Navitas stock soars as company advances 800V tech for NVIDIA AI platforms

WM Technology Inc (NASDAQ:MAPS) reported mixed second-quarter 2025 results, showing a slight revenue decline but improved profitability amid ongoing challenges in the cannabis market. The company’s presentation, released on August 7, 2025, revealed continued client growth despite decreasing average revenue per client.

Quarterly Performance Highlights

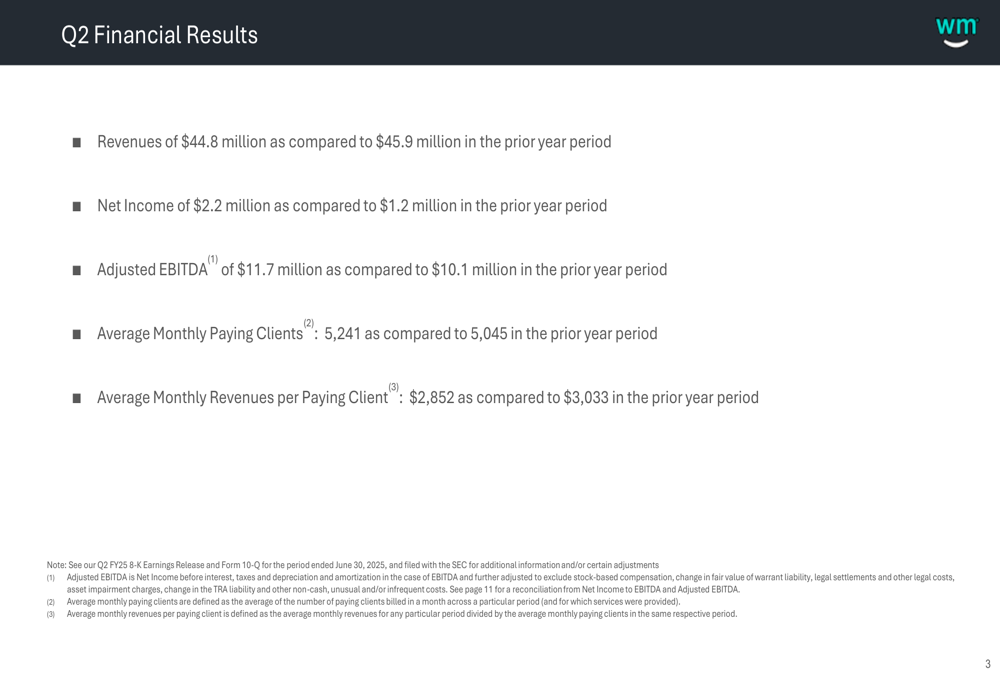

WM Technology reported Q2 2025 revenues of $44.8 million, representing a 2% year-over-year decline from $45.9 million in Q2 2024, but a modest 1% sequential increase from Q1 2025. Despite the revenue challenges, the company significantly improved its bottom line, with net income rising to $2.2 million compared to $1.2 million in the prior year period.

The company’s adjusted EBITDA reached $11.7 million, up from $10.1 million in Q2 2024, with margins expanding to 26% from 22% a year earlier. This profitability improvement came despite the slight revenue decline, suggesting effective cost management strategies.

As shown in the following summary of Q2 financial results:

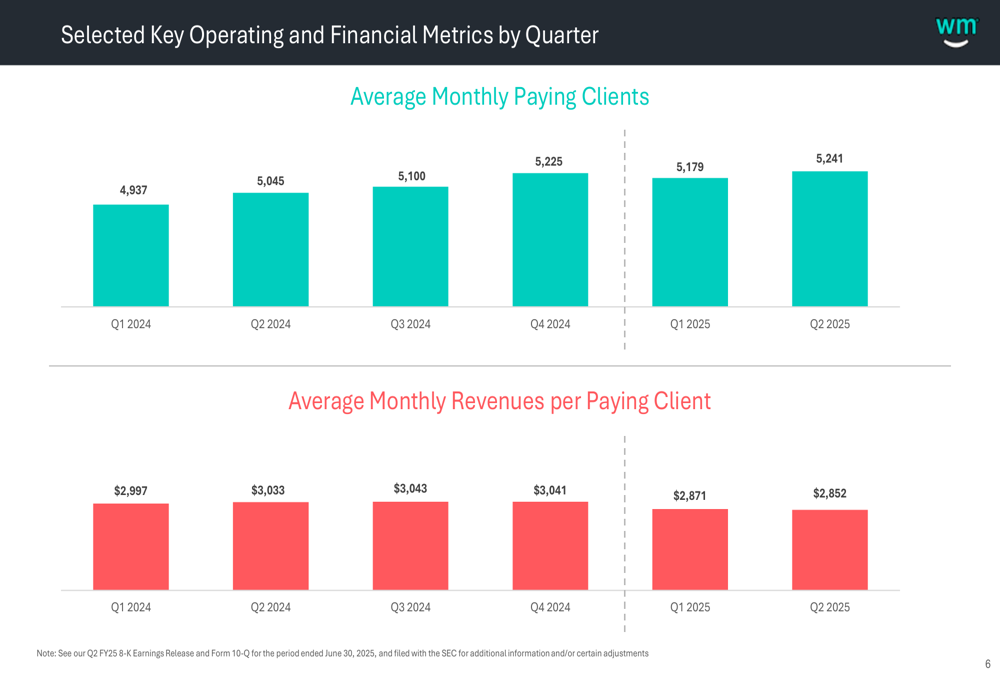

WM Technology’s client metrics showed mixed results for the quarter. The company reported 5,241 average monthly paying clients, a 4% increase from 5,045 in the prior year period. However, average monthly revenues per paying client declined to $2,852, down approximately 6% from $3,033 in Q2 2024.

The following chart illustrates the company’s client growth trajectory over recent quarters:

Detailed Financial Analysis

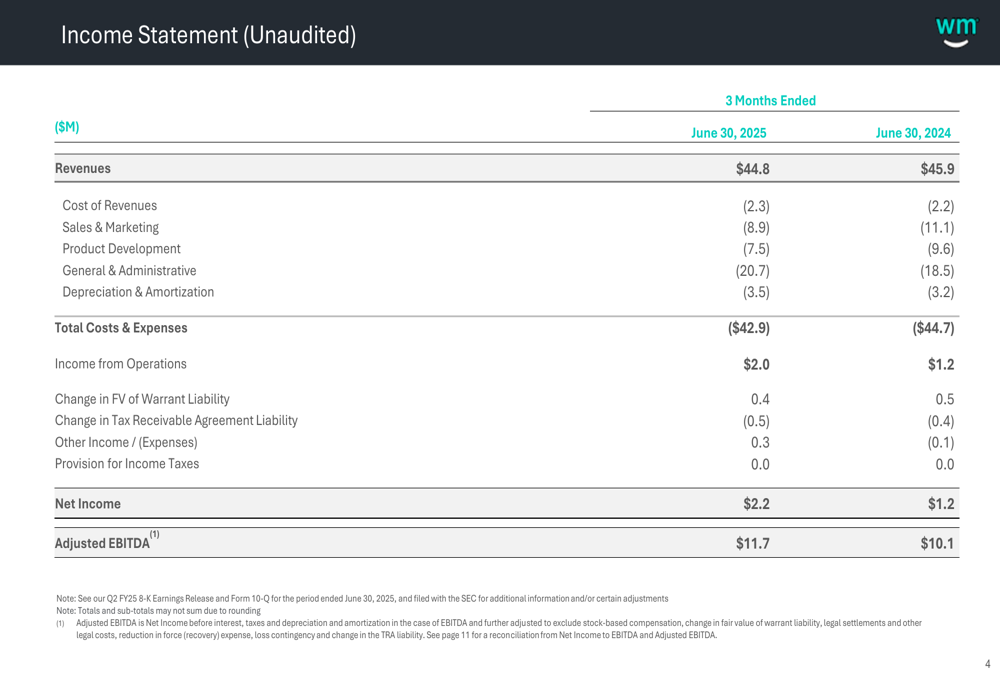

A closer examination of WM Technology’s income statement reveals significant cost reductions in key operational areas. Sales and marketing expenses decreased to $8.9 million from $11.1 million in Q2 2024, while product development costs fell to $7.5 million from $9.6 million. These reductions were partially offset by an increase in general and administrative expenses, which rose to $20.7 million from $18.5 million in the prior year period.

The company’s complete income statement provides additional context for these changes:

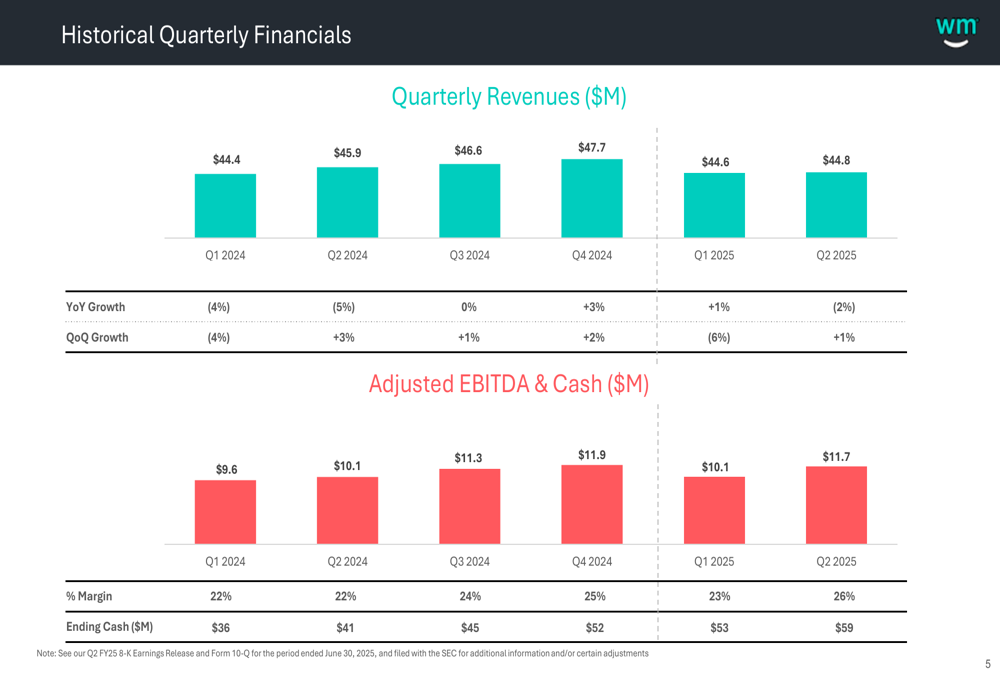

Revenue trends over the past six quarters show stabilization after earlier declines, with modest sequential growth in the most recent quarter. The company’s adjusted EBITDA has shown more consistent improvement, reflecting the company’s focus on operational efficiency.

The following chart illustrates these quarterly financial trends:

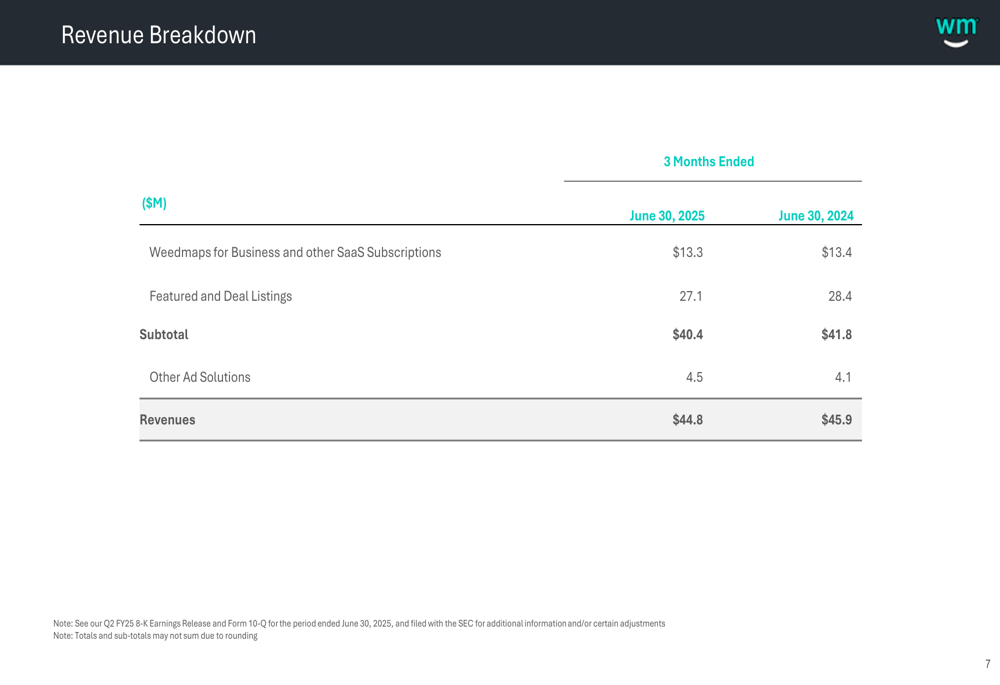

WM Technology’s revenue breakdown reveals that Featured and Deal Listings remain the largest revenue component at $27.1 million, though this segment declined from $28.4 million in Q2 2024. The company’s SaaS subscription revenue was relatively stable at $13.3 million, while Other Ad Solutions grew to $4.5 million from $4.1 million in the prior year period.

The detailed revenue breakdown is shown here:

Financial Position and Outlook

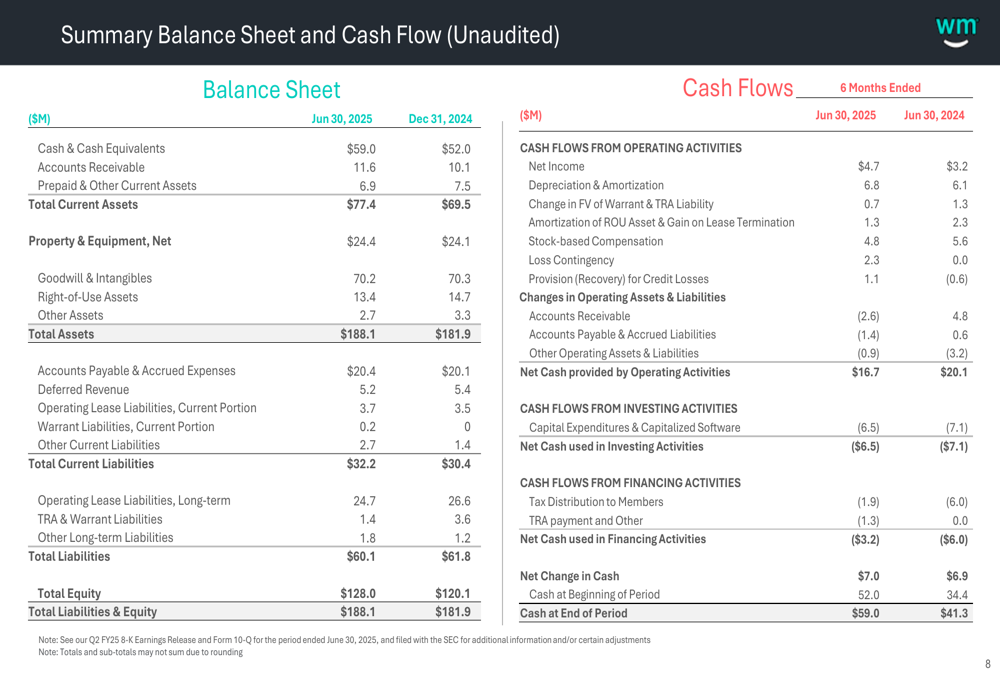

WM Technology continues to strengthen its financial position, with cash and cash equivalents increasing to $59.0 million as of June 30, 2025, up from $52.0 million at the end of 2024 and $41.3 million a year earlier. This cash growth demonstrates the company’s ability to generate positive cash flow despite challenging market conditions.

For the first half of 2025, the company reported $16.7 million in net cash provided by operating activities, though this represents a decrease from $20.1 million in the same period of 2024. The company maintains a debt-free balance sheet, with total assets of $188.1 million against total liabilities of $60.1 million.

The company’s balance sheet summary provides additional details:

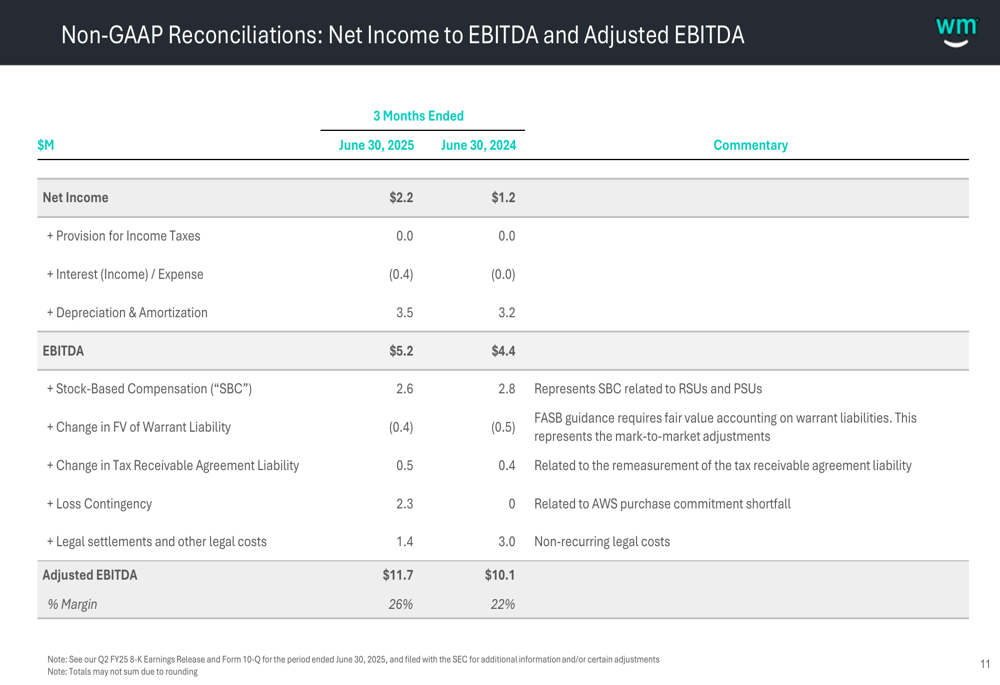

WM Technology’s adjusted EBITDA reconciliation shows several significant adjustments to net income, including stock-based compensation of $5.4 million and changes in fair value of warrant liabilities of $0.6 million. These adjustments help explain the difference between the company’s reported net income of $2.2 million and its adjusted EBITDA of $11.7 million.

The following reconciliation details these adjustments:

The Q2 2025 results show that WM Technology exceeded its adjusted EBITDA guidance of $8 million provided during the Q1 earnings call, but slightly missed its revenue projection of $45 million. The company’s stock has faced pressure in recent months, trading at $0.902 as of August 7, 2025, down 5.35% for the day and well below its 52-week high of $1.65.

Despite these challenges, WM Technology’s improved profitability metrics and growing cash reserves provide some stability as the company navigates the evolving cannabis market landscape. The company’s ability to grow its client base while improving margins suggests a strategic focus on operational efficiency and selective growth opportunities in a challenging industry environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.