Caterpillar bids for Australia’s RPMGlobal- AFR

Introduction & Market Context

Vodafone (NASDAQ:VOD) Qatar P.Q.S.C. (DSM:VFQS) reported solid financial results for the first quarter of fiscal year 2025, showcasing continued growth across all business segments. The company presented its quarterly performance on April 22, 2025, highlighting its successful diversification strategy and improved profitability metrics.

The telecom provider’s stock closed at QR 2.13 on the presentation day, up 3.38% and approaching its 52-week high of QR 2.21, reflecting positive investor sentiment toward the company’s performance and strategic direction.

Quarterly Performance Highlights

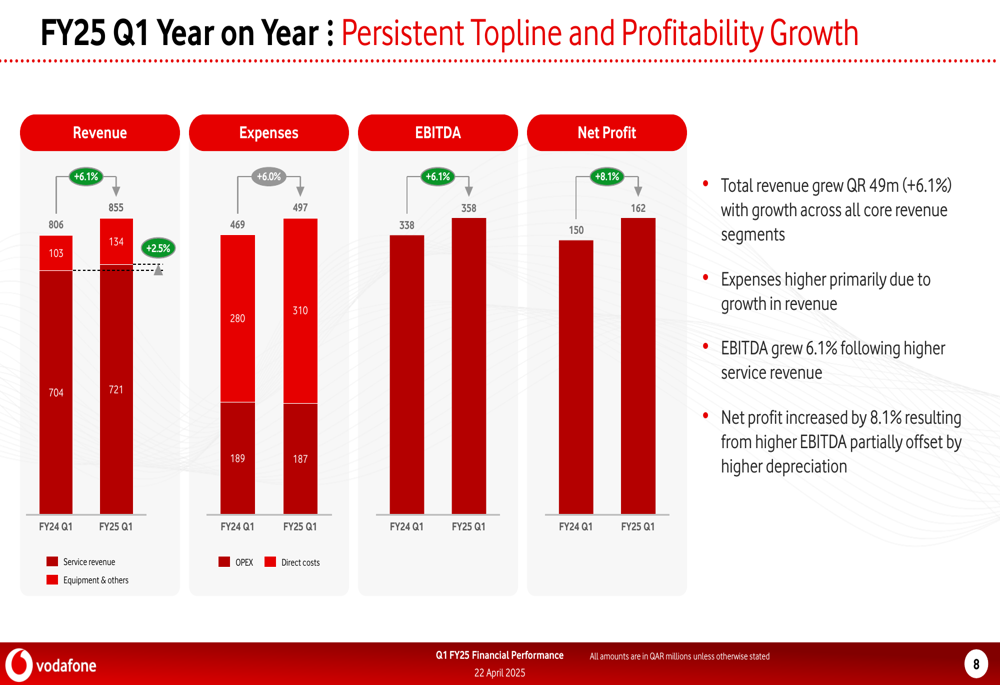

Vodafone Qatar reported total revenue of QR 855 million for Q1 FY25, representing a 6.1% increase year-over-year, while net profit rose 8.1% to QR 162 million compared to the same period last year.

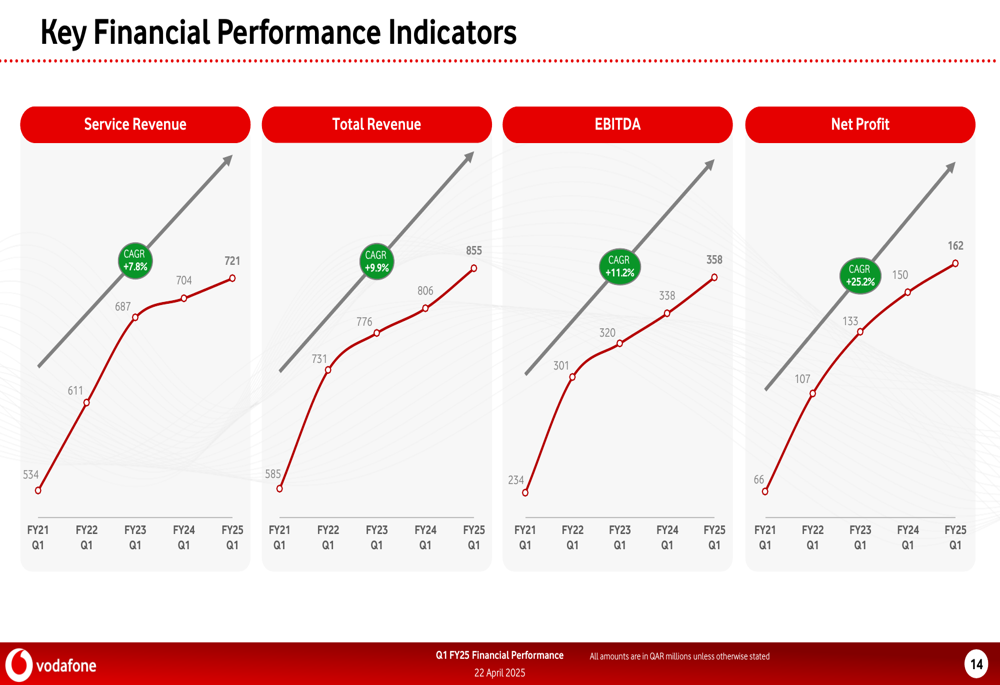

As shown in the following chart of quarterly financial performance, the company demonstrated growth across all key metrics, with EBITDA rising 6.1% to QR 358 million:

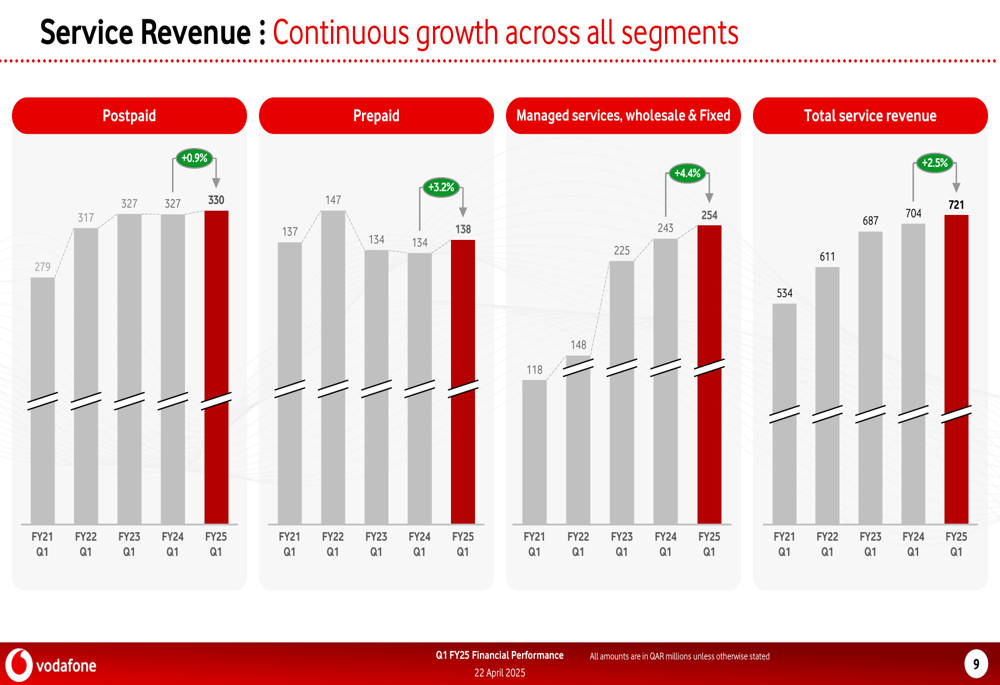

The company’s service revenue reached QR 721 million, up from QR 687 million in Q1 FY24, with growth across all segments. Postpaid revenue increased to QR 330 million, prepaid revenue grew to QR 138 million, and managed services, wholesale & fixed revenue rose to QR 254 million.

This segment breakdown illustrates the company’s diversified revenue streams:

CEO Hamad Al-Thani emphasized the company’s strategic focus on diversification, noting that more than 41% of revenue now comes from outside mobile services, representing a significant 23 percentage point increase over the past five years.

Detailed Financial Analysis

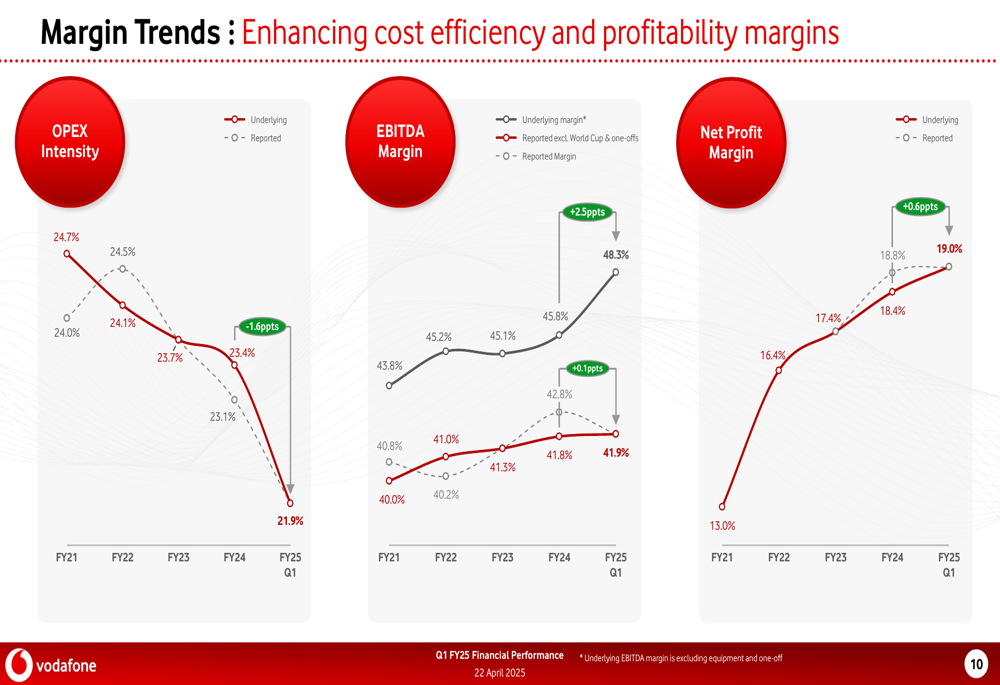

Vodafone Qatar demonstrated improved operational efficiency in Q1 FY25, with OPEX intensity decreasing from 24.1% to 21.9% year-over-year. This efficiency gain, combined with revenue growth, helped drive margin improvements across the board.

The company’s EBITDA margin expanded to 48.3% from 45.8% in the prior-year period, while net profit margin increased to 19.0% from 17.4%, as illustrated in the following margin trends:

Capital allocation metrics also showed significant improvement, with return on capital employed (ROCE) rising to 12% from 7.2% and return on equity (ROE) increasing to 12.7% from 10.7%. Capital expenditure as a percentage of revenue decreased to 5.0% from 13.8% in the comparable period.

Free cash flow generation was particularly strong, increasing 22.3% year-over-year to QR 282 million, while net debt decreased to QR 510 million from QR 579 million. The company’s net debt to EBITDA ratio improved to 0.37x from 0.44x, indicating a strengthened balance sheet position.

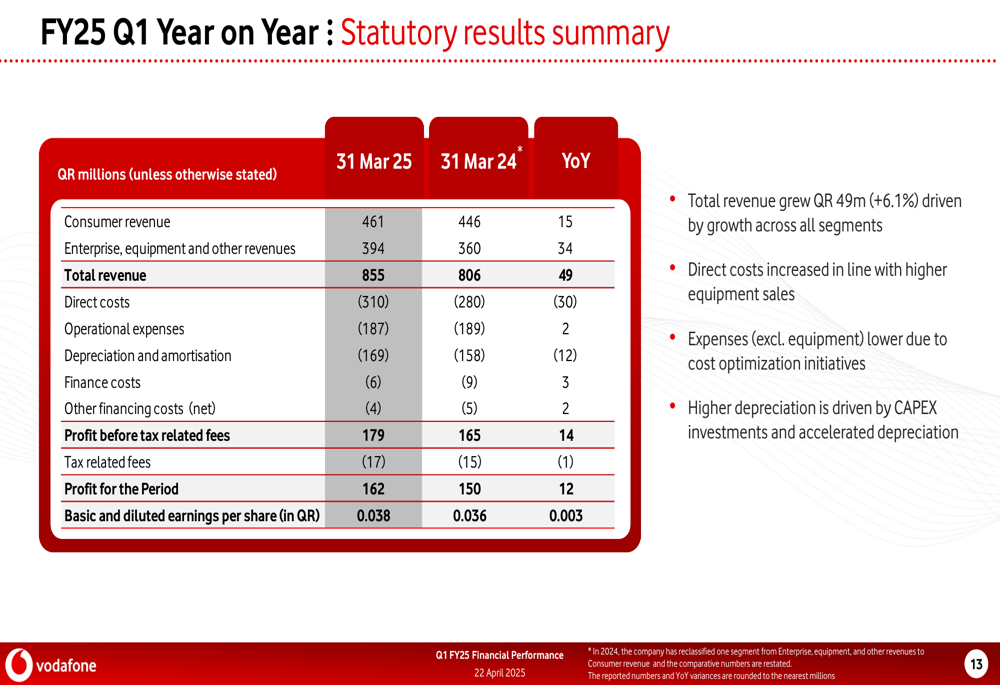

The comprehensive statutory results summary provides additional context for the company’s performance:

Looking at longer-term trends, Vodafone Qatar has maintained consistent growth over the past five years, with compound annual growth rates (CAGR) of 7.8% for service revenue, 9.9% for total revenue, 11.2% for EBITDA, and an impressive 25.2% for net profit since FY21 Q1.

Strategic Initiatives

A key strategic initiative highlighted in the presentation was the launch of Vodafone’s new loyalty program, "iPoints." The program is designed to enhance customer experience by rewarding spending and offering tiered benefits.

The loyalty program allows customers to convert points into Avios (airline miles) and receive discounts with partners like Snoonu, reflecting Vodafone Qatar’s focus on building customer loyalty and enhancing service offerings beyond traditional telecommunications.

CFO Masroor Anjum noted that the company’s diversification strategy is on track, with growing fintech services and further penetration in enterprise solutions representing critical focus areas for future growth.

Forward-Looking Statements

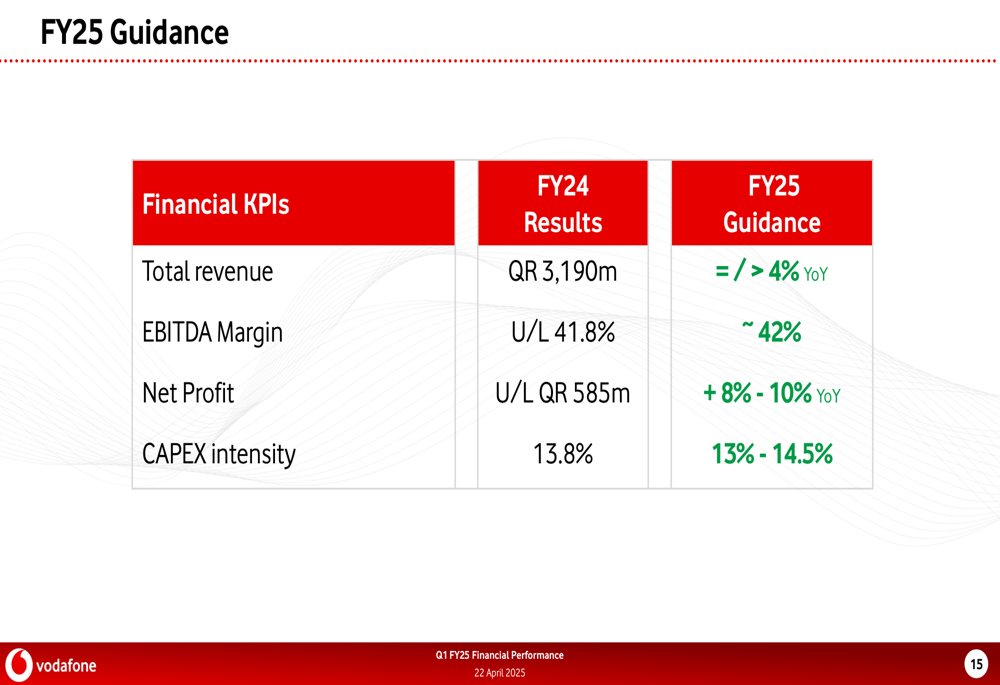

Vodafone Qatar provided guidance for FY25, projecting total revenue growth of at least 4% year-over-year, an EBITDA margin of approximately 42%, and net profit growth of 8-10%. Capital expenditure intensity is expected to be between 13% and 14.5%.

The detailed guidance metrics are presented in the following slide:

The company’s subscriber base remains strong, with 2,123 mobility subscribers as of Q1 FY25, comprising 569 postpaid and 1,554 prepaid customers. Average revenue per user (ARPU) metrics show QR 194.3 for postpaid customers and QR 29.5 for prepaid customers, resulting in a total mobility ARPU of QR 73.4.

With continued focus on diversification, enterprise solutions, and enhanced customer experience, Vodafone Qatar appears well-positioned to maintain its growth trajectory through FY25, building on its strong start to the fiscal year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.