Gold prices steady ahead of Fed decision; weekly weakness noted

Introduction & Market Context

Wendy’s Co. (NASDAQ:WEN) presented its first quarter 2025 results on May 2, revealing a challenging domestic environment offset partially by international growth. The fast-food chain is trading near its 52-week low of $11.70, with shares closing at $12.12 on May 9, down 0.91% for the day.

The company’s presentation highlighted strategic initiatives aimed at revitalizing performance amid headwinds in the U.S. quick-service restaurant market. While Wendy’s maintained its traffic and dollar share in the U.S. QSR burger category, overall financial results showed declines in key metrics compared to the same period last year.

Quarterly Performance Highlights

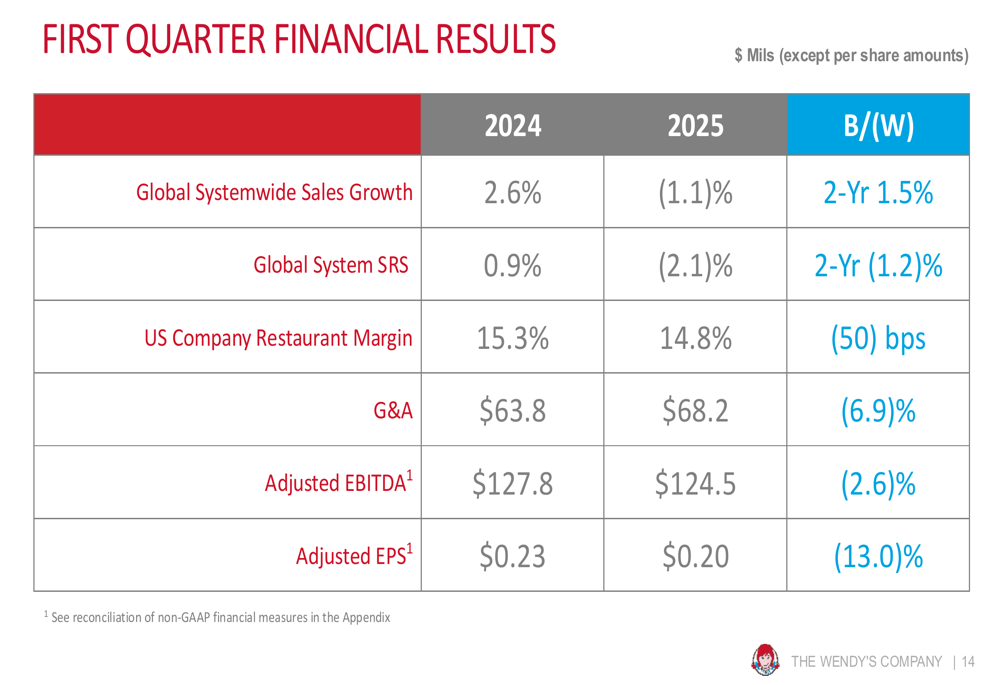

Wendy’s reported mixed results for Q1 2025, with global systemwide sales declining 1.1% compared to 2.6% growth in the same period last year. Global same-restaurant sales (SRS) fell 2.1%, a significant reversal from the 0.9% growth seen in Q1 2024.

The U.S. market proved particularly challenging, with same-restaurant sales declining 2.8%. However, international operations provided a bright spot, delivering 8.9% systemwide sales growth and 2.3% same-restaurant sales growth.

As shown in the following quarterly highlights:

The company’s restaurant expansion continued despite sales challenges, with 74 new restaurants opened globally during the quarter. Wendy’s also maintained its commitment to shareholder returns, distributing over $173 million through dividends and share repurchases.

Strategic Initiatives

CEO Kirk Tanner outlined three strategic pillars driving Wendy’s long-term strategy: doubling down on fresh, famous food; delivering an exceptional customer experience; and accelerating global unit growth.

The company’s strategic framework is illustrated in this overview:

For the food pillar, Wendy’s emphasized local sourcing of ingredients and highlighted successful collaborations, including the Thin Mint Frosty partnership with Girl Scouts. The company is launching a "100 Days of Summer" promotion featuring new collaborations like Takis to drive customer engagement.

"Listening to the customer will always steer you in the right direction," noted Tanner during the earnings call, emphasizing the company’s customer-centric approach.

On the customer experience front, Wendy’s completed the rollout of its new field organization and is implementing technological enhancements:

The company is on track to deploy digital menu boards and FreshAI technology to more than 500 restaurants in 2025, which management believes will improve order accuracy and operational efficiency.

Financial Analysis

Wendy’s financial performance showed several concerning trends in Q1 2025. Adjusted EBITDA fell 2.6% to $124.5 million, while adjusted earnings per share declined 13% to $0.20, matching analyst expectations but reflecting underlying pressure on profitability.

The detailed financial comparison reveals the extent of the challenges:

U.S. company-operated restaurant margin decreased to 14.8% from 15.3% in the prior year, reflecting cost pressures. General and administrative expenses increased 6.9% to $68.2 million.

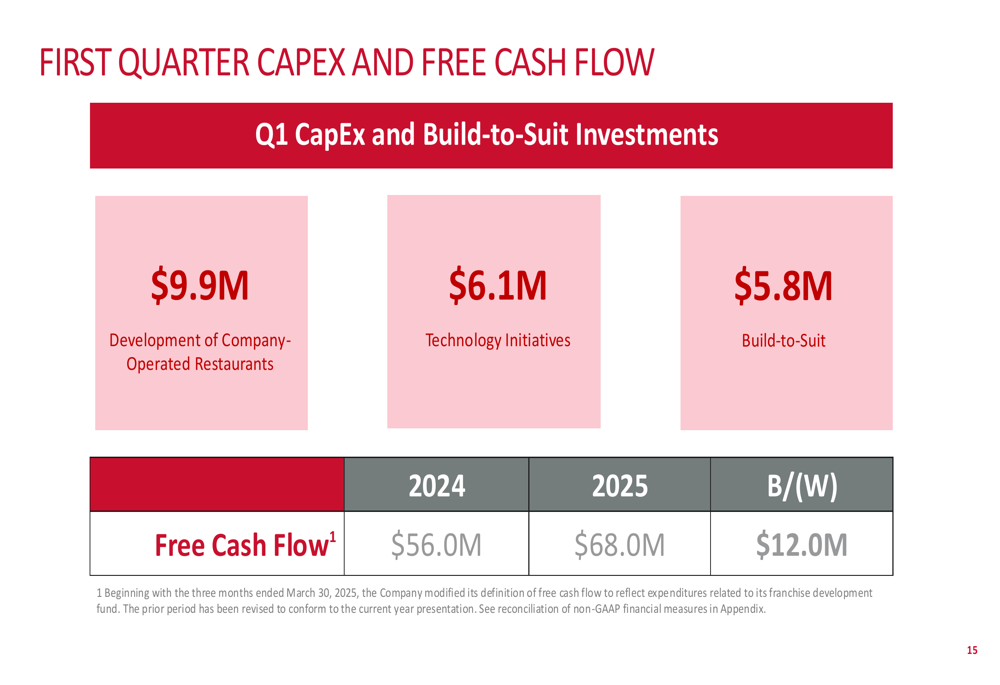

Despite these challenges, free cash flow improved to $68 million from $56 million in the prior year:

The company continued its share repurchase program, buying back 8.2 million shares during the quarter and anticipating up to $25 million in additional repurchases through the remainder of 2025. Wendy’s declared a quarterly dividend of $0.14 per share, maintaining its target payout ratio of 50-60% of adjusted earnings.

2025 Outlook

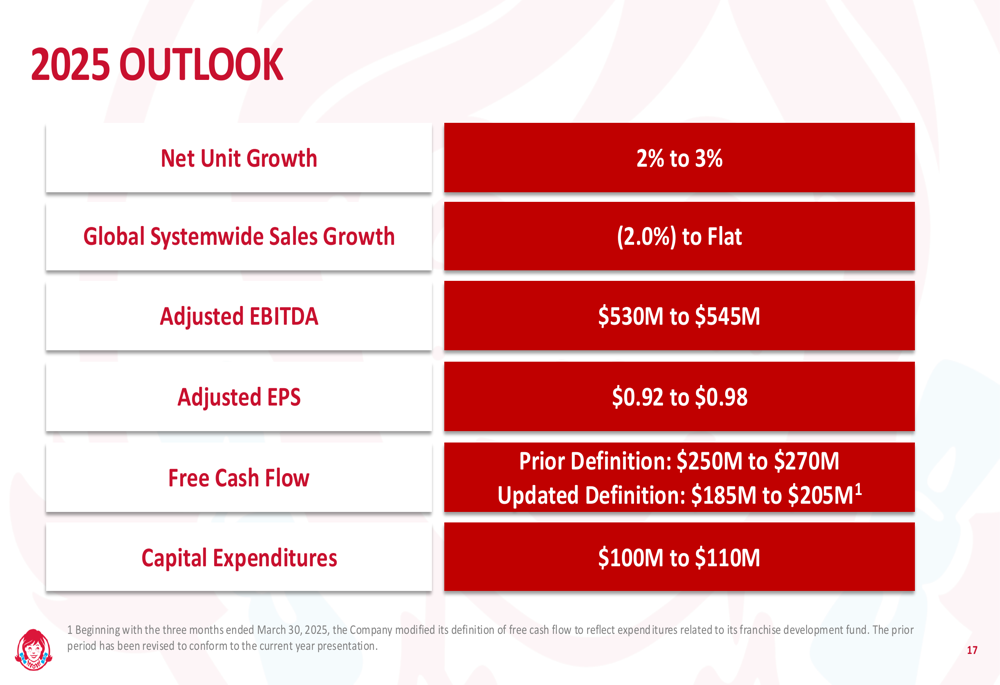

Wendy’s maintained its full-year guidance despite the challenging first quarter, projecting global systemwide sales to range from a 2% decline to flat growth. The company expects net unit growth of 2-3% for the year.

The full outlook is detailed in this guidance summary:

Adjusted EBITDA is projected between $530 million and $545 million, with adjusted earnings per share expected to range from $0.92 to $0.98. Capital expenditures are anticipated between $100 million and $110 million.

CFO Ken Cook emphasized the company’s long-term focus, stating, "We continue to manage the business for the long term, investing in our strategic priorities."

The company anticipates similar performance in Q2, with potential momentum building in Q3 driven by summer initiatives. International markets are expected to continue outperforming domestic operations, providing a partial offset to U.S. weakness.

While Wendy’s faces significant challenges in its core U.S. market, its international growth, restaurant expansion, and commitment to shareholder returns demonstrate management’s efforts to navigate the current environment while positioning for future recovery.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.