Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

Walker & Dunlop (NYSE:WD) released its Q1 2025 earnings presentation on May 1, 2025, revealing a mixed financial performance characterized by modest revenue growth but declining profitability metrics. The commercial real estate finance company’s stock traded down 2.01% in pre-market trading at $75, continuing a downward trend that began after its Q4 2024 earnings release.

The presentation highlighted strong underlying market fundamentals in the multifamily sector, with significant capital targeting commercial real estate investments and improving investor sentiment. These positive market indicators stand in contrast to the company’s own profitability challenges during the quarter.

Quarterly Performance Highlights

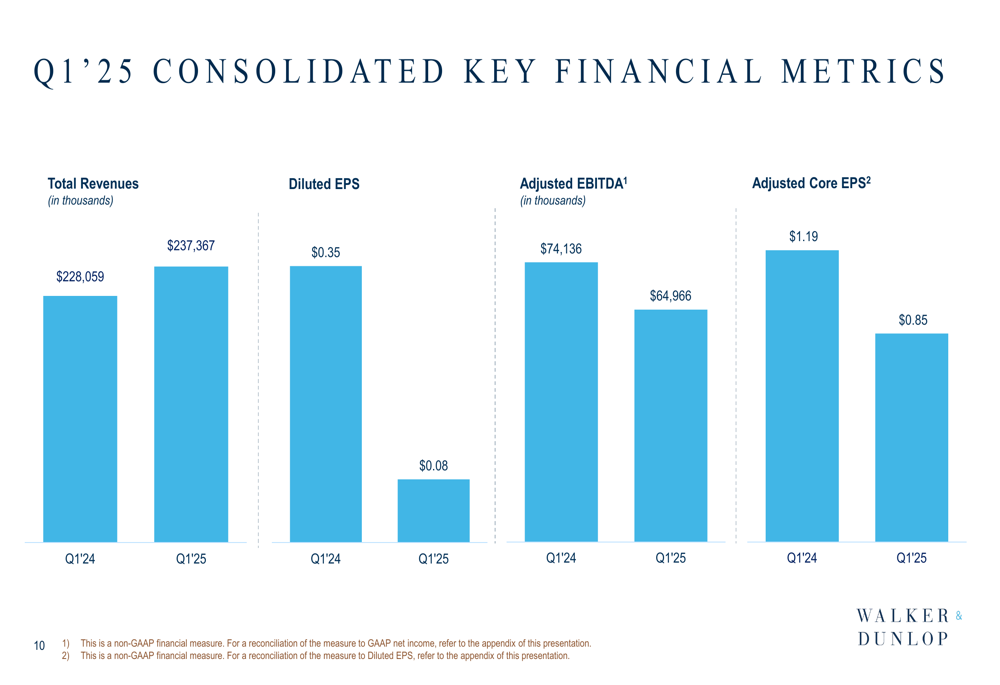

Walker & Dunlop reported total revenues of $237.4 million for Q1 2025, a modest 4% increase from $228.1 million in Q1 2024. However, profitability metrics showed significant declines across the board. Diluted EPS fell 77% to $0.08 from $0.35 in the prior-year period, while adjusted EBITDA decreased 12% to $65.0 million from $74.1 million. Adjusted core EPS, a key metric for the company, dropped 29% to $0.85 from $1.19 year-over-year.

As shown in the following consolidated financial metrics chart:

This performance represents a notable shift from the company’s Q4 2024 results, which had exceeded analyst expectations with an EPS of $1.34 and record adjusted EBITDA of $329 million. The sequential decline suggests Walker & Dunlop is facing new challenges in maintaining profitability despite growing transaction volumes.

Multifamily Market Trends

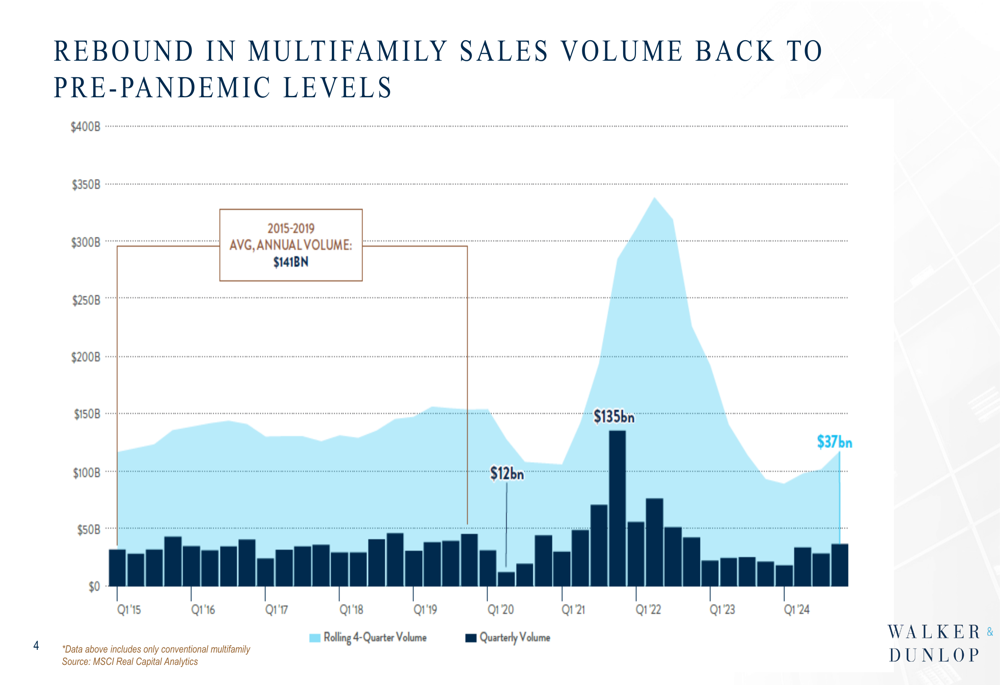

Despite the company’s profitability challenges, Walker & Dunlop’s presentation emphasized several positive trends in the multifamily market that could support future growth. The company highlighted that multifamily sales volume has rebounded to pre-pandemic levels, with the average annual volume from 2015-2019 at $141 billion serving as a benchmark.

The following chart illustrates this rebound in multifamily sales volume:

Investor sentiment toward multifamily properties has also improved significantly, with the percentage of investors looking to buy increasing from approximately 35% in Q1 2020 to nearly 70% in Q1 2025, according to data from the Zelman Quarterly Apartment Transaction (JO:NTUJ) Survey presented by the company.

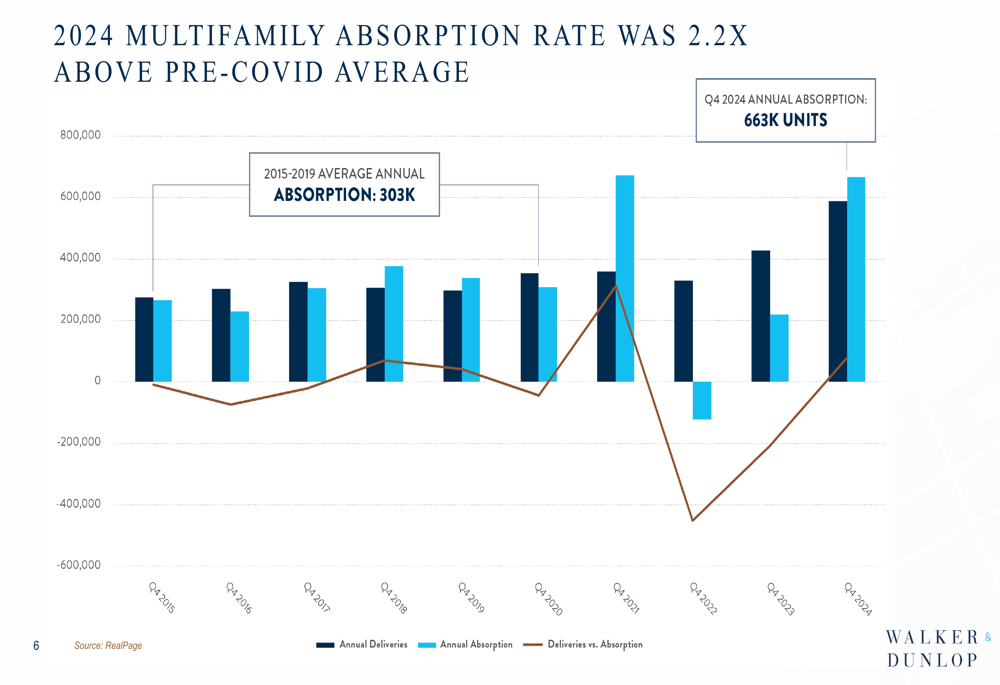

A particularly notable trend is the strong absorption rate in the multifamily sector. According to the presentation, Q4 2024 annual absorption was 2.2 times above the pre-COVID average, reaching 663,000 units compared to a historical average of 303,000 units.

This absorption data is illustrated in the following chart:

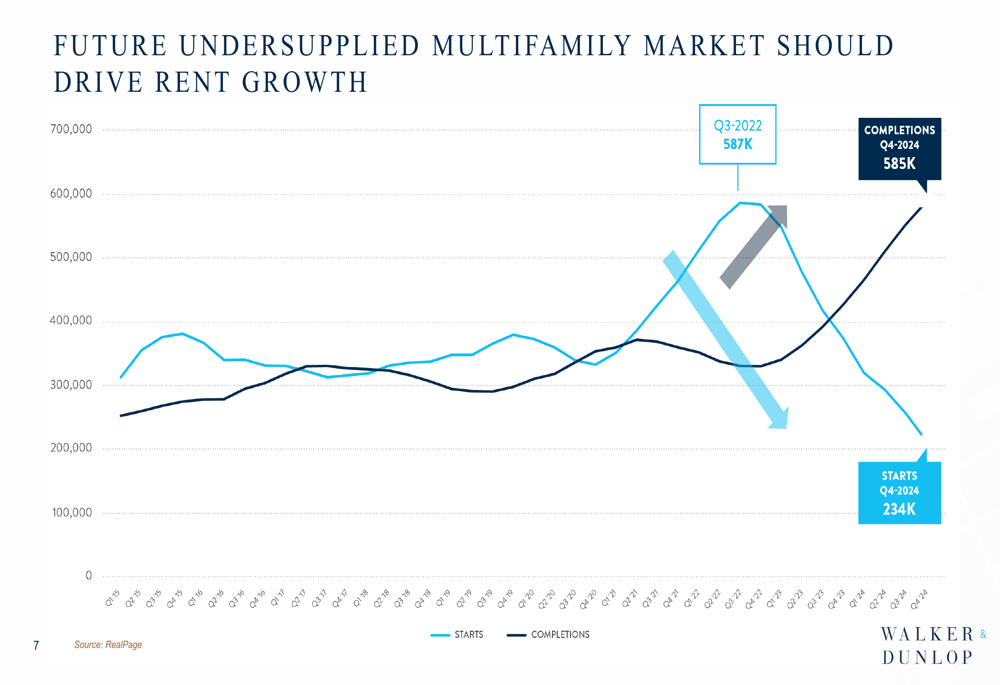

The presentation also highlighted a developing supply-demand imbalance that could benefit the multifamily sector. Multifamily starts have decreased dramatically to 234,000 in Q4 2024, while completions remain high at 585,000, suggesting a potential undersupply in the coming years that could drive rental growth.

As shown in the following starts and completions chart:

Another factor supporting multifamily demand is the widening gap between home ownership costs and renting costs. The presentation showed that median single-family list prices have increased significantly more than effective rents since 2019, making renting relatively more affordable and potentially driving demand for multifamily units.

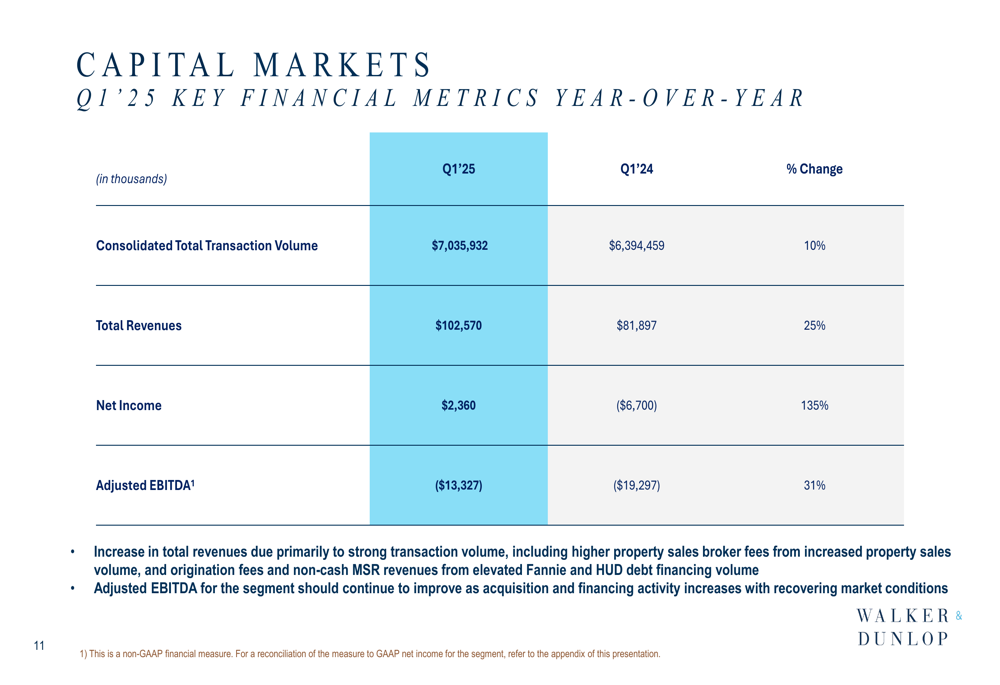

Capital Markets Segment Performance

While the company’s overall profitability declined, Walker & Dunlop’s Capital Markets segment showed significant improvement. The segment’s total transaction volume grew 10% year-over-year to $7.04 billion, while revenues increased 25% to $102.6 million. Most notably, the segment’s net income swung from a loss of $6.7 million in Q1 2024 to a profit of $2.4 million in Q1 2025, representing a 135% improvement.

The Capital Markets segment’s adjusted EBITDA, while still negative, improved by 31% from -$19.3 million to -$13.3 million year-over-year.

The following chart details the Capital Markets segment’s financial performance:

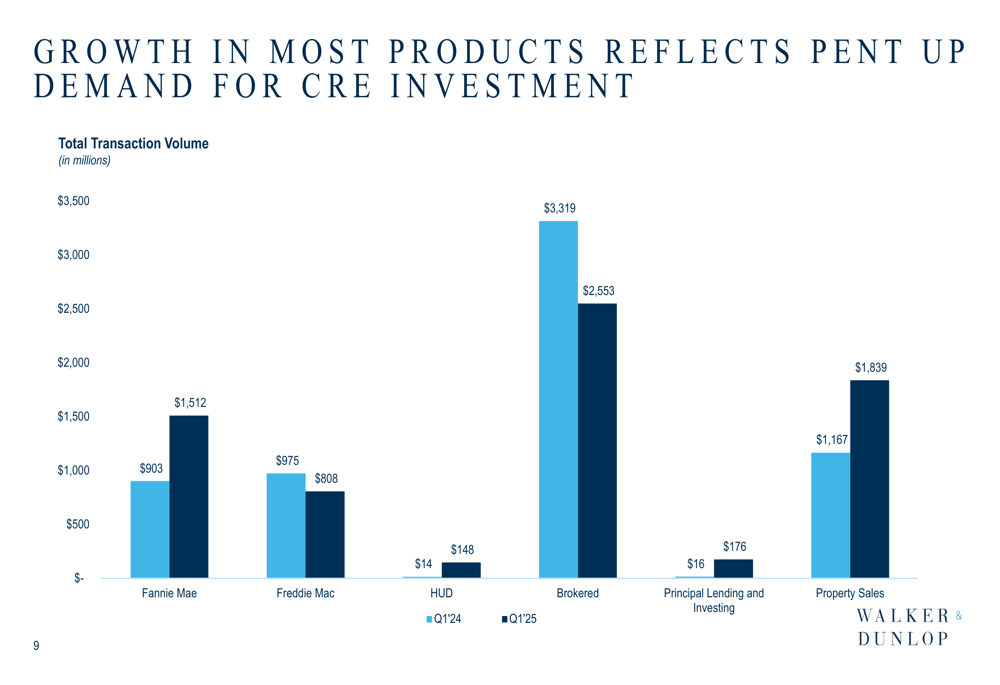

The transaction volume breakdown by product type reveals growth in most categories, reflecting what the company describes as "pent-up demand for CRE investment." Particularly strong growth was seen in Fannie Mae (OTC:FNMA) transactions (up 67% to $1.51 billion), HUD transactions (up 957% to $148 million), Principal Lending and Investing (up 1000% to $176 million), and Property Sales (up 58% to $1.84 billion). Only Freddie Mac (OTC:FMCC) and Brokered transactions showed declines.

As illustrated in the following transaction volume chart:

Forward-Looking Statements

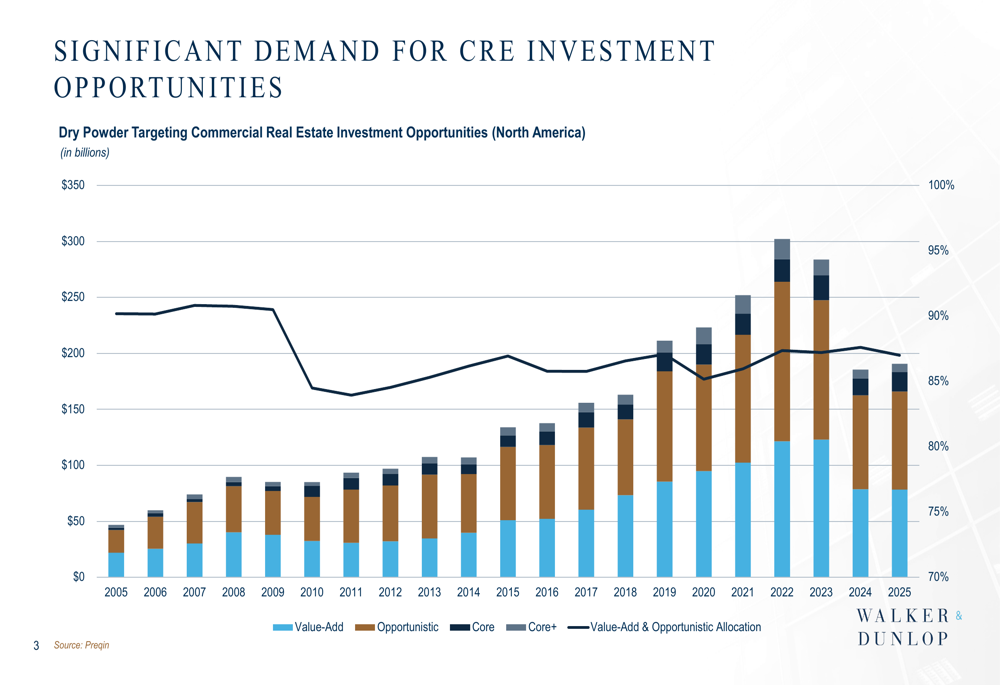

Walker & Dunlop’s presentation emphasized the significant amount of capital targeting commercial real estate investment opportunities. According to the company, dry powder targeting North American commercial real estate has grown from approximately $50 billion in 2005 to about $250 billion in 2025, though this represents a decline from the peak of nearly $300 billion in 2022.

The following chart illustrates this trend in available capital:

The company’s servicing portfolio has also shown consistent growth over the past five years, providing a stable revenue stream that could help offset volatility in transaction-based business lines.

While Walker & Dunlop did not provide specific forward guidance in the presentation materials, the company’s emphasis on strong market fundamentals suggests confidence in a potential recovery despite the current profitability challenges. However, investors appear to remain cautious, as evidenced by the continued decline in the company’s stock price, which is now trading near its 52-week low of $69.59.

The disconnect between improving market fundamentals and declining company profitability will likely be a key focus for analysts and investors in the coming quarters as they assess whether Walker & Dunlop can capitalize on the apparent opportunities in the multifamily market to reverse its profitability decline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.