Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Westwing Group AG (XETRA:ETR:WEW) presented its Q1 2025 results on May 8, showing significant profitability improvements despite a slight revenue decline. The home and living e-commerce company’s stock rose 1.87% to €7.62 following the presentation, reflecting investor confidence in the company’s strategic direction and improved margins.

The premium home furnishings retailer continues to execute its three-step value creation plan, now focusing on the third phase of "Scaling with Operating Leverage" after successfully completing its turnaround and platform-building phases. This comes amid challenging market conditions in the European home and living sector.

Quarterly Performance Highlights

Westwing reported a modest 1% year-over-year revenue decline in Q1 2025, attributed primarily to shifts in product assortment as the company continues to emphasize premium offerings. Despite this top-line challenge, profitability metrics showed remarkable improvement.

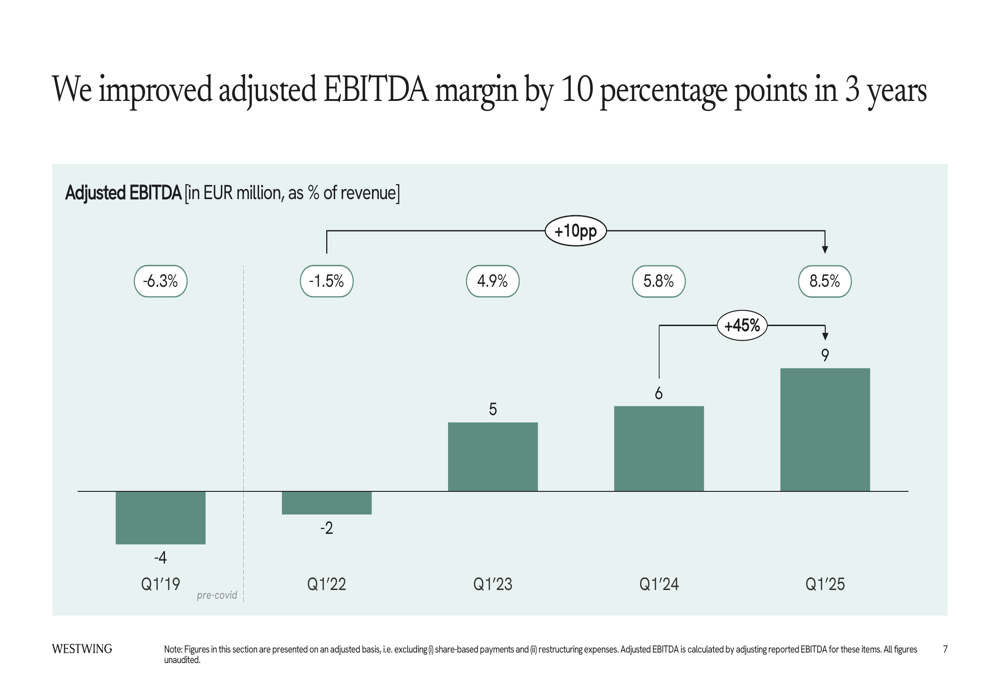

As shown in the following chart of adjusted EBITDA development:

The company achieved an adjusted EBITDA of €9 million in Q1 2025, representing an 8.5% margin – a significant improvement from 5.8% in Q1 2024 and a dramatic turnaround from negative territory in earlier years. This 10 percentage point improvement over three years demonstrates the effectiveness of Westwing’s strategic initiatives.

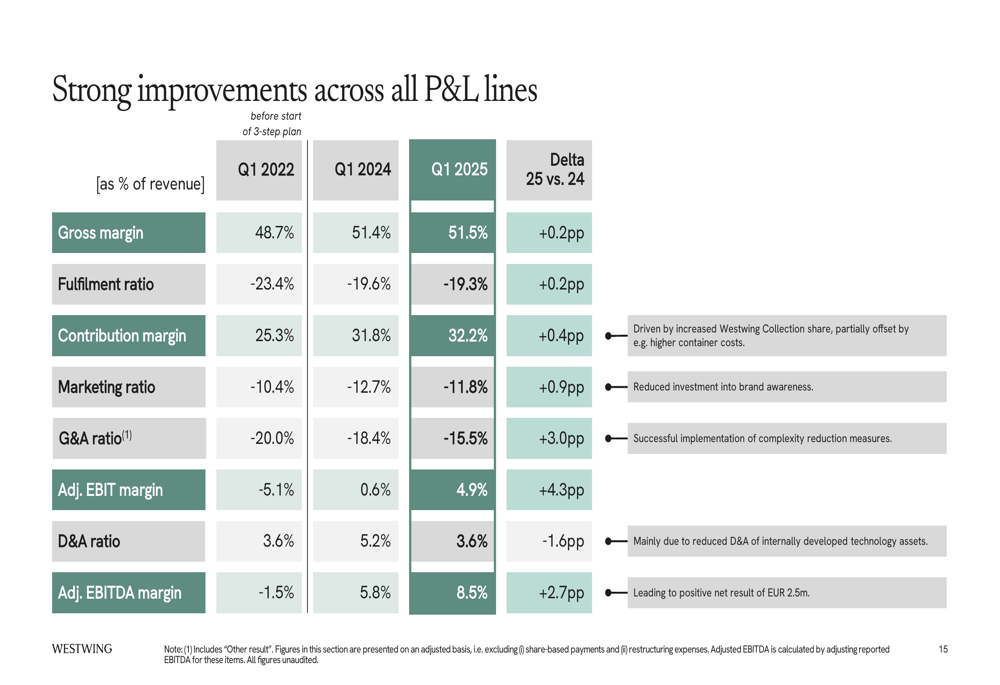

The company’s P&L metrics show improvements across virtually all lines:

Particularly notable is the adjusted EBIT margin, which improved to 4.9% in Q1 2025 from 0.6% in Q1 2024, driven by better G&A cost management and marketing efficiency. The company maintained its strong gross margin at 51.5%, nearly identical to Q1 2024’s 51.4%.

Strategic Initiatives

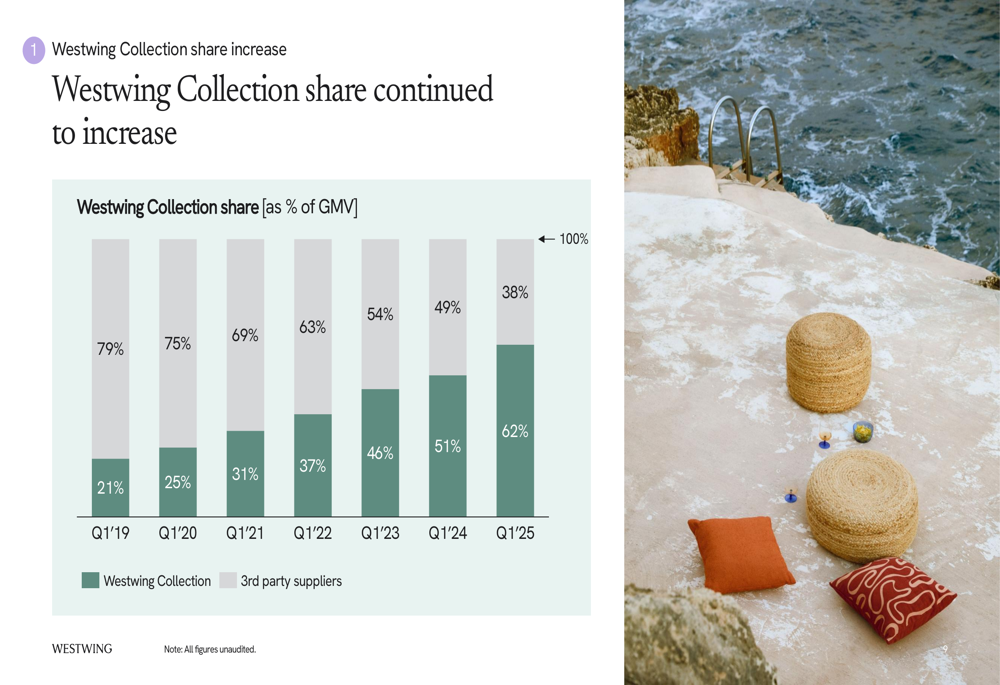

A cornerstone of Westwing’s strategy is increasing the share of its own-brand products. The Westwing Collection has grown dramatically as a percentage of Gross Merchandise Value (GMV):

This shift to 62% Westwing Collection share (up from 51% a year ago) has been instrumental in maintaining gross margins and strengthening brand identity. The company’s own products typically carry higher margins than third-party merchandise.

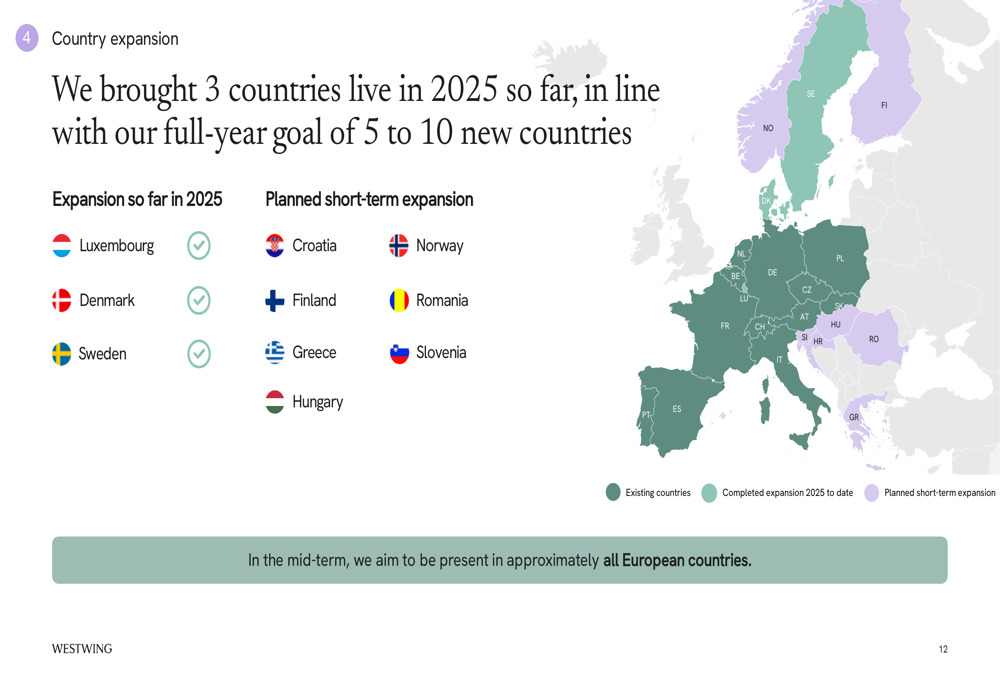

Geographic expansion represents another key growth vector for Westwing. The company has already launched in three new countries in 2025 – Luxembourg, Denmark, and Sweden – with plans to enter 5-10 new markets this year:

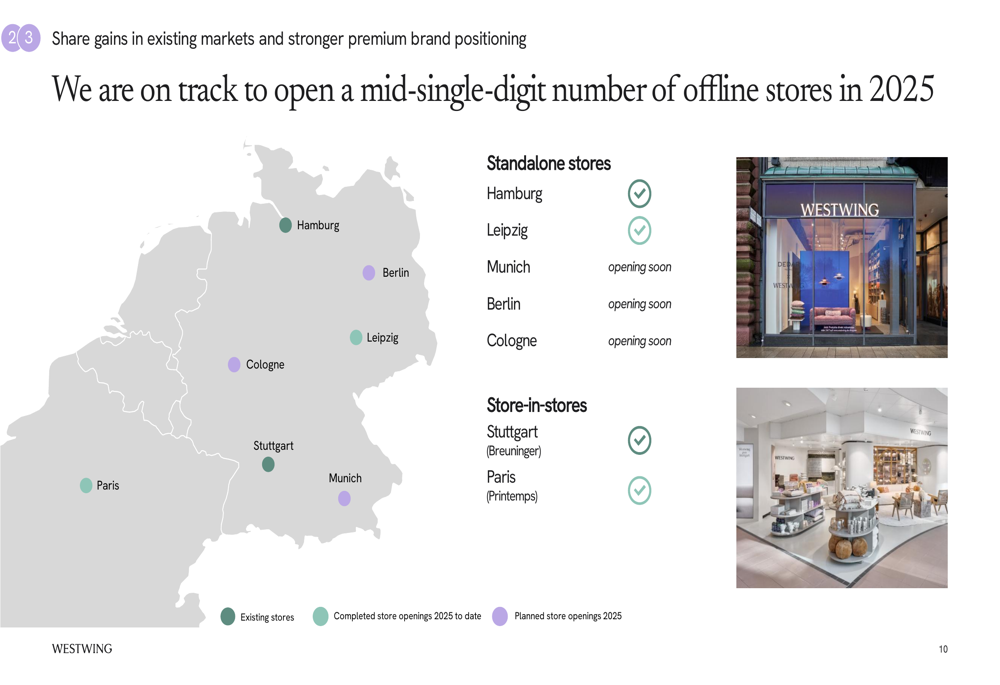

Complementing its online presence, Westwing continues to expand its physical retail footprint with both standalone stores and store-in-store concepts:

The company recently opened a new store-in-store at Printemps in Paris, a prestigious high-end department store, reinforcing Westwing’s premium positioning.

Detailed Financial Analysis

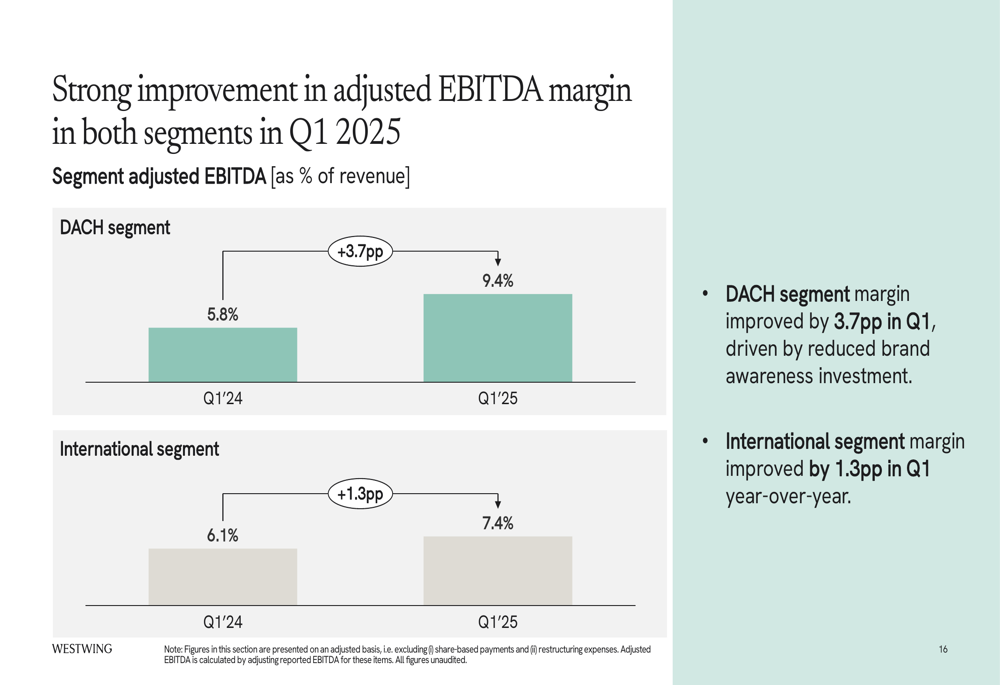

Segment performance shows strong profitability improvements in both regions. The DACH segment (Germany, Austria, Switzerland) saw its adjusted EBITDA margin increase by 3.7 percentage points to 9.4%, while the International segment improved by 1.3 percentage points to 7.4%:

The DACH segment, representing 56% of total revenue, grew by 1% year-over-year, while the International segment declined by 4%, reflecting the more significant impact of product assortment changes in those markets.

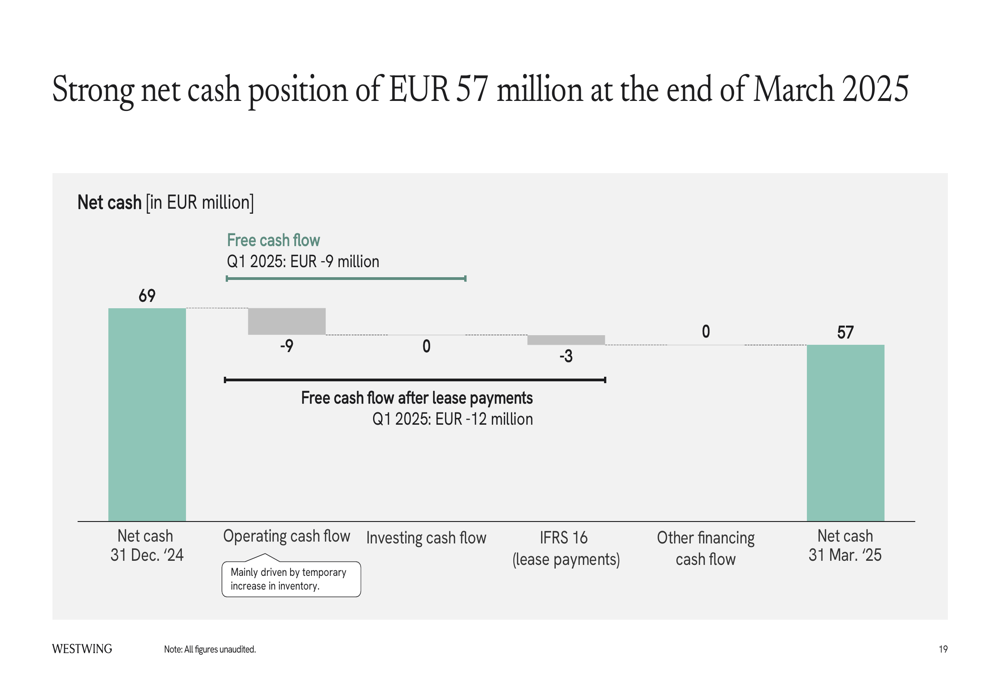

Westwing’s balance sheet remains robust with a net cash position of €57 million at the end of Q1 2025, though this represents a decrease from €69 million at year-end 2024:

The free cash flow of -€9 million in Q1 was primarily attributed to a temporary increase in inventory. Net working capital stood at -€2 million, compared to -€18 million a year earlier.

Capital expenditure decreased significantly to €2 million (2.0% of revenue) in Q1 2025 from €5 million (4.9%) in Q1 2024, reflecting fewer logistics center leasing contract changes and reduced investments in internally developed tech assets.

Forward-Looking Statements

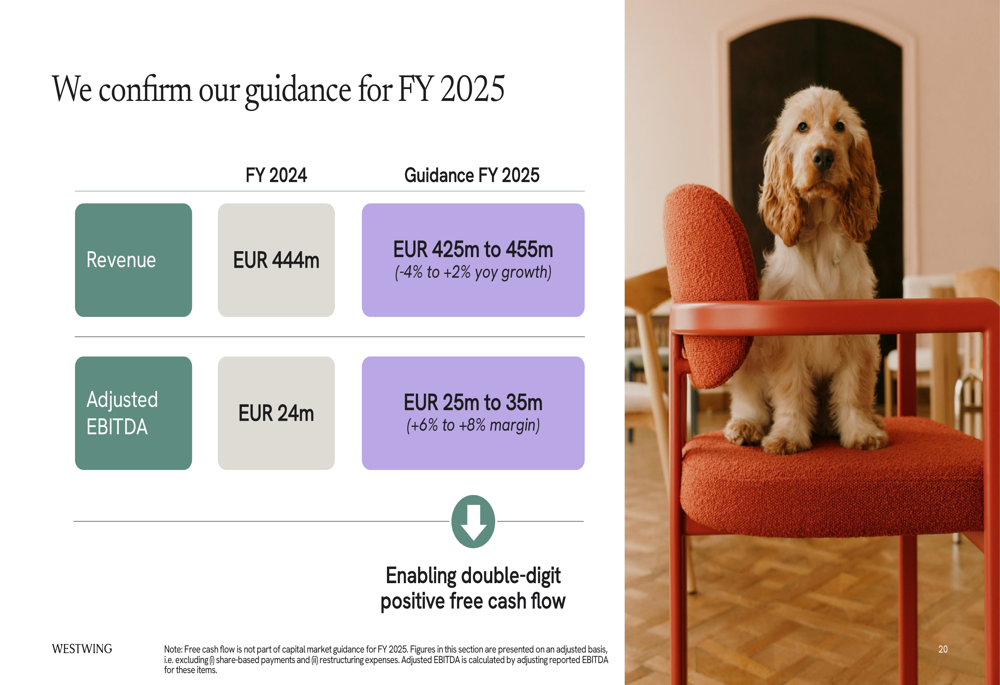

Westwing confirmed its full-year 2025 guidance:

The company expects revenue between €425 million and €455 million, representing growth between -4% and +2% year-over-year. Adjusted EBITDA is projected at €25-35 million, translating to a 6-8% margin.

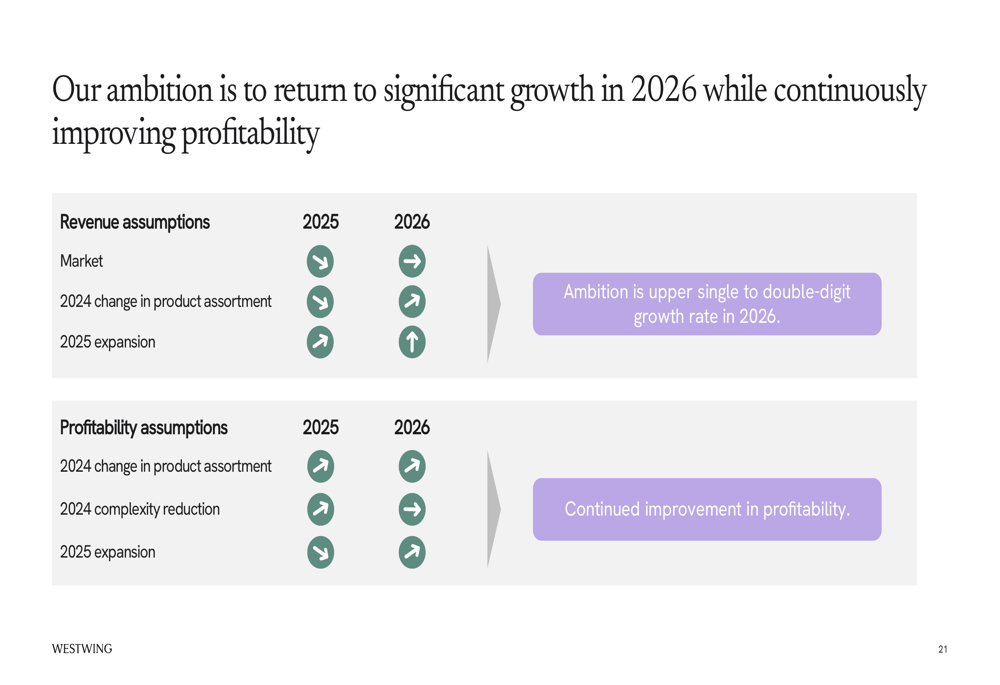

For the longer term, Westwing’s ambitions include:

The company targets upper single to double-digit growth rates in 2026 with continued profitability improvements, aiming for an adjusted EBITDA margin path to 10%+ in the medium term.

The investment case for Westwing centers on several key pillars:

Management emphasizes Westwing’s unique customer value proposition, market potential in the €130 billion premium home and living segment, brand strength, margin potential, and solid balance sheet as key factors supporting future growth.

CEO Andreas Hernig highlighted the company’s strategic direction during the earnings call, stating: "We are developing the superbrand in design with high loyalty and true potential to grow further." CFO Sebastian Vestricht added that the company’s "ambition is to return to significant growth in 2026 while continuously improving profitability."

While Westwing faces challenges including dampened consumer sentiment and intense competition in the premium design market, its Q1 2025 results demonstrate that the company’s focus on profitability and strategic expansion is yielding positive results despite modest top-line performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.