Raytheon awarded $71 million in Navy contracts for missile systems

Williams Companies Inc (NYSE:WMB) reported an 8% year-over-year increase in Adjusted EBITDA for the second quarter of 2025, according to the company’s earnings presentation released on August 5, 2025. The natural gas infrastructure company also raised its full-year guidance, highlighting strong performance across its core business segments.

Quarterly Performance Highlights

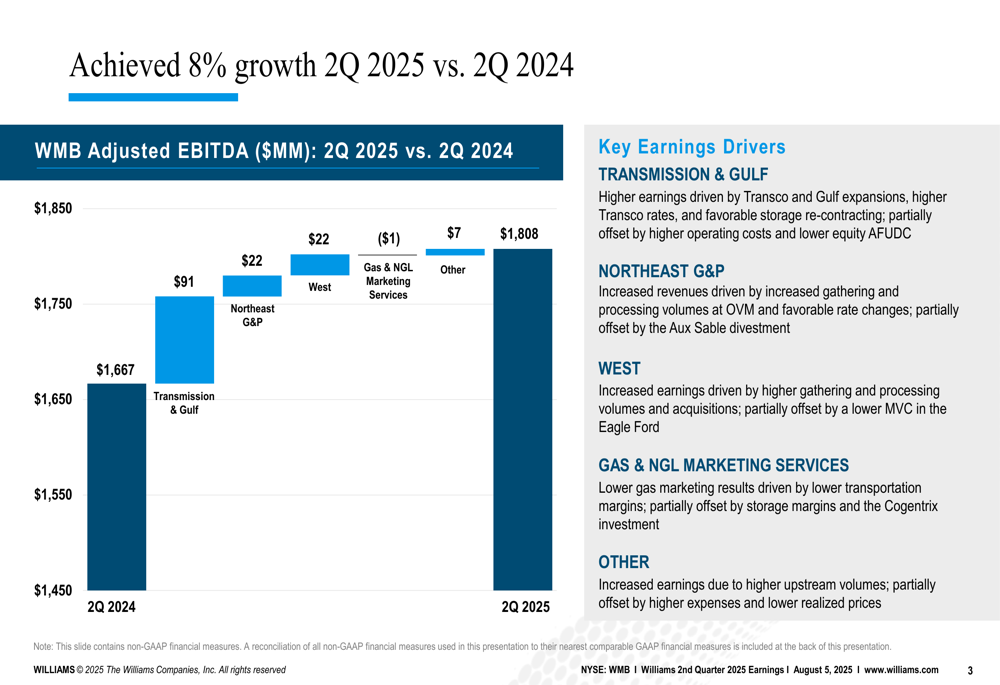

Williams reported Q2 2025 Adjusted EBITDA of $1,808 million, compared to $1,667 million in the same period last year. This 8% increase was primarily driven by the company’s Transmission & Gulf segment, which saw a $91 million improvement year-over-year due to Transco and Gulf expansions, higher Transco rates, and favorable storage re-contracting.

As shown in the following chart of quarterly Adjusted EBITDA performance:

The Northeast G&P and West segments also contributed positively to the year-over-year growth, each adding $22 million to Adjusted EBITDA. However, when compared sequentially to Q1 2025, these segments showed slight declines, with Northeast G&P down $13 million and West down $13 million.

For the first half of 2025, Williams reported year-to-date Adjusted EBITDA of $3,797 million, representing a 5% increase from the $3,601 million reported in the first half of 2024. This growth was driven by strong performance across most business segments, with only Gas & NGL Marketing Services showing a decline.

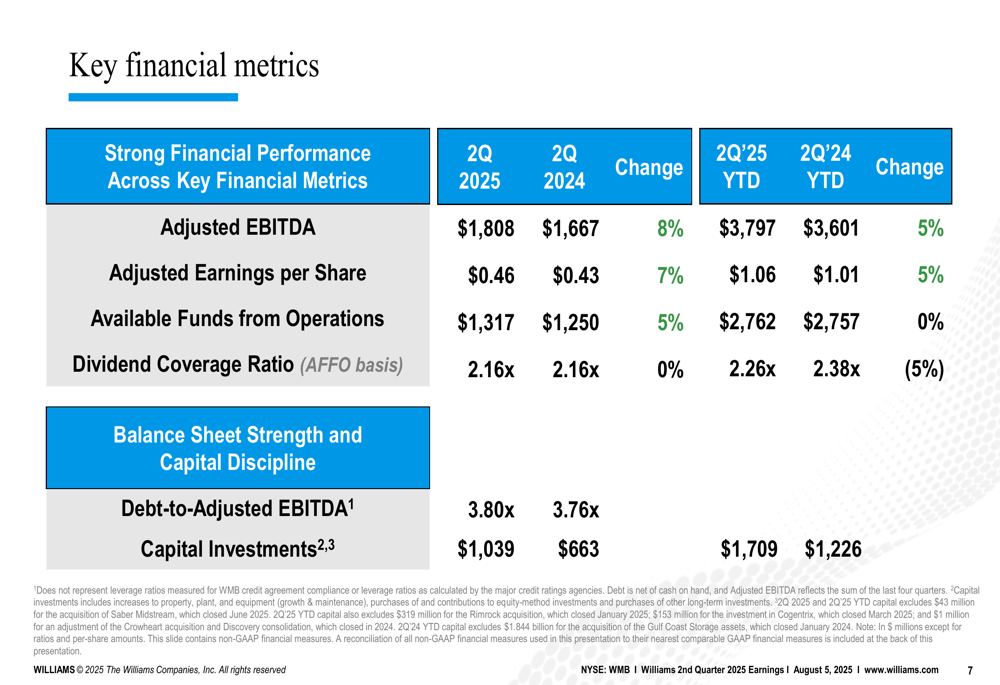

The company’s key financial metrics demonstrate solid performance across multiple indicators:

Adjusted earnings per share increased 7% year-over-year to $0.46 for Q2 2025, while Available Funds from Operations grew 5% to $1,317 million. The dividend coverage ratio remained stable at 2.16x, indicating sustainable shareholder returns despite increased capital investments, which grew from $663 million in Q2 2024 to $1,039 million in Q2 2025.

Strategic Initiatives and Growth Projects

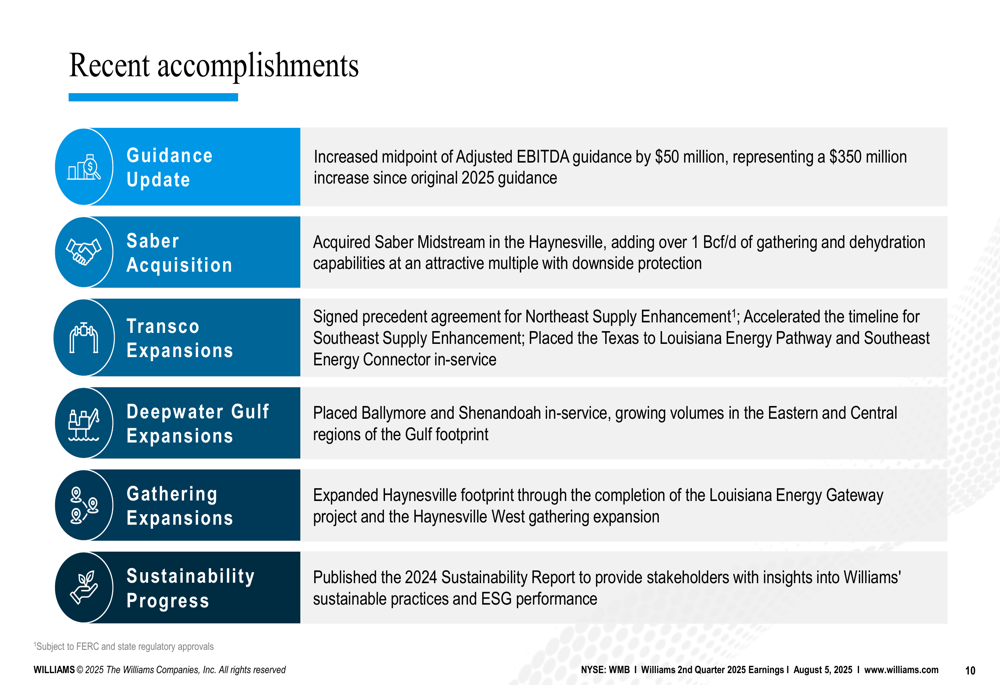

Williams highlighted several strategic accomplishments in its presentation, including the completion of six projects that increased earnings across its Transmission, Gulf, and West segments. The company also expanded its footprint in the Haynesville region through the acquisition of Saber Midstream.

As illustrated in the following slide detailing recent accomplishments:

The company signed a precedent agreement for Transco’s Northeast Supply Enhancement and accelerated the timeline for Southeast Supply Enhancement. Williams also placed the Texas to Louisiana Energy Pathway and Southeast Energy Connector in-service, along with Ballymore and Shenandoah projects in the Deepwater Gulf.

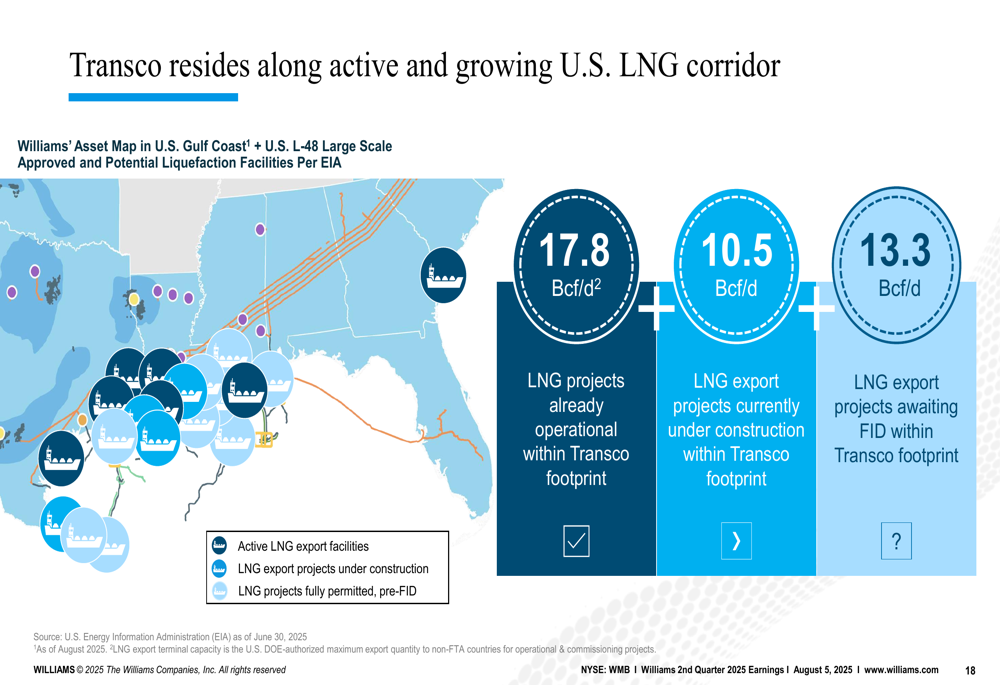

Williams’ strategic positioning along the growing U.S. LNG corridor represents a significant competitive advantage:

The company noted that 17.8 Bcf/d of LNG projects are already operational within its Transco footprint, with an additional 10.5 Bcf/d under construction and 13.3 Bcf/d awaiting final investment decisions. This positioning aligns with the growing demand for natural gas exports, which the company reported averaged 100 Bcf/d in Q2 2025, up from 96 Bcf/d in Q2 2024.

Financial Guidance and Outlook

Williams increased its 2025 Adjusted EBITDA guidance by $50 million, now guiding to a midpoint of $7.75 billion. This represents the third guidance increase since the company’s original 2025 forecast, for a cumulative increase of $350 million.

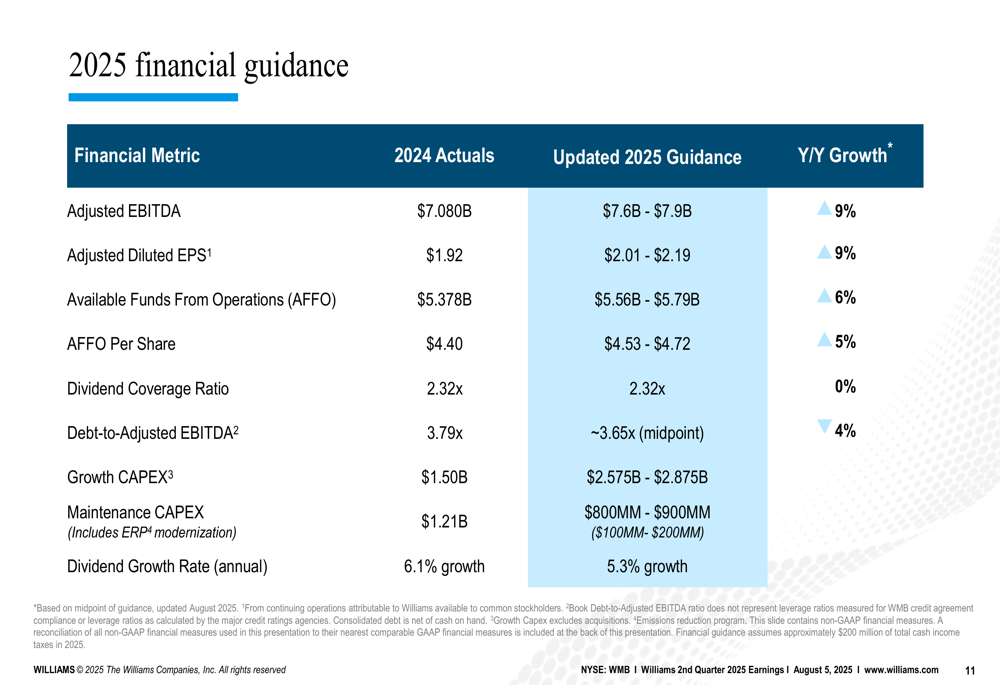

The company’s updated financial guidance for 2025 shows strong projected growth:

Based on the midpoint of guidance, Williams expects 9% year-over-year growth in both Adjusted EBITDA and Adjusted Diluted EPS. The company also anticipates improving its debt-to-Adjusted EBITDA ratio to approximately 3.65x by the end of 2025, down from 3.79x in 2024.

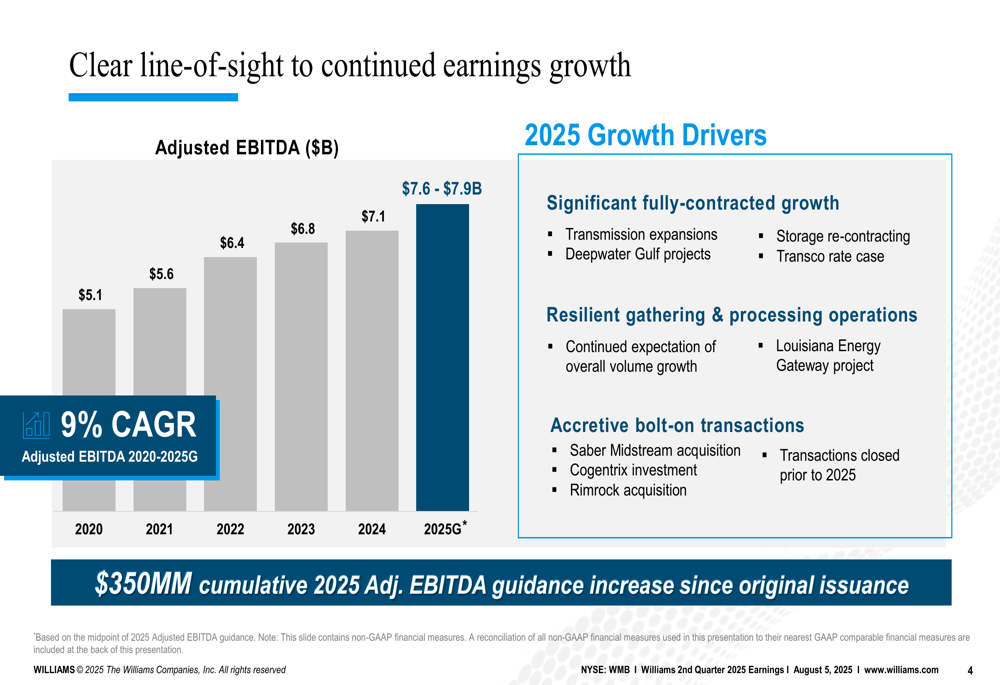

The clear growth trajectory in Adjusted EBITDA is illustrated in the following chart:

Williams has demonstrated consistent growth in Adjusted EBITDA from $5.1 billion in 2020 to a projected $7.6-$7.9 billion in 2025, representing a 9% compound annual growth rate. This growth has been driven by fully-contracted expansion projects, resilient gathering and processing operations, and accretive acquisitions.

Competitive Industry Position

Williams emphasized the growing demand for natural gas across multiple sectors, positioning itself as a key player in meeting this demand through its infrastructure assets. The company highlighted the role of natural gas in supporting growing electricity demand, particularly with the expansion of data centers and AI applications.

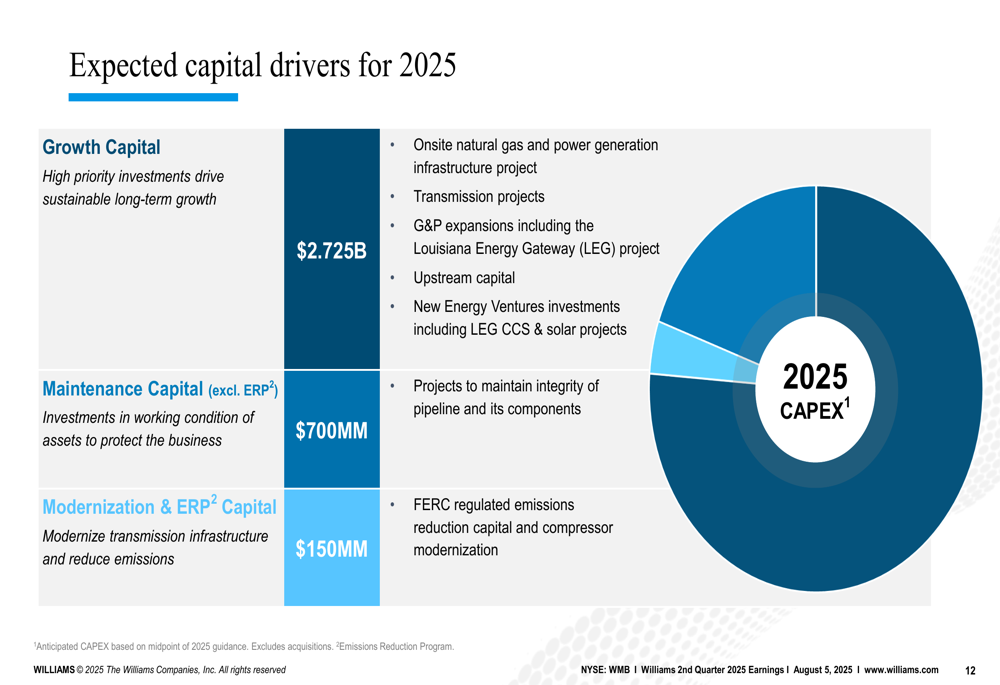

The company’s capital allocation for 2025 reflects its strategic priorities:

Williams plans to allocate $2.725 billion to growth capital in 2025, with investments focused on onsite natural gas and power generation infrastructure, transmission projects, gathering and processing expansions, upstream capital, and new energy ventures.

The company also emphasized its commitment to sustainability, noting a 24% reduction in intensity-based greenhouse gas emissions since 2018, with a goal of achieving a 30% reduction by 2028. Williams positions natural gas as a solution that meets the "trifecta" for energy needs: clean, affordable, and reliable.

In conclusion, Williams’ Q2 2025 earnings presentation depicts a company with strong financial performance, strategic growth initiatives, and favorable market positioning. The 8% year-over-year increase in Adjusted EBITDA and raised guidance suggest continued momentum, though investors should note that the presentation naturally emphasizes positive aspects of the company’s performance and outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.