BitMine increases ethereum holdings to $6.6 billion, adds 373,000 tokens

Introduction & Market Context

Western Midstream Partners LP (NYSE:WES) released its second-quarter 2025 earnings presentation on August 6, 2025, highlighting record quarterly performance and strategic growth initiatives. The company’s stock closed at $40.33, up 1.38% on the day, continuing the positive momentum seen after its Q1 results when the stock rose 2.7% despite missing earnings expectations.

The midstream operator, which is 44.7% owned by Occidental Petroleum (NYSE:OXY), maintains a market capitalization of approximately $15 billion and continues to position itself as a leading provider of gathering, processing, and transportation services across multiple U.S. basins.

Quarterly Performance Highlights

Western Midstream reported record second-quarter 2025 Adjusted EBITDA of $618 million, representing a 4% increase from the first quarter. This growth was supported by increased throughput volumes across all product categories.

As shown in the following performance highlights chart, the company achieved solid sequential growth in all key operational metrics:

Natural gas throughput reached 5.4 Bcf/d, up 3% quarter-over-quarter, while crude oil and NGLs throughput increased by 6% to 543 MBbls/d. Produced water throughput grew 4% to 1,242 MBbls/d. These improvements represent a significant turnaround from Q1 2025, when the company experienced throughput declines as noted in its previous earnings report.

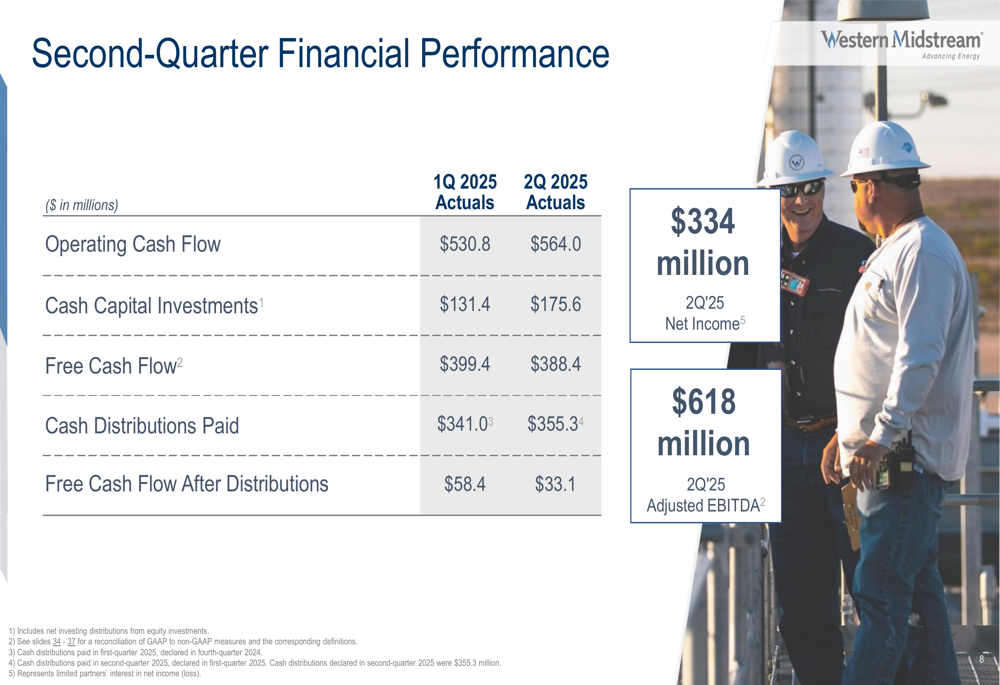

The financial performance for Q2 2025 showed mixed results, with operating cash flow increasing to $564.0 million from $530.8 million in Q1, while free cash flow decreased slightly to $388.4 million from $399.4 million due to higher capital investments:

Cash distributions paid to unitholders increased to $355.3 million from $341.0 million in the previous quarter, reflecting the company’s commitment to returning capital to investors. However, free cash flow after distributions decreased to $33.1 million from $58.4 million in Q1 2025.

Strategic Initiatives

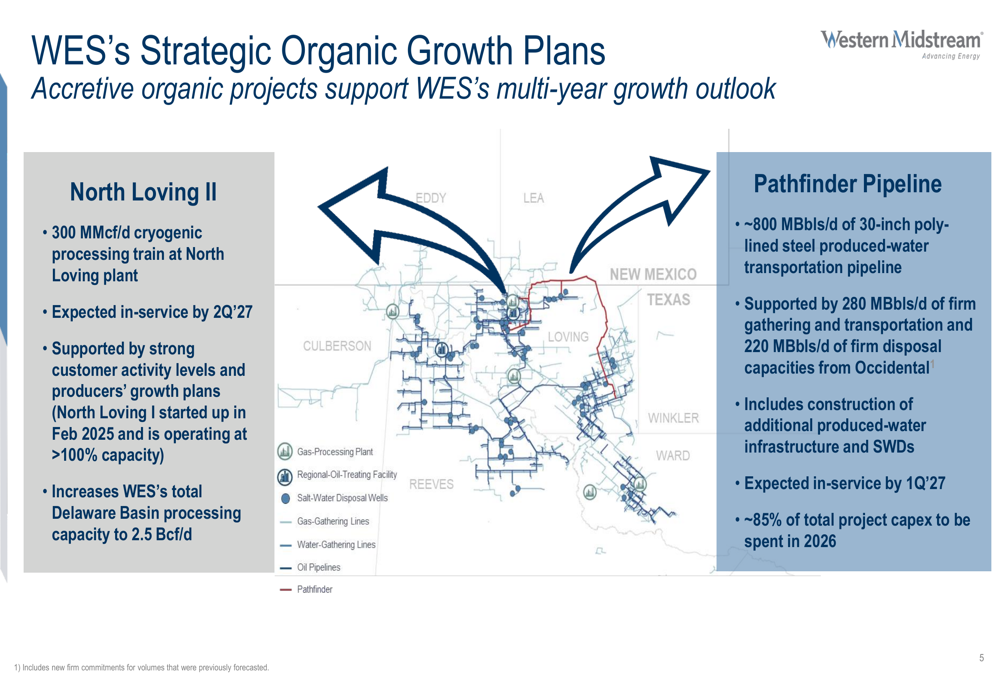

Western Midstream outlined two major strategic growth projects during its presentation: the North Loving II cryogenic processing train and the Pathfinder Pipeline. These initiatives are designed to expand the company’s capacity and capabilities in the Delaware Basin, one of its core operating areas.

The following slide details these strategic organic growth plans:

The North Loving II project includes a 300 MMcf/d cryogenic processing train at the North Loving plant, expected to be in service by Q2 2027. This expansion will increase Western Midstream’s total Delaware Basin processing capacity to 2.5 Bcf/d, supporting customer activity and producers’ growth plans in the region.

The Pathfinder Pipeline represents a significant investment in produced-water infrastructure, featuring an 800 MBbls/d capacity 30-inch poly-lined steel transportation pipeline. Supported by firm commitments from Occidental, the project includes 280 MBbls/d of firm gathering and transportation capacity and 220 MBbls/d of firm disposal capacities. The pipeline is expected to be in service by Q1 2027, with approximately 85% of the total project capital expenditures to be spent in 2026.

Additionally, Western Midstream announced an agreement to acquire Aris Water Solutions, further strengthening its position in the water management segment of the midstream sector.

Financial Outlook & Guidance

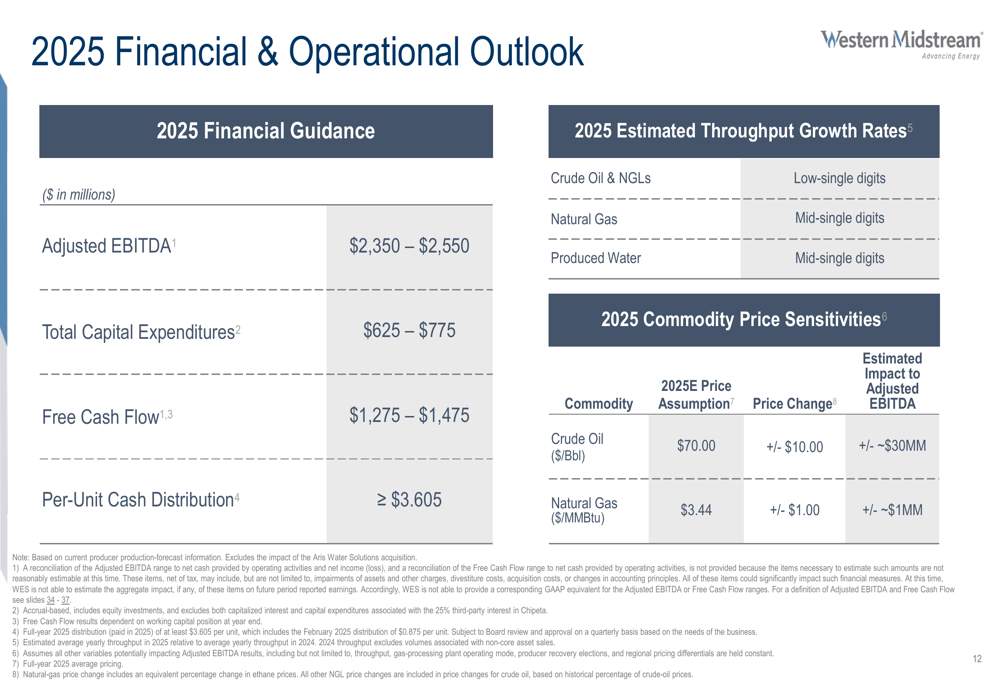

Western Midstream maintained its 2025 financial guidance, projecting Adjusted EBITDA between $2,350 million and $2,550 million, total capital expenditures of $625-$775 million, and free cash flow of $1,275-$1,475 million. The company also committed to a per-unit cash distribution of at least $3.605 for the year.

The following chart details the company’s 2025 financial and operational outlook:

For 2025, Western Midstream expects low-single-digit growth for crude oil and NGLs throughput, and mid-single-digit growth for both natural gas and produced water throughput. The company’s sensitivity analysis indicates that a $10.00 change in crude oil price from the $70.00 assumption would impact Adjusted EBITDA by approximately $30 million, while a $1.00 change in natural gas price from the $3.44 assumption would affect Adjusted EBITDA by approximately $1 million.

Western Midstream’s capital allocation strategy emphasizes expansion opportunities while maintaining net leverage below 3.0x. The company plans to allocate 66% of its 2025 capital expenditures toward expansion projects, including $60 million for the North Loving Train II in the Delaware Basin.

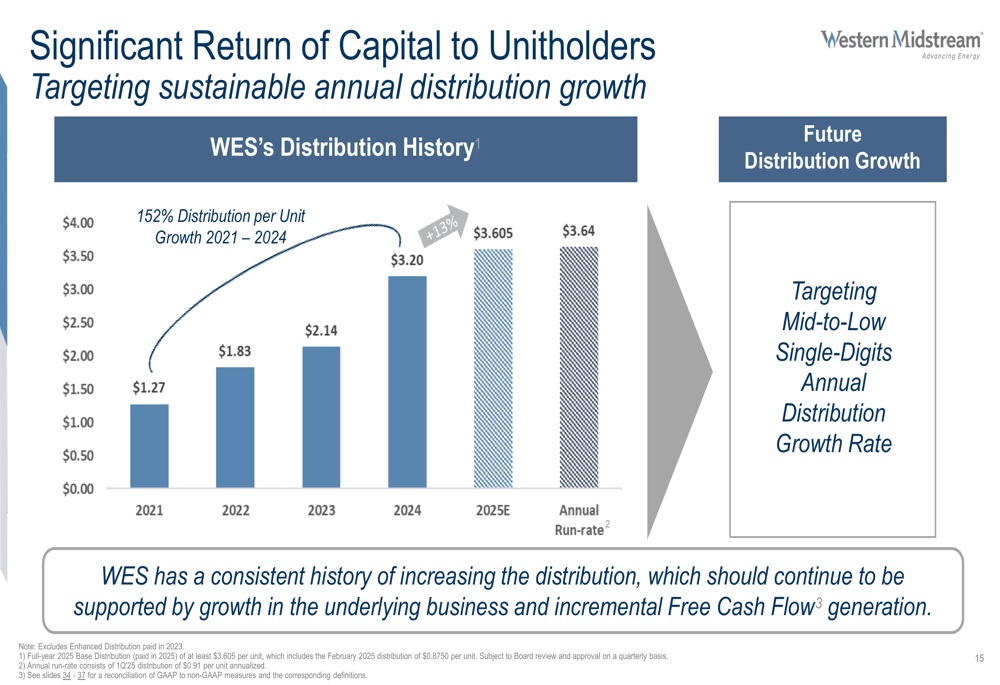

The company has demonstrated a strong commitment to returning capital to unitholders, with distribution per unit growing 152% from 2021 to 2024. For 2025, Western Midstream is targeting mid-to-low single-digit annual distribution growth:

Competitive Industry Position

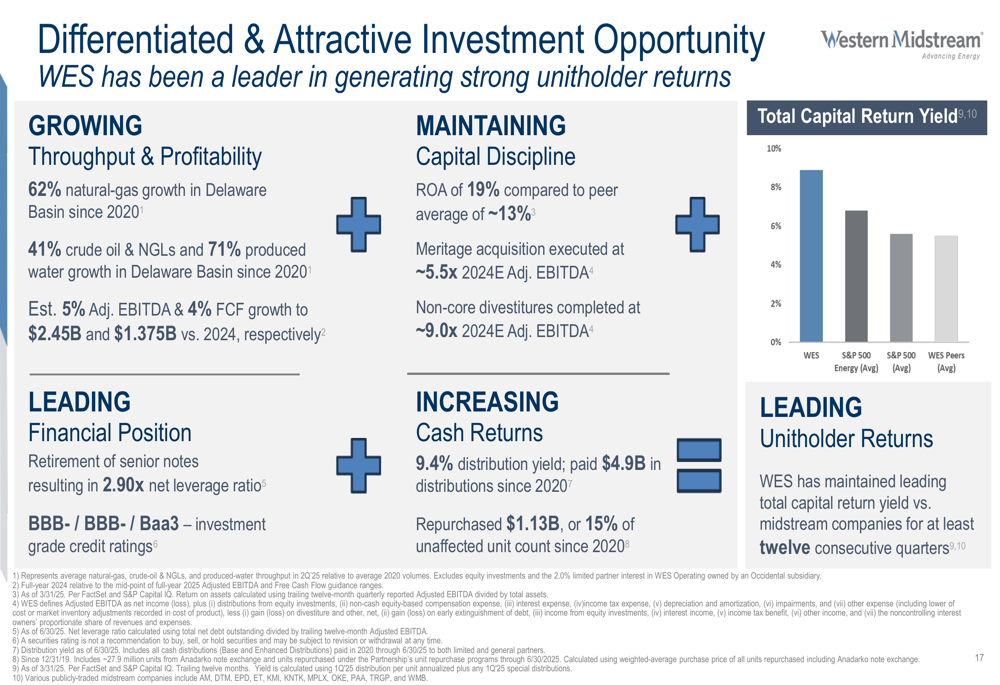

Western Midstream positions itself as a differentiated investment opportunity in the midstream sector, highlighting its growing throughput and profitability, capital discipline, and increasing cash returns to unitholders.

The company’s presentation emphasizes its competitive advantages:

With a return on assets of 19% compared to a peer average of approximately 13%, Western Midstream demonstrates strong operational efficiency. The company has paid $4.9 billion in distributions since 2020 and repurchased $1.13 billion in units, maintaining a leading total capital return yield compared to midstream peers for twelve consecutive quarters.

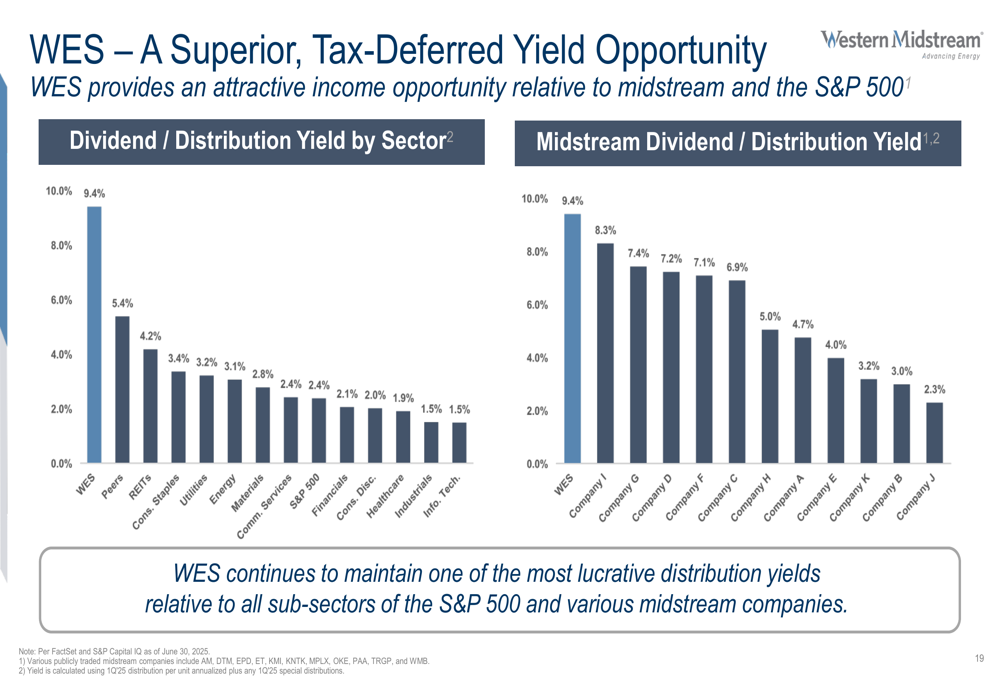

Western Midstream’s distribution yield of 9.4% stands out as particularly attractive when compared to other sectors and midstream companies:

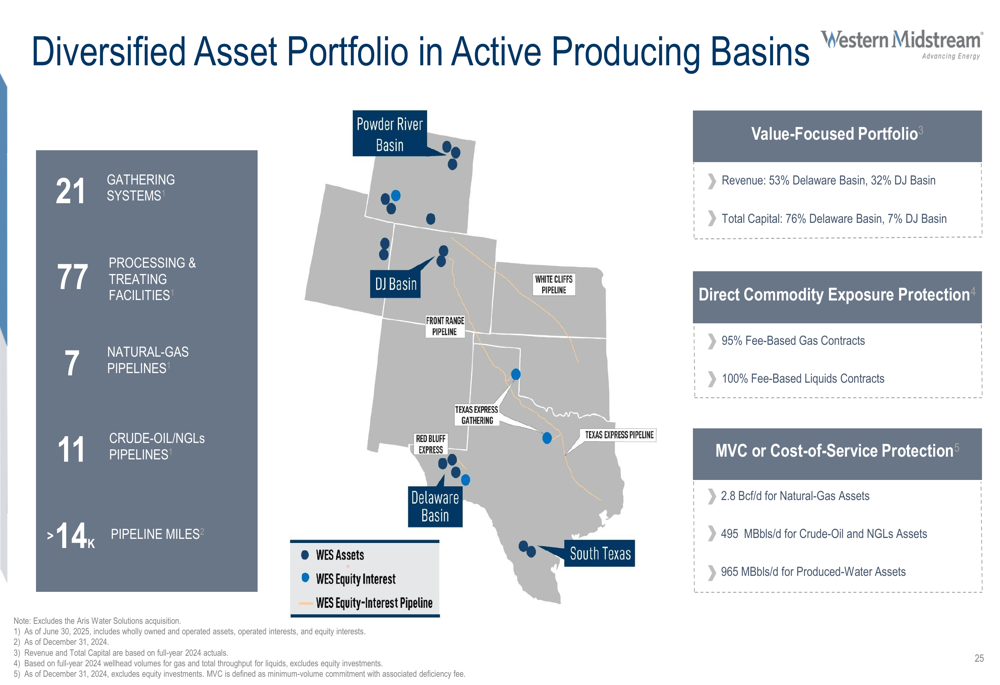

The company’s diversified asset portfolio spans multiple producing basins, providing operational stability and growth opportunities:

Western Midstream operates 21 gathering systems, 77 processing and treating facilities, 7 natural gas pipelines, and 11 crude-oil/NGLs pipelines across more than 14,000 pipeline miles. The Delaware Basin contributes 53% of revenue, while the DJ Basin accounts for 32%. The company’s contracts are predominantly fee-based, with 95% fee-based gas contracts and 100% fee-based liquids contracts, providing revenue stability.

Forward-Looking Statements

Looking ahead, Western Midstream is focused on executing its expansion projects while maintaining financial discipline. The North Loving II and Pathfinder Pipeline projects represent significant growth opportunities, with most of the capital expenditures planned for 2026.

The company expects continued throughput growth across all product types in 2025, supported by producer activity in its core operating areas. Western Midstream’s strong contract position, with minimum volume commitments or cost-of-service protection for substantial portions of its capacity, provides revenue visibility and stability.

While the company maintains an optimistic outlook, investors should note that commodity price fluctuations could impact financial results, as indicated in the sensitivity analysis. Additionally, the slight decrease in free cash flow after distributions in Q2 2025 suggests that balancing growth investments with shareholder returns may present challenges in the near term.

Nevertheless, Western Midstream’s record Q2 2025 performance, strategic growth initiatives, and competitive position in key basins support its ability to continue delivering value to unitholders through both growth and distributions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.