Barclays now sees two Fed cuts this year, says jumbo Fed cuts ’very unlikely’

Introduction & Market Context

Wintrust Financial Corporation (NASDAQ:WTFC) released its Q2 2025 earnings presentation on July 22, 2025, reporting record quarterly net income of $195.5 million and continued strong balance sheet growth. The company’s stock closed at $131.38 on July 21, down 2.01% ahead of the earnings release, but had risen 3.77% following its Q1 2025 results announced earlier this year.

The Chicago-based regional bank demonstrated robust performance across key metrics, building on momentum from Q1 when it exceeded analyst expectations with earnings per share of $2.69 versus the forecasted $2.48. The Q2 results show continued strength in core banking operations, with significant growth in loans, deposits, and net interest income.

Quarterly Performance Highlights

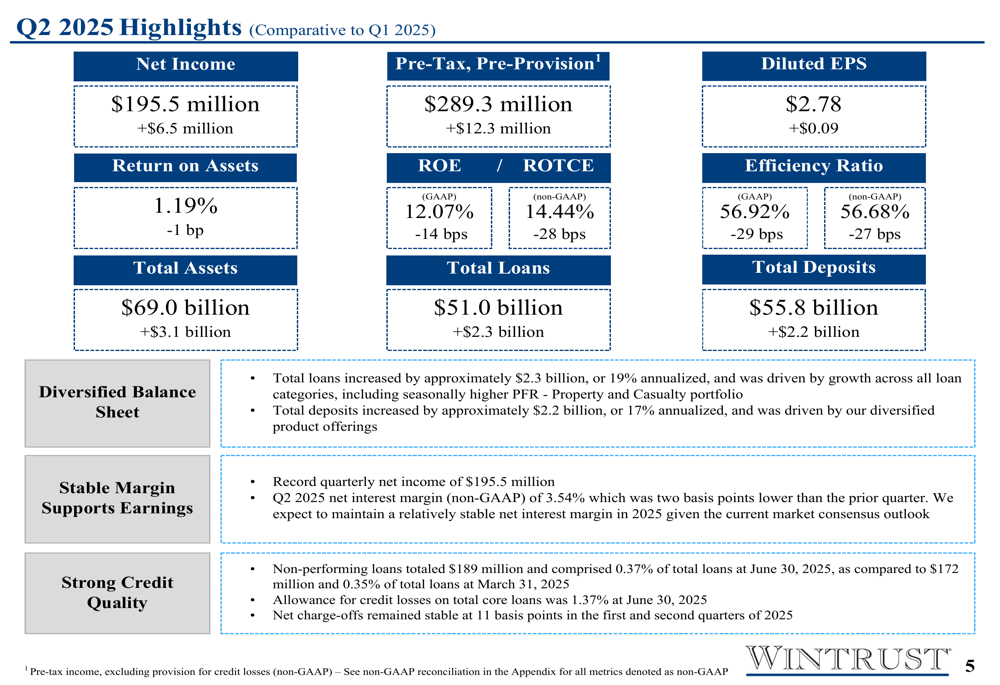

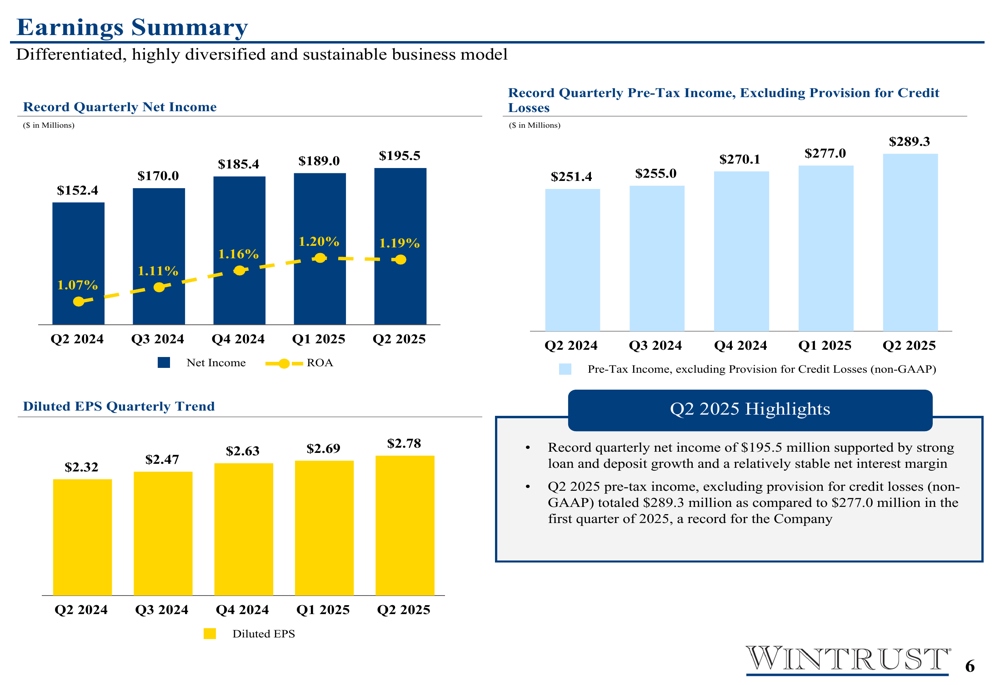

Wintrust reported record quarterly net income of $195.5 million for Q2 2025, an increase of $6.5 million from Q1 2025. Diluted earnings per share reached $2.78, up $0.09 from the previous quarter. Year-to-date net income totaled $384.6 million, representing a 13% increase compared to the same period in 2024.

As shown in the following quarterly highlights chart, the company achieved strong growth across all major financial metrics:

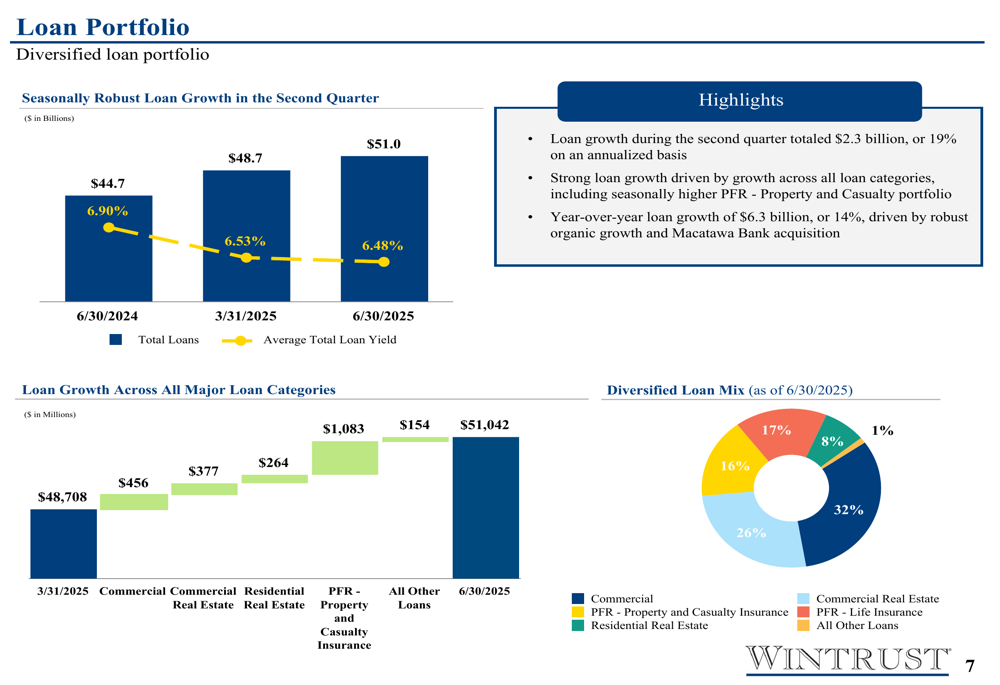

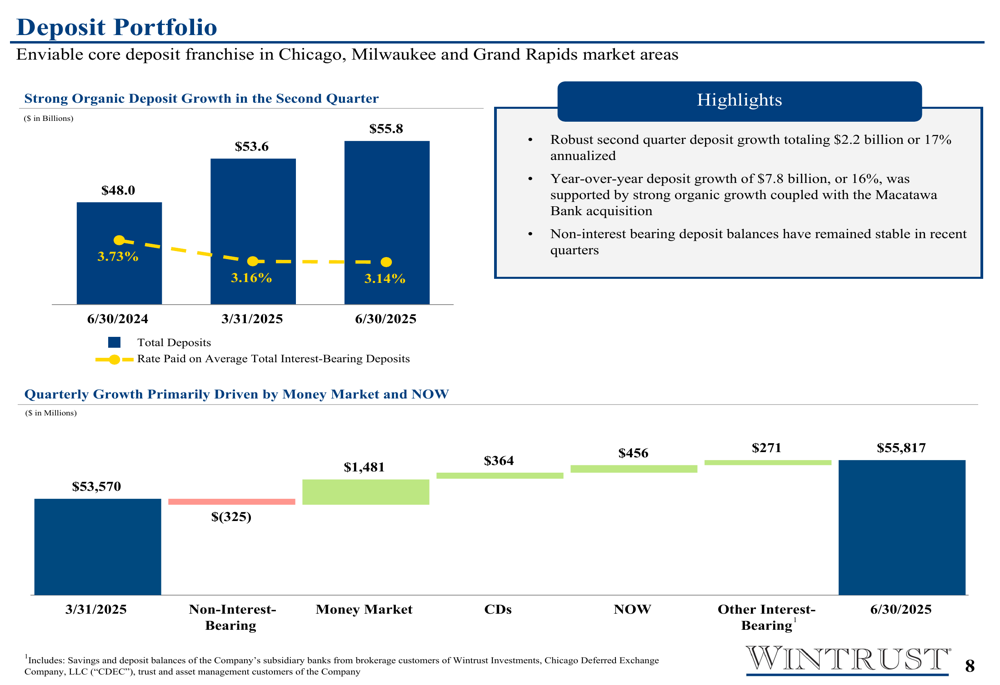

Total (EPA:TTEF) assets grew to $69.0 billion, increasing by $3.1 billion (4.7%) from Q1 2025 and by $9.2 billion (15%) year-over-year. Total loans rose to $51.0 billion, up $2.3 billion (19% annualized) from the previous quarter and $6.3 billion (14%) year-over-year, with growth across all loan categories. Total deposits increased to $55.8 billion, up $2.2 billion (17% annualized) from Q1 2025 and $7.8 billion (16%) year-over-year.

The company’s efficiency ratio improved to 56.68% in Q2 2025 from 56.97% in Q1 2025, indicating better operational efficiency as income growth outpaced expense growth.

Detailed Financial Analysis

Wintrust’s earnings growth has shown consistent improvement over the past year, as illustrated in the following chart:

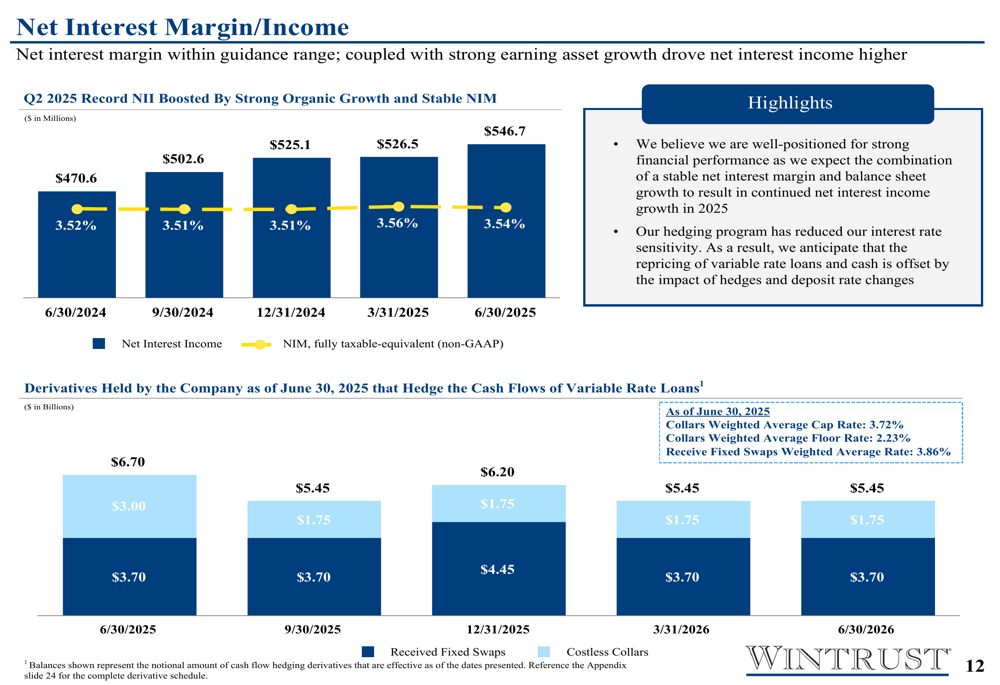

Net interest income reached a record $546.7 million in Q2 2025, up from $536.3 million in Q1 2025 and $470.6 million in Q2 2024. The net interest margin (non-GAAP) remained stable at 3.54% in Q2 2025, compared to 3.55% in Q1 2025 and 3.52% in Q2 2024.

The loan portfolio showed robust growth across all major categories. As illustrated in the following chart, the company maintained a well-diversified loan mix with commercial loans representing 32%, property and casualty insurance premium finance receivables at 26%, residential real estate at 16%, commercial real estate at 17%, life insurance premium finance at 8%, and other loans at 1%:

Deposit growth was equally impressive, with money market accounts contributing $1.48 billion to the quarterly increase, certificates of deposit adding $364 million, and NOW accounts growing by $456 million. The rate paid on average total interest-bearing deposits decreased slightly to 3.14% in Q2 2025 from 3.16% in Q1 2025, helping to maintain the net interest margin.

Non-interest income increased primarily due to higher asset management fees and mortgage originations. Wealth management revenue rose to $53.2 million in Q2 2025 from $48.2 million in Q2 2024, driven by higher asset valuations. Assets under administration increased to $36.8 billion from $35.4 billion a year earlier.

Credit Quality & Risk Management

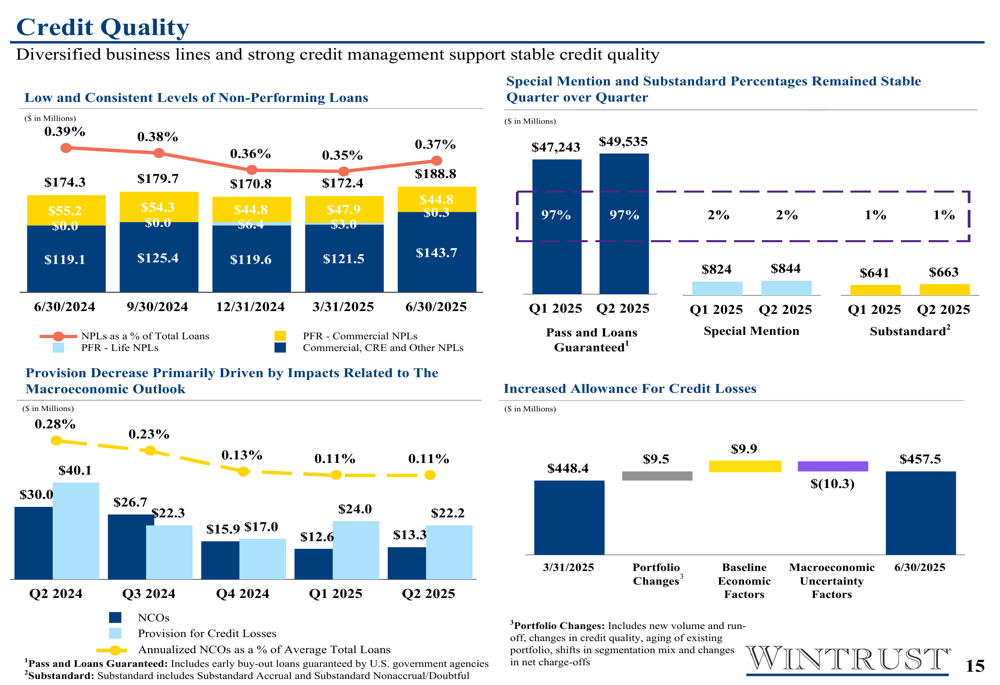

Wintrust maintained strong credit quality metrics in Q2 2025. Non-performing loans totaled $188.8 million, representing 0.37% of total loans, a slight improvement from 0.39% in Q2 2024. The allowance for credit losses on total core loans was 1.37% at June 30, 2025, providing appropriate coverage for potential credit risks.

The following chart illustrates the stable levels of non-performing loans and consistent credit quality:

The provision for credit losses was $13.3 million in Q2 2025, slightly up from $12.6 million in Q1 2025 but significantly lower than the $30.0 million recorded in Q2 2024. This decrease primarily reflects improvements in the macroeconomic outlook.

Wintrust’s commercial real estate portfolio, particularly the office segment, has been an area of focus given market concerns. The company’s CRE office exposure represents just 3.14% of total loans, with 48% being owner-occupied or medical properties. The non-performing loan ratio in this segment was 1.19% as of June 30, 2025.

The company has implemented a hedging strategy to mitigate the potential negative impacts of falling interest rates. As of June 30, 2025, Wintrust had $3.0 billion in receive-fixed swaps and $3.7 billion in costless collars to hedge the cash flows of variable rate loans:

Capital Position & Shareholder Returns

Wintrust maintained strong capital levels, with a Common Equity Tier 1 (CET1) ratio of 10.0% as of June 30, 2025, up from 9.5% a year earlier. These capital levels exceed regulatory requirements, providing flexibility for continued growth and shareholder returns.

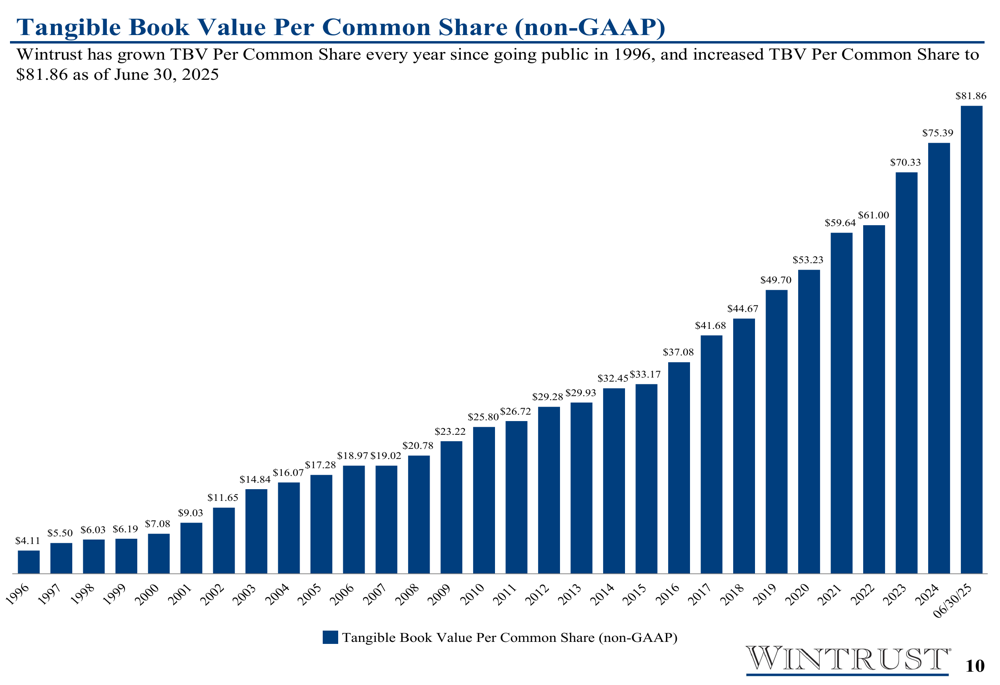

The tangible book value per common share increased to $81.86 as of June 30, 2025, up from $70.33 at the end of 2024 and $72.01 at the end of Q1 2025. This represents a continuation of Wintrust’s track record of growing tangible book value every year since going public in 1996:

Wintrust’s total shareholder return has generally outperformed the KBW Nasdaq Regional Banking Total Return Index (KRXTR) over various time periods. For the one-year period ending June 30, 2025, Wintrust delivered a total shareholder return of 27.67% compared to 26.80% for the index. Over the five-year period, Wintrust’s return was 201.05% versus 87.50% for the index.

Forward-Looking Statements

Looking ahead, Wintrust appears well-positioned for continued growth in the second half of 2025. The company’s diversified loan portfolio, strong deposit base, and effective hedging strategy provide a solid foundation for navigating potential interest rate changes.

During the Q1 2025 earnings call, CEO Tim Crane had expressed cautious optimism about the company’s prospects, noting, "We had a solid first quarter." The Q2 results have built upon that momentum, with record net income and continued balance sheet growth.

The company’s loan growth is expected to remain strong, particularly in the premium finance segment, which showed robust origination volume in Q2 2025. Management had previously guided for mid to high single-digit loan growth for the year, but the actual results have exceeded these expectations with 14% year-over-year growth through the first half of 2025.

While economic uncertainty remains due to potential tariffs and funding cuts, as mentioned in the Q1 earnings call, Wintrust’s diversified business model and strong credit quality position it well to navigate potential challenges in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.