U.S. stocks steady; Cook’s dismissal, Nvidia earnings in spotlight

Introduction & Market Context

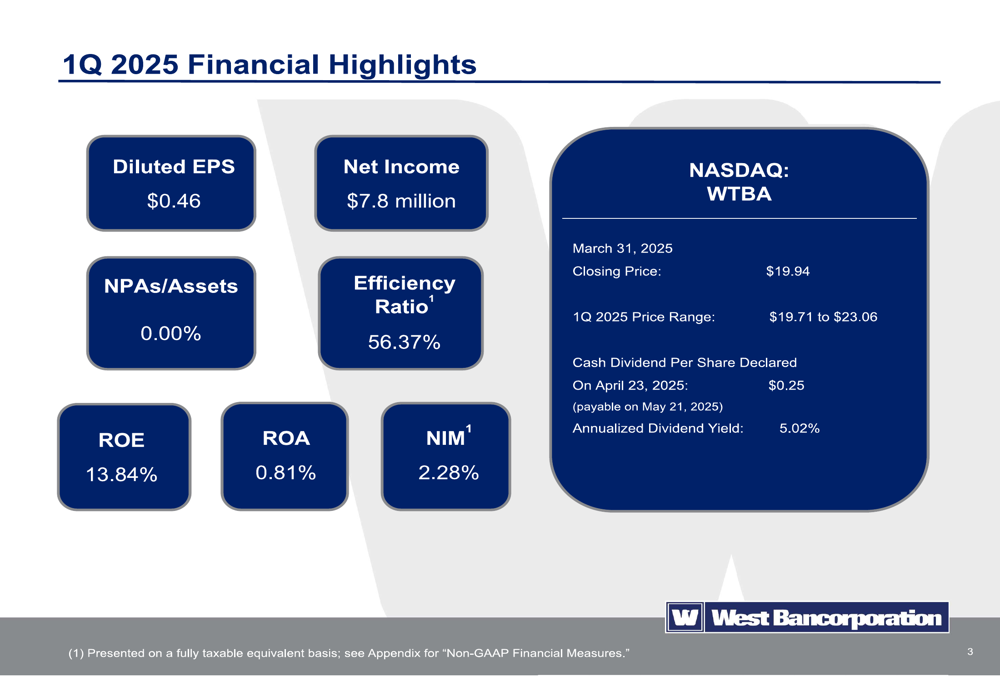

West Bancorporation, Inc. (NASDAQ:WTBA) released its first quarter 2025 earnings presentation, revealing improved profitability metrics and continued execution of its conservative growth strategy. The Iowa-based financial holding company reported diluted earnings per share of $0.46 and net income of $7.8 million, showing sequential improvement from the previous quarter’s results.

The company’s stock closed at $19.66 on April 23, 2025, trading within its 52-week range of $16.18 to $24.85. West Bancorporation declared a quarterly cash dividend of $0.25 per share on April 23, 2025, payable on May 21, 2025, representing an annualized dividend yield of 5.02%.

Quarterly Performance Highlights

West Bancorporation delivered solid financial results for the first quarter of 2025, with notable improvements in key performance metrics compared to both the previous quarter and the same period last year.

As shown in the following financial highlights from the presentation:

The company reported a return on equity of 13.84% and return on assets of 0.81%, both showing improvement from previous quarters. The efficiency ratio improved to 56.37%, indicating better operational performance. Most notably, the company maintained excellent asset quality with a non-performing assets to total assets ratio of 0.00%.

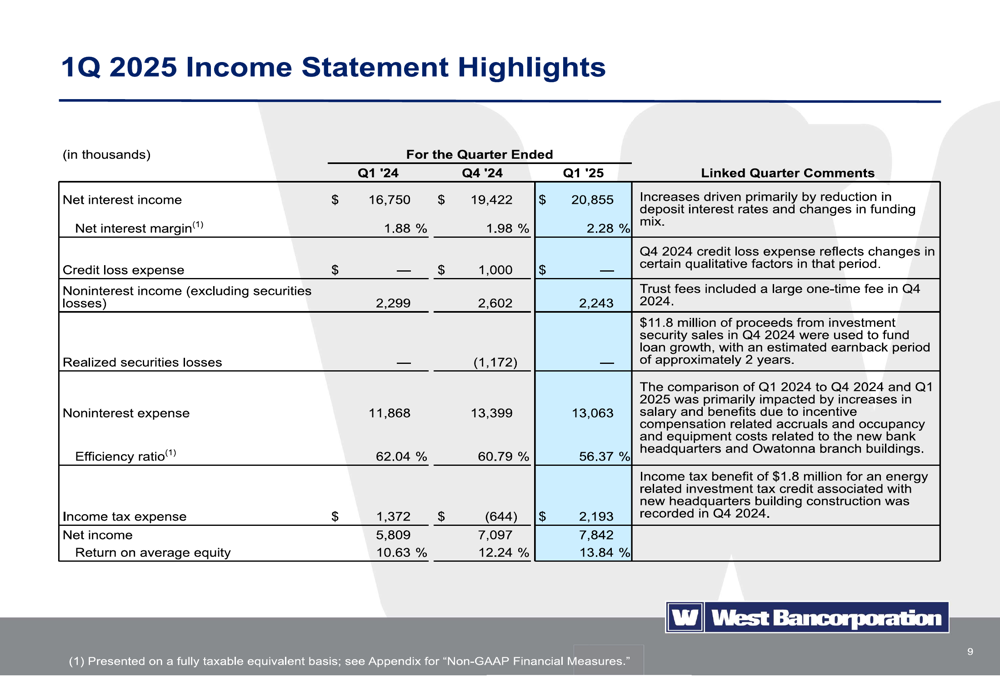

A more detailed breakdown of the income statement reveals the drivers behind these improvements:

Net income increased to $7.8 million in Q1 2025, up from $7.1 million in Q4 2024 and $5.8 million in Q1 2024, representing a 35% year-over-year increase. This growth was primarily driven by higher net interest income and lower noninterest expenses compared to the previous quarter.

Net Interest Income and Margin

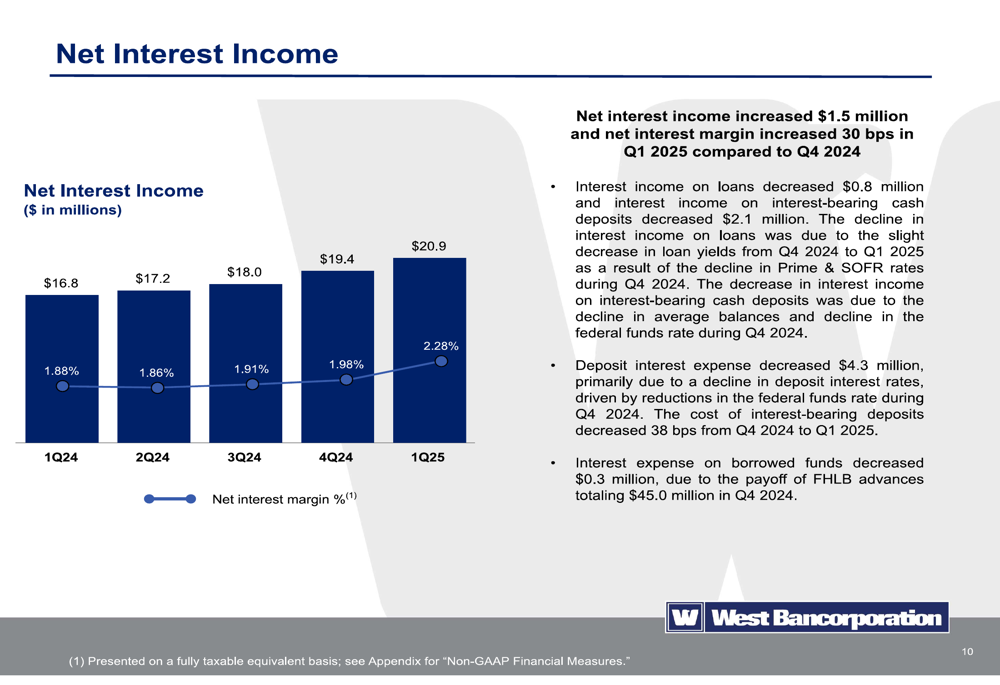

The most significant improvement in West Bancorporation’s performance came from its net interest income and margin, which have been steadily increasing over the past five quarters.

The following chart illustrates this positive trend:

Net interest income reached $20.9 million in Q1 2025, increasing by $1.5 million or 7.7% from Q4 2024, and by $4.1 million or 24.4% compared to Q1 2024. More importantly, the net interest margin expanded to 2.28% in Q1 2025, a 30 basis point improvement from the previous quarter and 40 basis points higher than the same period last year.

This margin expansion appears to be driven by decreasing funding costs, which fell to 3.25% in Q1 2025 from 3.57% in Q4 2024, while loan yields remained relatively stable at 5.52%.

Loan and Deposit Trends

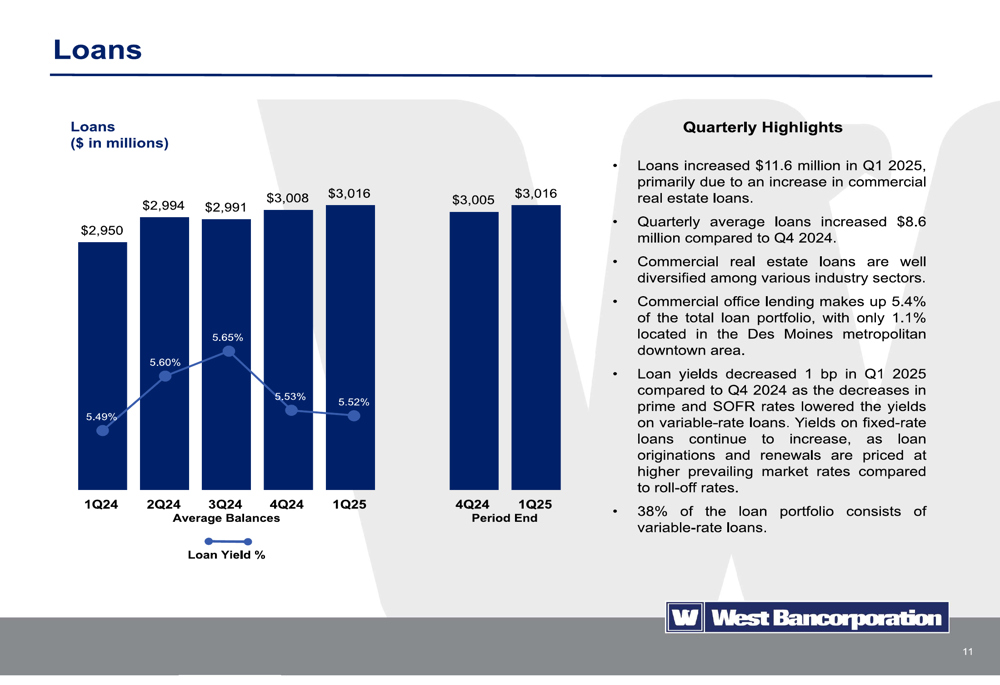

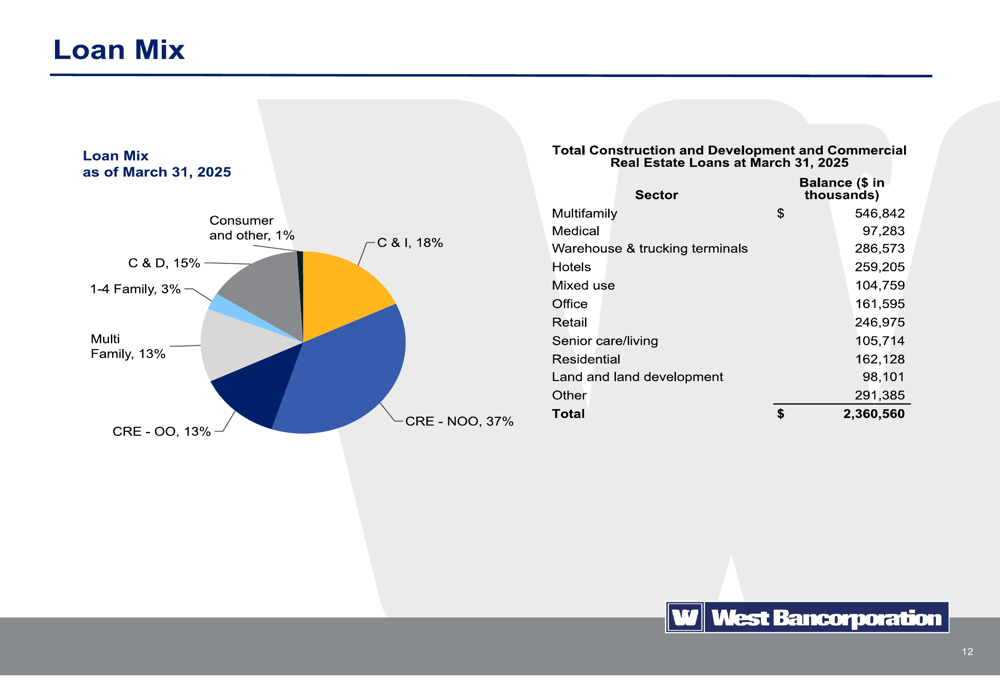

West Bancorporation’s loan portfolio continued to show modest growth, increasing by $11.6 million in Q1 2025 to reach $3.016 billion.

The following chart shows the loan growth trend over the past five quarters:

The company’s loan portfolio remains well-diversified, with commercial real estate loans representing the largest segment. Commercial office lending, an area of concern for many banks in the current market environment, makes up only 5.4% of the total loan portfolio, limiting exposure to this potentially volatile sector.

The loan mix as of March 31, 2025, shows a balanced approach to commercial lending:

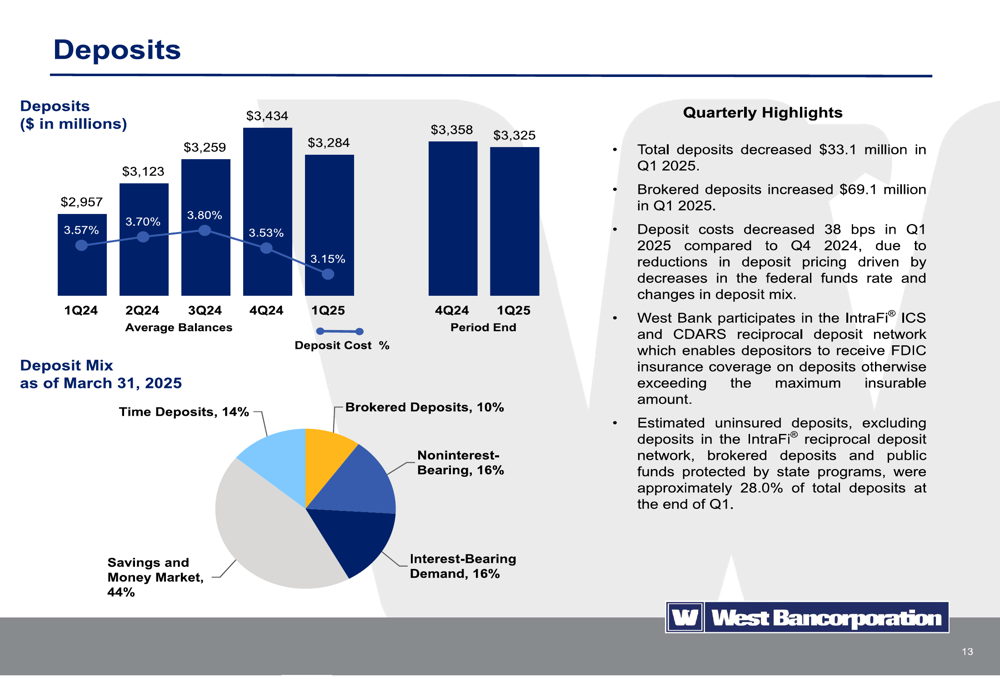

On the funding side, total deposits decreased by $33.1 million in Q1 2025 to $3.284 billion, while brokered deposits increased by $69.1 million. However, deposit costs decreased significantly by 38 basis points to 3.15%, contributing to the overall improvement in net interest margin.

The deposit composition and trends are illustrated in the following chart:

Credit Quality and Risk Management

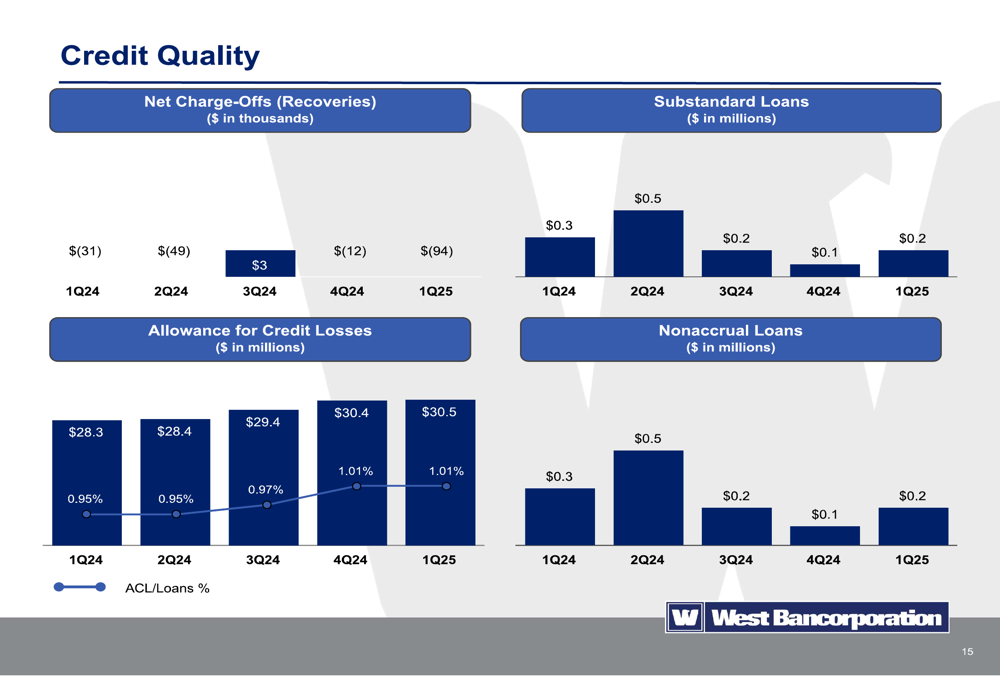

West Bancorporation continues to demonstrate exceptional credit quality, with minimal non-performing assets and consistent loan loss reserves. The allowance for credit losses stood at $30.5 million as of March 31, 2025, representing 1.01% of total loans.

The following chart highlights the company’s strong credit metrics:

The company reported net recoveries of $94 thousand in Q1 2025, compared to net recoveries of $12 thousand in Q4 2024. Substandard loans remained low at $8.1 million, representing just 0.27% of the total loan portfolio.

This strong credit performance reflects West Bancorporation’s disciplined approach to risk management, which includes a centralized committee structure and regular commercial real estate stress testing. The company employs 30 high-quality commercial bankers with an average of 21 years of commercial banking experience, contributing to its strong credit culture.

Strategic Positioning and Outlook

West Bancorporation continues to execute its strategy of conservative organic growth with successful lift-out strategies. The company has a strong presence in the Des Moines metropolitan area since 1893 and has expanded into Minnesota markets including Rochester, St. Cloud, Mankato, and Owatonna.

In 2024, the company opened a new corporate headquarters building in West Des Moines, Iowa, reinforcing its commitment to its home market. West Bancorporation also emphasized its community involvement, with employees volunteering over 8,200 hours of community service in 2024, while the West Bancorporation Foundation and West Bank provided over $450,000 in philanthropic contributions to more than 160 organizations.

Building on the momentum from Q4 2024, when the company beat analyst expectations with an EPS of $0.42 versus a forecasted $0.33, West Bancorporation appears well-positioned to continue its improved performance throughout 2025. The company’s focus on relationship banking, strong credit quality, and efficient operations should continue to support profitability as it navigates the evolving interest rate environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.