5 big analyst AI moves: Nvidia guidance warning; Snowflake, Palo Alto upgraded

Introduction & Market Context

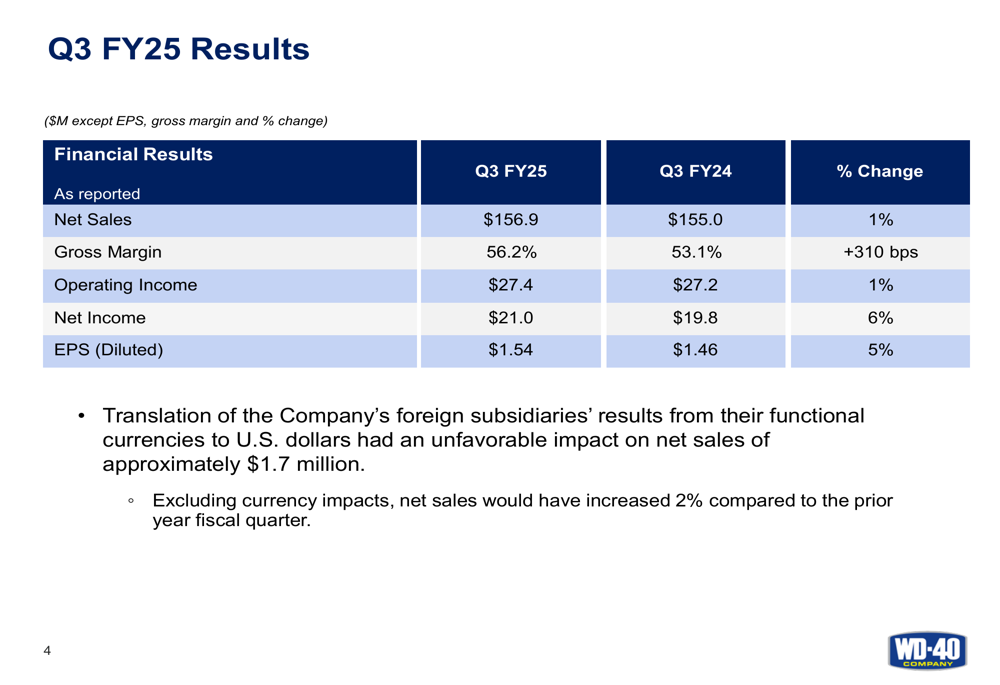

WD-40 Company (NASDAQ:WDFC) released its third-quarter fiscal year 2025 earnings results on July 10, 2025, reporting mixed performance with an earnings beat despite falling short on revenue expectations. The company’s stock saw minimal movement in after-hours trading, edging up just 0.02% to $229.78, following a 2.1% decline during the regular trading session.

The maintenance products manufacturer reported diluted earnings per share (EPS) of $1.54, exceeding analyst expectations of $1.42 and representing a 5% year-over-year increase. However, revenue of $156.9 million missed forecasts of $160.6 million, though it still represented a 1% increase compared to the same period last year.

Quarterly Performance Highlights

WD-40’s third-quarter results showed modest top-line growth with significant margin improvement. The company achieved net sales of $156.9 million, up 1% year-over-year, while gross margin expanded substantially to 56.2%, an increase of 310 basis points from 53.1% in the prior year period.

As shown in the following financial results summary:

Operating income increased by 1% to $27.4 million, while net income rose 6% to $21.0 million compared to Q3 FY24. The company noted that foreign currency translation had an unfavorable impact of approximately $1.7 million on net sales, meaning that excluding currency impacts, net sales would have increased by 2% compared to the prior year fiscal quarter.

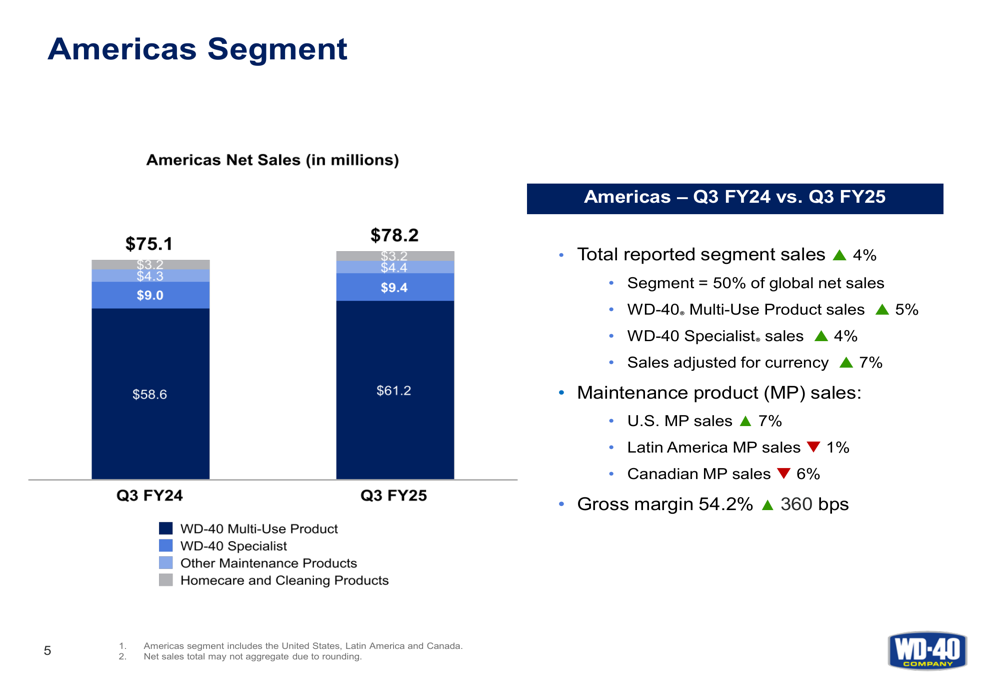

Regional performance varied significantly across WD-40’s three geographic segments. The Americas segment, which represents 50% of global net sales, saw a 4% increase in sales, driven primarily by a 5% growth in WD-40 Multi-Use Product sales and a 4% increase in WD-40 Specialist sales.

The following chart illustrates the Americas segment performance:

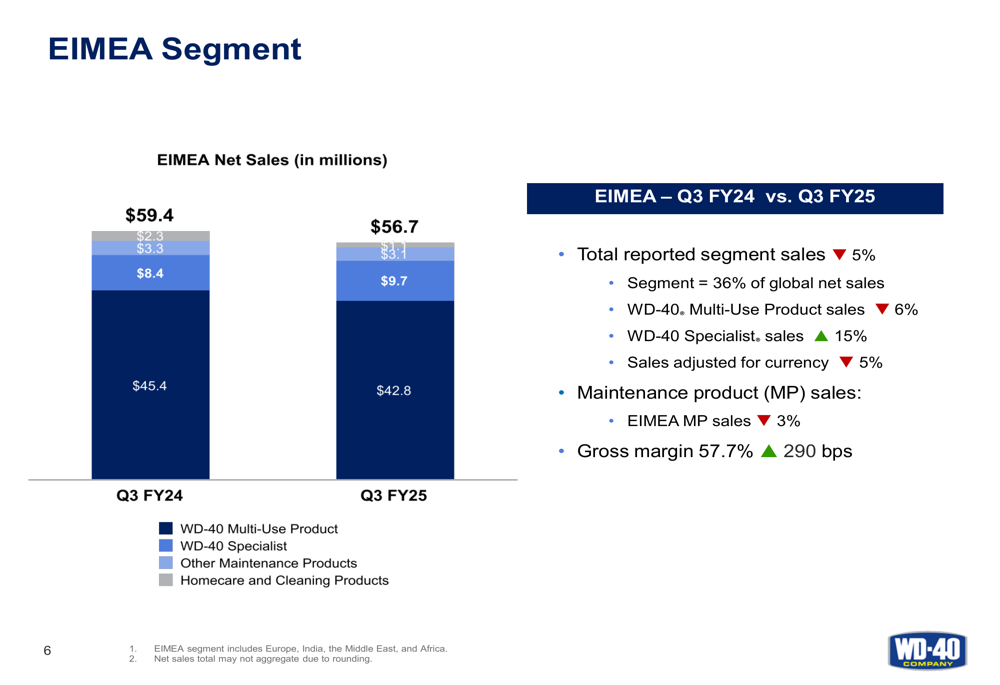

In contrast, the EIMEA (Europe, India, Middle East, and Africa) segment, which accounts for 36% of global net sales, experienced a 5% decline in sales. While WD-40 Specialist sales grew impressively by 15% in this region, WD-40 Multi-Use Product sales decreased by 6%.

The regional breakdown for EIMEA is shown here:

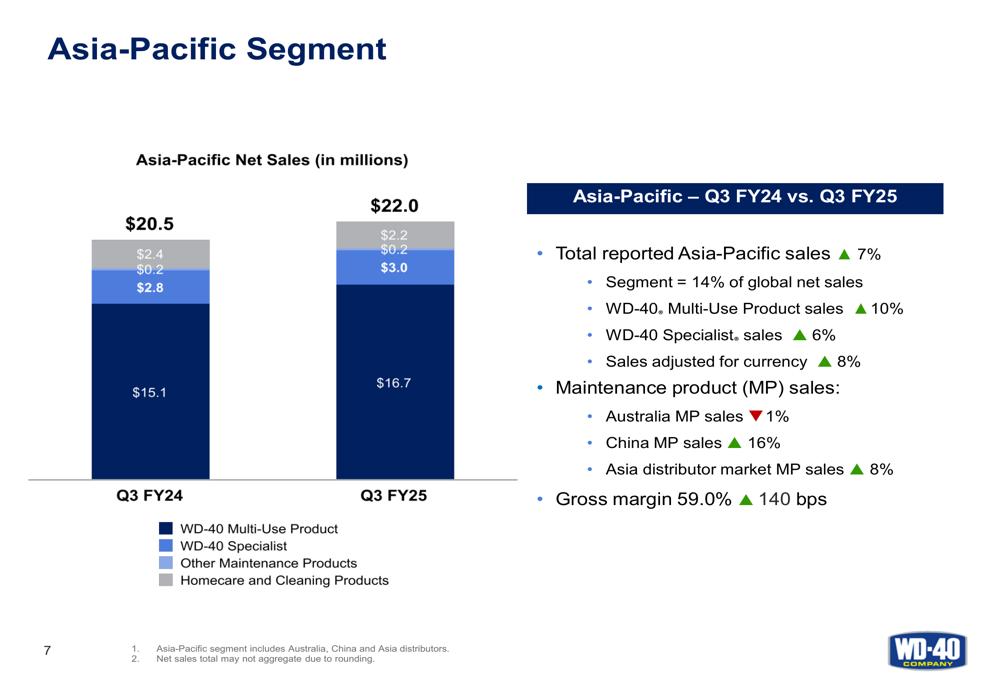

The Asia-Pacific segment, representing 14% of global net sales, delivered the strongest performance with a 7% increase in sales. This growth was fueled by a 10% rise in WD-40 Multi-Use Product sales and a 6% increase in WD-40 Specialist sales. Particularly notable was the 16% growth in China maintenance product sales.

The Asia-Pacific performance is detailed in this chart:

Strategic Initiatives

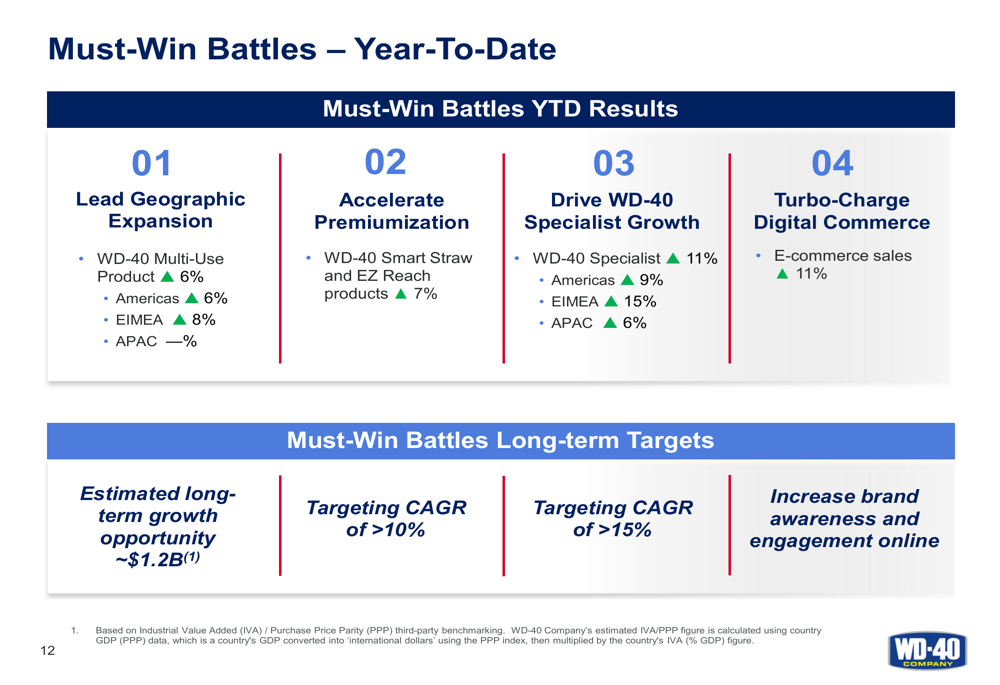

WD-40 continues to execute its "Four-by-Four" strategic framework, which consists of four "Must-Win Battles" and four "Strategic Enablers." The company’s strategic focus areas include geographic expansion, premiumization, WD-40 Specialist growth, and digital commerce acceleration.

The strategic framework is outlined here:

Year-to-date progress on these strategic initiatives shows mixed results. WD-40 Multi-Use Product sales are up 6% overall, with growth in Americas (6%) and EIMEA (8%) but a decline in Asia-Pacific. The company’s premiumization efforts are yielding results, with WD-40 Smart Straw and EZ Reach products up 7%. WD-40 Specialist products have shown strong growth of 11% overall, and e-commerce sales have increased by 11%.

The following chart details the year-to-date progress on these strategic initiatives:

Detailed Financial Analysis

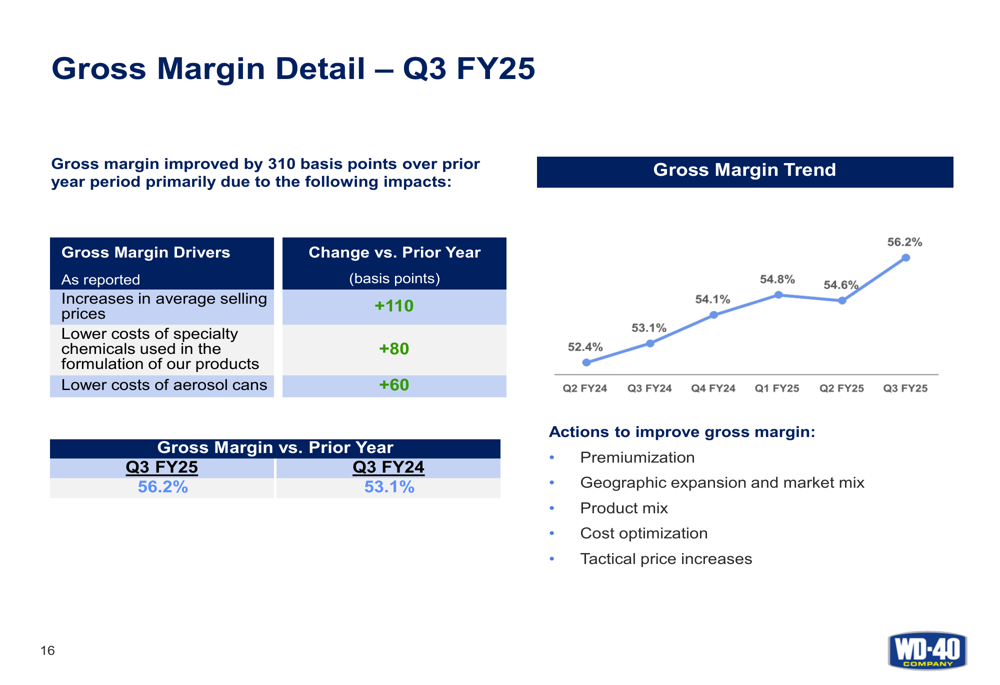

A key highlight of WD-40’s Q3 FY25 results was the significant improvement in gross margin, which reached 56.2%, up 310 basis points from 53.1% in the same period last year. This improvement was driven by three main factors: increases in average selling prices (+110 basis points), lower costs of specialty chemicals (+80 basis points), and lower costs of aerosol cans (+60 basis points).

The gross margin trend and detailed breakdown are illustrated here:

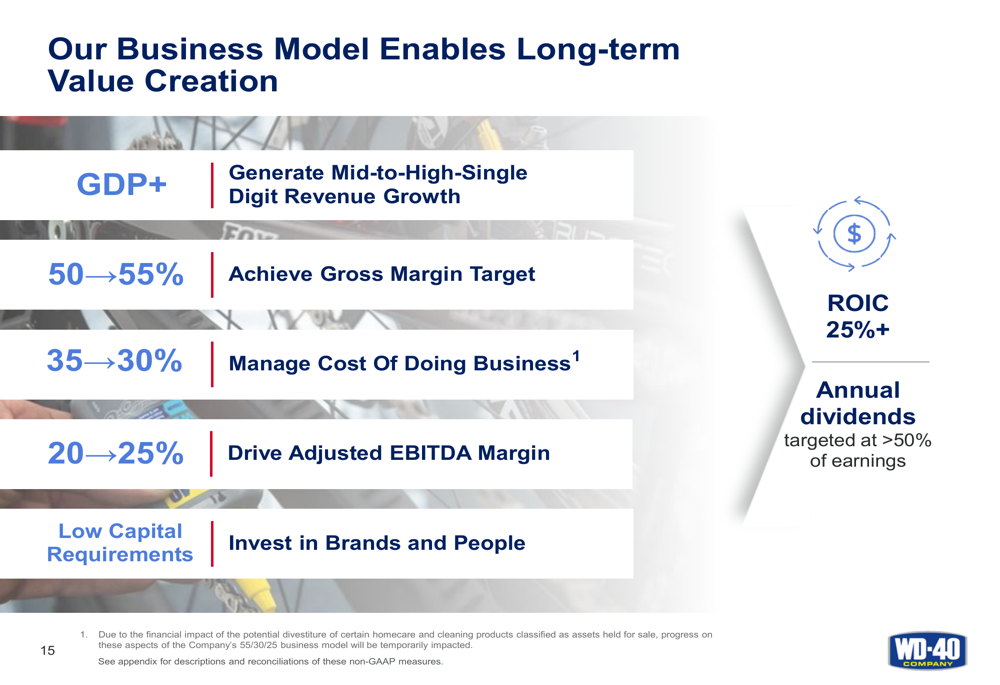

The company’s long-term business model targets include achieving a gross margin of 50-55%, managing the cost of doing business from 35% to 30%, and driving adjusted EBITDA margin to 20-25%. For Q3 FY25, WD-40 reported an adjusted EBITDA margin of 20%, up from 19% in the prior year period.

The business model overview is shown in this image:

Forward-Looking Statements

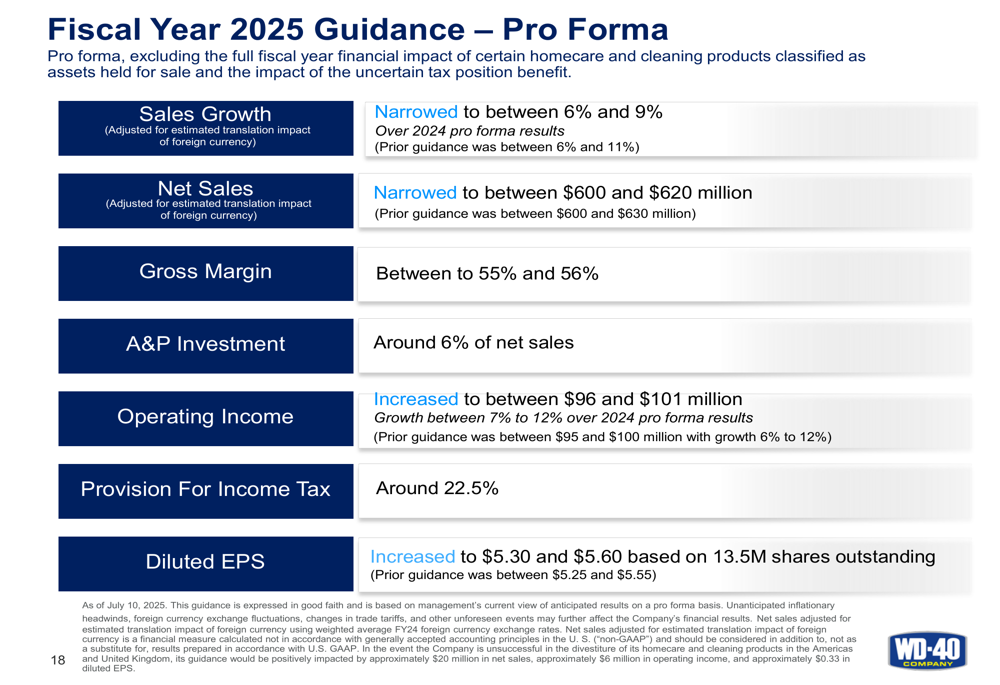

WD-40 has narrowed its fiscal year 2025 sales growth guidance to between 6% and 9% over 2024 pro forma results, down from the previous range of 6% to 11%. Net sales are now expected to be between $600 million and $620 million, compared to the earlier projection of $600 million to $630 million.

Despite the narrowed revenue guidance, the company increased its EPS outlook, now projecting diluted EPS between $5.30 and $5.60, up from the previous range of $5.25 to $5.55. Operating income is expected to be between $96 million and $101 million, representing growth of 7% to 12% over 2024 pro forma results.

The updated FY25 guidance is detailed here:

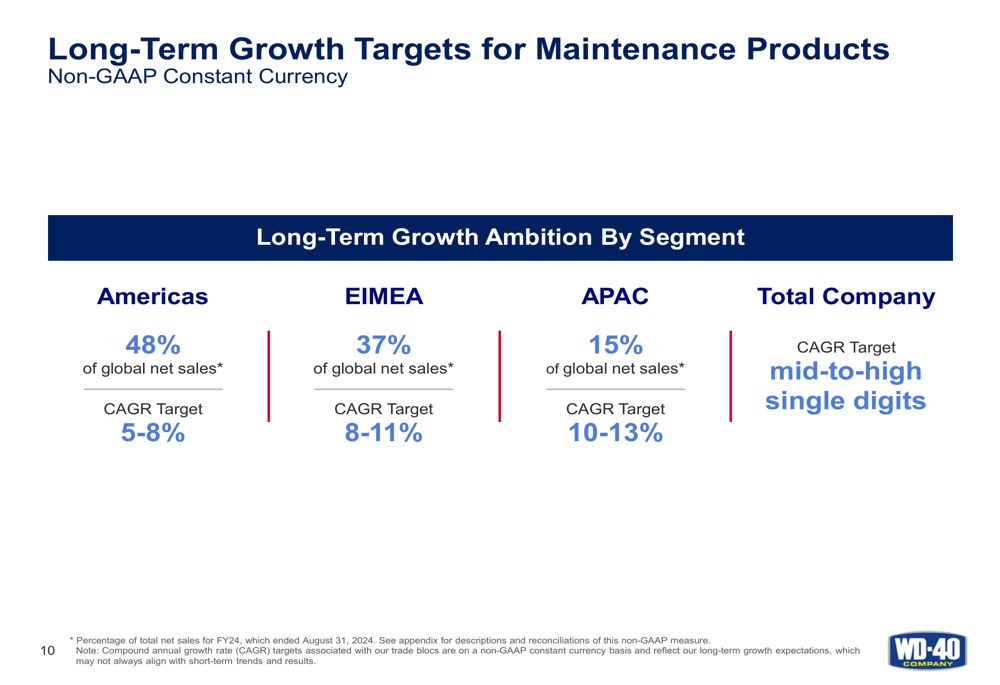

Looking at longer-term growth targets, WD-40 aims to achieve different growth rates across its geographic segments: 5-8% CAGR for the Americas, 8-11% CAGR for EIMEA, and 10-13% CAGR for Asia-Pacific. Overall, the company targets mid-to-high single-digit compound annual growth rate for total maintenance product sales.

The long-term growth targets by region are illustrated in this chart:

Divestiture Plans

WD-40 is planning to divest certain homecare and cleaning brands in the coming months to focus on its core maintenance products business. To provide better visibility into the ongoing business, the company has presented pro forma results excluding the impact of these assets held for sale.

On a pro forma basis for Q3 FY25, excluding the homecare and cleaning products classified as assets held for sale, WD-40 reported net sales of $152.6 million (up 2% year-over-year), gross margin of 56.6% (up 300 basis points), and diluted EPS of $1.48 (up 8%).

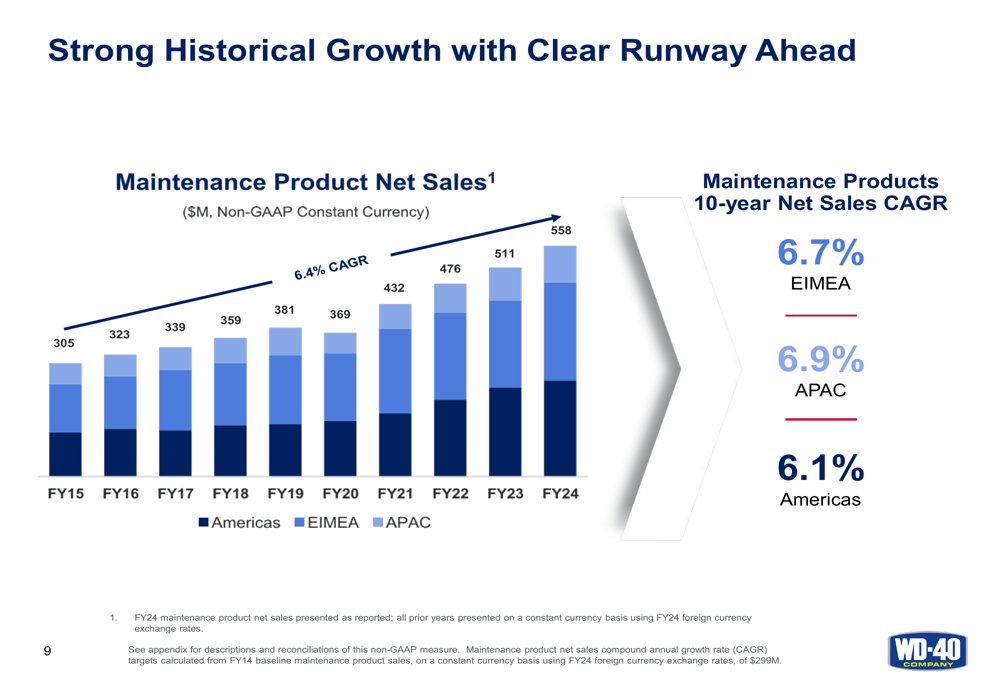

The historical performance of the maintenance products business shows consistent growth, with a 10-year compound annual growth rate (CAGR) of 6.4%. This growth has been relatively balanced across regions, with EIMEA at 6.7% CAGR, Asia-Pacific at 6.9% CAGR, and Americas at 6.1% CAGR over the past decade.

The historical growth trend for maintenance products is shown here:

CEO Steve Brass highlighted the company’s record sales quarter and ongoing supply chain initiatives during the earnings call, stating, "The third quarter was a record sales quarter for the company reflecting continued progress and momentum." He also emphasized the importance of digital commerce, noting, "Our digital channel serves as far more than a transactional platform."

While WD-40 continues to make progress on its strategic initiatives and margin improvement, the company faces challenges including supply chain pressures, potential market saturation in mature markets, rising operational costs, currency fluctuations, and competitive pressures in the maintenance products sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.