Joby Aviation closes $591 million stock offering with full underwriter option

Introduction & Market Context

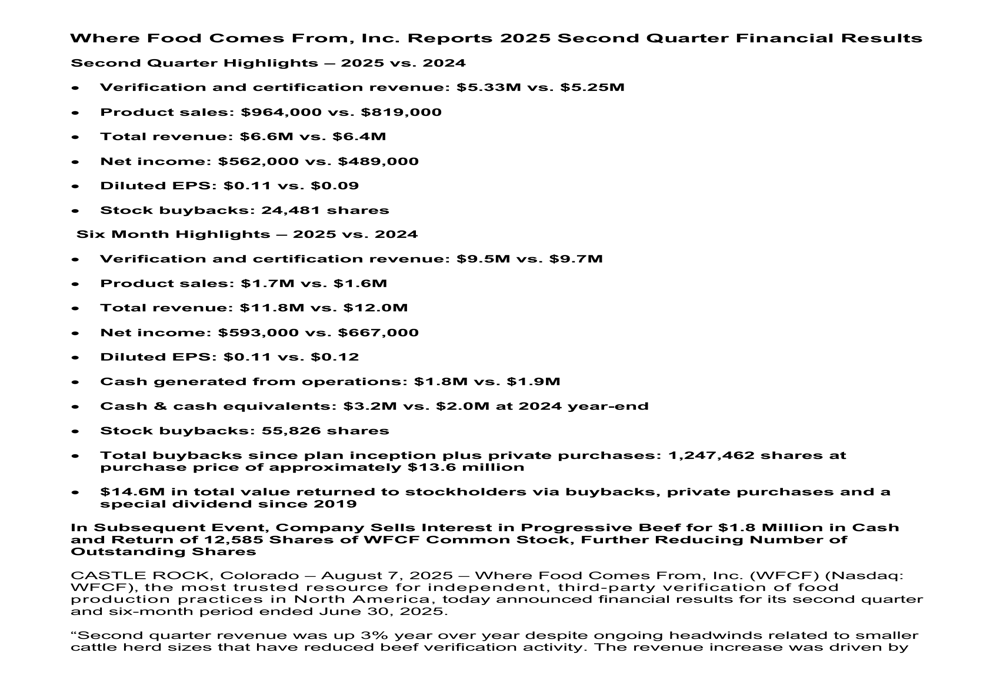

Where Food Comes From Inc. (OTCQB:WFCF), a leading provider of certification, verification, and traceability solutions for the agriculture and food industry, presented its second quarter 2025 financial results on August 7, showing modest revenue growth despite ongoing industry challenges. The company’s stock closed at $11.16, down 0.89% on the day, and continues to trade closer to its 52-week low of $9.26 than its high of $13.50.

The presentation highlighted WFCF’s strategic initiatives, including retail expansion and AI investments, alongside a significant divestiture of its Progressive Beef stake, as the company navigates a challenging market environment characterized by tight labor conditions and changing consumer preferences.

Quarterly Performance Highlights

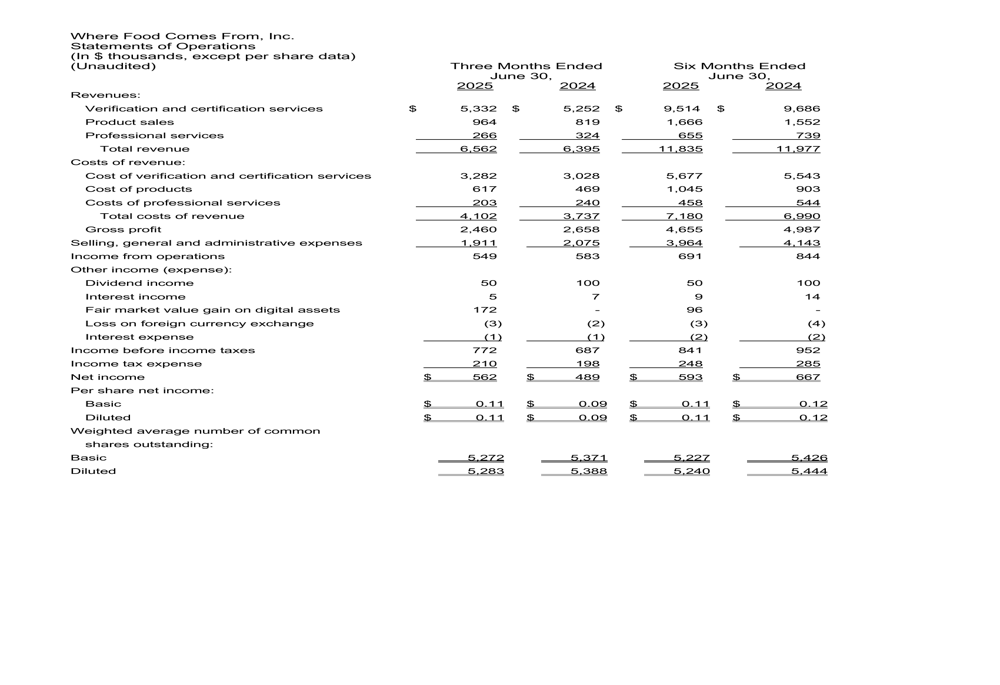

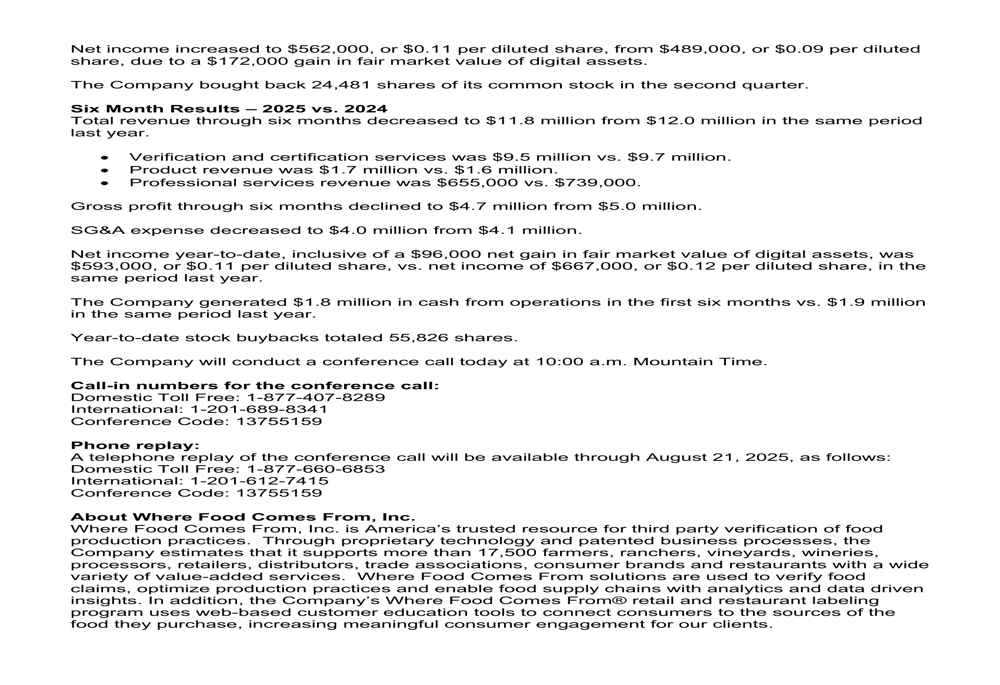

WFCF reported a 3% year-over-year increase in total revenue for Q2 2025, reaching $6.6 million compared to $6.4 million in the same period last year. This growth was primarily driven by modest increases in verification services and more substantial gains in product sales.

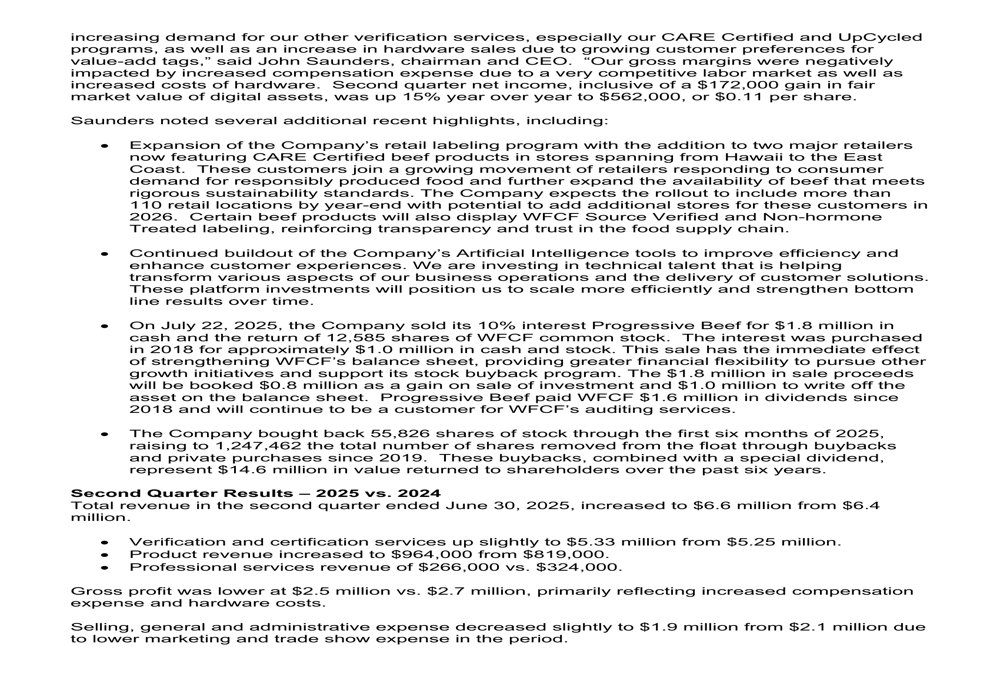

Net income for the quarter showed stronger improvement, rising 15% to $562,000 from $489,000 in Q2 2024. Diluted earnings per share increased to $0.11 from $0.09 in the prior-year period, meeting market expectations.

As shown in the following quarterly financial summary:

The company’s product sales segment demonstrated particularly strong performance, growing to $964,000 from $819,000 in the prior year quarter, representing an 18% increase. Meanwhile, verification and certification services, the company’s core business, saw a more modest 1.5% increase to $5.33 million.

Detailed Financial Analysis

While quarterly results showed improvement, the six-month performance painted a more challenging picture. Total (EPA:TTEF) revenue for the first half of 2025 declined slightly to $11.8 million from $12.0 million in the comparable period of 2024, representing a 1.7% decrease.

The detailed income statement reveals the pressure points in the company’s financial performance:

Gross profit margins contracted in both the quarterly and six-month periods, primarily due to increased compensation expenses and higher hardware costs. For Q2, gross profit decreased to $2.5 million from $2.7 million despite the revenue increase, indicating margin compression. The company did manage to partially offset this through reduced selling, general and administrative expenses, which decreased slightly to $1.9 million from $2.1 million.

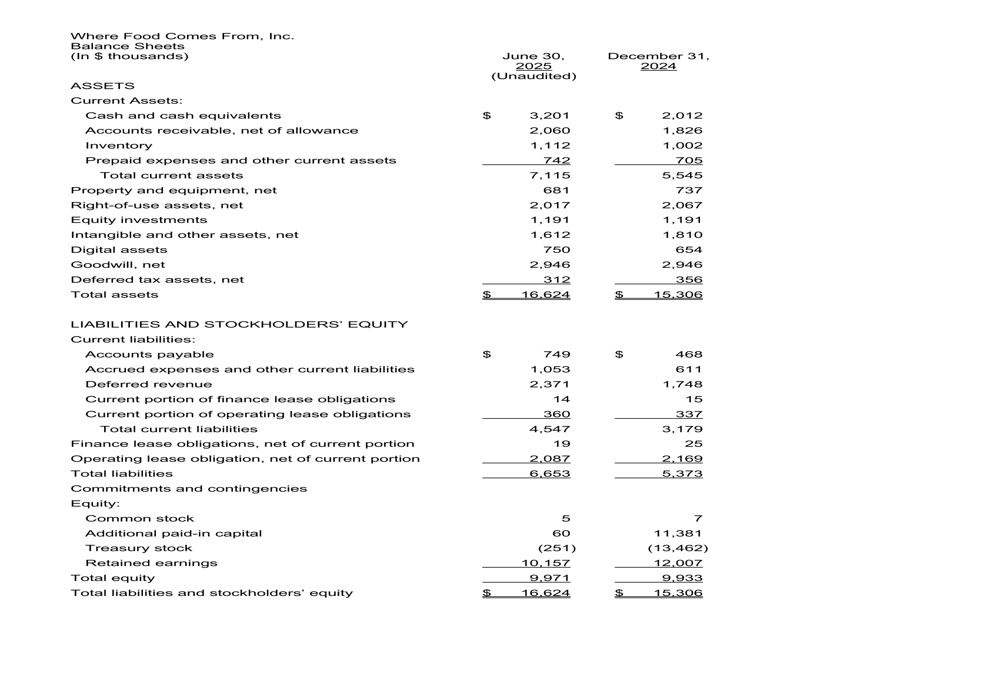

WFCF’s balance sheet showed improvement, with cash and cash equivalents increasing to $3.2 million as of June 30, 2025, compared to $2.0 million at the end of 2024:

This cash position improvement positions the company well for its ongoing strategic initiatives and continued shareholder returns through stock buybacks.

Strategic Initiatives

The presentation highlighted several key strategic developments that could impact WFCF’s future growth trajectory. Most notably, the company announced the sale of its 10% interest in Progressive Beef for $1.8 million in cash and the return of 12,585 shares of WFCF common stock. Management indicated they will book $0.8 million as a gain on sale while writing off $1.0 million.

WFCF also reported progress in its retail expansion featuring CARE Certified beef products:

The company expects to include more than 110 retail locations by year-end, potentially creating a more diversified revenue stream beyond its core verification services. This expansion aligns with growing consumer demand for verified and certified food products.

Additionally, WFCF continues to invest in artificial intelligence tools aimed at improving operational efficiency and enhancing customer experience. These investments may help address the margin pressure from rising compensation costs, though they represent a near-term investment that could impact profitability.

Capital Allocation & Shareholder Returns

WFCF maintained its commitment to returning capital to shareholders, reporting the repurchase of 24,481 shares during Q2 and a total of 55,826 shares in the first half of 2025. Since the inception of its buyback program, the company has repurchased or acquired through private transactions a total of 1,247,462 shares at an approximate cost of $13.6 million.

In total, WFCF has returned approximately $14.6 million to stockholders through buybacks, private purchases, and a special dividend since 2019, demonstrating a consistent focus on shareholder value despite the challenging operating environment.

Forward-Looking Statements

Looking ahead, WFCF management expressed optimism about market share gains driven by consumer preferences for value-added tags and verification services. The company highlighted its unique ability to bundle services, resulting in cost savings and convenience for customers.

The retail expansion of CARE Certified beef products represents a significant growth opportunity, with more than 110 locations expected by year-end. This initiative could provide a more stable revenue stream to complement the company’s core verification business.

However, challenges remain, including continued pressure on gross margins from compensation and hardware costs. The tight labor market was specifically mentioned as an ongoing concern that could impact profitability in future quarters.

The Progressive (NYSE:PGR) Beef divestiture provides additional financial flexibility, with the $1.8 million cash infusion potentially funding further investments in AI capabilities or additional shareholder returns through the buyback program.

As WFCF navigates these opportunities and challenges, investors will be watching closely to see if the company can translate its strategic initiatives into sustained revenue growth and margin improvement in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.