BETA Technologies launches IPO of 25 million shares priced $27-$33

Introduction & Market Context

Vista Land and Lifescapes Inc (PSE:VLL) reported its full-year 2024 results on May 7, 2025, showing modest revenue growth coupled with significant margin expansion, though higher financing costs weighed on bottom-line performance. The Philippine property developer, which operates across 147 cities and municipalities in 49 provinces, saw its stock trading at ₱1.58 as of May 20, 2025, up 1.9% following the presentation.

The company maintained its diversified approach across residential and commercial segments while continuing to expand its footprint through new project launches valued at approximately ₱40.8 billion.

Financial Performance Highlights

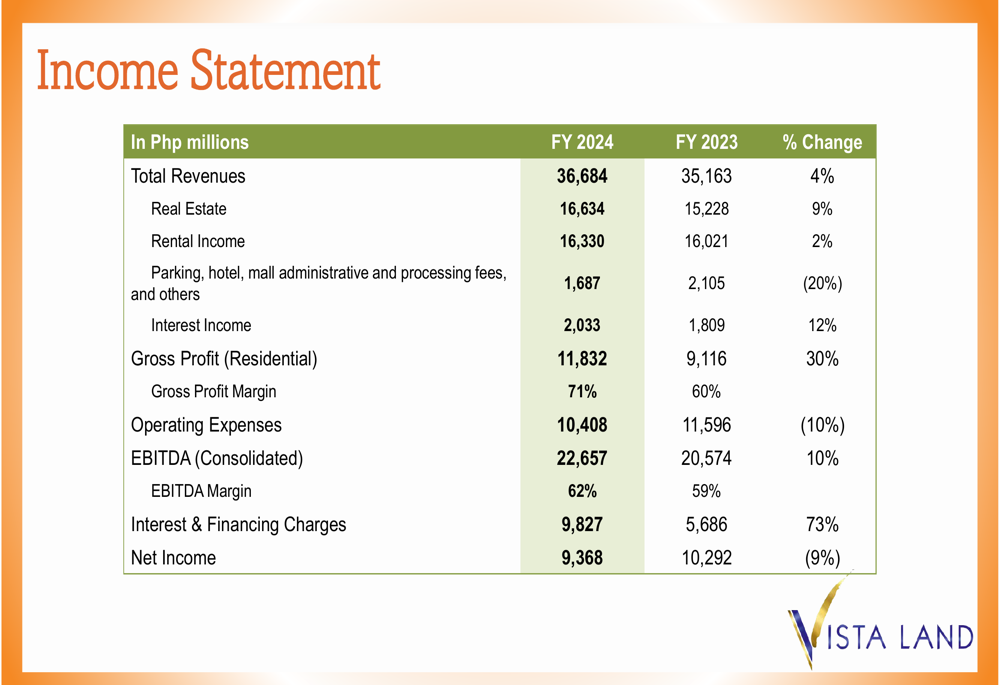

Vista Land reported total revenue of ₱36.7 billion for fiscal year 2024, representing a 4% increase from the ₱35.2 billion recorded in 2023. The company’s gross profit reached ₱11.8 billion with a significantly improved gross profit margin of 71%, up from 60% in the previous year.

As shown in the following income statement breakdown:

EBITDA grew by 10% to ₱22.7 billion, with the EBITDA margin expanding to 62% from 59% in FY 2023. However, net income declined by 9% to ₱9.4 billion, primarily due to a substantial 73% increase in interest and financing charges, which rose to ₱9.8 billion from ₱5.7 billion in the previous year.

The company’s real estate revenue increased by 9% to ₱16.6 billion, while rental income showed modest growth of 2% to ₱16.3 billion. Interest income also grew by 12% to ₱2.0 billion.

Segment Performance Analysis

Vista Land’s residential segment demonstrated strong performance with reservation sales increasing by 10% to ₱79.1 billion in FY 2024 from ₱71.9 billion in FY 2023. The fourth quarter of 2024 alone saw reservation sales of ₱20.6 billion, representing a 9.4% increase compared to the same period in 2023.

The residential segment’s performance is illustrated in the following chart:

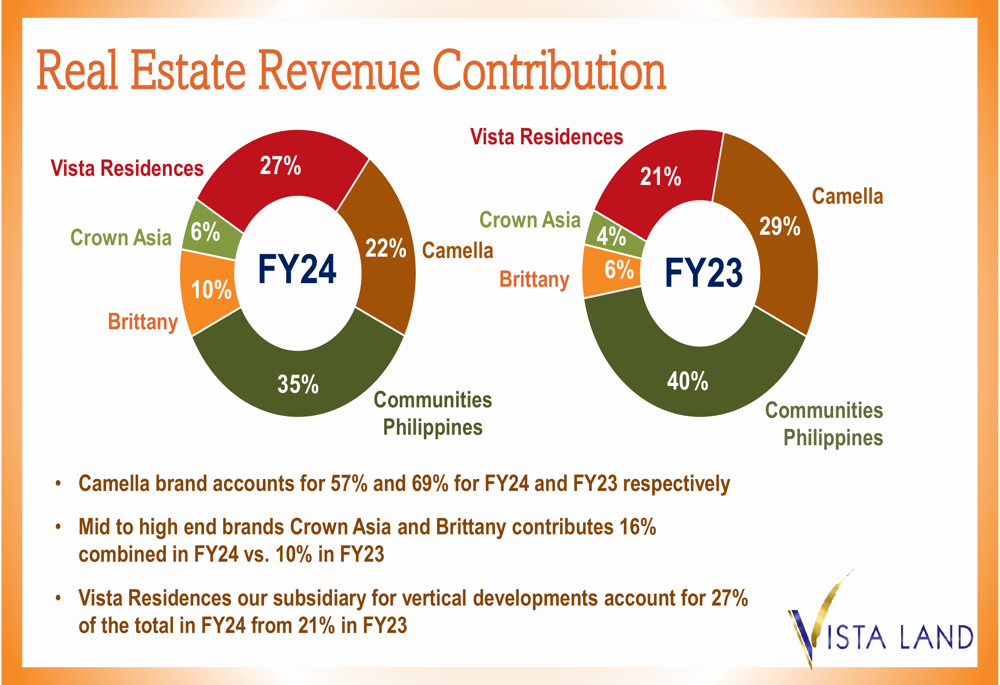

The company’s real estate revenue contribution showed a notable shift in brand mix. Vista Residences, the company’s vertical development arm, increased its contribution to 27% of total real estate revenue in FY 2024, up from 21% in FY 2023. Meanwhile, Camella’s contribution decreased to 22% from 29% in the previous year.

This strategic shift toward higher-end and vertical developments is evident in the following breakdown:

The mid to high-end brands Crown Asia and Brittany increased their combined contribution to 16% in FY 2024, up from 10% in FY 2023, further indicating the company’s strategic pivot toward premium segments.

Commercial Portfolio and Leasing Operations

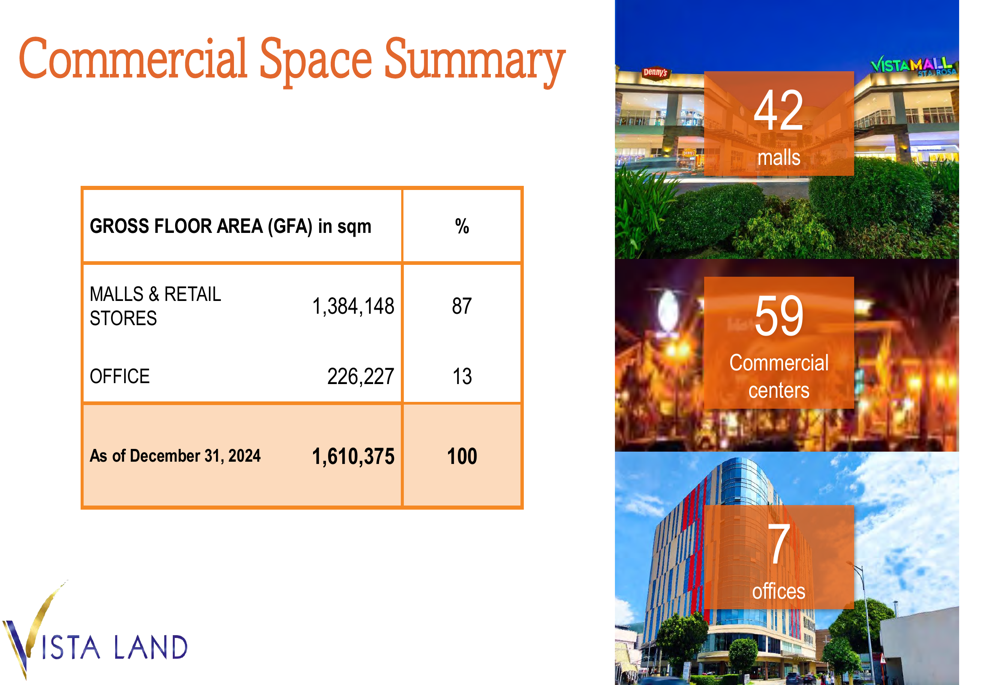

Vista Land’s commercial space portfolio reached a total gross floor area (GFA) of 1.61 million square meters as of December 31, 2024. Malls and retail stores account for 87% (1.38 million sqm) of this space, while office space represents the remaining 13% (226,227 sqm).

The company’s commercial assets include 42 malls, 59 commercial centers, and 7 offices, as detailed in the following summary:

Leasing operations maintained stable performance with system-wide occupancy rates at 87%, mall occupancy at 86%, and office occupancy at 92%. Foot traffic has fully recovered to pre-COVID levels, reaching 100% of pre-pandemic figures.

Balance Sheet and Capital Management

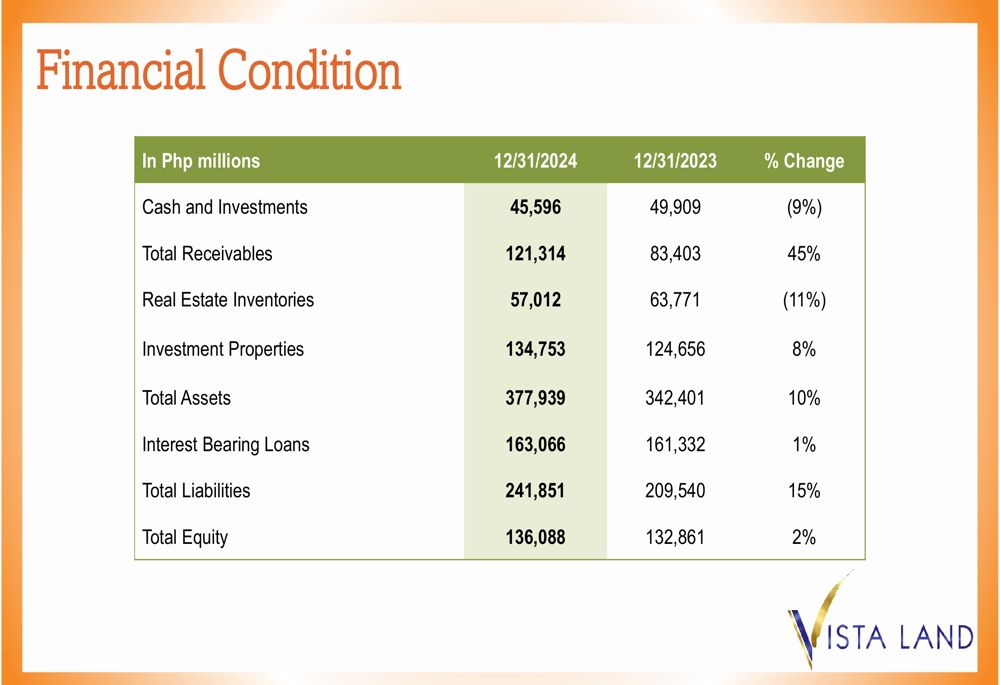

Vista Land’s total assets grew by 10% to ₱377.9 billion as of December 31, 2024, from ₱342.4 billion at the end of 2023. The company’s financial condition showed significant growth in total receivables, which increased by 45% to ₱121.3 billion, while investment properties rose by 8% to ₱134.8 billion.

The company’s financial position is summarized in the following table:

Vista Land maintained a relatively stable debt profile with a slight increase in its net debt to equity ratio to 0.86x from 0.84x in the previous year. Total (EPA:TTEF) interest-bearing debt increased marginally by 1% to ₱163.1 billion, while cash and investments decreased by 9% to ₱45.6 billion.

The company’s debt profile shows a balanced funding mix with bank loans (34%), corporate notes (31%), USD bonds (22%), and retail peso bonds (13%). The debt maturity profile indicates 61% long-term debt and 39% short-term debt.

Strategic Initiatives and Outlook

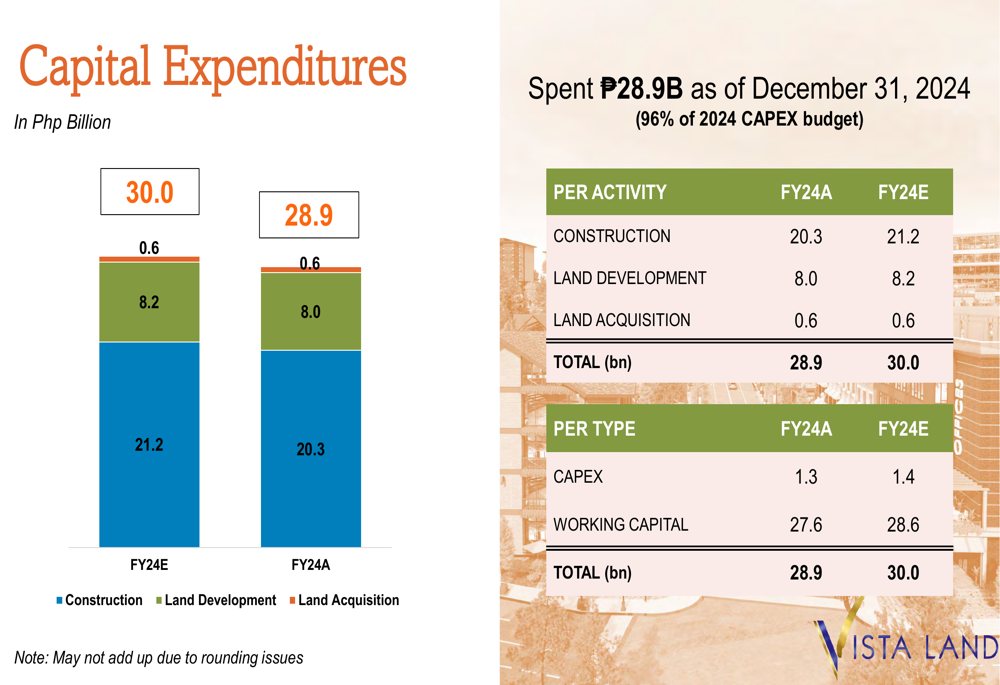

Vista Land launched 25 projects with an estimated value of ₱40.8 billion during 2024, demonstrating its continued commitment to expansion. The company deployed ₱28.9 billion in capital expenditures, representing 96% of its 2024 CAPEX budget.

The capital expenditure breakdown is illustrated below:

The company maintains a substantial land bank of 2,690.52 hectares, with 85% owned directly and 15% through joint ventures. This land bank is strategically distributed with 70% in provincial areas and 30% in Mega Manila, positioning the company for continued growth across diverse markets.

Vista Land also successfully refinanced $150 million through international banks, including SMBC, Chang Hwa Bank, Mega International Commercial Bank, First Commercial Bank, Cathay United Bank, and OBank, strengthening its financial flexibility for future developments.

Despite higher financing costs impacting net income, Vista Land’s improved margins, strong reservation sales, and strategic shift toward premium segments position the company to navigate the evolving real estate landscape in the Philippines.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.