JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

Warrior Met Coal Inc (NYSE:HCC) released its first quarter 2025 results on April 30, revealing a challenging period marked by significantly lower coal prices despite increased production volumes. The metallurgical coal producer reported a net loss as average selling prices plunged 42% year-over-year, reflecting continued weakness in the global steelmaking coal market.

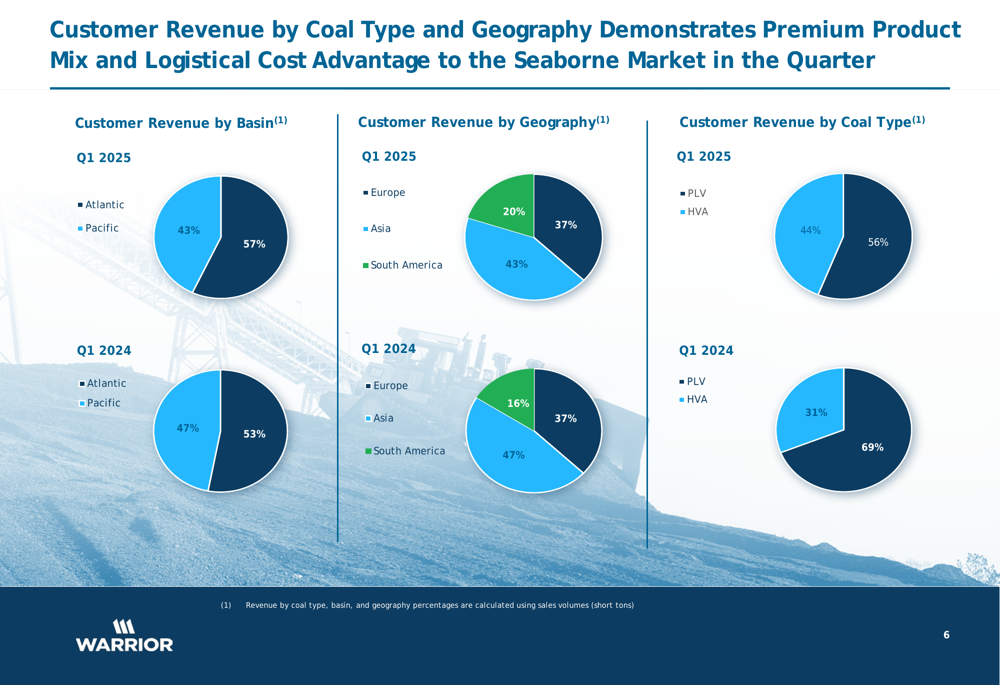

Despite these headwinds, Warrior continues to advance its strategic Blue Creek project, which remains on schedule and on budget. The company’s customer base remains diversified across the Atlantic and Pacific basins, with a slight shift toward Pacific markets in the most recent quarter.

Quarterly Performance Highlights

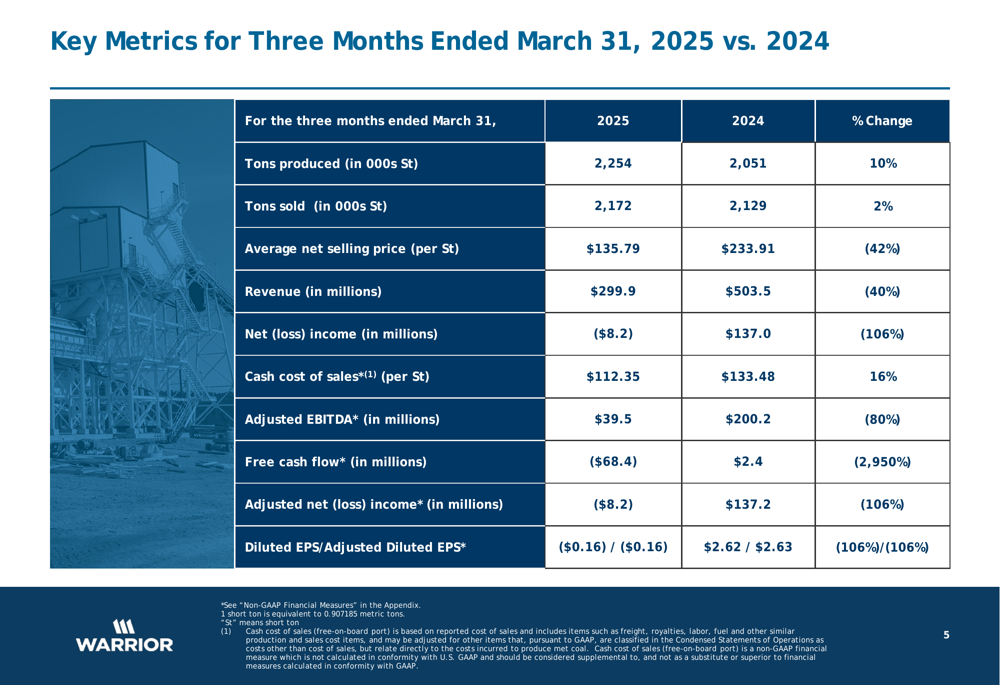

Warrior reported a 10% increase in production volumes to 2.25 million short tons in Q1 2025, compared to 2.05 million short tons in the same period last year. Sales volumes also increased by 2% to 2.17 million short tons. Notably, the company produced 251,000 short tons at its new Blue Creek operation.

As shown in the following comprehensive comparison of key metrics:

Despite the production increase, Warrior’s financial performance deteriorated significantly due to lower coal prices. The average net selling price fell 42% to $135.79 per ton from $233.91 in Q1 2024, resulting in a 40% decrease in revenue to $299.9 million. This price decline led to a net loss of $8.2 million, compared to net income of $137.0 million in the prior-year period.

The company’s customer revenue distribution shows a slight shift in geographical focus:

Detailed Financial Analysis

While revenue and earnings declined substantially, Warrior achieved a 16% reduction in cash cost of sales to $112.35 per ton, helping to partially offset the impact of lower prices. Adjusted EBITDA fell 80% to $39.5 million, with the EBITDA margin contracting to 13.2% from 39.8% a year earlier.

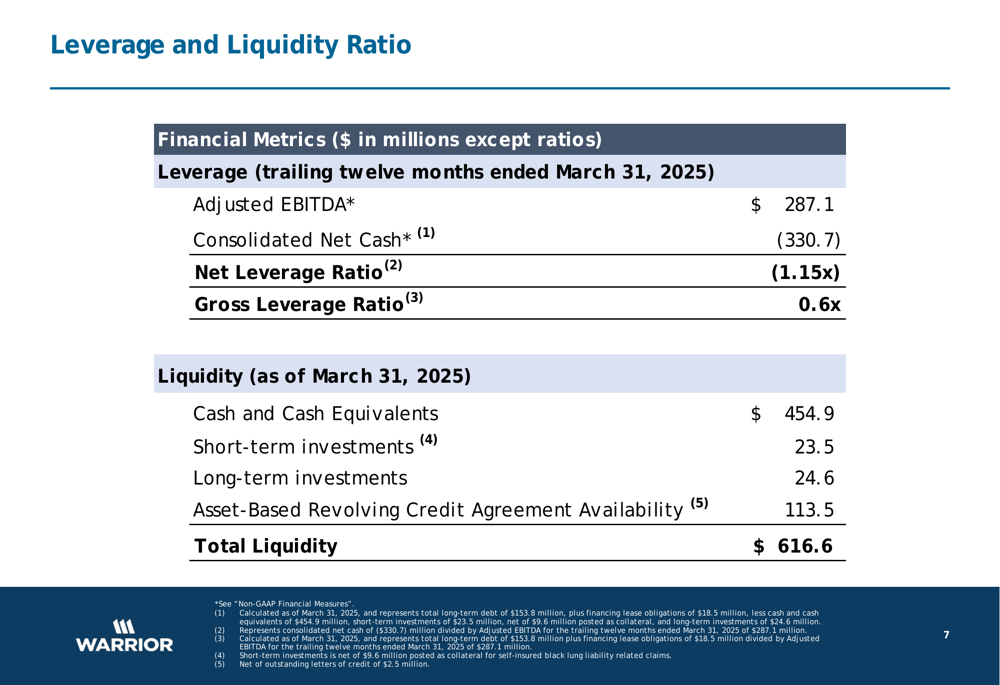

Free cash flow turned negative at -$68.4 million compared to positive $2.4 million in Q1 2024, primarily due to continued capital investments in the Blue Creek project. Despite these investments, Warrior maintains a strong financial position with total liquidity of $616.6 million as of March 31, 2025.

The company’s leverage and liquidity metrics demonstrate its financial stability:

Strategic Initiatives

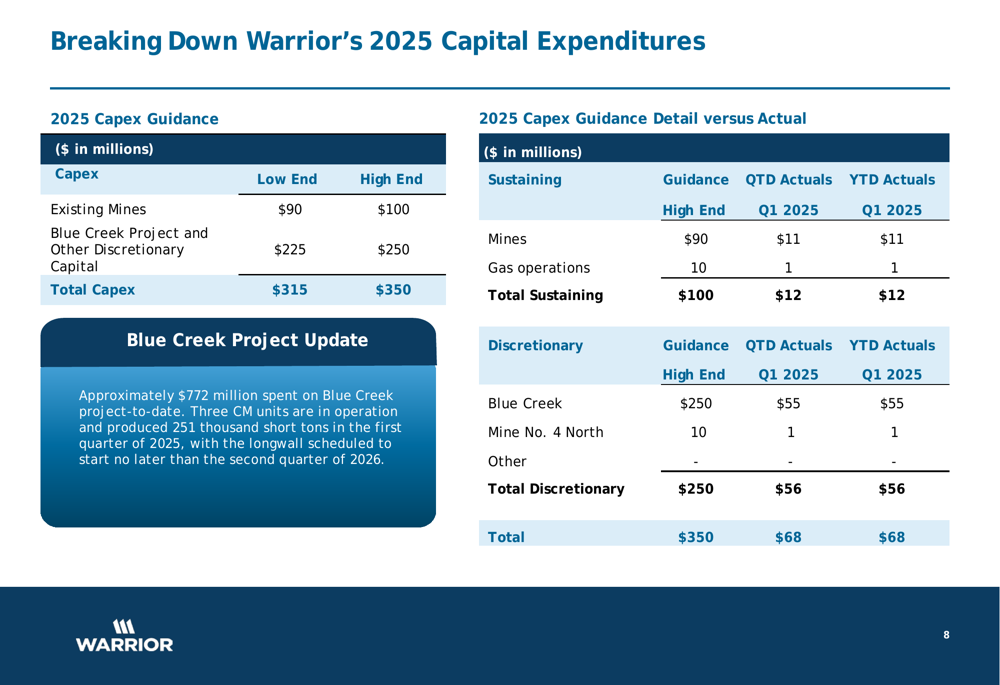

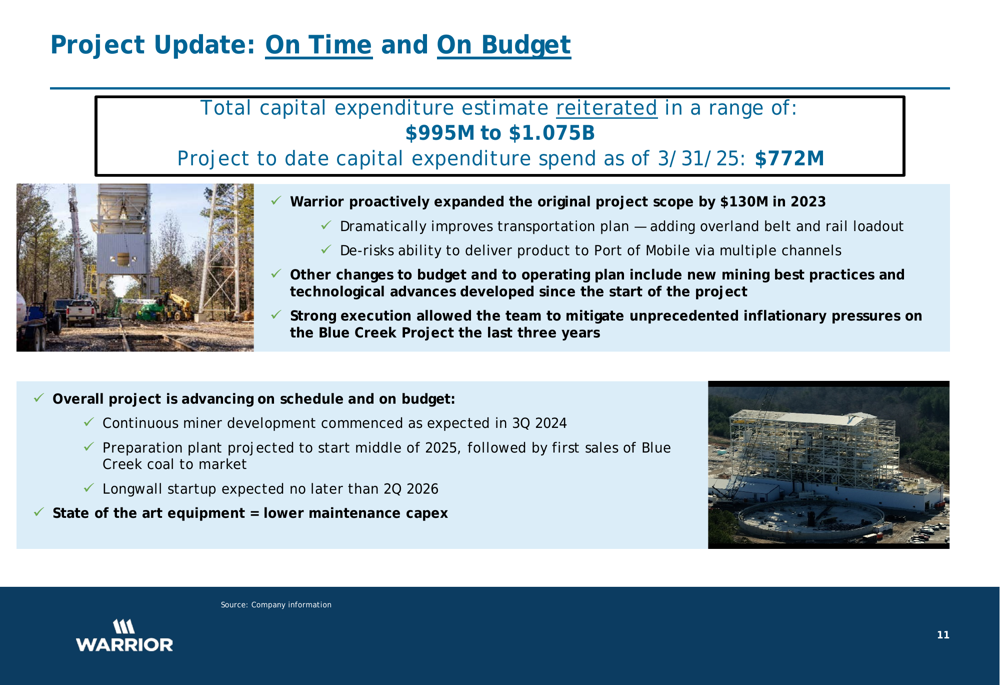

Warrior continues to make significant progress on its transformational Blue Creek project, which represents a major growth initiative for the company. The project remains on time and on budget, with total capital expenditures estimated between $995 million and $1.075 billion. As of March 31, 2025, Warrior had invested $772 million in the project.

The following slide details the company’s capital expenditure breakdown for 2025:

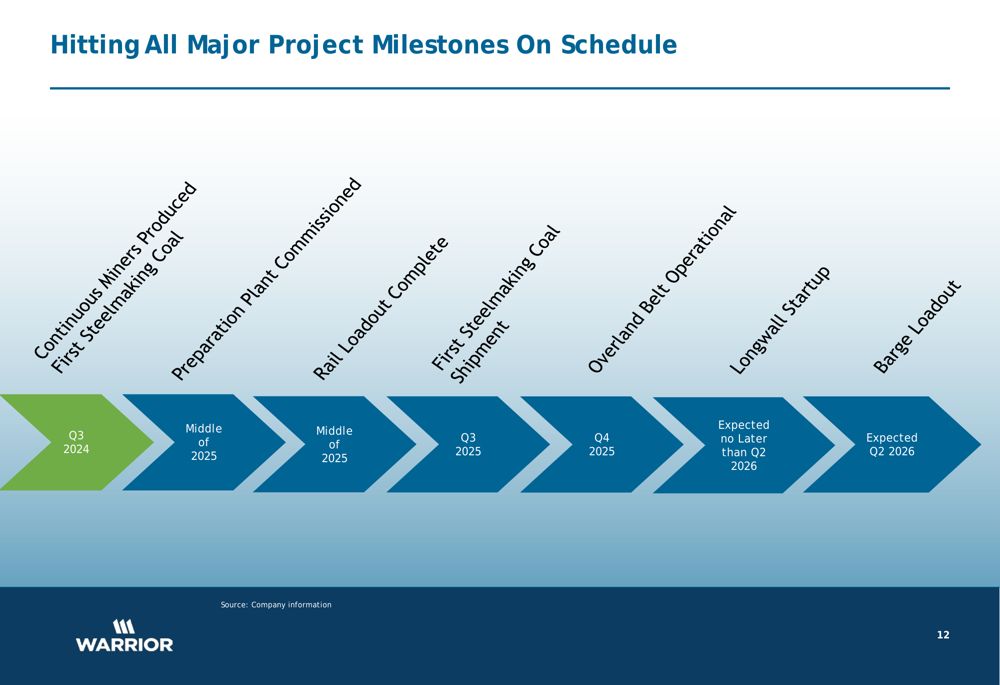

The Blue Creek project is advancing according to plan, with continuous miner development having commenced in Q3 2024 as expected. The preparation plant is projected to start in mid-2025, followed by the first sales of Blue Creek coal to market. Longwall startup is expected no later than Q2 2026.

As illustrated in this project update:

Warrior has proactively expanded the original project scope by $130 million in 2023 to improve transportation logistics and de-risk product delivery to the Port of Mobile via multiple channels. The company notes that strong execution has allowed it to mitigate unprecedented inflationary pressures on the project over the last three years.

The project timeline shows all major milestones are being hit on schedule:

Forward-Looking Statements

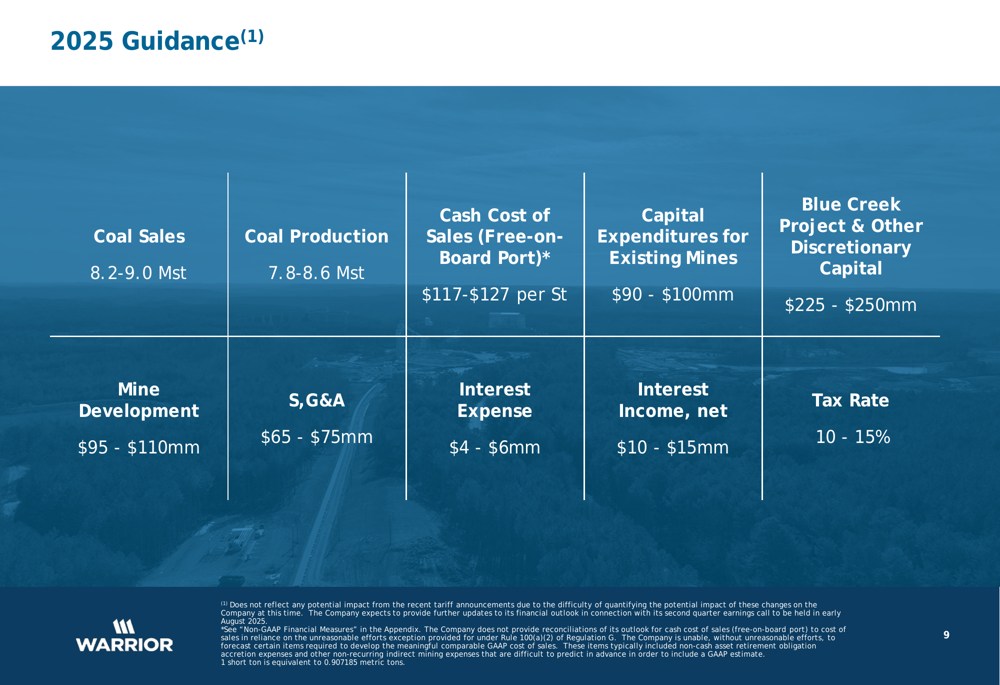

For 2025, Warrior provided guidance that reflects both operational growth and continued market challenges. The company expects coal sales of 8.2-9.0 million short tons and production of 7.8-8.6 million short tons. Cash cost of sales is projected to be $117-$127 per short ton.

Capital expenditures for 2025 are expected to range from $315-$350 million, with $225-$250 million allocated to the Blue Creek project and other discretionary capital.

The detailed 2025 guidance is presented below:

Warrior’s asset portfolio positions it for long-term growth despite current market challenges. The company’s three main operations include Mine 7 with a 20-year reserve life, the developing Blue Creek operation with a 40-year reserve life, and Mine 4 with a 35+ year reserve life. Together, these assets give Warrior one of the highest quality mixes of steelmaking coal products in the U.S. and a total annual nameplate capacity of 14.0 million short tons.

In the context of Warrior’s Q4 2024 performance, which also showed challenges with an EPS of $0.15 against a forecast of $0.81, the Q1 2025 results indicate continued market weakness. However, the company’s strategic investments, particularly in the Blue Creek project, demonstrate management’s confidence in the long-term fundamentals of the premium metallurgical coal market despite current pricing pressures.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.