Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

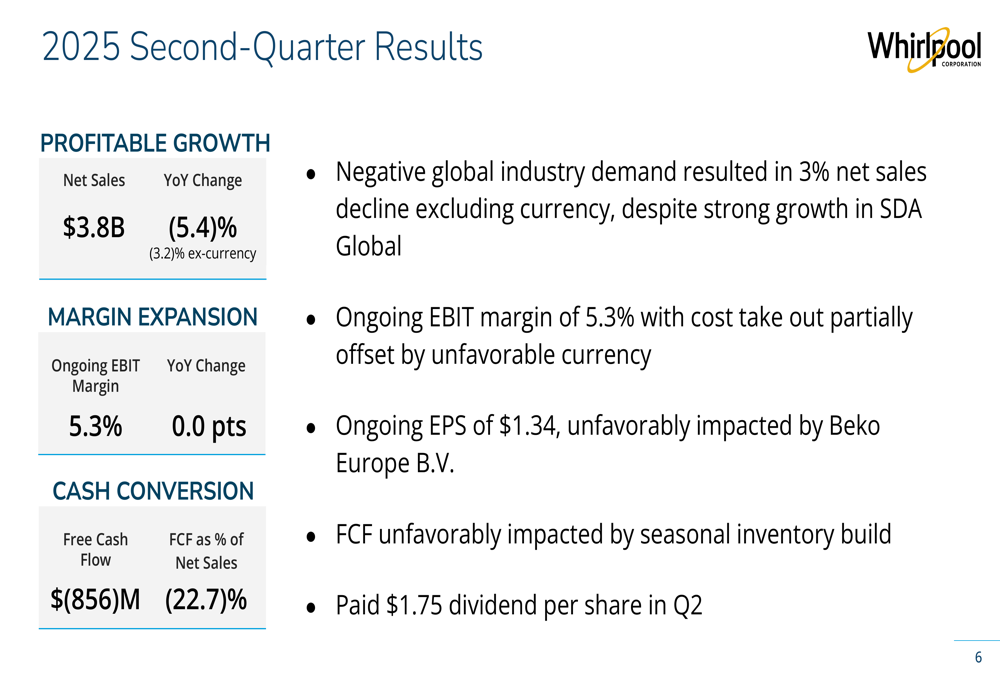

Whirlpool Corporation (NYSE:WHR) presented its second-quarter 2025 earnings results on July 29, 2025, revealing a company maintaining operational stability despite challenging market conditions. The appliance manufacturer reported a 5.4% decline in net sales (3.2% excluding currency effects), while managing to hold its ongoing EBIT margin steady at 5.3% year-over-year.

The company’s stock closed at $71.92 on the day of the earnings release, up 3.14%, though it showed a slight pre-market decline of 0.67% the following day. Trading near its 52-week low of $71.01, Whirlpool shares have declined 34% year-to-date according to available market data, indicating ongoing investor concerns despite the company’s operational resilience.

Quarterly Performance Highlights

Whirlpool reported second-quarter net sales of $3.8 billion, with an ongoing EBIT margin of 5.3% and ongoing earnings per share of $1.34. The company noted that its EPS was unfavorably impacted by Beko Europe B.V., while free cash flow was negatively affected by seasonal inventory build.

As shown in the following quarterly results summary:

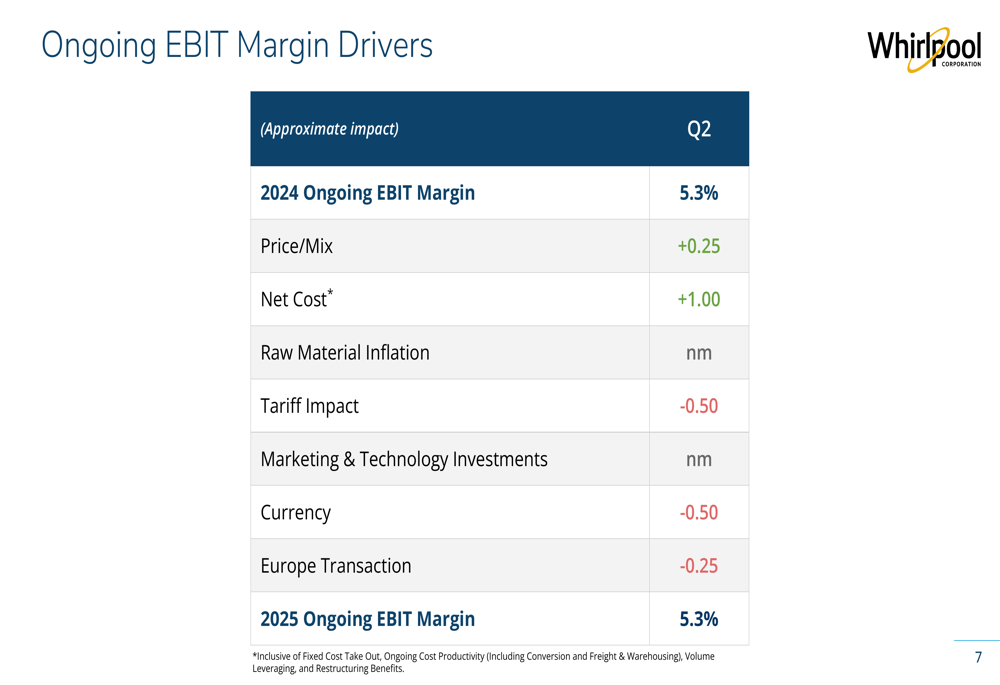

Breaking down the factors affecting EBIT margin, Whirlpool demonstrated that cost reduction initiatives (+1.00 point impact) helped offset negative pressures from tariffs (-0.50), currency (-0.50), and the Europe transaction (-0.25), resulting in a flat year-over-year margin:

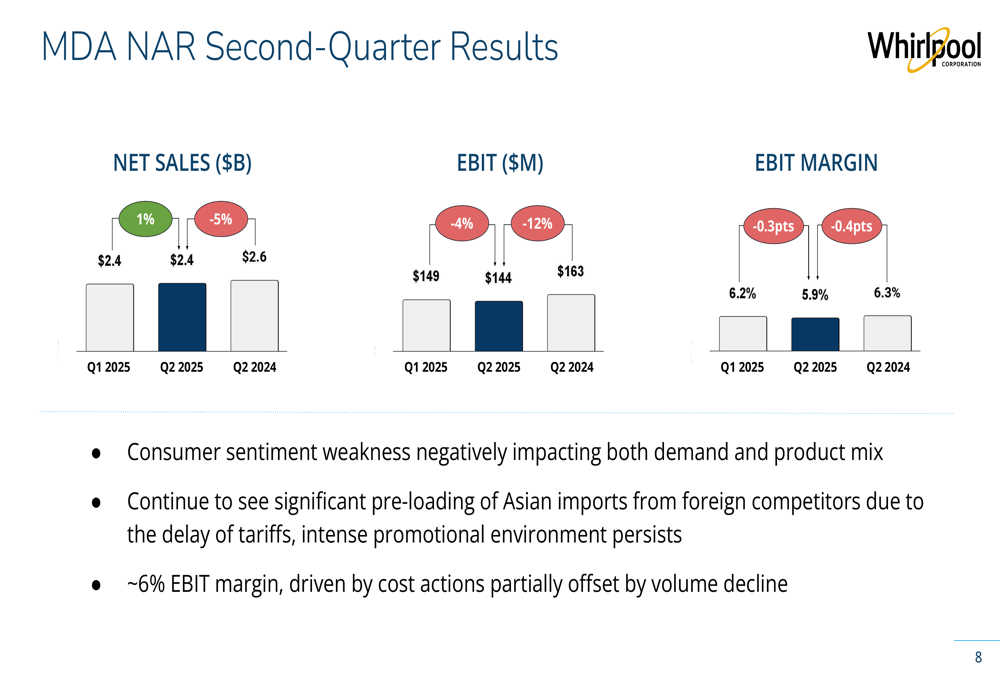

Segment performance varied significantly across regions. North America (NAR), Whirlpool’s largest market, faced headwinds with net sales of $2.4 billion (down 5% year-over-year) and EBIT of $144 million (down 12%), resulting in a 5.9% EBIT margin (down 0.4 percentage points). The company cited consumer sentiment weakness and pre-loading of Asian imports by competitors ahead of tariff implementation as key challenges:

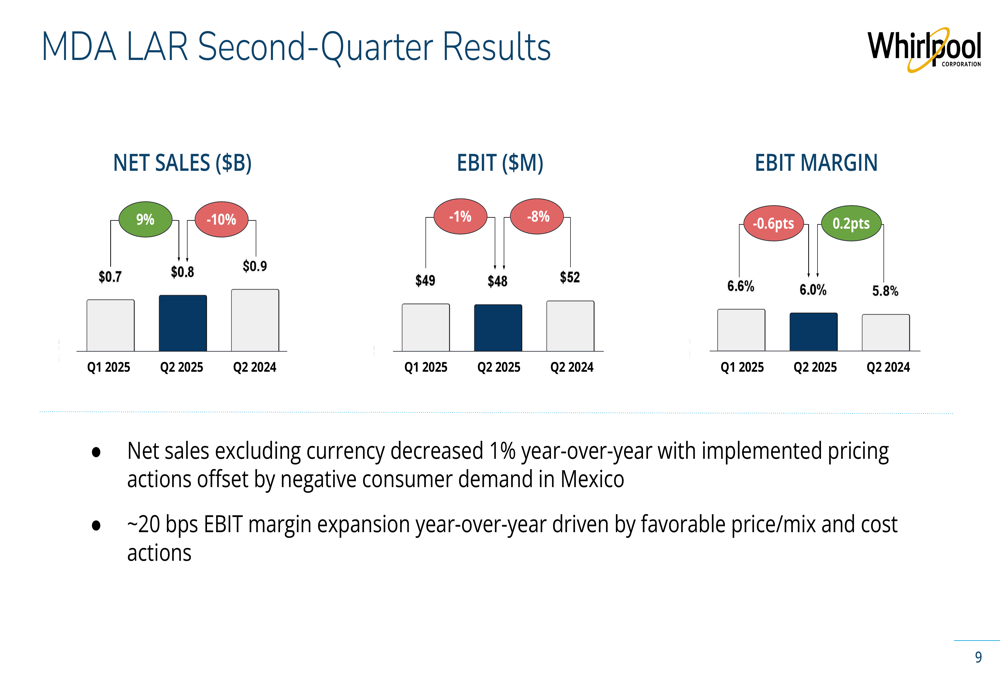

Latin America (LAR) showed resilience with net sales of $0.8 billion (down 10% year-over-year, but only 1% excluding currency) and a slight EBIT margin improvement to 6.0% (up 0.2 percentage points), driven by favorable price/mix and cost actions:

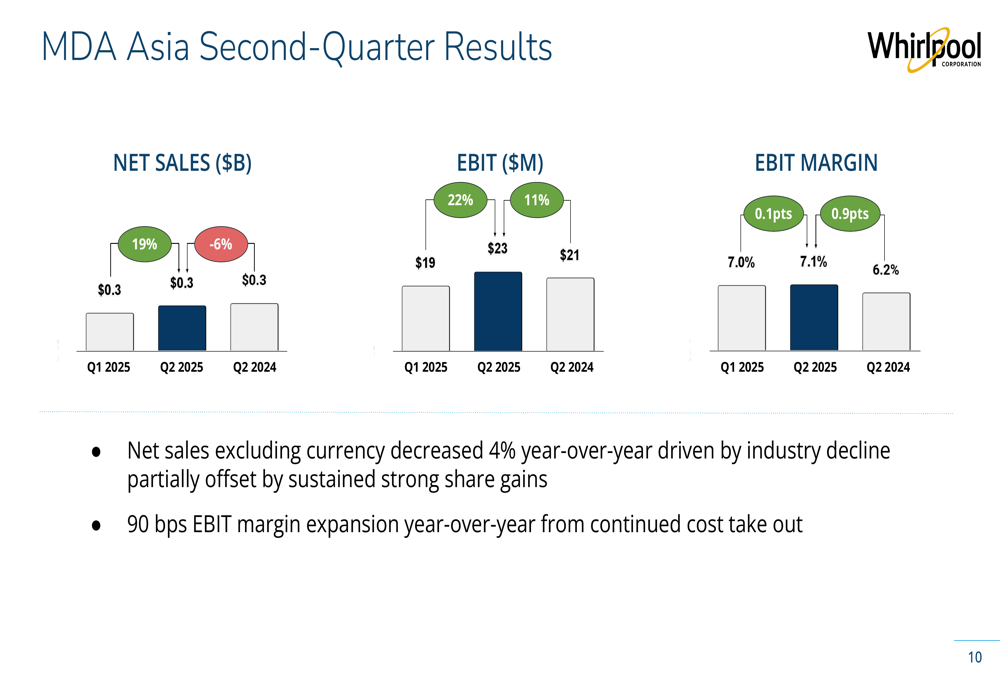

The Asia segment demonstrated strong margin expansion despite sales challenges, with net sales of $0.3 billion (down 6% year-over-year, down 4% excluding currency) but EBIT margin improving to 7.1% (up 0.9 percentage points) thanks to cost reduction initiatives:

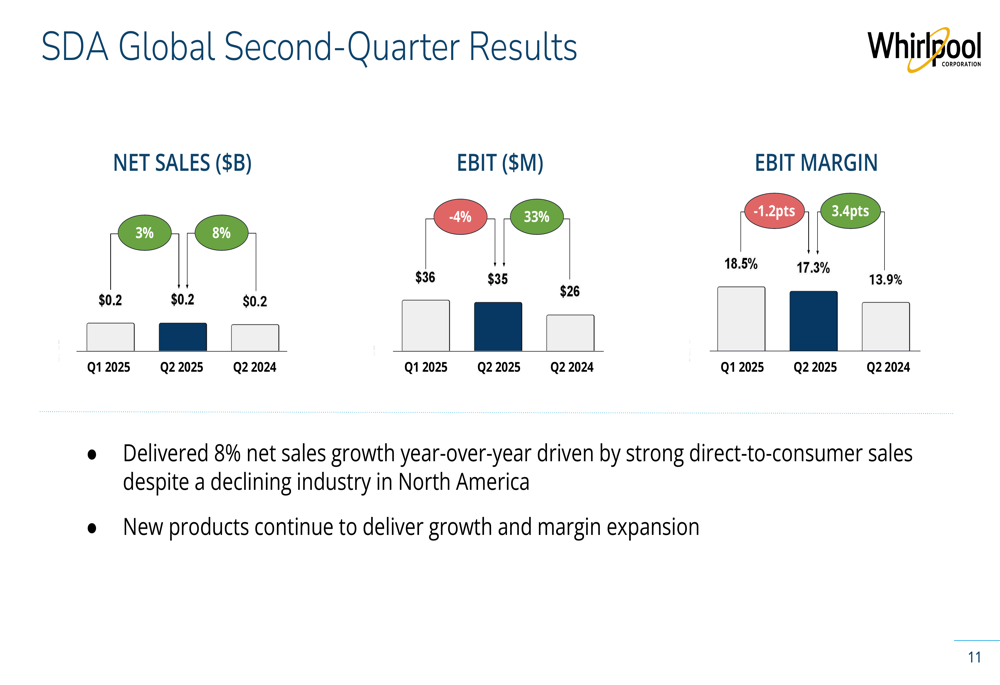

Small Domestic Appliances (SDA) Global emerged as the standout performer, delivering 3% net sales growth year-over-year to $0.2 billion, with an impressive EBIT margin of 17.3% (up 3.4 percentage points) and EBIT growth of 33% to $35 million, driven by strong direct-to-consumer sales and new product introductions:

Strategic Initiatives

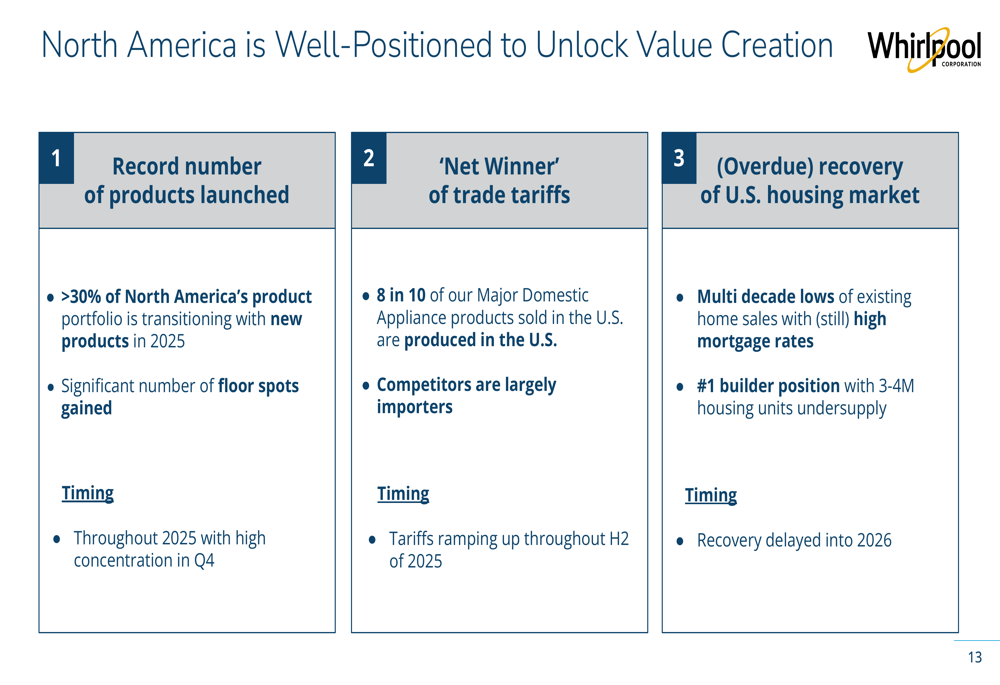

Whirlpool outlined three key catalysts for growth in North America, positioning the company for future value creation:

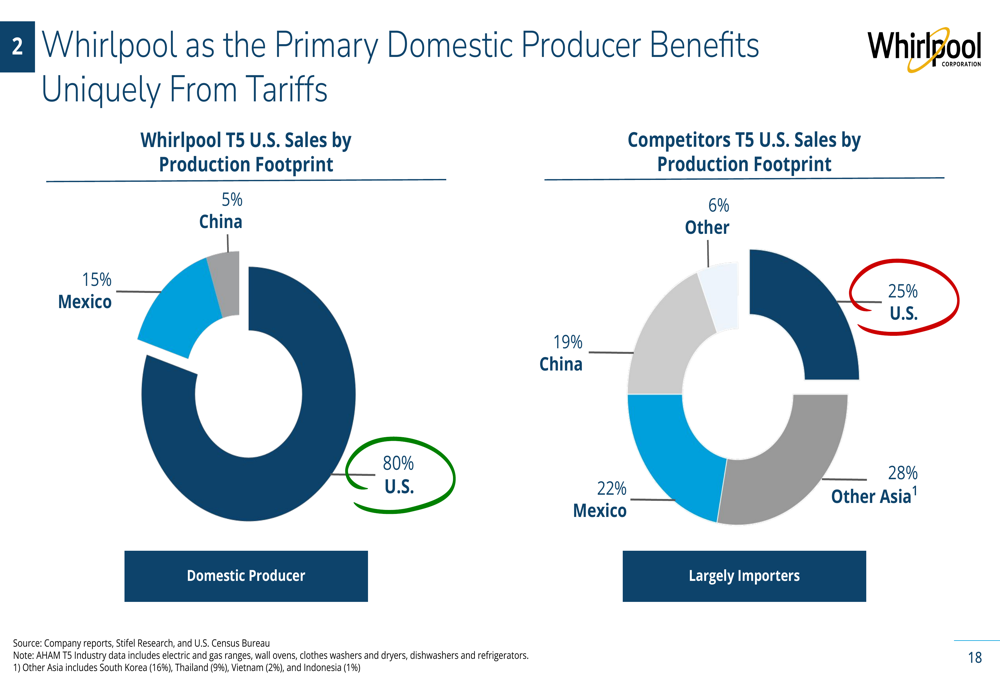

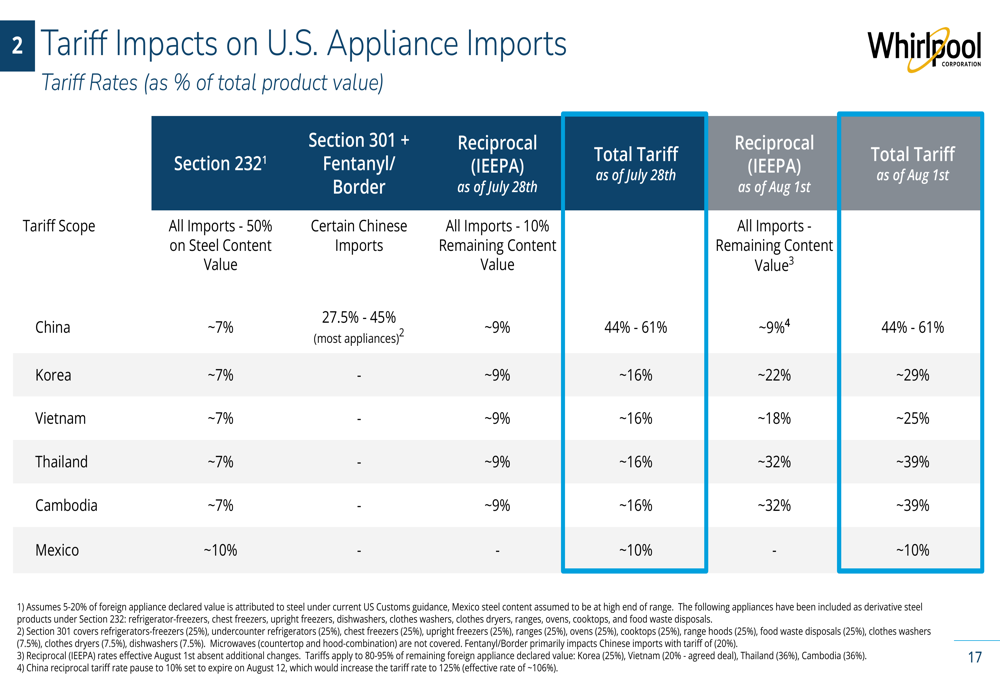

The company emphasized its unique position to benefit from U.S. tariffs on appliance imports, highlighting that 80% of its North American sales come from domestically produced products, compared to competitors who rely heavily on imports from China, Mexico, and other Asian countries:

Whirlpool presented detailed analysis of tariff impacts across different regions, showing how various tariff sections affect imports from China, Korea, Vietnam, Thailand, Cambodia, and Mexico:

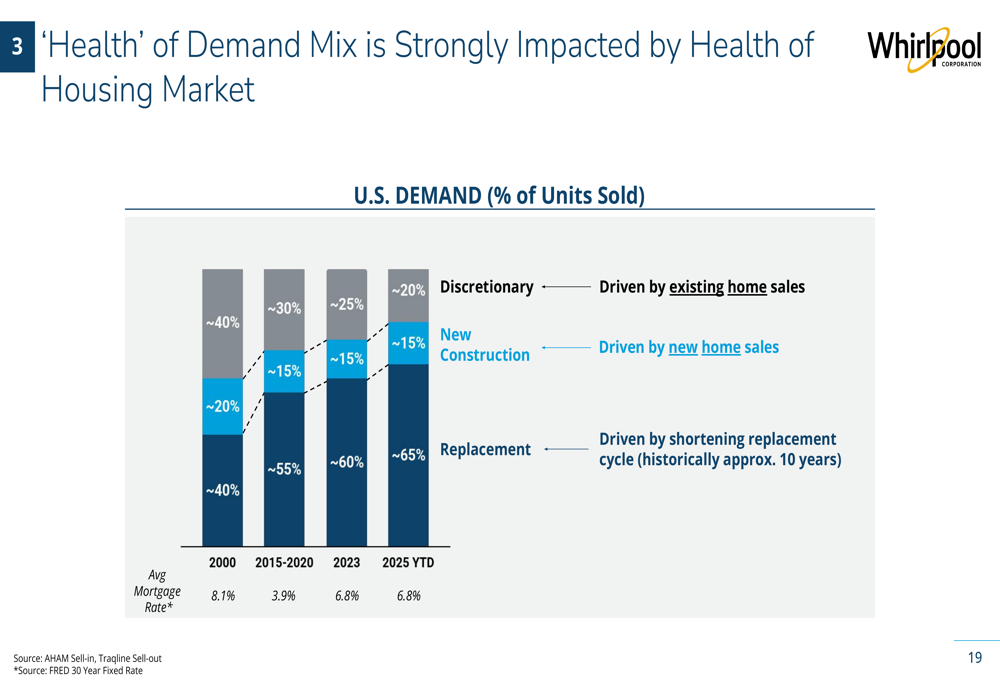

The company also highlighted the relationship between housing market health and appliance demand, noting that existing home sales have decreased substantially over the past three years, affecting discretionary demand which represents approximately 20% of total industry demand:

Forward-Looking Statements

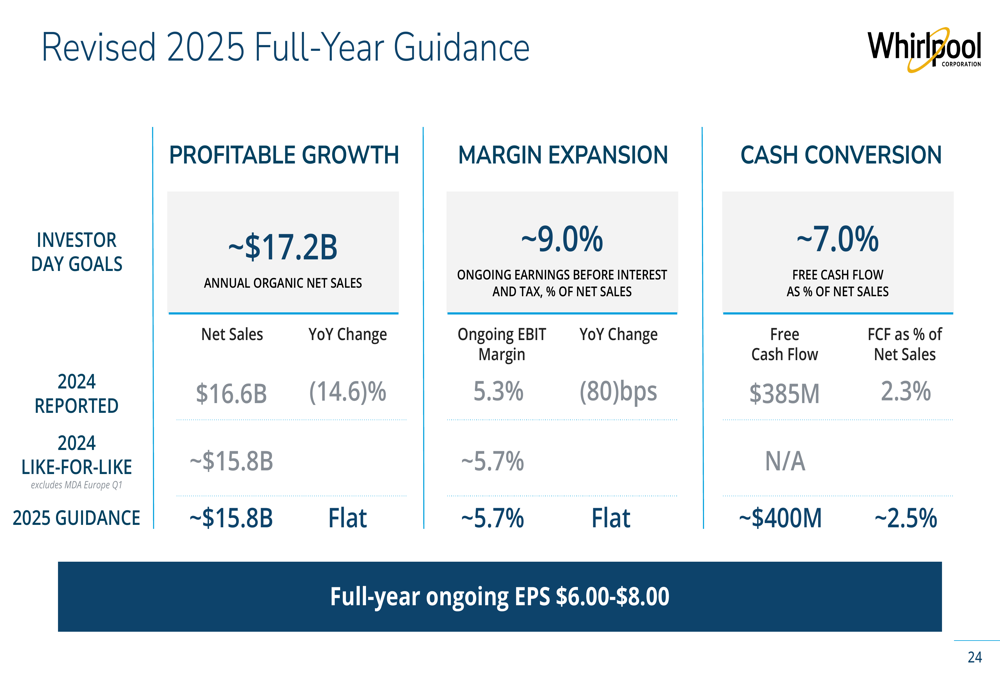

Whirlpool revised its 2025 full-year guidance, projecting net sales of approximately $15.8 billion, ongoing EBIT margin of around 5.7%, and free cash flow as a percentage of net sales at approximately 2.5%. The company set its full-year ongoing EPS guidance at $6.00-$8.00:

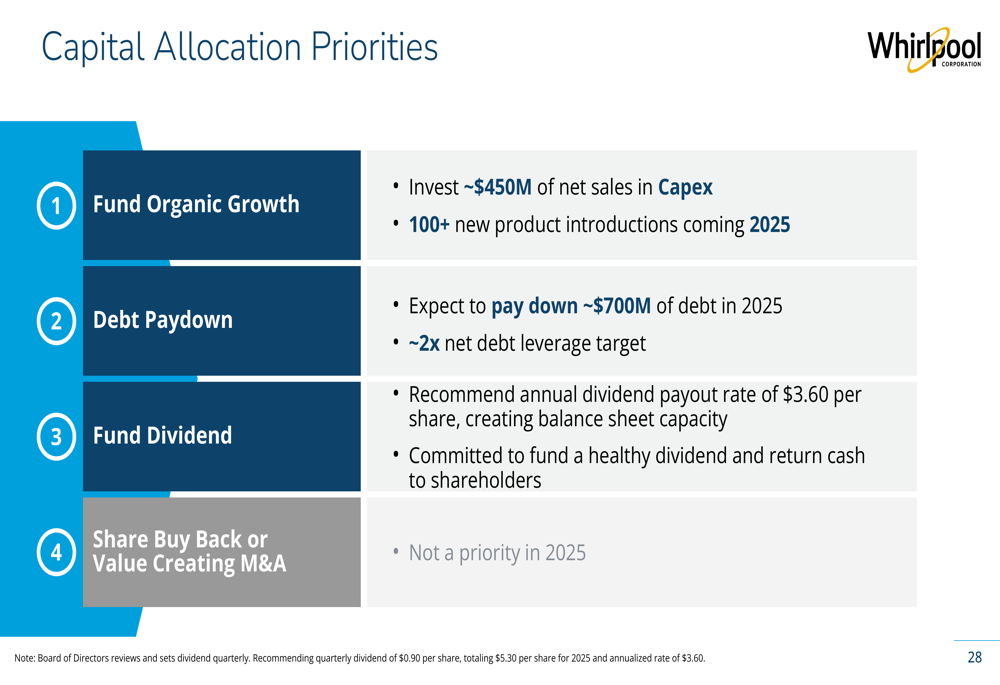

For capital allocation, Whirlpool outlined four priorities: funding organic growth with approximately $450 million in capital expenditures, paying down around $700 million in debt, maintaining a dividend payout of $3.60 per share, and deferring share buybacks or M&A activities for the year:

Conclusion

Despite challenging market conditions and a sales decline, Whirlpool demonstrated operational resilience in Q2 2025 by maintaining stable EBIT margins through cost management initiatives. The company’s SDA Global and Asia segments showed particular strength, helping to offset headwinds in North America.

Looking forward, Whirlpool is positioning itself for growth through new product introductions, leveraging its domestic manufacturing advantage amid increasing tariffs on imports, and preparing for an eventual housing market recovery. While the company has revised its guidance to reflect current market realities, it maintains a focus on debt reduction and shareholder returns through dividends.

As CEO Marc Bitzer noted during the earnings call, "We are well positioned to deliver sustained long-term value," highlighting the company’s strategic initiatives despite near-term challenges in the global appliance market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.