Gold prices steady above $3,400/oz on rate cut bets; PCE data awaited

Introduction & Market Context

Vodafone (NASDAQ:VOD) Qatar (DSM:VFQS) released its investor presentation for the first half of fiscal year 2025, revealing accelerated growth across key financial metrics and significant progress in network expansion. The company’s stock closed at 2.435 on July 31, 2025, down 2.05% on the day, but remains near its 52-week high of 2.665.

The presentation follows Vodafone Qatar’s strong Q1 2025 performance, where the company reported 6.1% year-over-year revenue growth. The latest results indicate a notable acceleration in Q2, contributing to the impressive first-half figures.

H1 2025 Financial Highlights

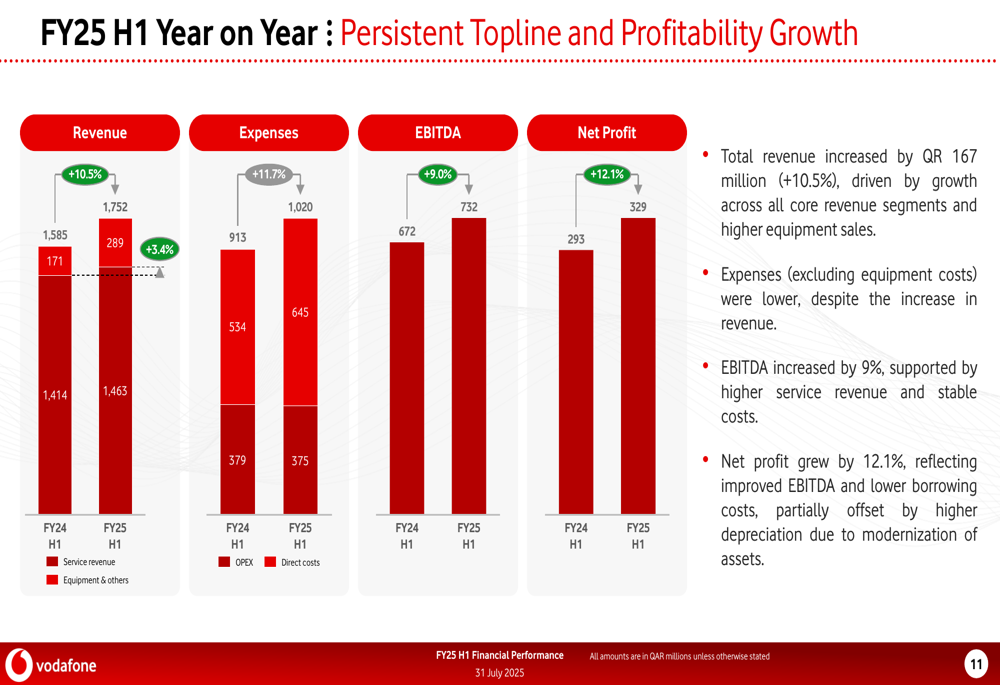

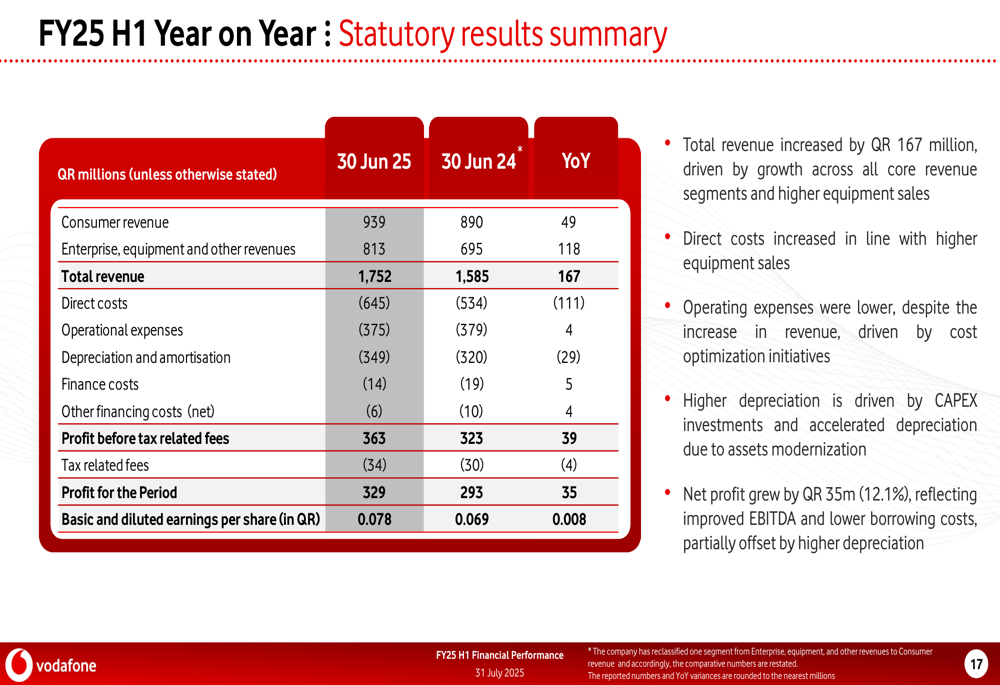

Vodafone Qatar reported total revenue of QR 1,752 million for H1 2025, representing a 10.5% increase year-over-year. Net profit grew even faster at 12.1% to reach QR 329 million, while EBITDA rose 9% to QR 732 million.

As shown in the following chart of year-on-year financial performance:

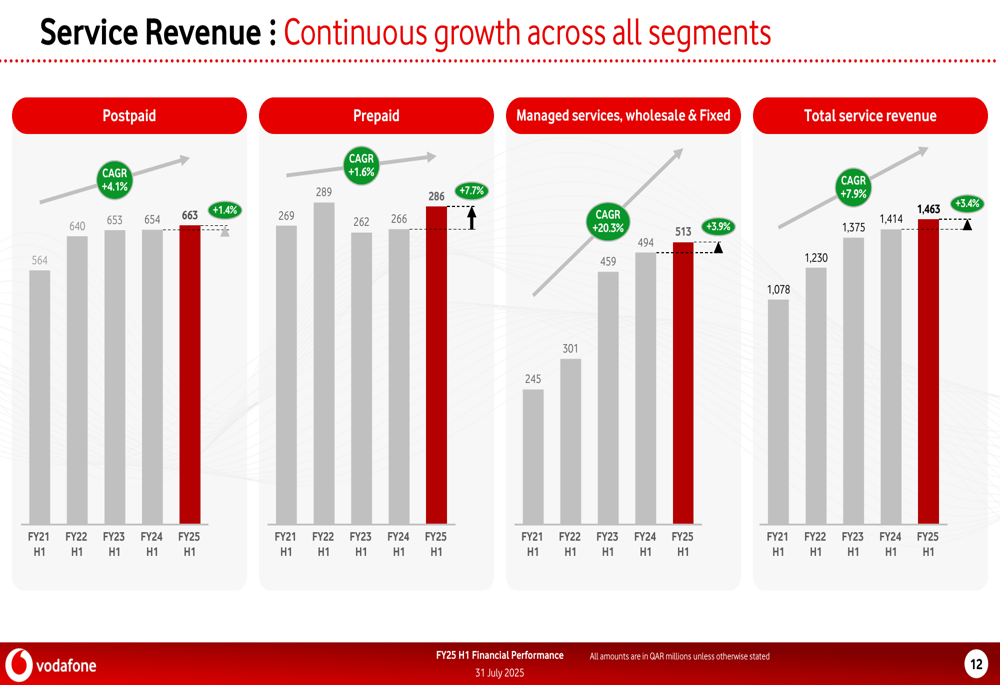

The company’s service revenue, which excludes equipment sales, reached QR 1,463 million with growth across all segments. Postpaid services continue to be the largest contributor to service revenue, followed by prepaid and managed services.

The breakdown of service revenue by segment demonstrates balanced growth:

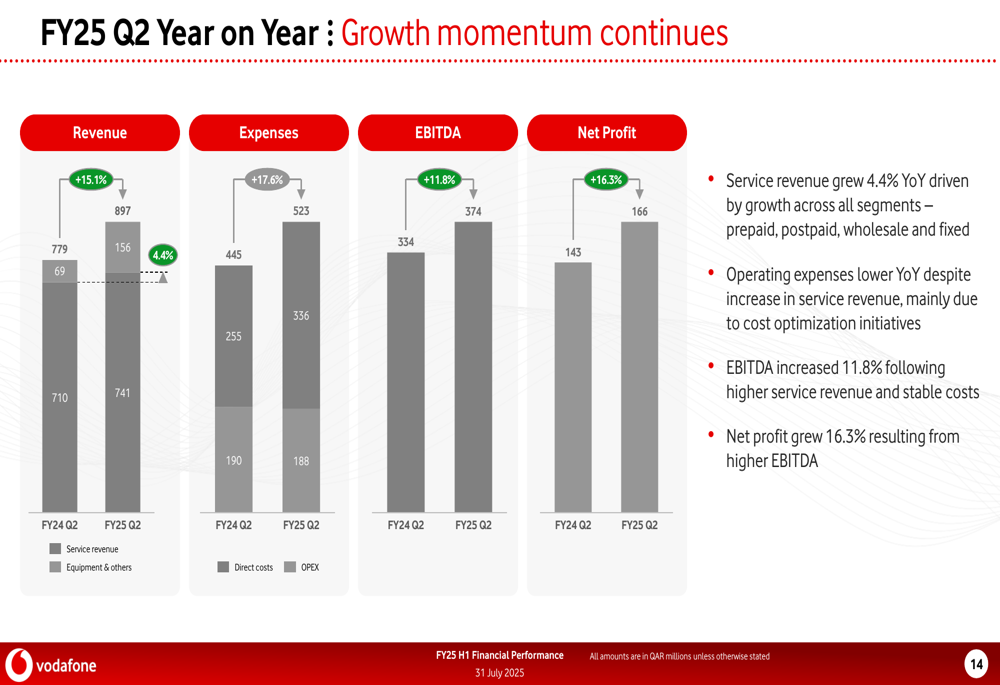

Q2 performance was particularly strong, showing acceleration from Q1 results. For the second quarter, Vodafone Qatar reported:

- Revenue of QR 897 million (+4.4% YoY)

- EBITDA of QR 374 million (+11.8% YoY)

- Net profit of QR 166 million (+16.3% YoY)

This quarterly performance breakdown reveals the momentum building in the company’s operations:

Network Expansion and Digital Transformation

Vodafone Qatar’s financial growth is underpinned by significant investments in network infrastructure and digital capabilities. The company reported a 52% year-over-year increase in 5G indoor network sites and a 12% increase in 5G outdoor network sites, with over 90% of outdoor sites now upgraded with a second carrier.

The company’s digitalization efforts have yielded impressive results, with digital visits growing 16% year-over-year and e-commerce sales surging 2.25x compared to the previous year. Digital channel revenue increased by 49%, reflecting successful customer migration to digital platforms.

Profitability Improvements and Margin Expansion

Vodafone Qatar has made significant strides in improving operational efficiency, with operating expenses decreasing by 1.2% despite revenue growth. This has led to a 2.5 percentage point improvement in OPEX intensity, which now stands at 21.4%.

The company’s EBITDA margin expanded by 2.7 percentage points, while net profit margin increased by 0.4 percentage points. These improvements reflect Vodafone Qatar’s focus on cost management and operational efficiency.

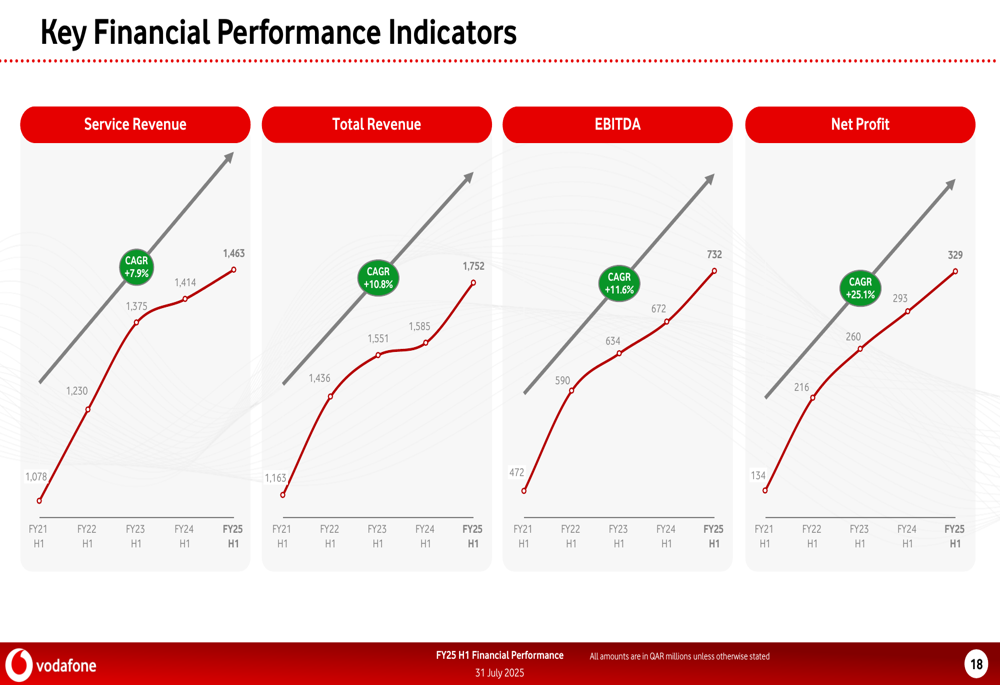

The company’s long-term EBITDA growth has significantly outperformed the market:

Financial efficiency metrics also show improvement, with return on equity (ROE) increasing to 12.8% (+0.8 percentage points) and free cash flow growing by 16.8%. Net debt to EBITDA decreased to 0.30x, indicating a strengthened balance sheet.

The comprehensive statutory results provide a detailed view of the company’s financial performance:

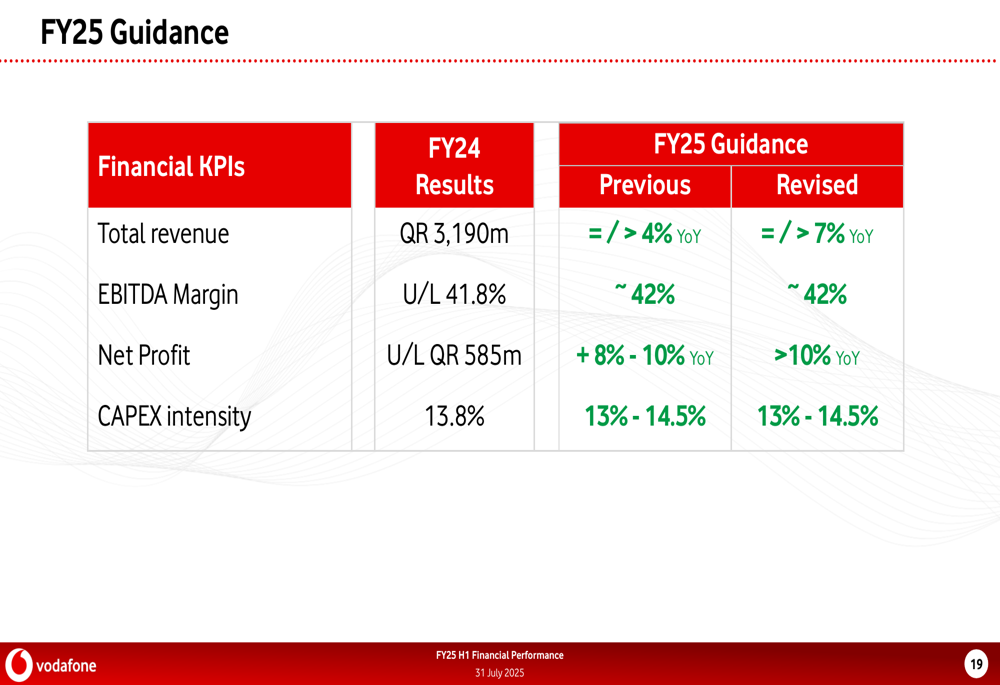

Updated Guidance and Outlook

Following the strong first-half performance, Vodafone Qatar has raised its full-year guidance for FY25:

The company now expects total revenue growth of at least 7% year-over-year, up from the previous guidance of over 4% mentioned in the Q1 earnings call. EBITDA margin is projected to remain stable at approximately 42%, while net profit is expected to grow by more than 10% year-over-year.

Capital expenditure intensity is forecasted to be between 13% and 14.5%, reflecting continued investments in network infrastructure and digital capabilities.

Sustainability and Strategic Initiatives

Vodafone Qatar has also made progress in its sustainability efforts, with 95% of diesel generator sites achieving hybrid active status. The company highlighted its ESG achievements, including 89% digital invoice payments and a 4-star GSAS rating for its facilities.

Strategic partnerships with digital and consumer businesses such as Talabat, Snoonu, and Uber (NYSE:UBER) are expected to further enhance the company’s digital ecosystem and drive future growth.

The company’s focus on customer experience has yielded positive results, with digital TNPS improving by 14% year-over-year and Customer Effort Score (CES) reducing by 7%, indicating enhanced customer satisfaction.

As Vodafone Qatar continues to execute its growth strategy, the combination of network expansion, digital transformation, and operational efficiency positions the company well for sustained performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.