Praxis Precision Medicines general counsel sells $4.8m in shares

Introduction & Market Context

WM Technology, Inc. (NASDAQ:MAPS) released its second quarter 2025 financial results on August 7, 2025, revealing a mixed performance with declining revenue but improved profitability. The cannabis technology company, which operates the Weedmaps platform, continues to navigate a challenging market environment characterized by pricing pressures and regulatory uncertainties in the cannabis sector.

The company's stock closed at $1.02 on November 6, 2025, down 2.86% following its more recent Q3 earnings announcement, which showed further revenue challenges. However, the Q2 presentation provides important context for understanding the company's financial trajectory and strategic positioning.

Quarterly Performance Highlights

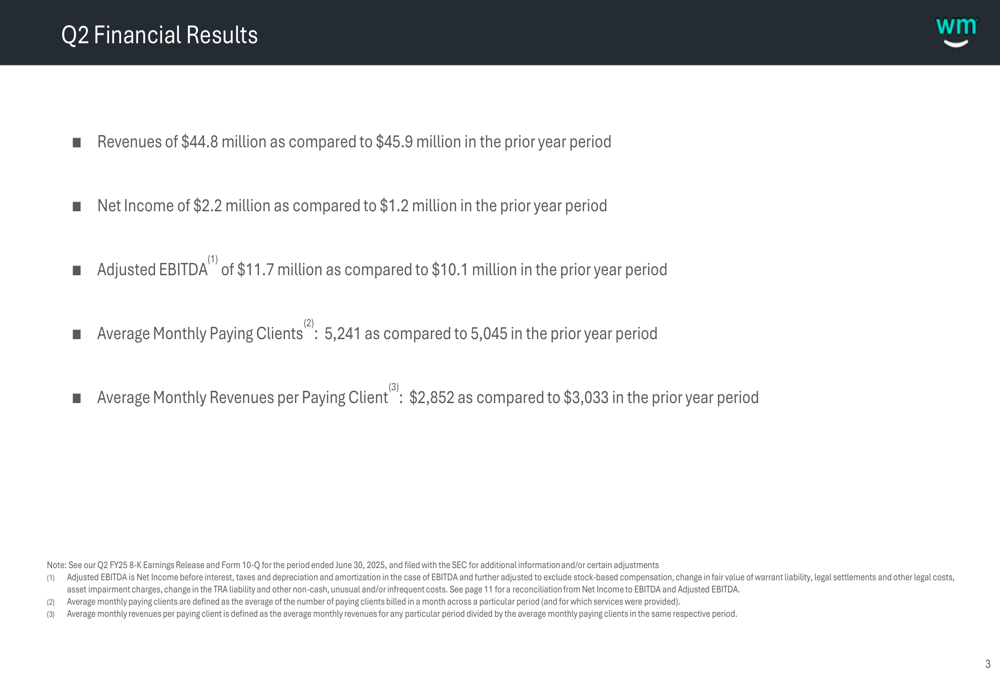

WM Technology reported Q2 2025 revenue of $44.8 million, representing a 2% year-over-year decrease from $45.9 million in Q2 2024. Despite this decline, the company achieved a 1% sequential growth compared to Q1 2025. More significantly, profitability metrics showed substantial improvement, with net income reaching $2.2 million, an 83% increase from $1.2 million in the prior year period.

As shown in the following financial results summary, the company demonstrated notable improvements in profitability metrics while maintaining client growth:

Adjusted EBITDA, a key measure of operational efficiency, increased to $11.7 million from $10.1 million in Q2 2024, representing a 16% improvement. The adjusted EBITDA margin expanded to 26%, up from 22% in the prior year period, highlighting the company's focus on operational efficiency and cost management.

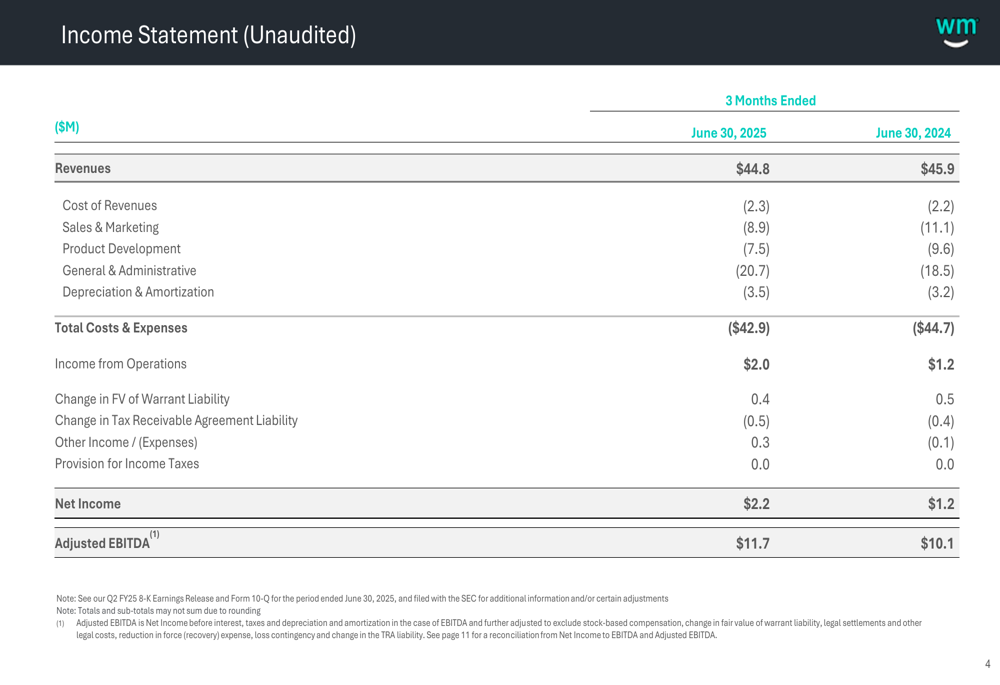

The detailed income statement reveals that WM Technology achieved these profitability gains through strategic cost reductions in sales and marketing (down 20% year-over-year) and product development (down 22% year-over-year):

Detailed Financial Analysis

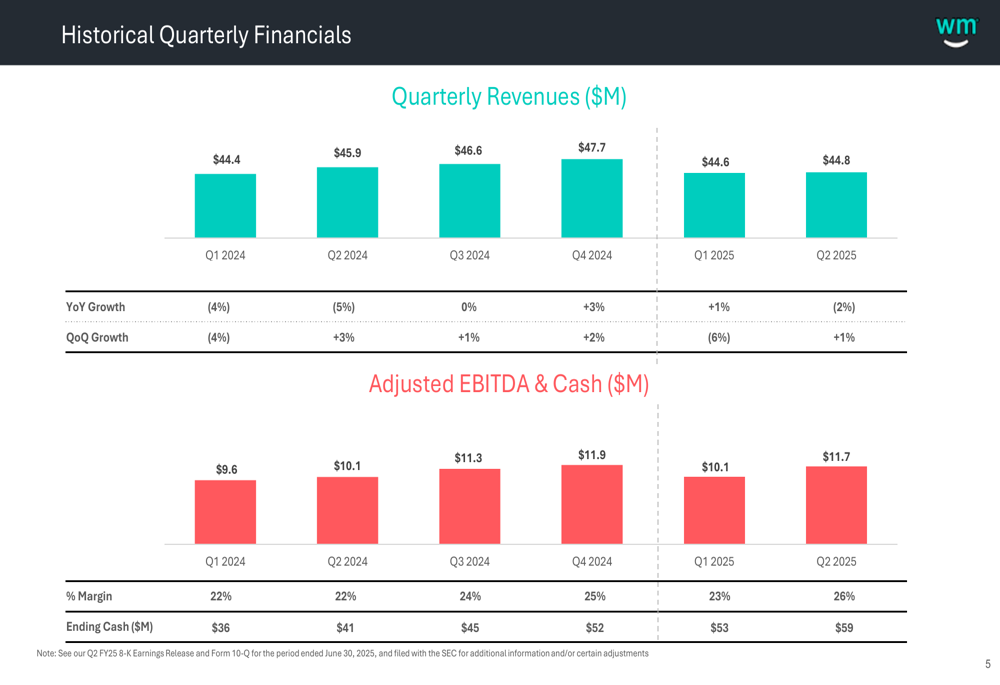

WM Technology's historical quarterly performance shows a stabilizing revenue trend after several quarters of fluctuation. While year-over-year comparisons remain challenging, the sequential quarterly growth suggests potential stabilization.

The following chart illustrates the company's revenue and adjusted EBITDA trends over the past six quarters:

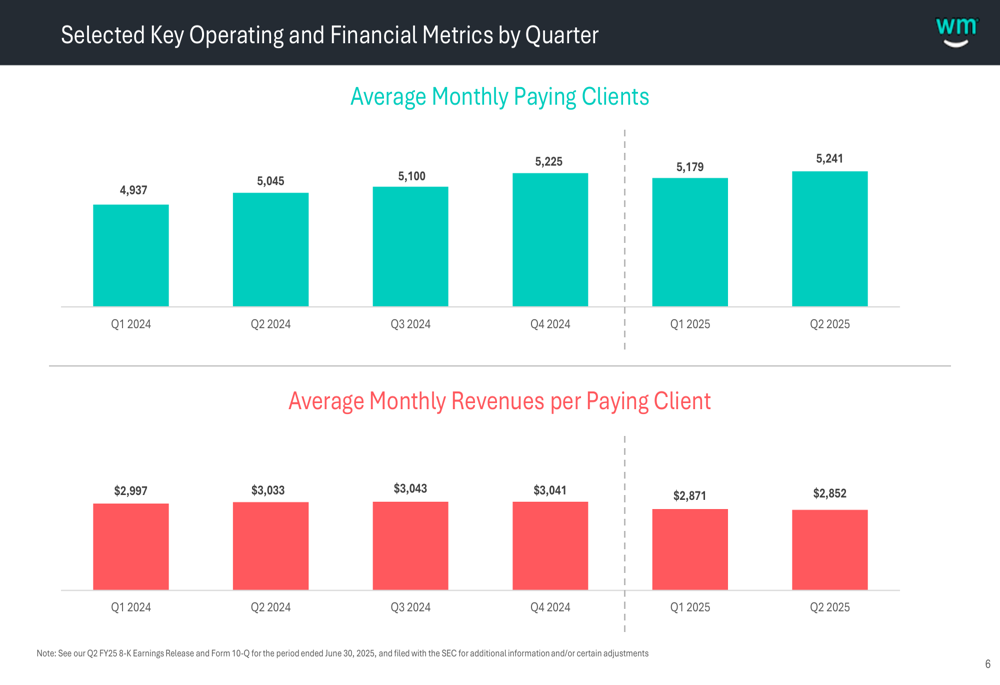

The company's client metrics present a mixed picture. Average monthly paying clients increased to 5,241 in Q2 2025, up from 5,045 in Q2 2024, representing a 4% year-over-year growth. However, average monthly revenue per paying client decreased to $2,852, down from $3,033 in the prior year period, indicating pricing pressures or changes in client composition.

This trend is clearly visible in the operating metrics chart:

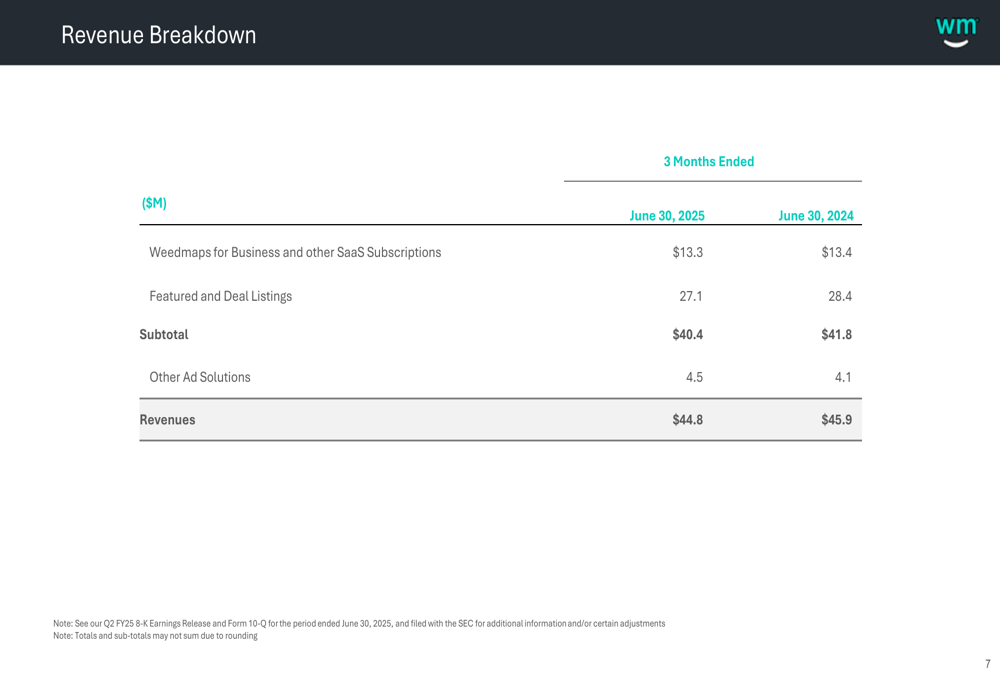

A deeper analysis of WM Technology's revenue composition reveals that the decline was primarily driven by a reduction in Featured and Deal Listings, which fell from $28.4 million in Q2 2024 to $27.1 million in Q2 2025. However, the company saw growth in Other Ad Solutions, which increased from $4.1 million to $4.5 million year-over-year.

The revenue breakdown provides further insight into these shifts:

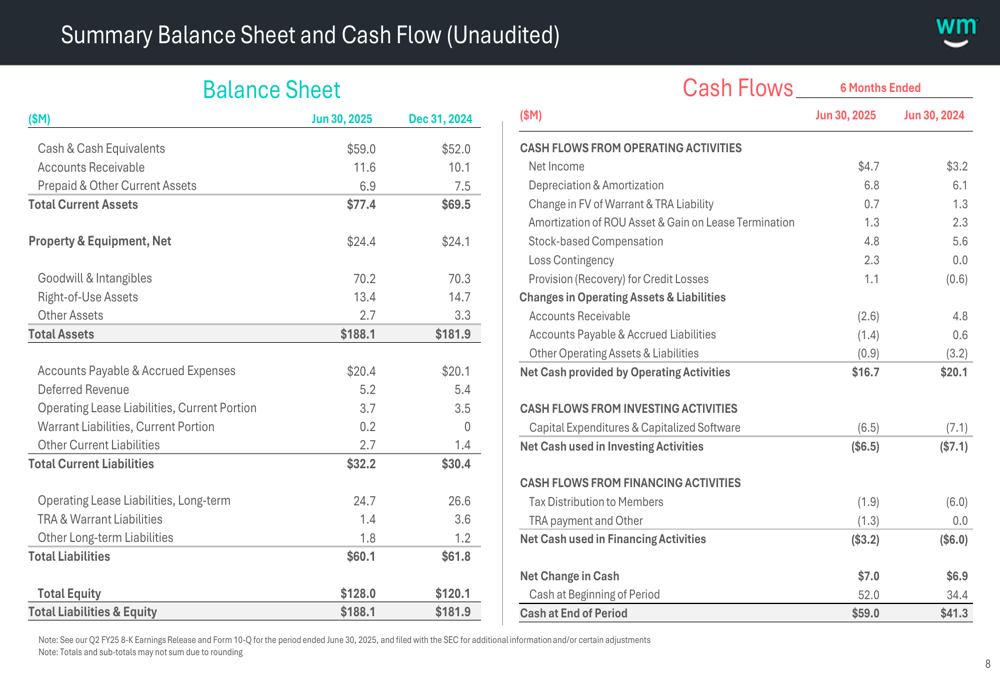

WM Technology maintains a strong financial position with $59.0 million in cash and cash equivalents as of June 30, 2025, up from $52.0 million at the end of 2024. The company generated $16.7 million in operating cash flow during the first half of 2025, demonstrating solid cash conversion despite revenue challenges.

The balance sheet summary highlights this financial strength:

Strategic Initiatives & Forward Outlook

WM Technology's Q2 2025 results should be viewed in the context of its subsequent Q3 performance, which showed further revenue decline to $42.2 million and an earnings miss. This suggests that the challenges observed in Q2 continued into the following quarter.

According to recent earnings information, CEO Doug Francis has emphasized a strategy of "control what we can control," focusing on operational efficiency while positioning the company to capitalize on potential regulatory changes in the cannabis industry. The company is also exploring opportunities in the intoxicating hemp market as a potential growth avenue.

The company's ownership structure, as illustrated below, shows a controlling interest of 67.9%, which may provide stability for implementing long-term strategic initiatives:

Looking ahead, WM Technology faces several challenges, including declining retail flower prices in key markets like California and Michigan, regulatory uncertainties, and potential market consolidation. However, its improved profitability metrics, growing client base, and strong cash position provide a foundation for navigating these challenges.

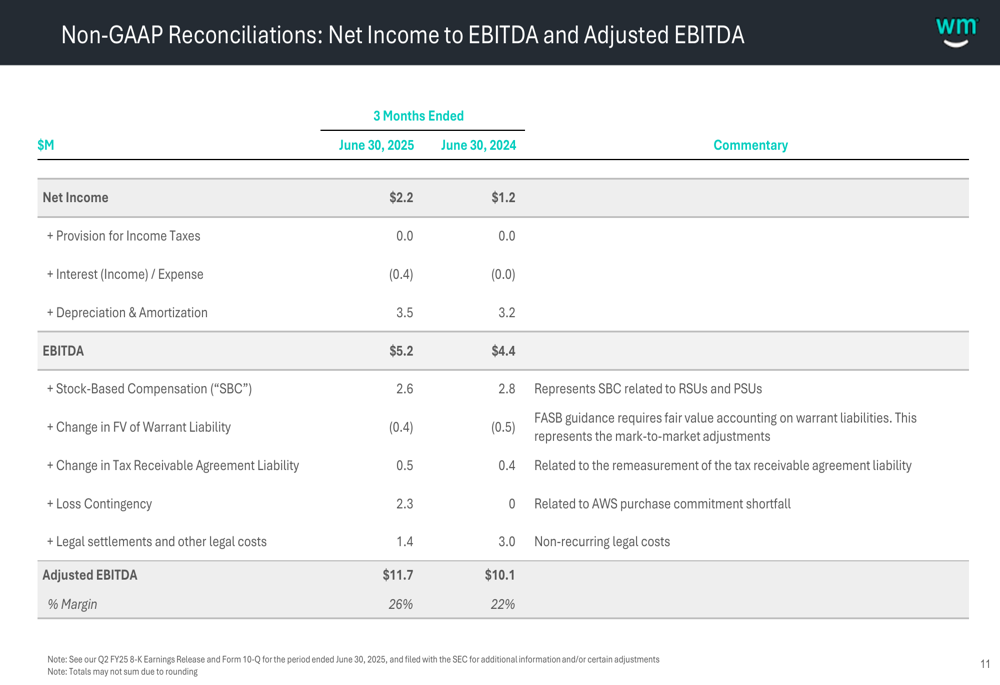

The reconciliation of net income to adjusted EBITDA reveals that stock-based compensation, legal settlements, and a loss contingency were significant factors affecting the company's reported profitability:

As WM Technology moves forward, investors will be watching closely to see if the company can reverse the revenue decline trend while maintaining its improved profitability. The cannabis technology sector continues to evolve rapidly, presenting both challenges and opportunities for established platforms like Weedmaps.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.