Gold prices edge higher with focus on Ukraine-Russia, Jackson Hole

Introduction & Market Context

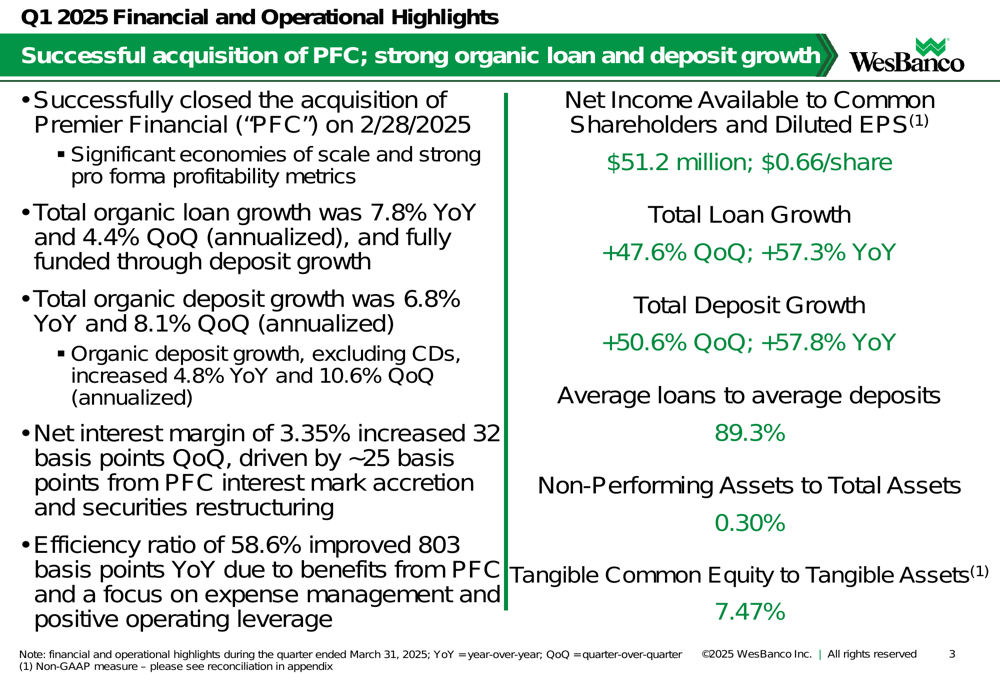

WesBanco Inc. (NASDAQ:WSBC) presented its first quarter 2025 earnings results on April 29, highlighting the transformative impact of its recently completed acquisition of Premier Financial Corporation (PFC). The acquisition, which closed on February 28, 2025, significantly expanded WesBanco’s footprint and contributed to substantial growth in key financial metrics.

The bank reported adjusted net income available to common shareholders of $51.2 million, or $0.66 per diluted share, after accounting for day one provision for credit losses on acquired loans and merger-related expenses. On a reported basis, the company posted a net loss of $11.5 million, or -$0.15 per share, primarily due to these one-time items.

WesBanco’s stock closed at $29.91 on the day of the earnings presentation, within its 52-week range of $25.56 to $37.36, showing modest market reaction to the results.

Quarterly Performance Highlights

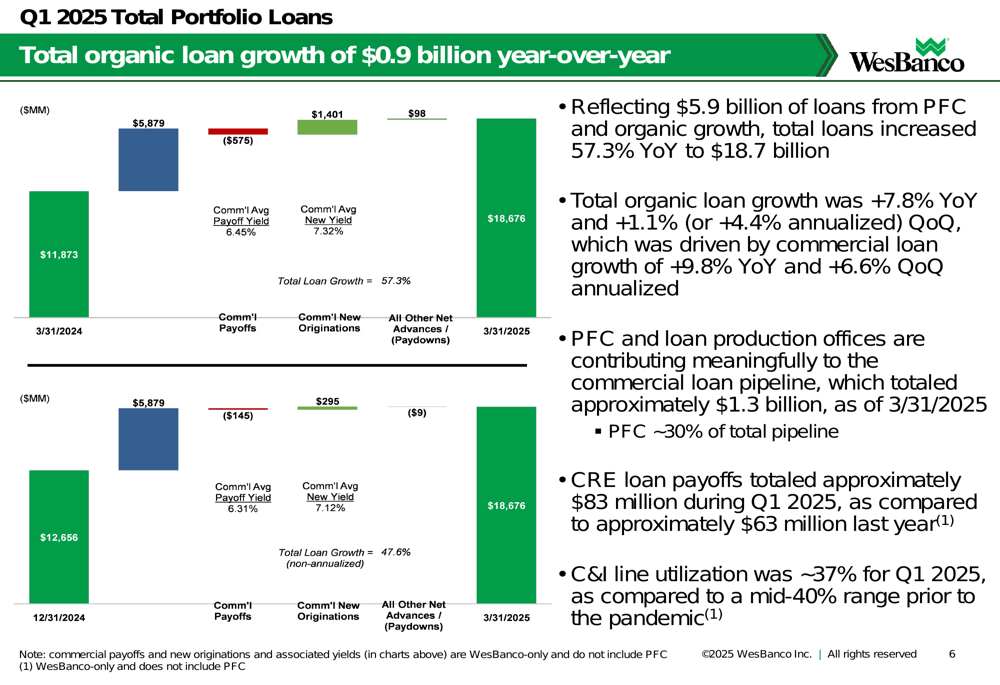

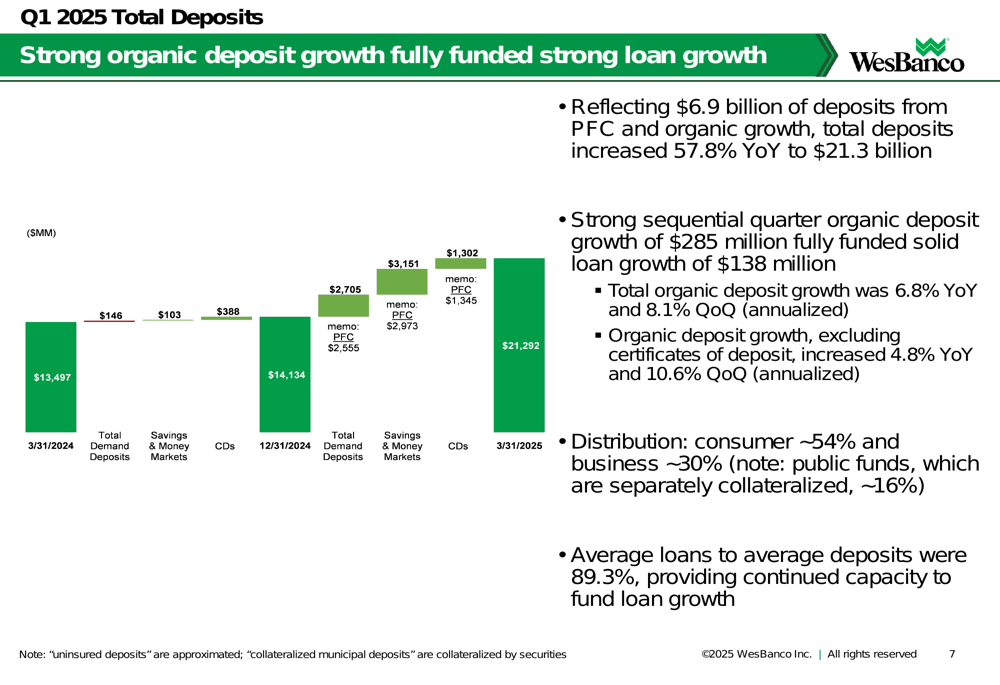

The first quarter results revealed substantial growth across key metrics, largely driven by the PFC acquisition but also showing solid organic performance. Total (EPA:TTEF) loans increased 57.3% year-over-year to $18.7 billion, while total deposits grew 57.8% to $21.3 billion.

As shown in the following summary of financial and operational highlights:

On an organic basis, WesBanco demonstrated continued momentum with loan growth of 7.8% year-over-year and 4.4% quarter-over-quarter (annualized). Deposit growth was equally impressive at 6.8% year-over-year and 8.1% quarter-over-quarter (annualized), fully funding the loan growth.

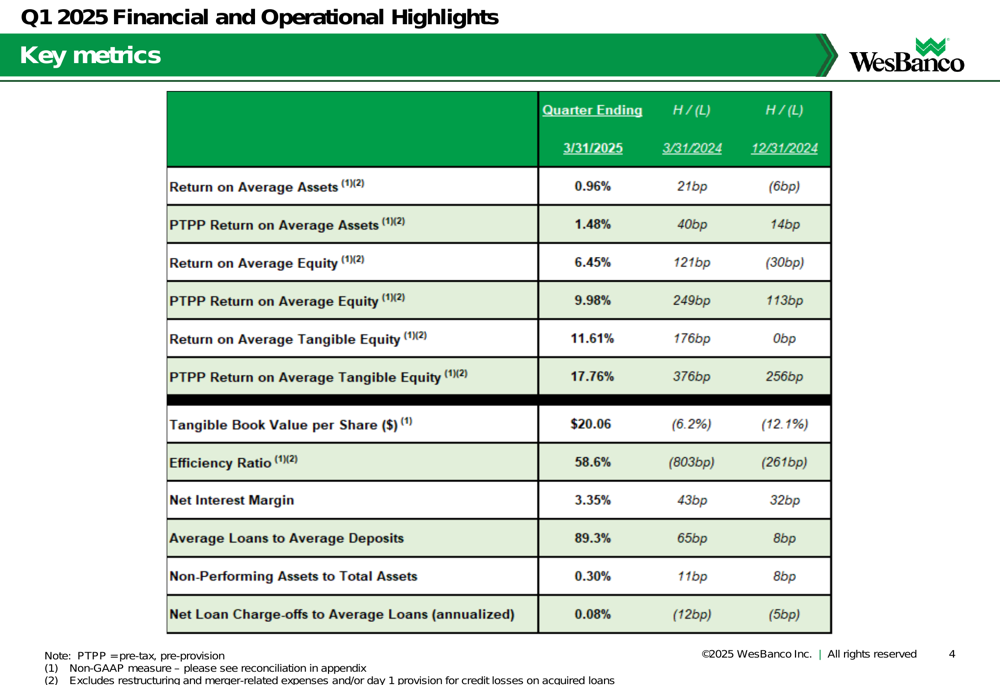

The company’s key performance metrics showed significant improvement compared to both the previous quarter and the same period last year:

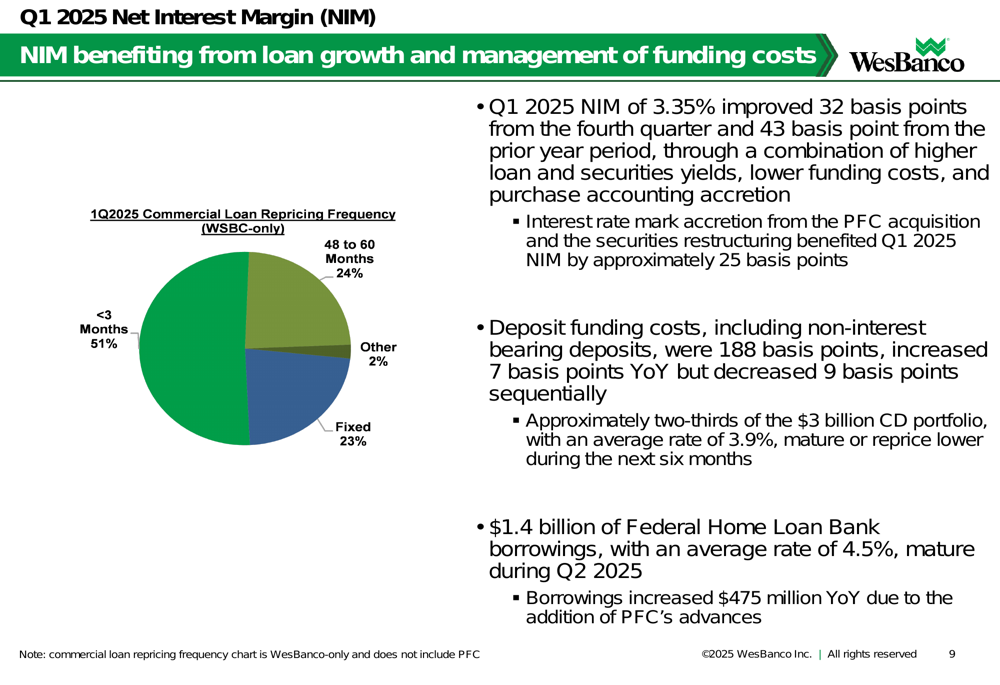

Net interest margin expanded to 3.35%, improving 32 basis points from the fourth quarter and 43 basis points year-over-year. This improvement was partially attributed to interest rate mark accretion from the PFC acquisition and securities restructuring, which benefited Q1 2025 NIM by approximately 25 basis points.

The efficiency ratio improved to 58.6%, representing an 803 basis point improvement year-over-year and 261 basis point improvement quarter-over-quarter, reflecting the benefits of the PFC acquisition and operational synergies.

Acquisition Impact

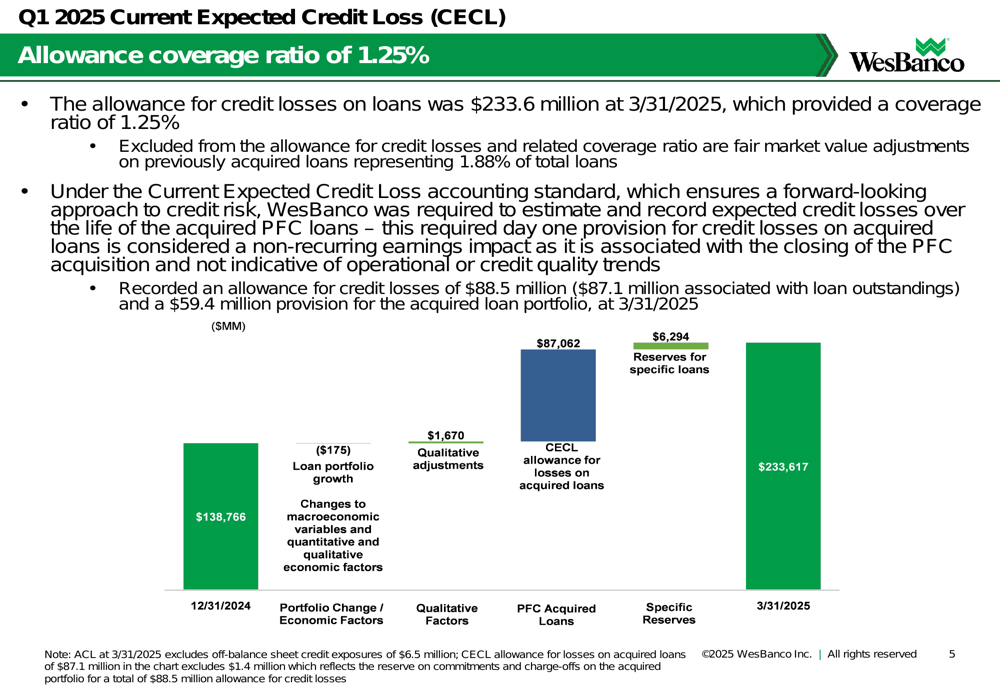

The PFC acquisition significantly transformed WesBanco’s balance sheet, adding approximately $5.9 billion in loans and $6.9 billion in deposits. However, the acquisition also necessitated a day one provision for credit losses on acquired loans of $46.9 million, which impacted reported earnings.

The following chart illustrates the components of the allowance for credit losses, including the impact of the PFC acquisition:

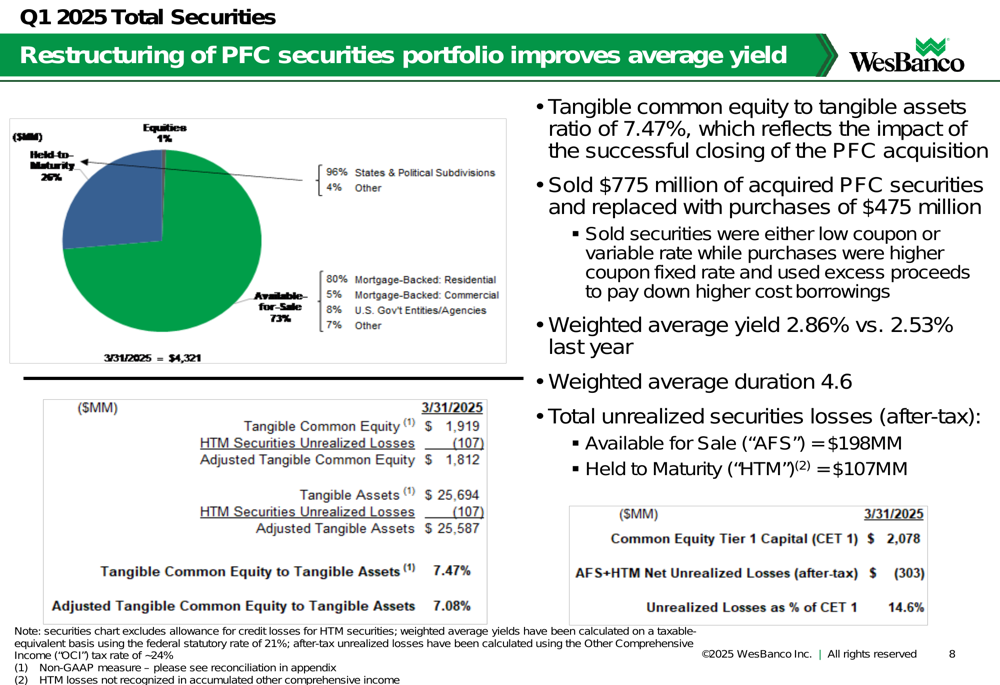

WesBanco also undertook a strategic restructuring of the acquired PFC securities portfolio to improve yield. The company sold $775 million of acquired PFC securities and replaced them with $475 million in new purchases, increasing the weighted average yield from 2.53% last year to 2.86%.

As shown in the following breakdown of the securities portfolio:

The tangible common equity to tangible assets ratio stood at 7.47%, reflecting a solid capital position despite the acquisition-related impacts. Total unrealized securities losses (after-tax) amounted to $305 million, split between Available for Sale ($198 million) and Held to Maturity ($107 million).

Detailed Financial Analysis

WesBanco’s loan portfolio experienced substantial growth, both from the acquisition and organic business activity. The following chart breaks down the changes in the loan portfolio:

On the deposit side, strong organic growth of $285 million in the quarter fully funded the loan growth of $138 million. The deposit mix remained favorable with consumer deposits representing approximately 54% of the total.

Net interest margin improvement was supported by the acquisition and securities restructuring. The commercial loan portfolio shows a balanced repricing frequency, with 51% repricing in less than three months, providing some protection against interest rate fluctuations:

Non-interest income increased $4.0 million, or 13%, year-over-year to $34.7 million, with notable growth in trust fees (+7.6%), service charges on deposits (+26.6%), and mortgage banking income (+64.5%). Bank-owned life insurance income increased 65.8% year-over-year, including a $0.9 million death benefit received and the addition of PFC.

Non-interest expense, excluding merger and restructuring charges, increased 17% year-over-year due to the addition of PFC operations. The improved efficiency ratio reflects operational synergies and scale benefits from the acquisition.

Credit Quality & Capital Position

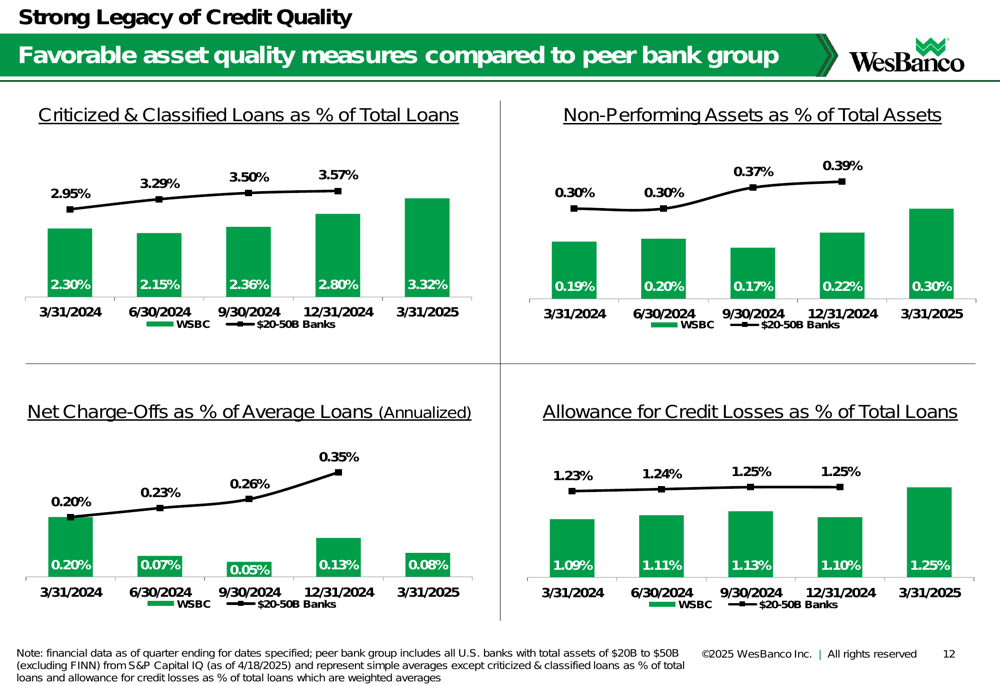

WesBanco maintained strong credit quality metrics compared to peer banks, continuing its legacy of prudent risk management. The following charts illustrate WesBanco’s favorable position relative to peers:

Non-performing assets as a percentage of total assets stood at 0.30%, while net charge-offs as a percentage of average loans were 0.08% (annualized). The allowance for credit losses as a percentage of total loans was 1.25%, providing adequate coverage for potential loan losses.

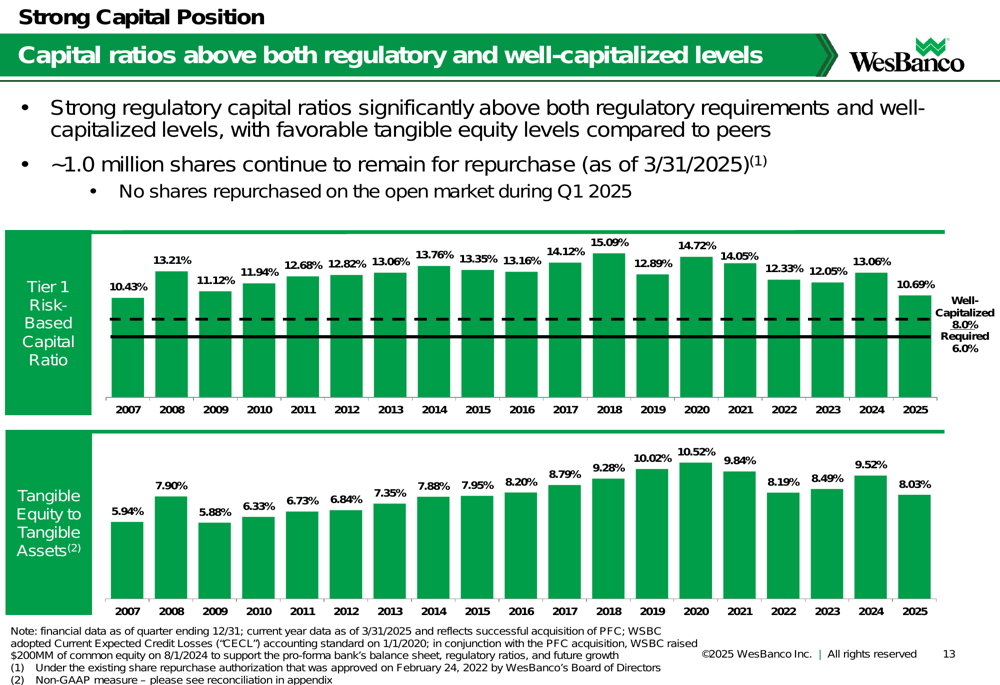

The company’s capital position remains solid, with capital ratios exceeding both regulatory requirements and well-capitalized levels:

The Tier 1 risk-based capital ratio stood at 10.69%, well above the well-capitalized requirement of 8.0%. The tangible equity to tangible assets ratio was 8.03%, demonstrating the company’s strong capital foundation even after completing the significant acquisition.

Forward-Looking Statements

WesBanco appears well-positioned for continued growth following the PFC acquisition, with integration efforts underway to realize additional cost synergies and operational efficiencies. The company’s strong organic growth in both loans and deposits suggests underlying business momentum beyond the acquisition impact.

The improved net interest margin and efficiency ratio point to potential earnings growth as the full benefits of the acquisition are realized in future quarters. The company’s share repurchase authorization, with approximately 1.0 million shares remaining for repurchase, provides flexibility for capital management.

WesBanco’s continued focus on credit quality and maintaining strong capital ratios suggests a conservative approach to growth, balancing expansion opportunities with risk management. The successful integration of PFC will be a key factor in determining the company’s performance through the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.