Stock market today: Stocks fall as investors rotate out of tech into Jackson Hole

Introduction & Market Context

Westinghouse Air Brake Technologies Corp (NYSE:WAB), commonly known as Wabtec, presented its Q2 2025 financial results on July 24, 2025, highlighting solid performance driven by strong Transit segment growth and continued margin expansion. The company operates in a market environment where North American freight traffic is expected to increase by 2.5% in Q2 2025, with varying conditions across international markets.

The rail technology provider’s stock closed at $214.38 on July 23, 2025, up 1.18% for the day, and has shown strong performance year-to-date with the price near its 52-week high of $216.10. This represents a significant gain from its 52-week low of $147.66, reflecting investor confidence in the company’s strategic direction.

Quarterly Performance Highlights

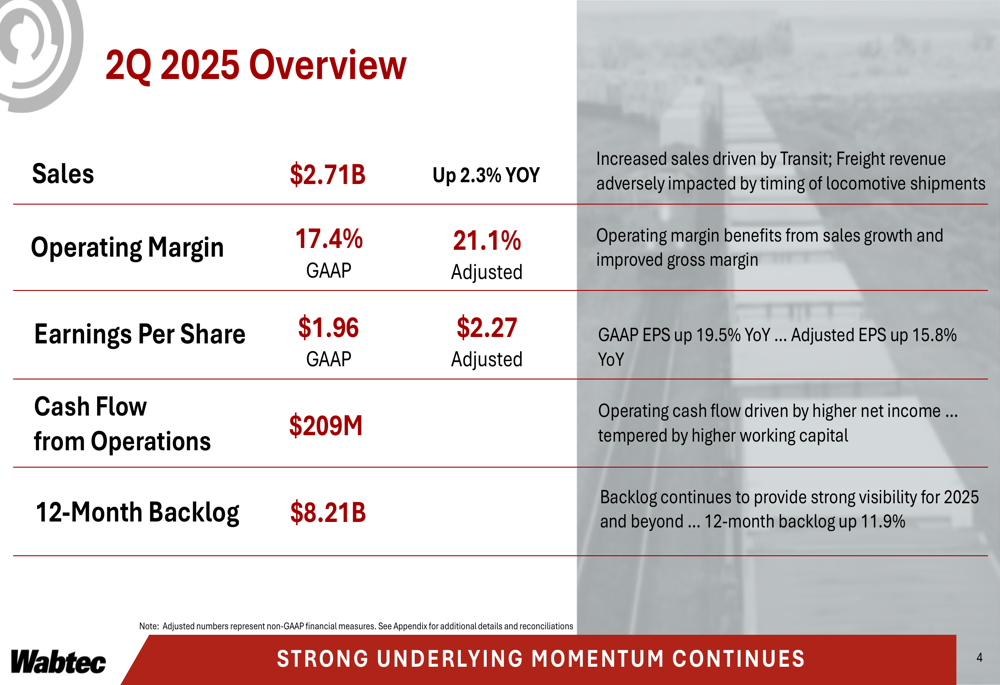

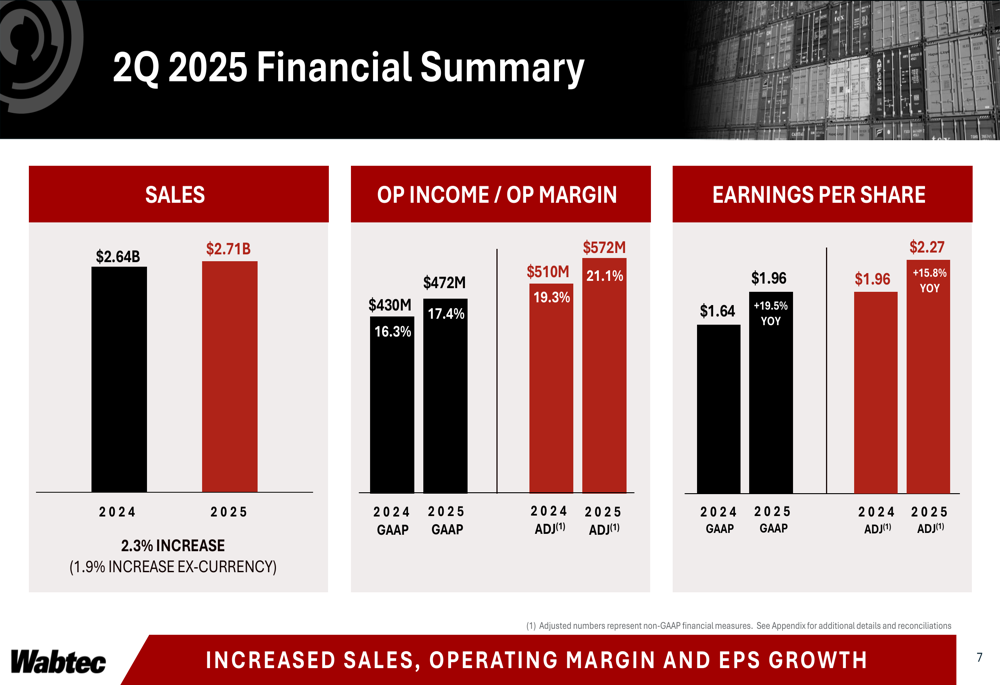

Wabtec reported Q2 2025 sales of $2.71 billion, a 2.3% increase year-over-year (1.9% excluding currency effects). The company achieved significant margin improvement, with GAAP operating margin rising to 17.4% and adjusted operating margin reaching 21.1%.

As shown in the following comprehensive financial overview:

Earnings per share showed strong growth, with GAAP EPS increasing 19.5% to $1.96 and adjusted EPS reaching $2.27. The company’s 12-month backlog grew to $8.21 billion, up 11.9% compared to the previous year, providing solid visibility for future revenue.

The financial summary below illustrates the year-over-year improvements across key metrics:

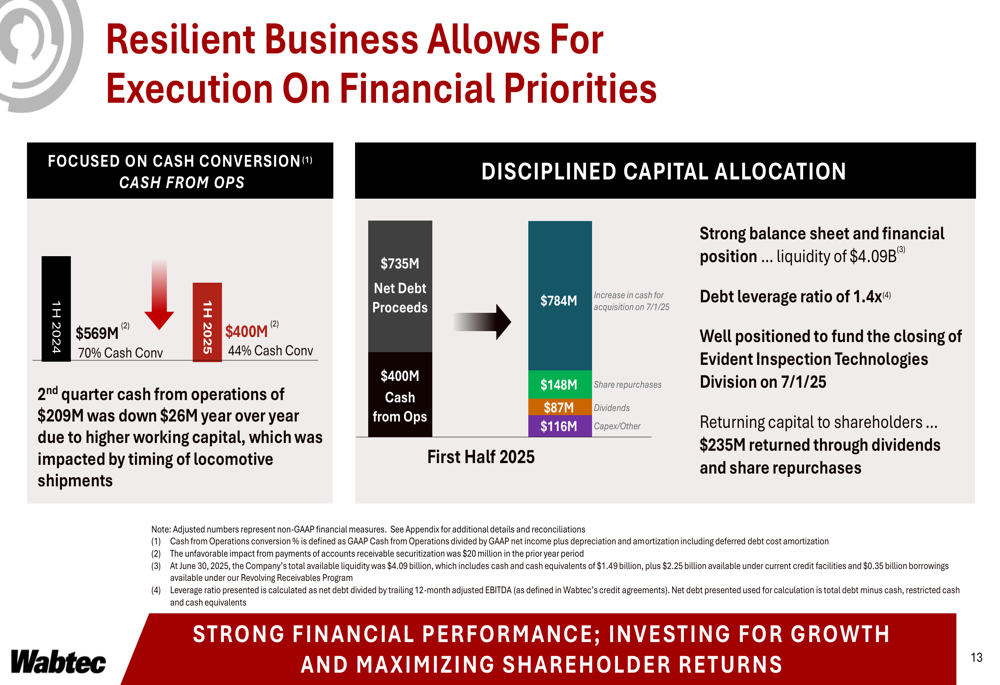

Cash flow from operations was $209 million for the quarter, though this represented a decrease from the previous year due to higher working capital, which was impacted by the timing of locomotive shipments. Despite this temporary challenge, the company maintained its strong balance sheet with $4.09 billion in liquidity and a debt leverage ratio of 1.4x.

Segment Analysis

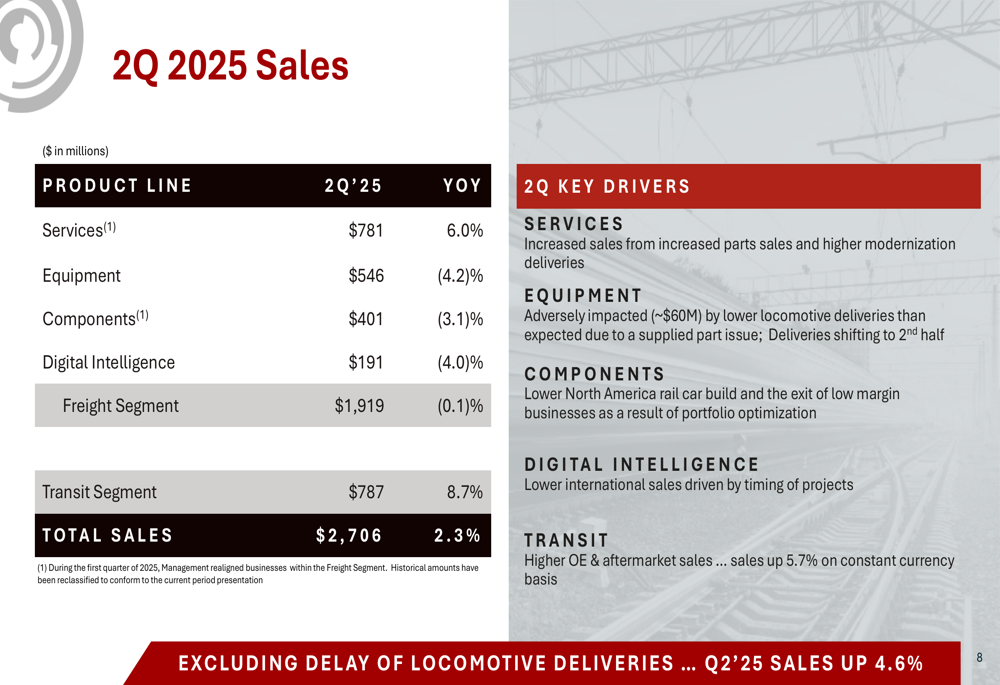

Wabtec’s performance showed a clear divergence between its two main segments. The Transit segment delivered exceptional results with 8.7% sales growth, reaching $787 million, while the Freight segment remained essentially flat at $1.919 billion, a slight decrease of 0.1% year-over-year.

The sales breakdown by product line reveals that Services led growth with a 6.0% increase, while Equipment sales declined by 4.2%, impacted by approximately $60 million in delayed locomotive deliveries:

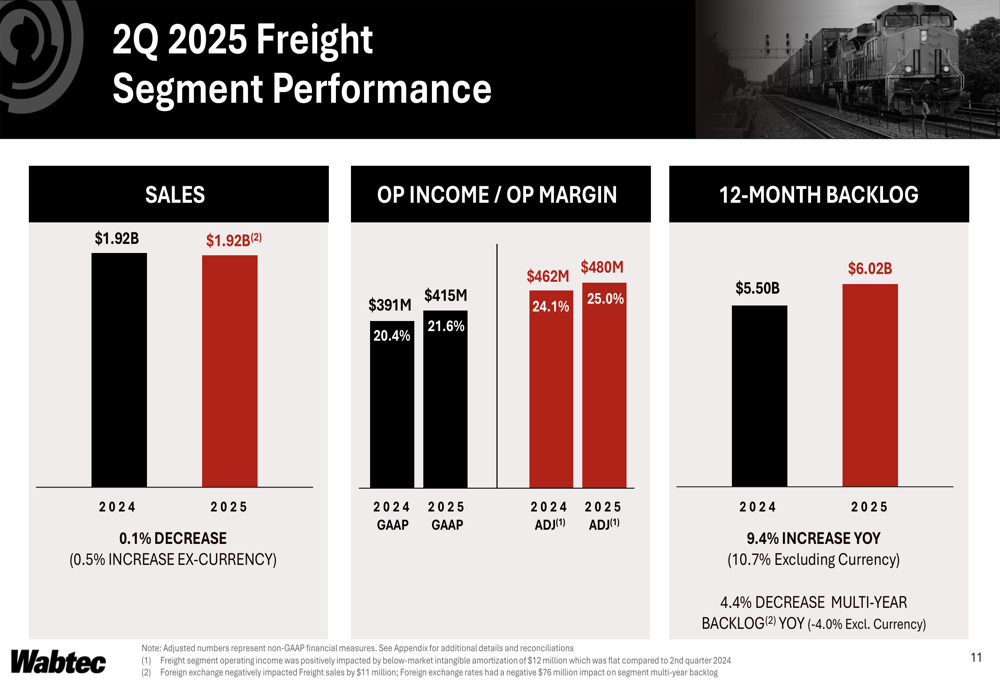

In the Freight segment, despite flat sales, profitability improved with GAAP operating margin increasing to 21.6% and adjusted operating margin reaching 25.0%. The segment’s 12-month backlog grew by 9.4% to $6.02 billion, indicating healthy future demand.

The following chart details the Freight segment’s performance metrics:

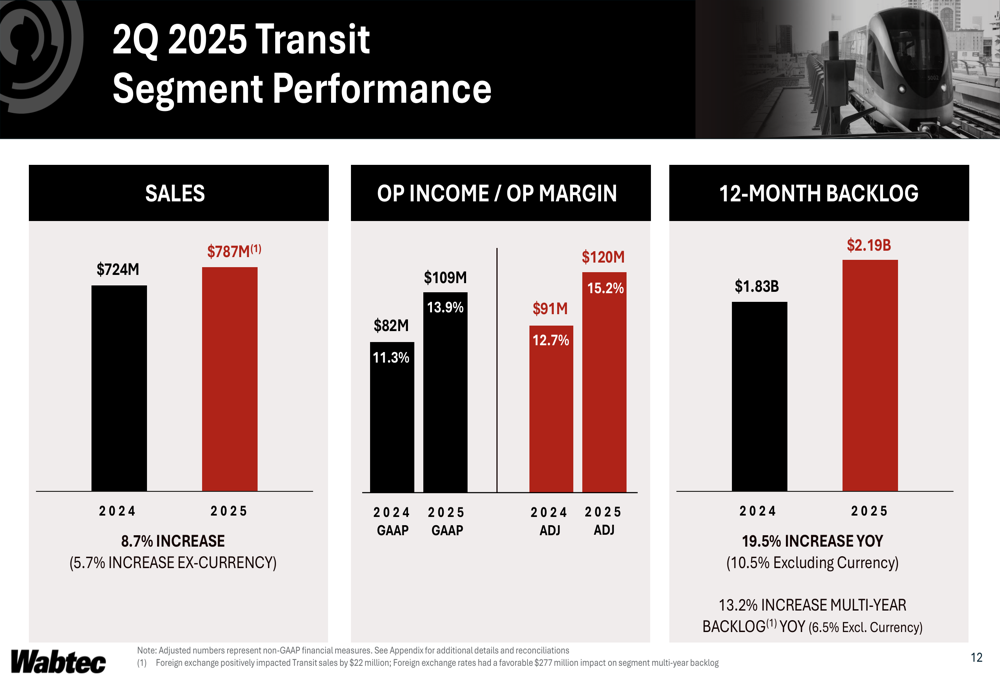

The Transit segment showed even more impressive margin expansion, with GAAP operating margin increasing to 13.9% and adjusted operating margin reaching 15.2%. The segment’s backlog grew by 19.5% to $2.19 billion, reflecting strong order activity.

As illustrated in the Transit segment performance summary:

Strategic Initiatives & Acquisitions

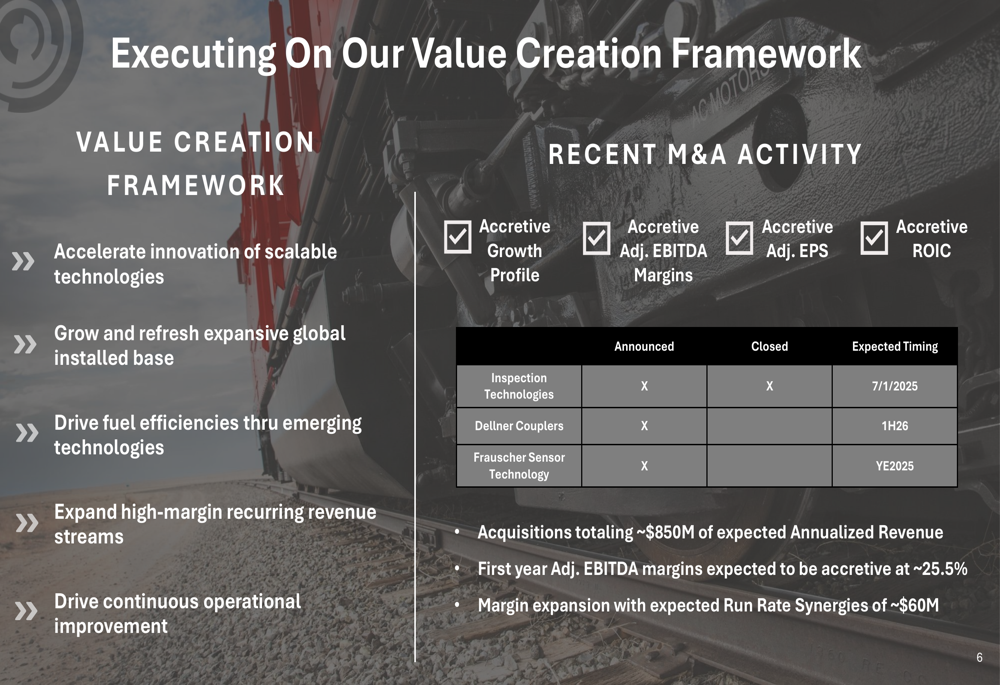

Wabtec is actively executing on its value creation framework, with a particular focus on strategic acquisitions. The company highlighted three recent acquisitions: Inspection Technologies (expected closing July 1, 2025), Dellner Couplers (first half of 2026), and Frauscher Sensor Technology (year-end 2025).

These acquisitions represent approximately $850 million in expected annualized revenue with first-year adjusted EBITDA margins expected to be accretive at approximately 25.5%. The company anticipates run-rate synergies of approximately $60 million.

The following slide outlines the company’s value creation framework and recent M&A activity:

Wabtec’s financial priorities remain focused on cash conversion and disciplined capital allocation. During the quarter, the company returned $235 million to shareholders while maintaining investment capacity for strategic growth initiatives.

The chart below illustrates the company’s approach to cash deployment:

Forward Guidance & Outlook

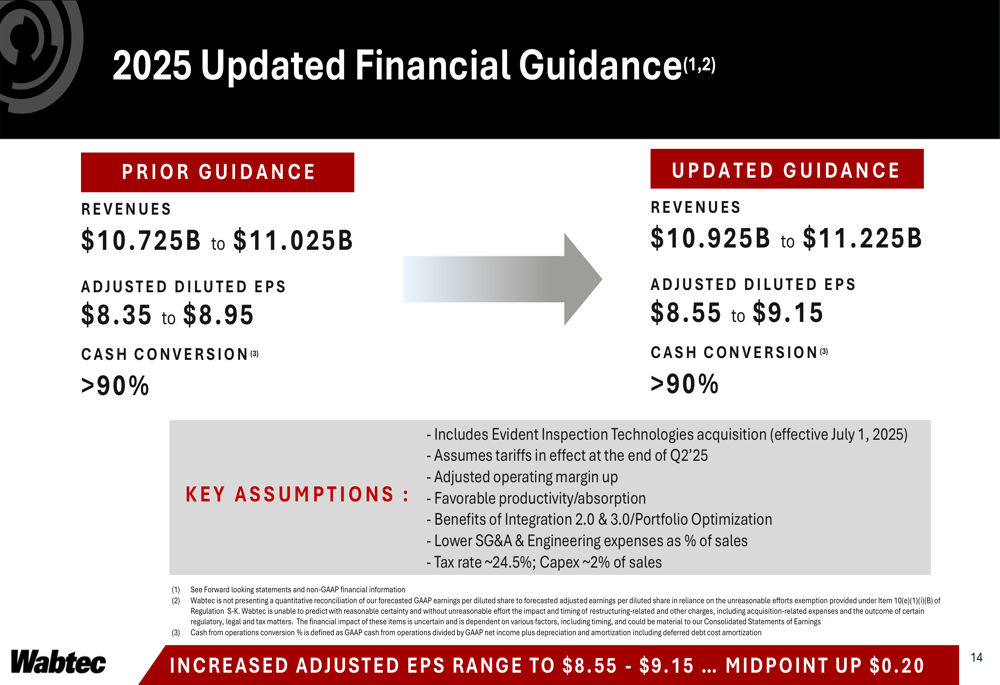

Based on strong first-half performance and confidence in future growth, Wabtec raised its full-year 2025 guidance. Revenue expectations increased from $10.725-$11.025 billion to $10.925-$11.225 billion, while adjusted diluted EPS guidance was raised from $8.35-$8.95 to $8.55-$9.15.

The updated guidance includes the impact of the Evident Inspection Technologies acquisition and assumes tariffs in effect as of the end of Q2 2025:

Looking beyond 2025, the company maintains an optimistic five-year outlook, projecting mid-single-digit organic sales CAGR, 350+ basis points of adjusted operating margin expansion, double-digit adjusted EPS CAGR, and greater than 90% cash from operations conversion.

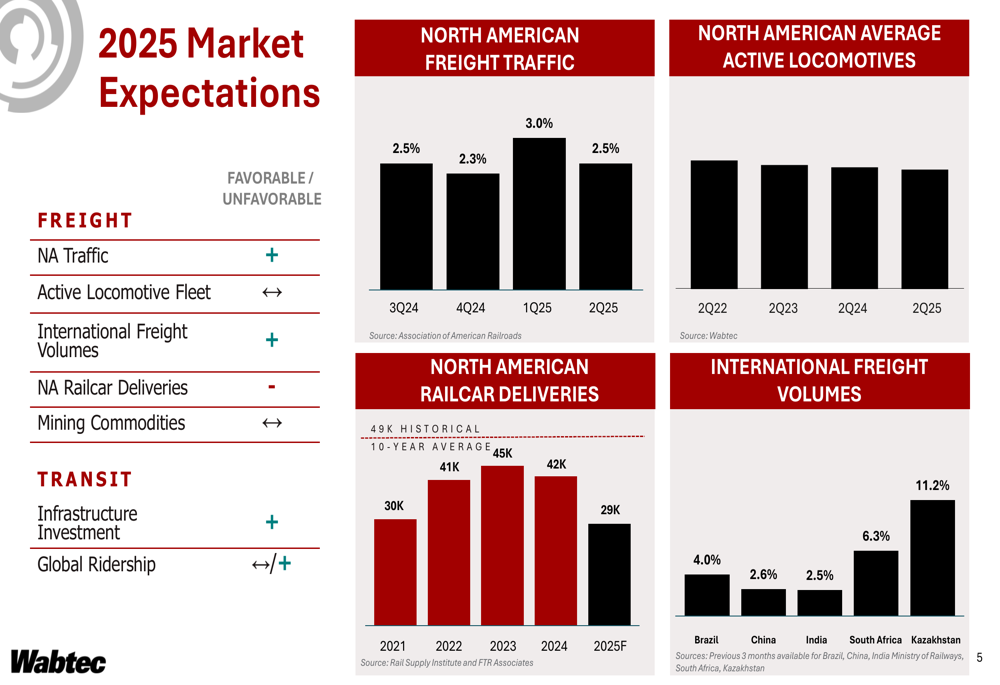

The company’s market expectations for 2025 show favorable outlooks for North American traffic and active locomotive fleet, with mixed expectations for international freight volumes and mining commodities:

Wabtec’s strong Q2 2025 performance, particularly in the Transit segment, combined with strategic acquisitions and raised guidance, positions the company well for continued growth despite some near-term challenges in the Freight segment. The substantial backlog growth across both segments provides visibility and stability for future revenue, while margin expansion demonstrates the effectiveness of the company’s operational improvement initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.