Index falls as earnings results weigh; pound above $1.33, Bodycote soars

Introduction & Market Context

Walmart Inc (NYSE:WMT) released its first quarter fiscal year 2026 financial results on May 15, 2025, showing steady growth despite currency headwinds. The retail giant reported total revenues of $165.6 billion, representing a 2.5% year-over-year increase, or 4.0% growth in constant currency terms. The company’s stock showed positive momentum in premarket trading, up 2.81% to $99.55.

The results come amid continued consumer focus on value and convenience, with Walmart maintaining its full-year guidance despite macroeconomic uncertainties. The company’s eCommerce business continued to be a standout performer, with global digital sales growing 22% compared to the same period last year.

Quarterly Performance Highlights

Walmart’s total revenues reached $165.6 billion, including a negative impact of $2.4 billion from currency fluctuations. On a constant currency basis, revenues grew 4.0% year-over-year, with strength across all segments. Global eCommerce net sales grew by 22%, while membership and other income increased by 3.7%, driven by 14.8% global growth in membership fee income.

As shown in the following chart of quarterly revenue growth:

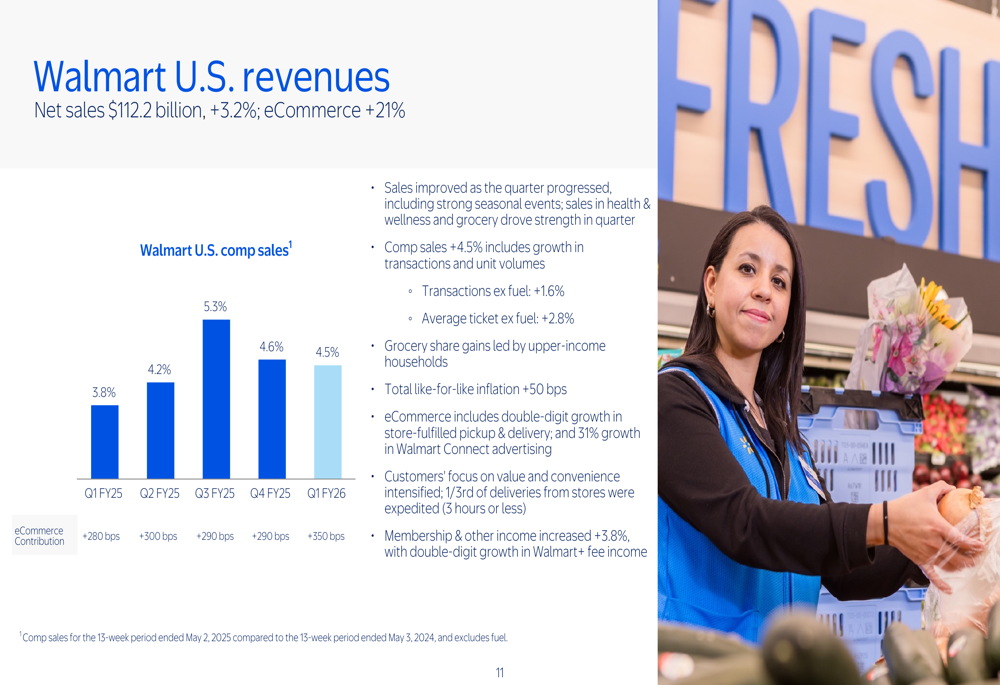

Walmart U.S., the company’s largest segment, delivered comp sales growth of 4.5%, including a 3.5% contribution from eCommerce. The segment saw net sales of $112.2 billion, up 3.2% year-over-year, with eCommerce sales growing 21%. Grocery share gains were led by upper-income households, and the company noted that one-third of deliveries from stores were expedited (3 hours or less).

The following chart illustrates Walmart U.S. comp sales performance:

Walmart International showed strong constant currency growth of 7.8%, reaching $32.1 billion in net sales. This growth was led by China, Flipkart, and Walmex, though currency rate fluctuations negatively affected reported sales by $2.4 billion. eCommerce sales grew 20% internationally, led by store-fulfilled pickup & delivery and marketplace offerings.

The international revenue trend is illustrated in this chart:

Sam’s Club U.S. reported net sales of $22.1 billion, up 2.9% year-over-year, or 5.5% excluding fuel. Comparable sales increased 5.3%, driven by increases in transactions and unit volumes. eCommerce delivery growth was approximately 160%, with digital sales now representing 17% of sales excluding fuel.

Detailed Financial Analysis

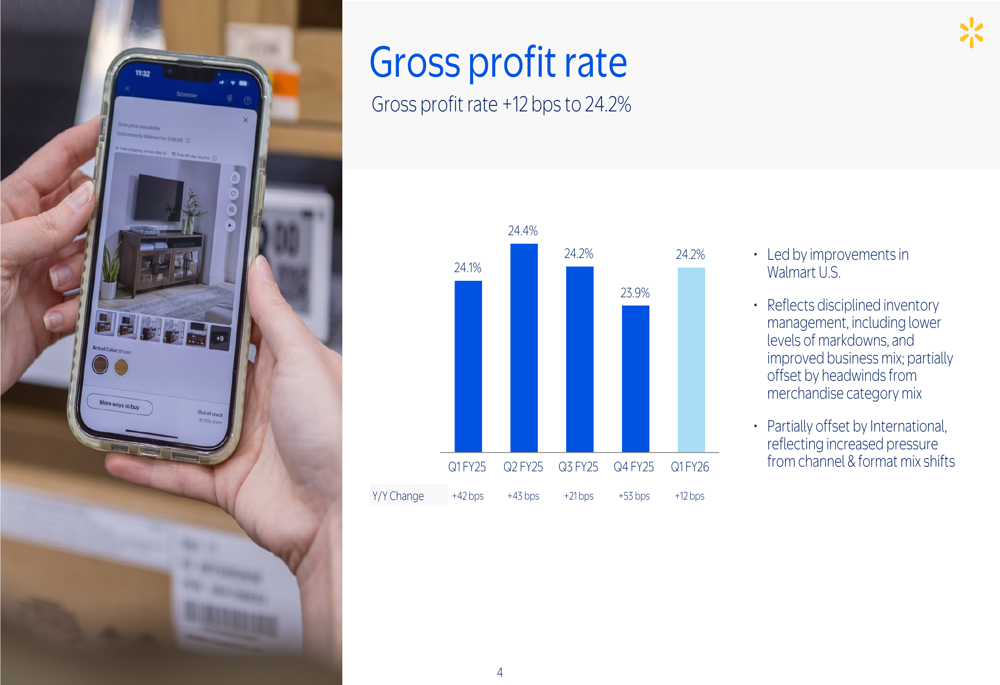

Walmart’s gross profit rate increased 12 basis points to 24.2%, led by improvements in Walmart U.S. This reflects disciplined inventory management, including lower levels of markdowns, and improved business mix, partially offset by headwinds from merchandise category mix.

The gross profit rate trend is shown in the following chart:

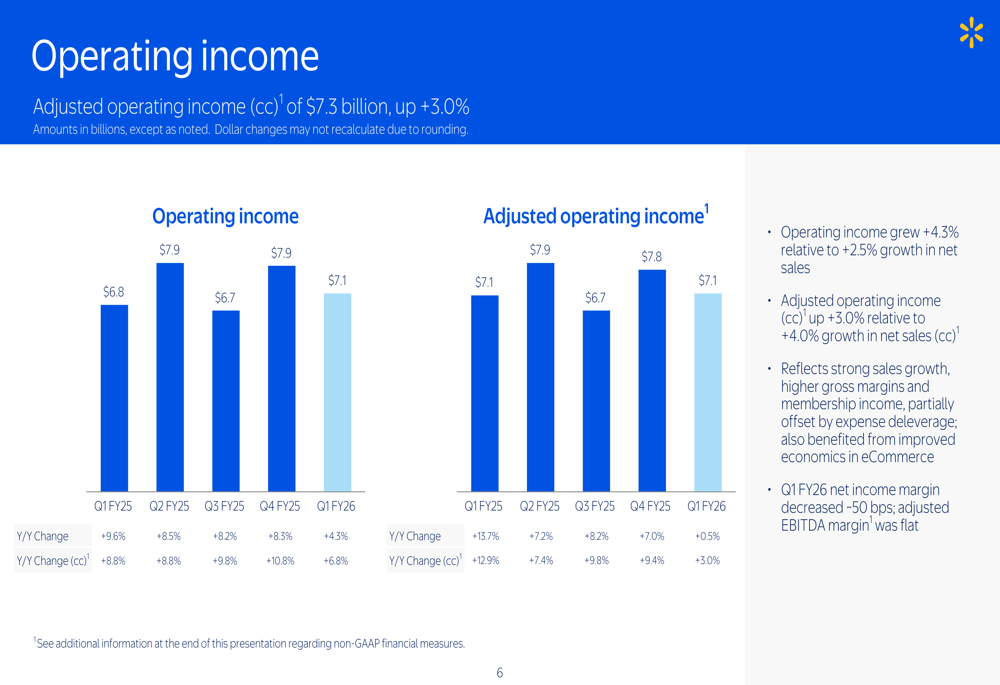

Adjusted operating income was $7.1 billion, up 0.5% year-over-year, or 3.0% in constant currency. Operating income grew 4.3% relative to 2.5% growth in net sales, reflecting strong sales growth, higher gross margins and membership income, partially offset by expense deleverage. The company also benefited from improved economics in eCommerce.

The operating income trend is illustrated in this chart:

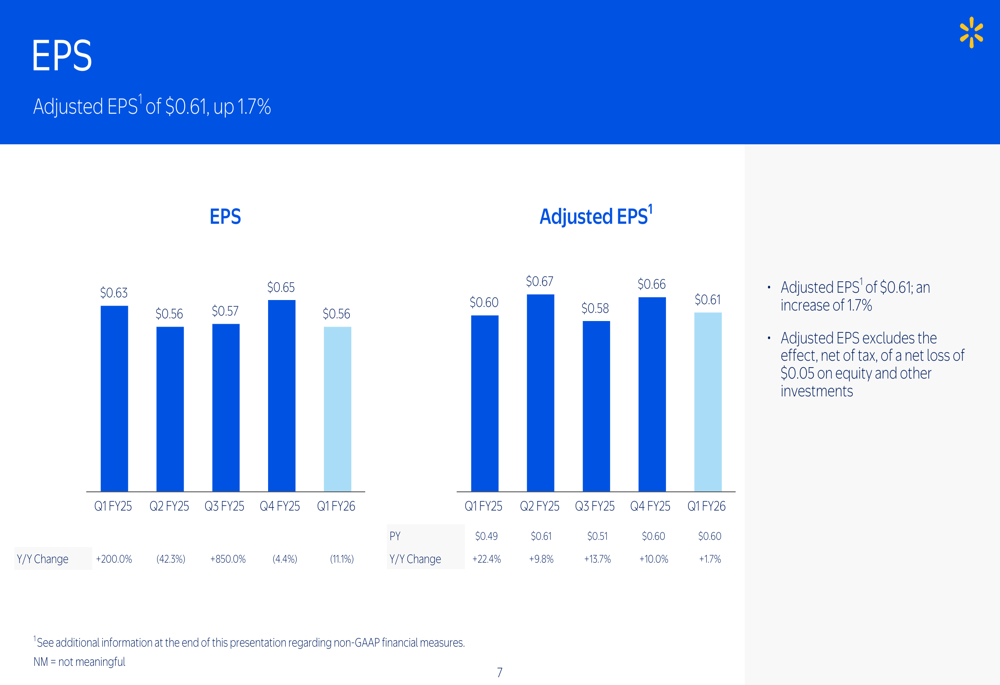

Adjusted earnings per share reached $0.61, an increase of 1.7% compared to the same period last year. This excludes the effect, net of tax, of a net loss of $0.05 on equity and other investments.

As shown in the following EPS chart:

Operating cash flow increased $1.2 billion to $5.4 billion, primarily due to an increase in cash provided by operating income and timing of certain payments. Free cash flow increased $0.9 billion, though it remained negative at $(0.4) billion due to increased capital expenditures supporting the company’s investment strategy.

The company significantly increased its share repurchases during the quarter, totaling $4.6 billion representing 50.4 million shares at an average price of $90.35 per share. This represents a substantial increase compared to previous quarters. Dividends remained stable at $1.1 billion, bringing total returns to shareholders to $6.4 billion for the quarter. The remaining share repurchase authorization stands at $7.5 billion.

Strategic Initiatives

Walmart continues to focus on eCommerce growth across all segments. In the U.S., eCommerce includes double-digit growth in store-fulfilled pickup & delivery, and 31% growth in Walmart Connect advertising. The company now offers store-fulfilled delivery in less than 3 hours to 93% of U.S. households.

In international markets, eCommerce growth of 20% was led by store-fulfilled pickup & delivery and marketplace offerings. China showed particularly strong performance with comparable sales growth of 16.8% and eCommerce net sales growth of 34%.

Membership income continues to be a growth driver, with global membership fee income increasing 14.8%. Sam’s Club U.S. reported membership income growth of 9.6%, with steady growth in member counts, renewal rates, and increased penetration of Plus members. Over 50% of total Sam’s Club members now transact digitally, either through the Scan & Go app or shopping online.

Forward-Looking Statements

Walmart maintained its guidance for Q2 FY26 and full-year FY26. For the second quarter, the company expects consolidated net sales to increase 3.5% to 4.5%, including approximately 20 basis points tailwind from the acquisition of VIZIO.

For fiscal year 2026, Walmart continues to expect:

- Net sales growth of 3.0% to 4.0% in constant currency

- Adjusted operating income growth of 3.5% to 5.5% in constant currency

- Adjusted EPS of $2.50 to $2.60, including approximately $0.05 headwind from currency

- Capital expenditures of approximately 3.0% to 3.5% of net sales

The company noted that its full-year guidance includes approximately 20 basis points headwind from lapping leap year and approximately 20 basis points tailwind from the acquisition of VIZIO. The adjusted operating income guidance includes approximately 70 basis points headwind from lapping leap year and approximately 80 basis points headwind from the acquisition of VIZIO.

As Walmart continues to navigate a dynamic retail environment, its focus on eCommerce, membership growth, and international expansion appears to be yielding positive results. The significant increase in share repurchases during the quarter may signal management’s confidence in the company’s future performance and financial health.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.