Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

WhiteHorse Finance , Inc. (NASDAQ:WHF) released its second quarter 2025 earnings presentation on August 7, revealing continued pressure on earnings and portfolio quality. The business development company (BDC), which focuses on originating senior secured loans to lower middle market companies, reported declining net investment income and net asset value amid ongoing portfolio challenges.

The stock responded negatively to the results, with premarket trading showing a decline of 4.33% to $8.40, extending its downward trend from the previous day’s close of $8.78. This reaction reflects investor concerns about the company’s ability to maintain its high dividend yield in the face of deteriorating fundamentals.

Quarterly Performance Highlights

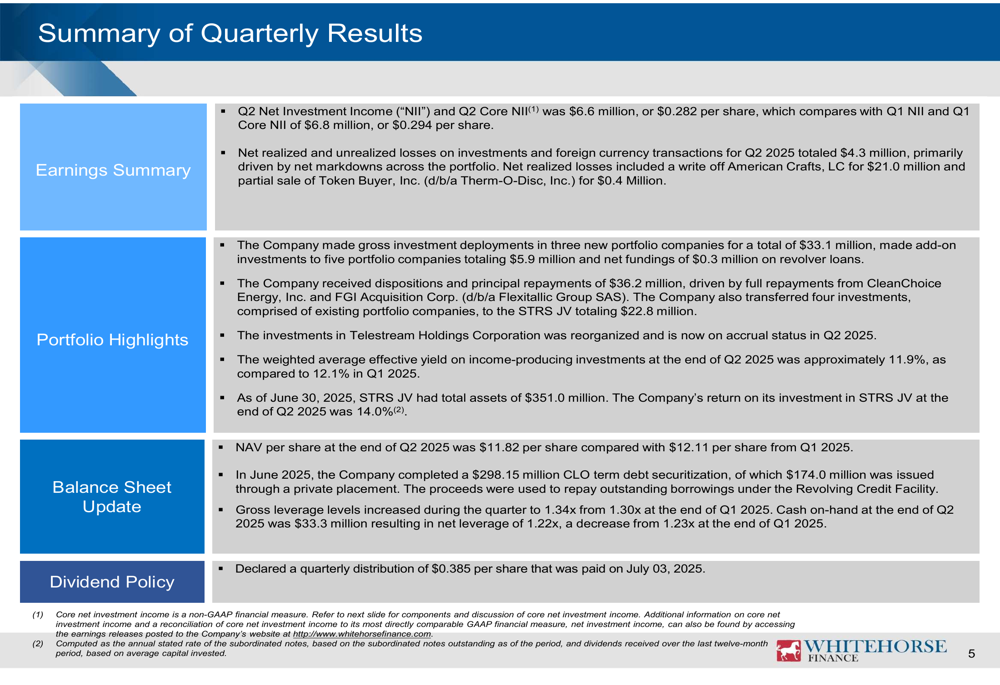

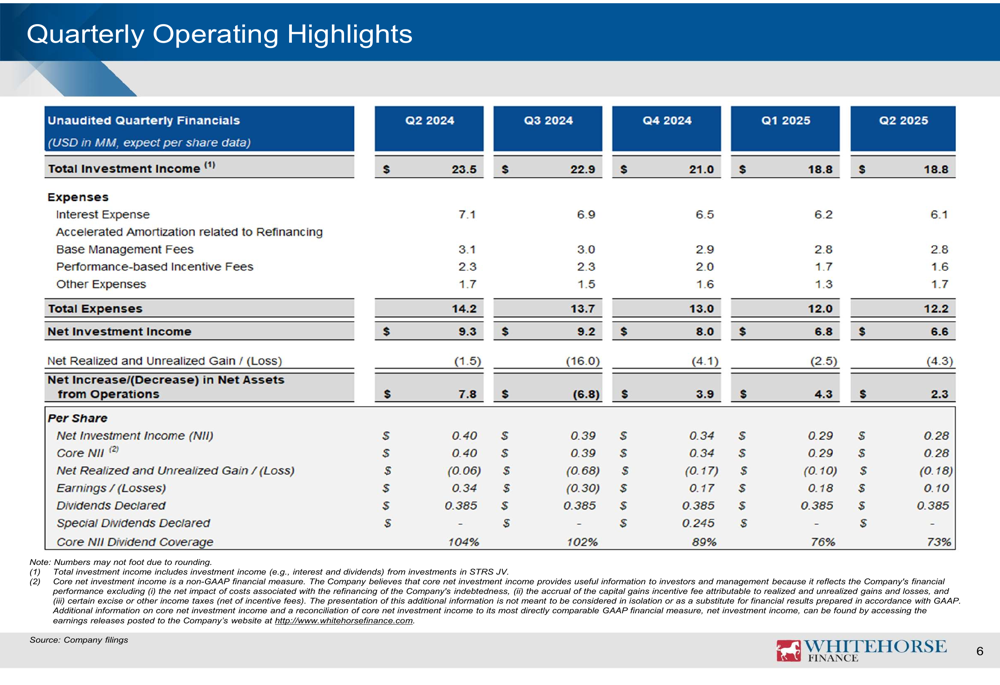

WhiteHorse Finance reported Q2 2025 net investment income (NII) of $6.6 million, or $0.282 per share, down from $6.8 million, or $0.294 per share, in the first quarter. This continues a downward trend from Q4 2024, when the company reported NII of $8.0 million, or $0.343 per share.

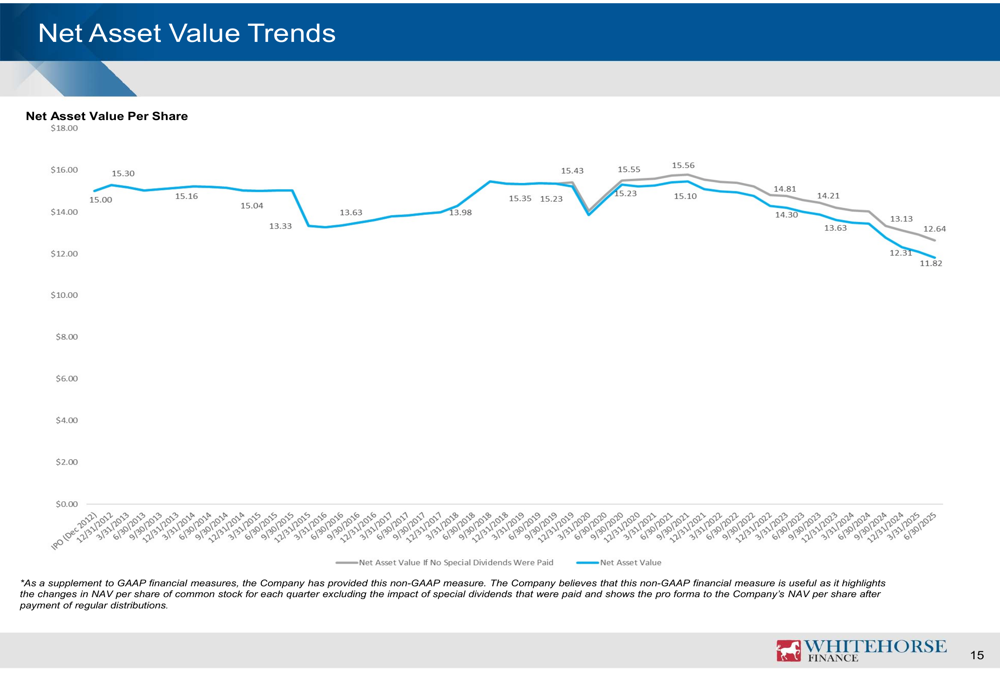

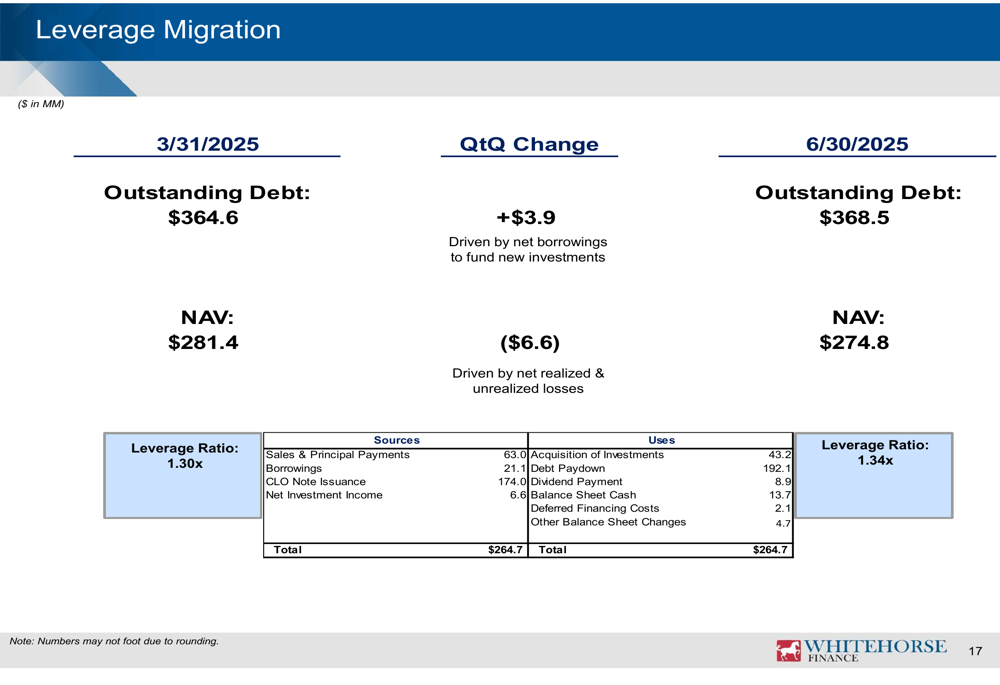

The company’s net asset value (NAV) per share declined to $11.82 as of June 30, 2025, compared to $12.11 at the end of the previous quarter, representing a 2.4% decrease. This decline was primarily driven by net realized and unrealized losses on investments totaling $4.3 million.

As shown in the following chart of quarterly operating results, WhiteHorse has experienced declining investment income and increasing pressure on earnings over recent quarters:

The NAV bridge clearly illustrates the factors contributing to the decline in book value during the quarter, with unrealized losses being the primary driver:

Portfolio Composition and Quality

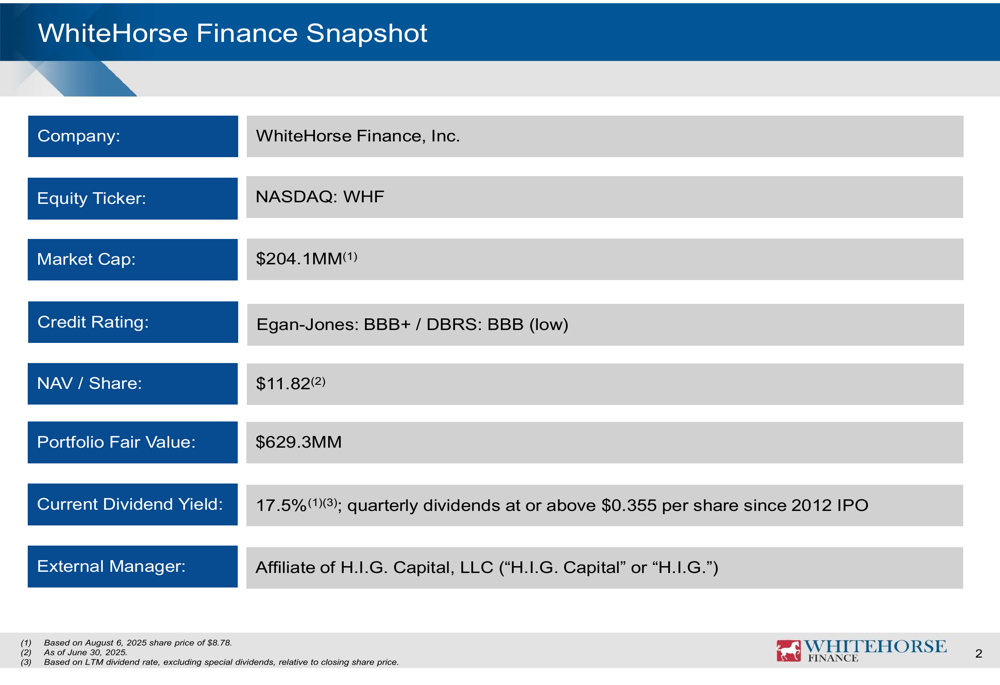

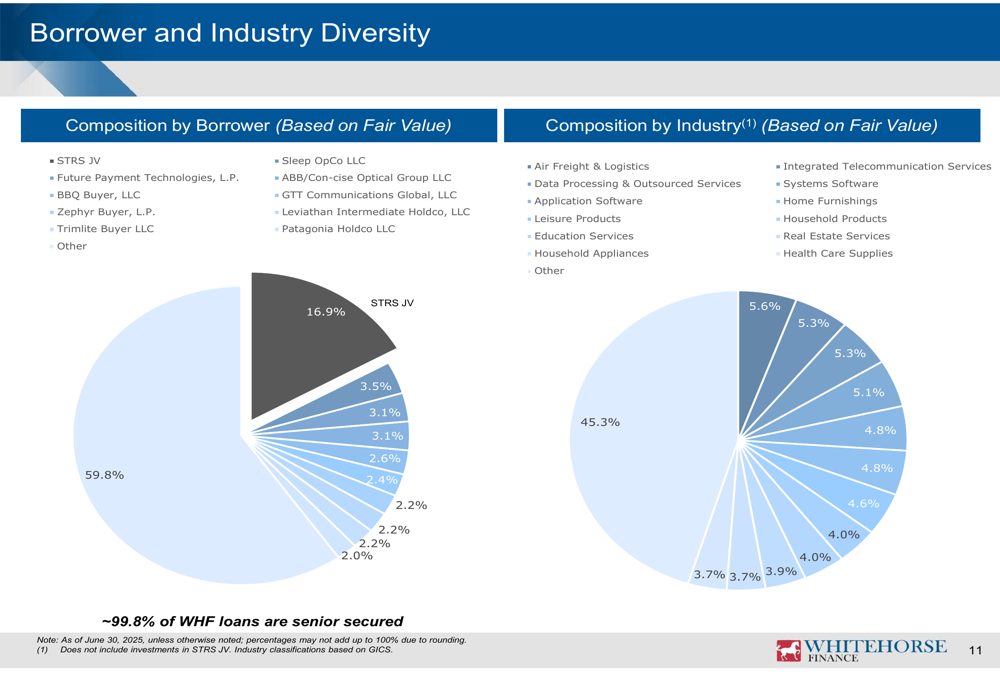

As of June 30, 2025, WhiteHorse Finance maintained a diversified investment portfolio totaling $629.3 million across 132 positions in 71 portfolio companies. The portfolio composition reflects the company’s focus on senior secured lending, with approximately 99.8% of loans being senior secured.

The following snapshot provides an overview of the company’s key metrics:

Portfolio quality remains a concern, as the company recorded significant write-offs during the quarter, including a $21.0 million write-off of American Crafts, LC. However, the company did note that its investment in Telestream Holdings Corporation was reorganized and is now on accrual status as of Q2 2025.

The portfolio’s weighted average effective yield on income-producing investments decreased to 11.9% at the end of Q2 2025, compared to 12.1% in Q1 2025, reflecting the challenging interest rate environment.

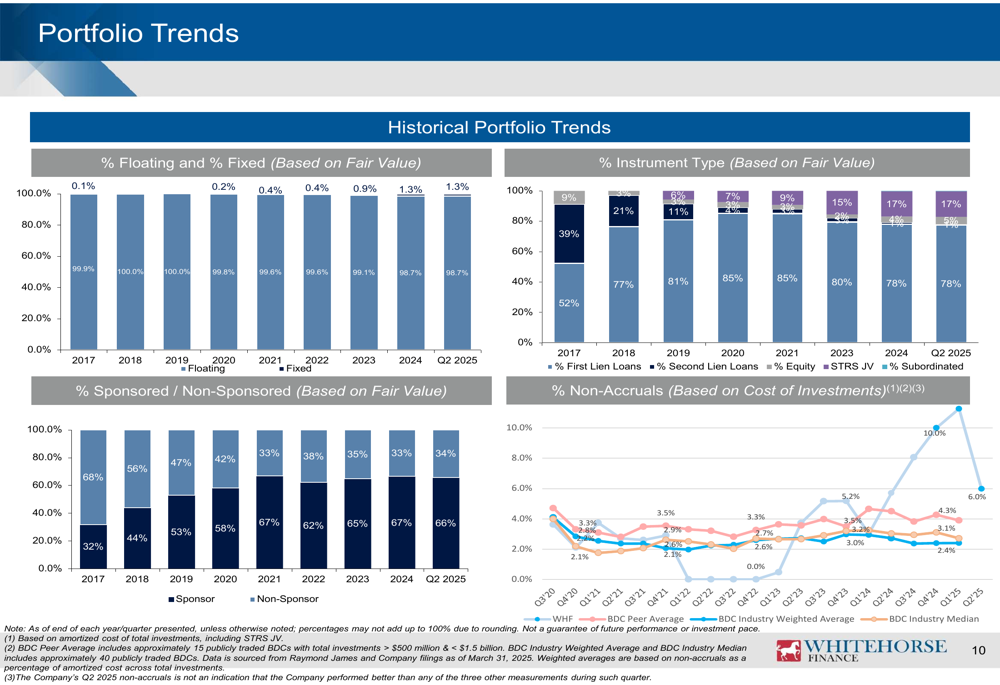

The company’s borrower and industry diversity is illustrated in the following chart:

Dividend and Yield Analysis

Despite the earnings pressure, WhiteHorse Finance declared a quarterly distribution of $0.385 per share that was paid on July 3, 2025. Based on the August 6, 2025 share price, this represents a current dividend yield of 17.5%, excluding special dividends.

However, the sustainability of this dividend is increasingly in question, as the company’s core NII dividend coverage ratio has declined to 73% in Q2 2025. This means the company is paying out more in dividends than it is earning, which is not sustainable in the long term without improvement in earnings or a reduction in the dividend.

The following chart illustrates the company’s dividend coverage trend:

Balance Sheet and Leverage

WhiteHorse Finance’s gross leverage levels increased during the quarter to 1.34x from 1.30x at the end of Q1 2025. However, net leverage decreased slightly to 1.22x from 1.23x, due to increased cash on hand of $33.3 million at the end of Q2 2025.

In June 2025, the company completed a $298.15 million CLO term debt securitization, which helped diversify its funding sources. The company’s balance sheet highlights are shown in the following table:

The company’s funding profile includes various debt instruments with maturities ranging from 2025 to 2028, as detailed below:

Forward Outlook

WhiteHorse Finance faces several challenges going forward, including declining earnings, portfolio quality concerns, and pressure on its dividend coverage. The company’s ability to address non-accrual investments and generate new quality investments will be crucial for reversing the negative trends.

The company’s joint venture with State Teachers Retirement System of Ohio (STRS JV) continues to be a bright spot, with total assets of $351.0 million as of June 30, 2025. The company’s return on its investment in STRS JV at the end of Q2 2025 was 14.0%, outperforming the overall portfolio.

WhiteHorse Finance’s origination capabilities, backed by H.I.G. Capital’s platform of approximately 70+ investment and origination professionals across 13 North American offices, remains a competitive advantage. However, the company will need to leverage this network effectively to improve portfolio quality and earnings in the coming quarters.

Given the current market conditions and the company’s recent performance, investors should closely monitor WhiteHorse Finance’s ability to maintain its dividend and improve its portfolio quality in the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.