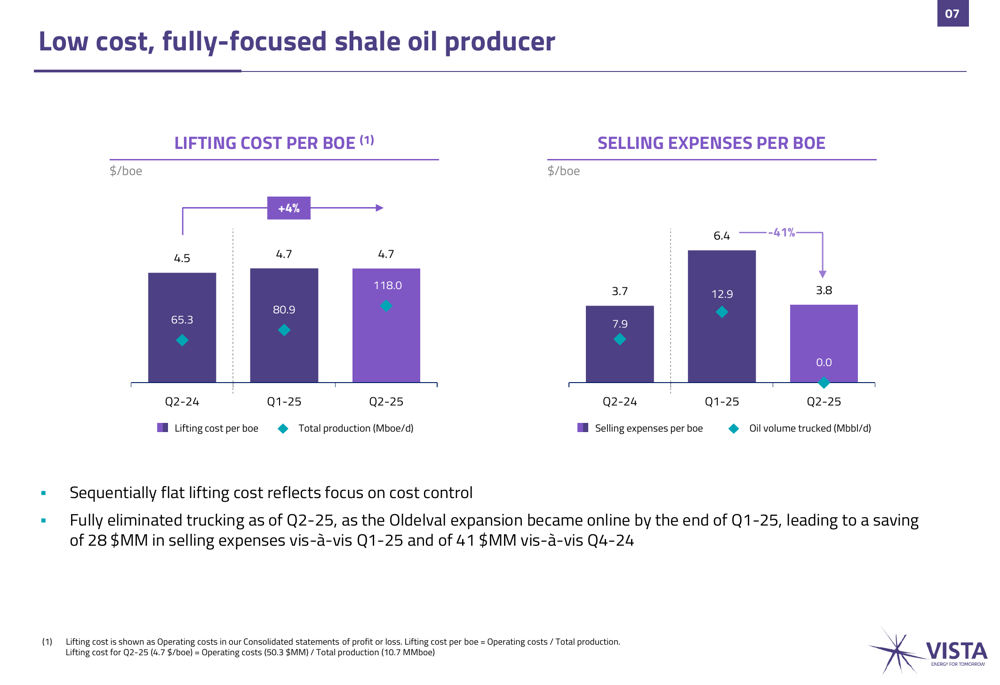

The company maintained disciplined cost control despite the significant expansion of operations. Lifting costs remained stable at $4.7/boe quarter-over-quarter, while selling expenses per barrel decreased dramatically from $12.9/boe in Q1 2025 to $3.8/boe in Q2, primarily due to the elimination of trucking costs.

As shown in the following cost efficiency metrics:

Financial Analysis

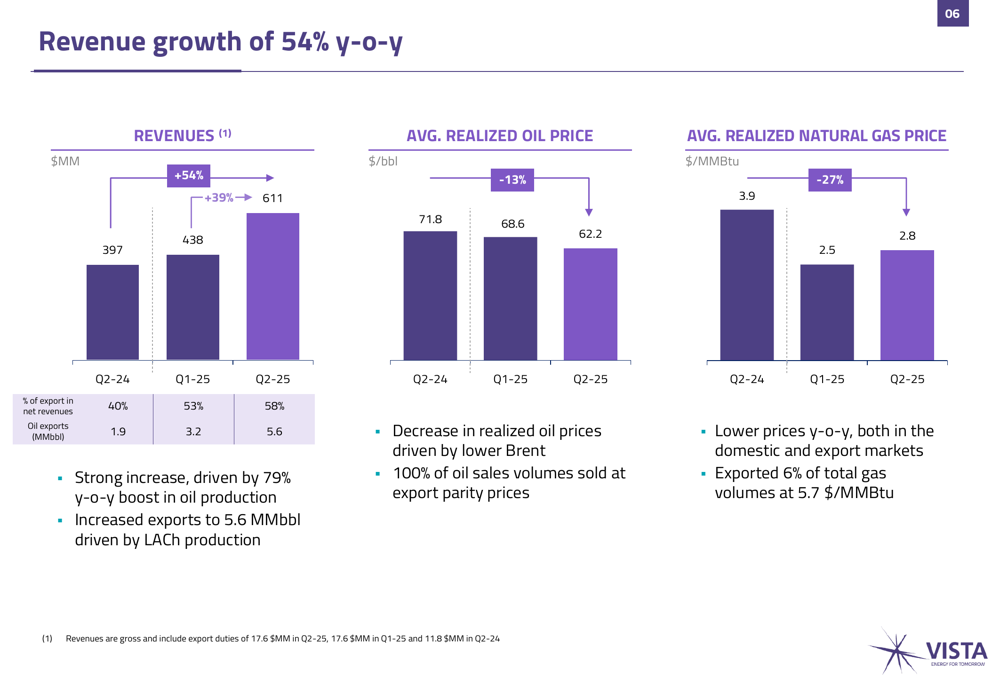

Vista’s revenue growth of 54% year-over-year is particularly impressive considering the challenging price environment. The company’s realized oil price decreased 13% year-over-year to $62.2/bbl, while natural gas prices fell 27% to $2.8/MMBtu.

The company significantly increased its export orientation, with exports representing 58% of net revenues in Q2 2025, up from 40% in Q2 2024. Oil exports more than doubled to 5.6 MMbbl in Q2 2025 from 1.9 MMbbl in the same period last year.

The following chart illustrates Vista’s revenue growth despite lower commodity prices:

Adjusted EBITDA increased 40% year-over-year to $405 million, with EBITDA margins improving to 66% from 62% in the previous quarter. This margin improvement, achieved despite lower oil prices, reflects the company’s focus on cost control and operational efficiency.

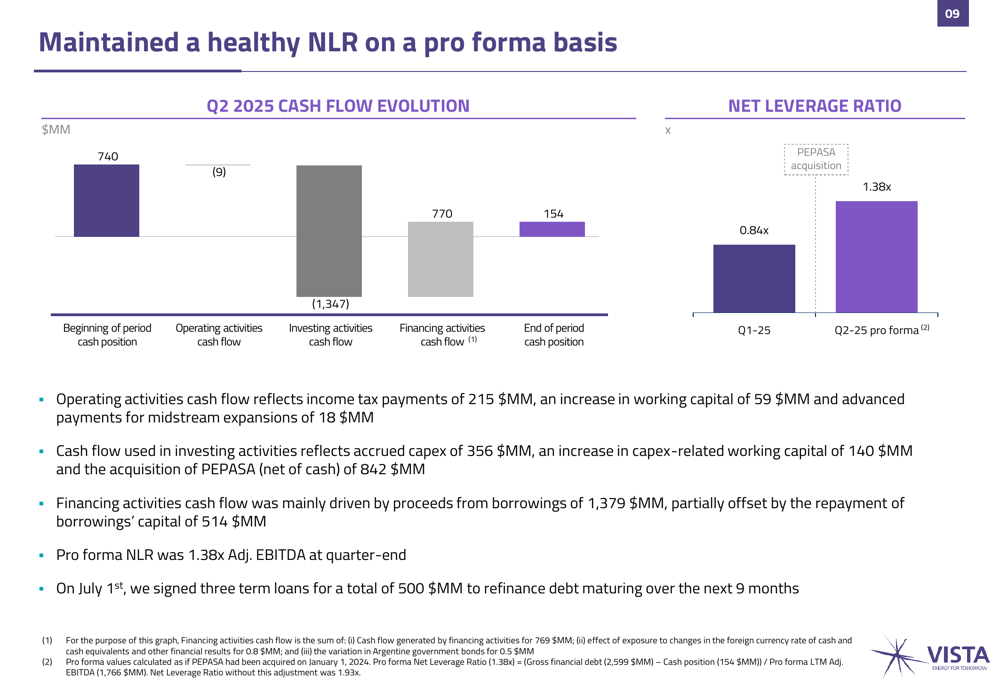

The company’s financial position reflects the impact of its recent acquisition activity. Free cash flow was negative at $1,356 million, primarily due to the PEPASA acquisition. The net leverage ratio stood at 1.38x on a pro forma basis, which the company considers healthy given the transformational nature of its recent acquisitions.

As illustrated in the cash flow evolution chart:

Vista secured additional financing to strengthen its balance sheet, signing three term loans totaling $500 million on July 1st to refinance debt maturing over the next nine months.

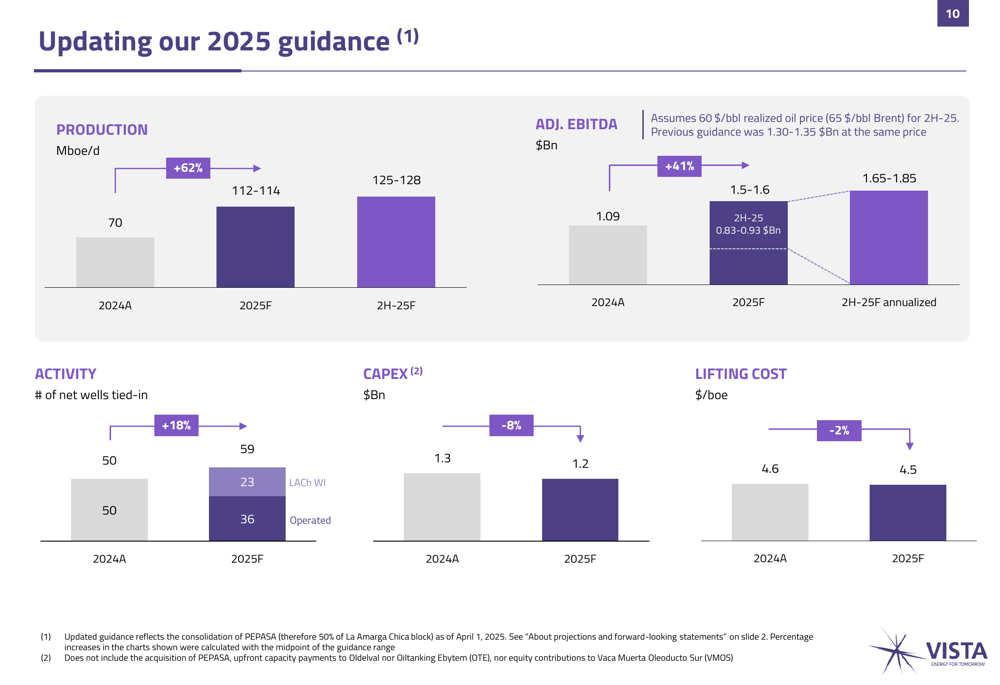

Updated 2025 Guidance

Vista provided an updated guidance for 2025, projecting continued strong growth. The company expects total production to reach 112-114 Mboe/d for the full year 2025, representing a 62% increase from 2024. For the second half of 2025, production is forecast to reach 125-128 Mboe/d.

Adjusted EBITDA is projected to be between $1.5-1.6 billion for 2025, a 41% increase from 2024. The company plans to connect 59 net wells in 2025, an 18% increase from 2024, while reducing capital expenditures by 8% to $1.2 billion.

The following chart details Vista’s updated 2025 guidance:

The updated guidance assumes a realized oil price of $60/bbl (Brent at $65/bbl) for the second half of 2025. The company expects to achieve neutral free cash flow in the second half of the year as capital expenditures moderate and production continues to increase.

Strategic Positioning

Vista’s Q2 2025 results reflect its successful execution of a transformational growth strategy. The acquisition of PEPASA and the consolidation of a 50% working interest in La Amarga Chica have significantly expanded the company’s production base and export capabilities.

The company’s focus on operational efficiency and cost control has allowed it to maintain strong margins despite lower oil prices. The elimination of trucking costs and reduction in drilling and completion costs demonstrate Vista’s commitment to continuous improvement.

Following the earnings announcement, Vista’s stock price rose by 2.44% to $38.34, reflecting positive investor sentiment. The stock currently trades at a P/E ratio of 6.9, which appears low relative to the company’s growth trajectory.

As summarized in the closing remarks of the presentation:

Vista’s transformation into Argentina’s largest independent oil producer and leading oil exporter positions the company for continued growth in the coming years. With its low-cost production base, increasing export orientation, and disciplined capital allocation, Vista appears well-positioned to deliver on its ambitious growth targets for 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.