Stock market today: S&P 500 hits fresh record close on stronger economic growth

Visteon Corp (NASDAQ:VC) shares rose 1.59% in premarket trading to $116 after the company presented its Q2 2025 earnings results on July 24, building on the previous day’s 3.99% gain. The automotive electronics supplier reported solid performance with expanded margins and raised its full-year guidance despite ongoing challenges in China.

Quarterly Performance Highlights

Visteon delivered $969 million in net sales for Q2 2025, achieving 1% growth-over-market despite headwinds in certain segments. The company reported adjusted EBITDA of $134 million, representing a robust 13.8% margin, and generated $67 million in adjusted free cash flow. The quarter’s performance was characterized by strong operational discipline and continued expansion into adjacent markets.

"We delivered robust growth outside of BMS and China, with 4% growth-over-market excluding China," the company noted in its presentation, highlighting the strategic initiatives that drove $2.0 billion in new business wins during the quarter.

As shown in the following quarterly performance summary:

The company’s balance sheet remains strong with $361 million in net cash, providing flexibility for capital allocation strategies including the recently initiated dividend and a completed bolt-on acquisition.

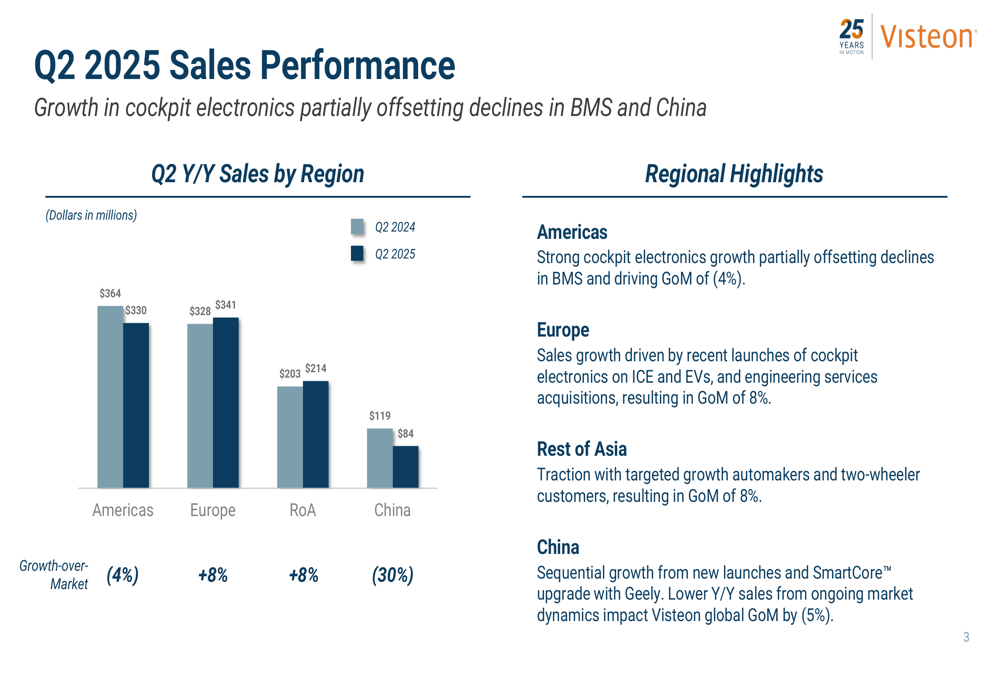

Regional Performance Analysis

Visteon’s regional performance revealed significant variations across markets. While Europe and Rest of Asia demonstrated strong growth with 8% growth-over-market in each region, China continued to face challenges with a 30% decline in growth-over-market. The Americas region showed a 4% decline in growth-over-market, partially offset by strong cockpit electronics growth.

The following regional breakdown illustrates these performance differences:

In Europe, sales growth was driven by recent launches of cockpit electronics on both internal combustion engine (ICE) and electric vehicles (EVs), as well as engineering services acquisitions. Rest of Asia benefited from traction with targeted growth automakers and two-wheeler customers. China, while showing sequential growth from new launches and SmartCore™ upgrades with Geely, continued to face "ongoing market dynamics" that impacted Visteon’s global growth-over-market by 5%.

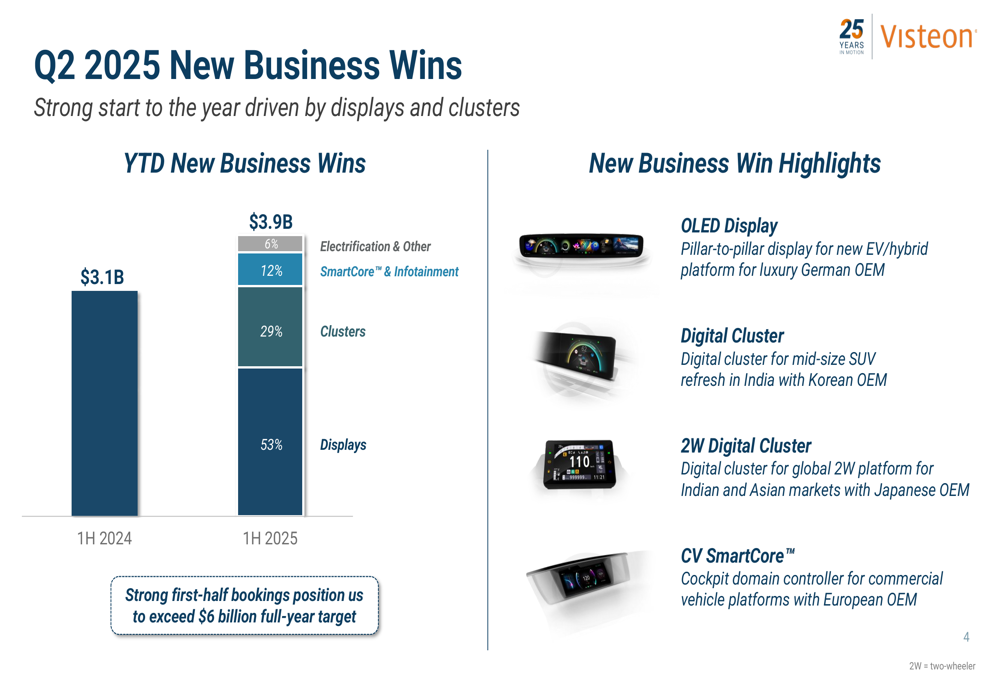

New Business Wins and Product Launches

Visteon reported strong momentum in new business wins, with year-to-date bookings of $3.9 billion, up from $3.1 billion in the first half of 2024. The company noted that these strong first-half bookings position it to exceed its $6 billion full-year target.

The breakdown of new business wins shows displays representing the largest segment at 53%, followed by clusters at 29%, SmartCore™ & Infotainment at 12%, and Electrification & Other at 6%.

The following chart details the composition of these new business wins:

Key wins included a pillar-to-pillar OLED display for a luxury German OEM, a digital cluster for a mid-size SUV in India, a two-wheeler digital cluster for global markets, and a cockpit domain controller for commercial vehicle platforms with a European OEM.

The company also highlighted 21 new product launches across 8 OEMs during the quarter, spanning passenger vehicles, commercial vehicles, and two-wheelers:

Notable launches included SmartCore™ technology for Volvo (OTC:VLVLY)’s EX30 electric vehicle and Volvo Construction commercial vehicles, a 25-inch panoramic display for the Audi Q3, and digital clusters for Royal Enfield’s 350 two-wheeler and Volvo Mack Trucks.

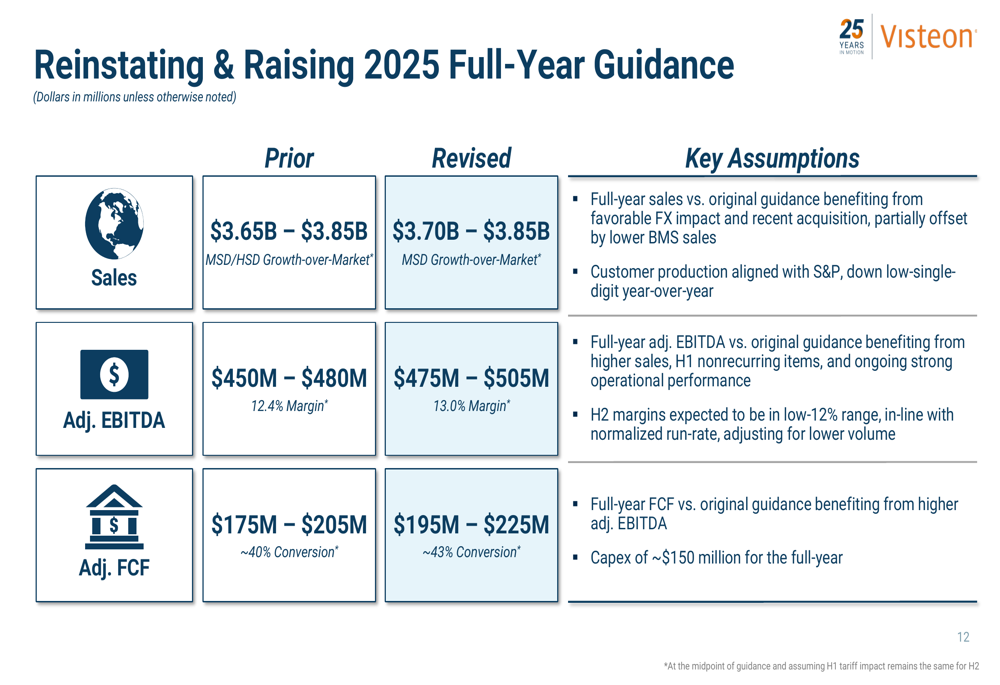

Updated Guidance and Outlook

Based on strong first-half performance, Visteon raised its full-year guidance across all key metrics. The company now expects sales between $3.70 billion and $3.85 billion (up from $3.65-$3.85 billion), adjusted EBITDA between $475 million and $505 million (up from $450-$480 million), and adjusted free cash flow between $195 million and $225 million (up from $175-$205 million).

The revised guidance and key assumptions are detailed in the following slide:

The company noted that its full-year sales guidance benefited from favorable foreign exchange impact and recent acquisitions, partially offset by lower Battery Management Systems (BMS) sales. Customer production is aligned with S&P forecasts, which project a low-single-digit decline year-over-year.

For the second half of 2025, Visteon expects margins to be in the low-12% range, in line with normalized run-rates after adjusting for lower volume. This projection is consistent with the company’s Q1 2025 performance, when it also reported a 13.8% adjusted EBITDA margin.

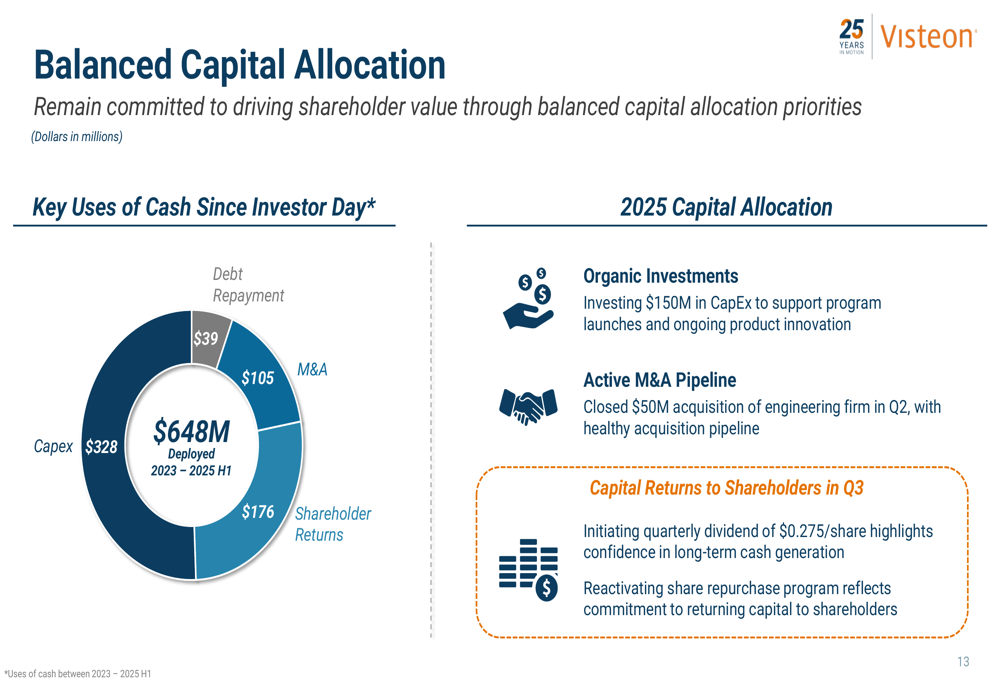

Capital Allocation Strategy

Visteon’s capital allocation strategy remains balanced across organic investments, acquisitions, and shareholder returns. The company announced it is initiating a quarterly dividend of $0.275 per share, highlighting confidence in long-term cash generation. Additionally, Visteon is reactivating its share repurchase program.

In Q2, the company completed a $50 million acquisition of an engineering services firm to enhance domain expertise in User Experience and Human-Machine Interface (NASDAQ:TILE) (HMI). This represents the third acquisition in the last 12 months as Visteon expands and enhances its technology capabilities.

The following chart illustrates Visteon’s capital allocation since its Investor Day:

Between 2023 and the first half of 2025, Visteon deployed a total of $648 million, with $328 million allocated to capital expenditures, $176 million to shareholder returns, $105 million to mergers and acquisitions, and $39 million to debt repayment.

Forward-Looking Statements

Visteon positioned itself as a digital cockpit electronics leader for cars, trucks, and two-wheelers, supporting the industry shift to hybrid and electric vehicles. The company emphasized its innovative product portfolio, competitive cost structure, and balanced capital allocation approach as key elements of its investment thesis.

"Industry-leading cockpit and electrification electronics product portfolio with best-in-class cost structure," the company stated in its investment thesis summary:

Looking ahead, Visteon faces both opportunities and challenges. While the company continues to win new business and expand into adjacent markets like commercial vehicles and two-wheelers, it also faces headwinds from declining customer production forecasts and ongoing challenges in the Chinese market.

The company’s strong balance sheet, with no material debt maturities until 2027, provides financial flexibility to navigate these challenges while continuing to invest in growth opportunities and return capital to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.