FTSE 100 today: Edges higher as pound slips; Mitchells & Butlers jumps on results

Introduction & Market Context

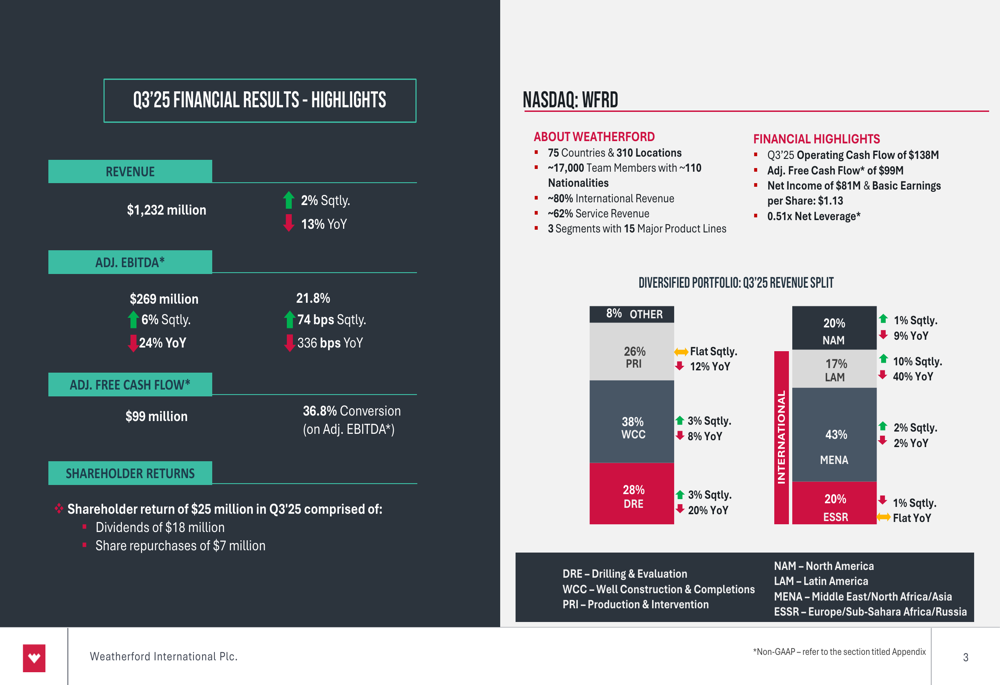

Weatherford International PLC (NASDAQ:WFRD) released its Q3 2025 investor presentation on October 22, highlighting strong revenue growth and significant balance sheet improvements despite falling short of earnings expectations. The oilfield services provider, which operates in 75 countries with approximately 17,000 employees, reported mixed results that saw its stock decline 0.88% in premarket trading to $66.13.

The company's presentation emphasized its international footprint, with approximately 80% of revenue coming from outside North America, providing some insulation from the softer North American market conditions mentioned during the earnings call.

Quarterly Performance Highlights

Weatherford reported Q3 2025 revenue of $1.23 billion, representing a 2% sequential increase and a robust 13% year-over-year growth. This exceeded analyst expectations of $1.17 billion by 5.13%. However, the company's earnings per share of $1.13 fell short of the forecasted $1.18, representing a negative surprise of 5.08%.

Adjusted EBITDA reached $269 million, increasing 6% sequentially and 24% year-over-year, with margins expanding to 21.8% – an improvement of 74 basis points sequentially and 336 basis points year-over-year.

As shown in the following financial highlights:

Net income for the quarter was $81 million, with the company generating $99 million in adjusted free cash flow, representing a 36.8% conversion rate on adjusted EBITDA. This cash flow performance, while solid, was lower than the 51.7% conversion rate achieved in Q3 2024.

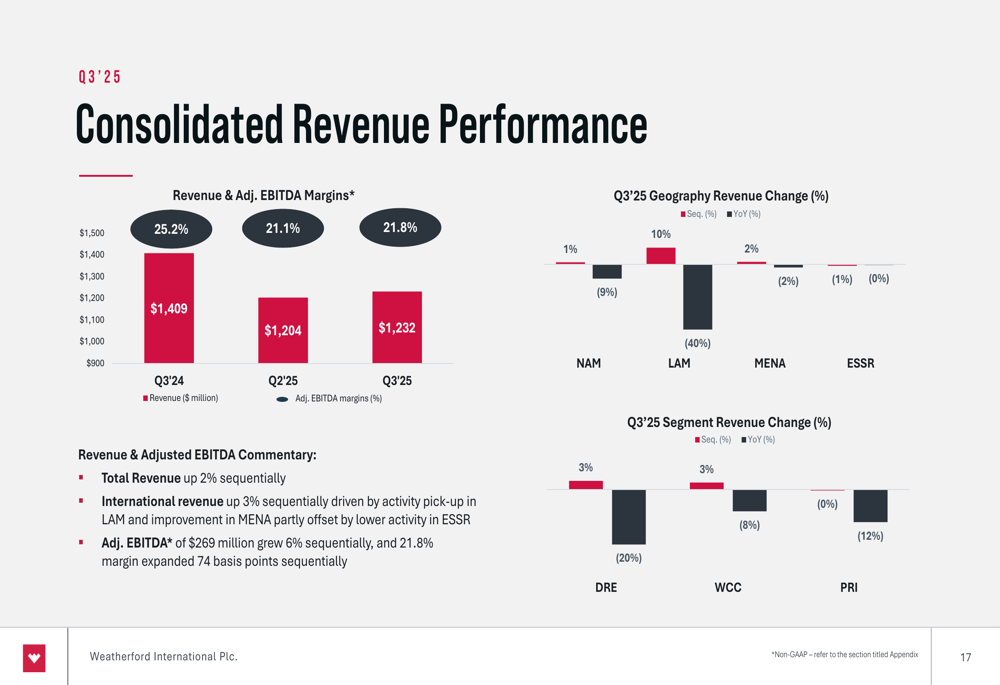

The consolidated revenue performance across regions showed significant variability:

Latin America emerged as the strongest performing region with an impressive 40% sequential growth, while North America declined by 9% sequentially, reflecting challenging market conditions in that region. The Middle East and North Africa (MENA) region, which accounts for 43% of Weatherford's revenue, experienced a slight 2% sequential decline.

Balance Sheet Improvements & Capital Allocation

A major focus of Weatherford's presentation was its significantly strengthened balance sheet and improved liquidity position. The company expanded its credit facility by $280 million to $1 billion with an extension through 2030, while also restructuring its debt through a $1.2 billion offering of 6.75% Senior Notes due 2033 and a cash tender offer of $1.3 billion 8.625% Senior Unsecured Notes due 2030.

These financial maneuvers resulted in a net leverage ratio of just 0.51x and annual interest cost savings of approximately $31 million. The improved financial position also led to credit rating upgrades from all three major rating agencies.

The following slide details these balance sheet improvements:

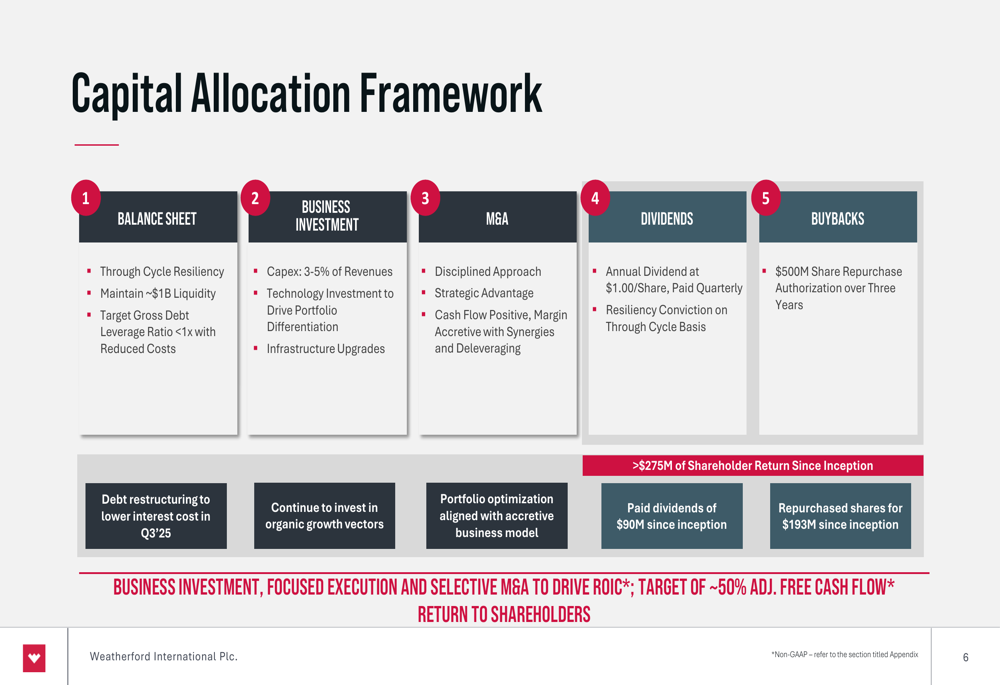

Weatherford's capital allocation framework prioritizes five key areas: balance sheet strength, business investment, strategic M&A, dividends, and share buybacks. The company has returned over $275 million to shareholders since initiating its return program, including $90 million in dividends and $193 million in share repurchases. For Q3 2025 specifically, Weatherford returned $25 million to shareholders through $18 million in dividends and $7 million in share repurchases.

The company's capital allocation strategy is illustrated below:

Segment Performance Analysis

Weatherford operates through three main segments, each showing varying performance in Q3 2025:

The Well Construction and Completions (WCC) segment, which represents 38% of revenue, was the strongest performer with revenue of $468 million and segment adjusted EBITDA of $125 million, yielding a 26.7% margin. This segment grew 3% sequentially but declined 8% year-over-year.

The Drilling and Evaluation (DRE) segment, accounting for 28% of revenue, generated $346 million in revenue and $83 million in adjusted EBITDA with a 24.0% margin. This segment grew 3% sequentially but declined 20% year-over-year.

The Production and Intervention (PRI) segment, representing 26% of revenue, reported $326 million in revenue and $59 million in adjusted EBITDA with an 18.1% margin. This segment remained flat sequentially but declined 12% year-over-year.

Strategic Initiatives & Digital Transformation

Weatherford highlighted its "Industrial Intelligence" platform as a key strategic initiative, which was launched at the company's FWRD 2025 Technology Conference. This platform aims to transform operational data through a modern edge computing architecture and software launchpad.

The company emphasized its market leadership positions, particularly as the #1 market leader in Managed Pressure Drilling (MPD) and Tubular Running Service (TRS). Weatherford's digitally enabled offerings, including Victus® Intelligent MPD, Centro™ Well Construction Planning and Optimization Platform, and Vero® Automated Connection Integrity, were presented as key differentiators in the competitive oilfield services landscape.

Forward-Looking Statements

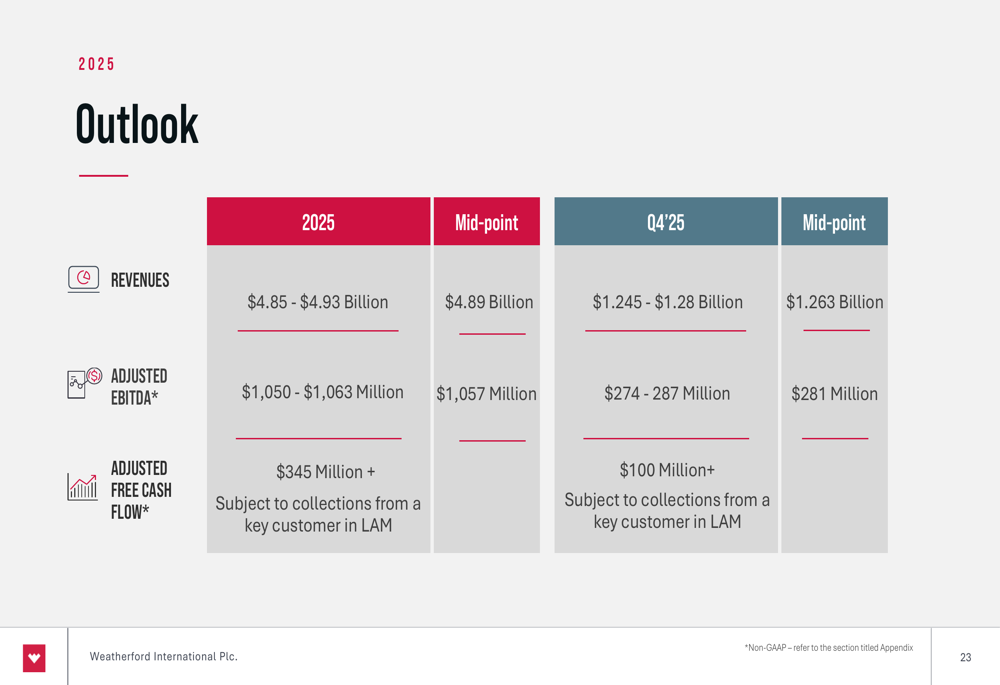

Weatherford provided a detailed outlook for the remainder of 2025 and offered some perspective on 2026:

For full-year 2025, the company expects revenues between $4.85 billion and $4.93 billion, with adjusted EBITDA between $1.05 billion and $1.06 billion. For Q4 2025, Weatherford projects revenues of $1.245-$1.28 billion and adjusted EBITDA of $274-287 million.

The company anticipates adjusted free cash flow of over $100 million in Q4 2025, subject to collections from a key customer in Latin America, and over $345 million for the full year 2025.

During the earnings call, CEO Girish Alagram expressed optimism about the company's future, stating, "I have never been more excited about the future of Weatherford," while emphasizing the company's commitment to margin expansion. CFO Anuj Drew highlighted the company's transformation, noting, "This is not just a technological transformation. It's going to rethink how we do business."

Looking ahead to 2026, management indicated expectations for a soft first half followed by a rebound in the latter half of the year, maintaining a focus on margin expansion and free cash flow conversion above 40%.

Weatherford concluded its presentation with a compelling investment thesis, highlighting five key reasons to invest in the company:

With its differentiated product and service portfolio, international focus, improved financial performance, asset-light balance sheet strategy, and strong cash flow generation, Weatherford aims to create long-term shareholder value despite the near-term challenges reflected in its recent stock performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.