TPI Composites files for Chapter 11 bankruptcy, plans delisting from Nasdaq

Introduction & Market Context

Worksport Ltd (NASDAQ:WKSP) presented its Q2 2025 earnings results on August 13, showing significant revenue growth and margin expansion despite the stock trading down 12.14% on the day to close at $3.78. The company, which specializes in tonneau covers for pickup trucks and is expanding into clean energy solutions, highlighted its progress toward operational cash flow positivity while navigating tariff pressures and scaling production.

The company’s stock has traded between $2.44 and $12.00 over the past 52 weeks, with the current price representing a significant discount to analyst price targets ranging from $7.00 to $12.50, according to available market data.

Quarterly Performance Highlights

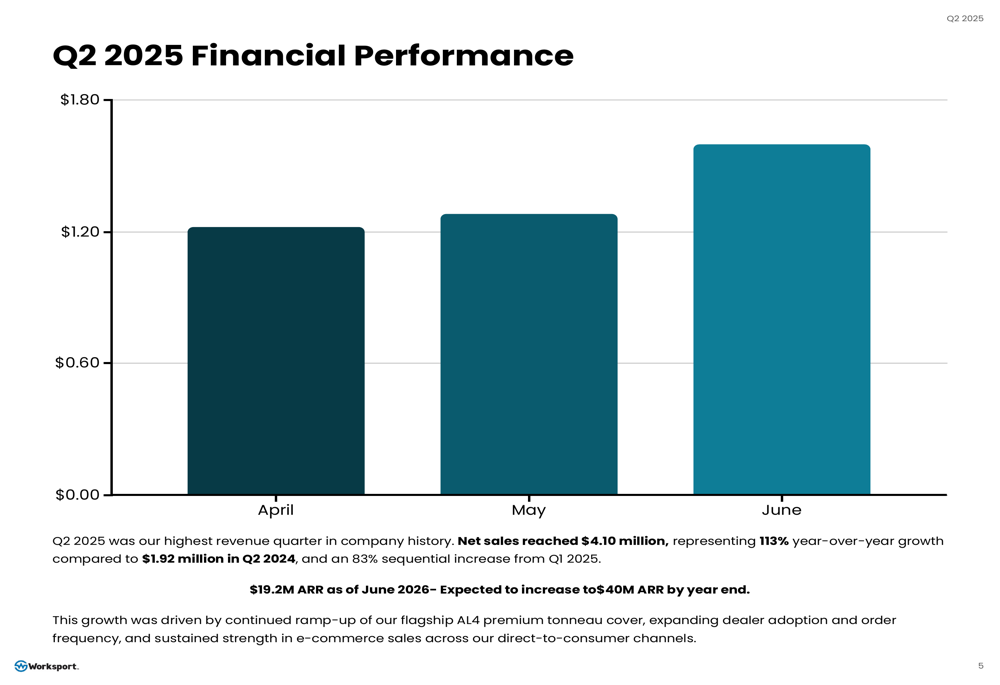

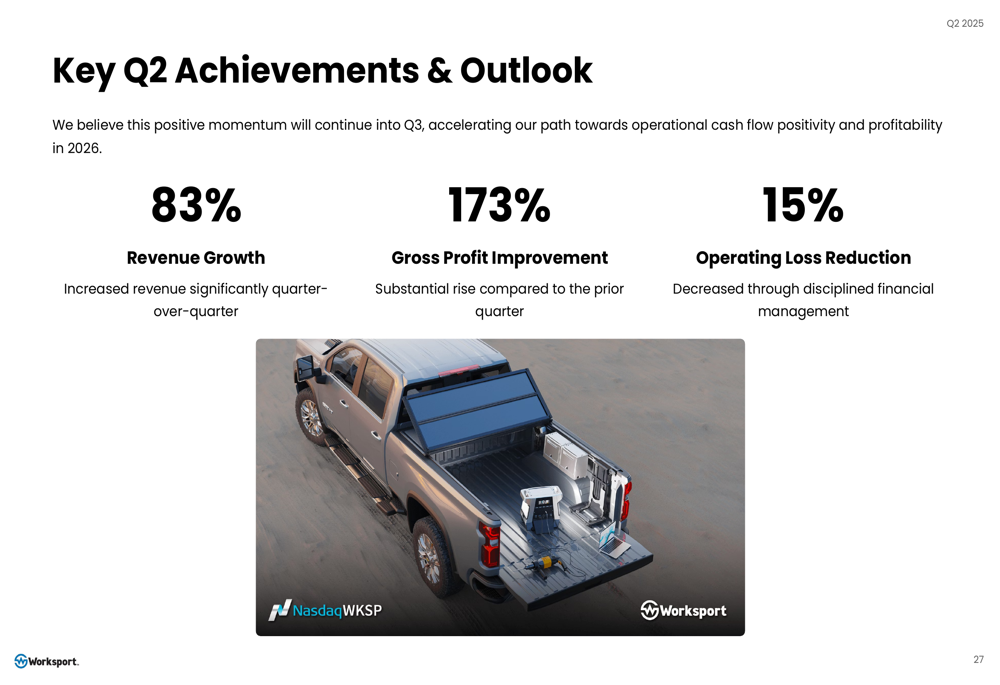

Worksport reported Q2 2025 revenue of $4.10 million, representing 113% year-over-year growth compared to $1.92 million in Q2 2024, and an 83% sequential increase from Q1 2025. This marked the highest quarterly revenue in company history, driven by the continued ramp-up of the AL4 premium tonneau cover, expanding dealer adoption, and sustained strength in e-commerce sales.

As shown in the following chart of quarterly revenue growth:

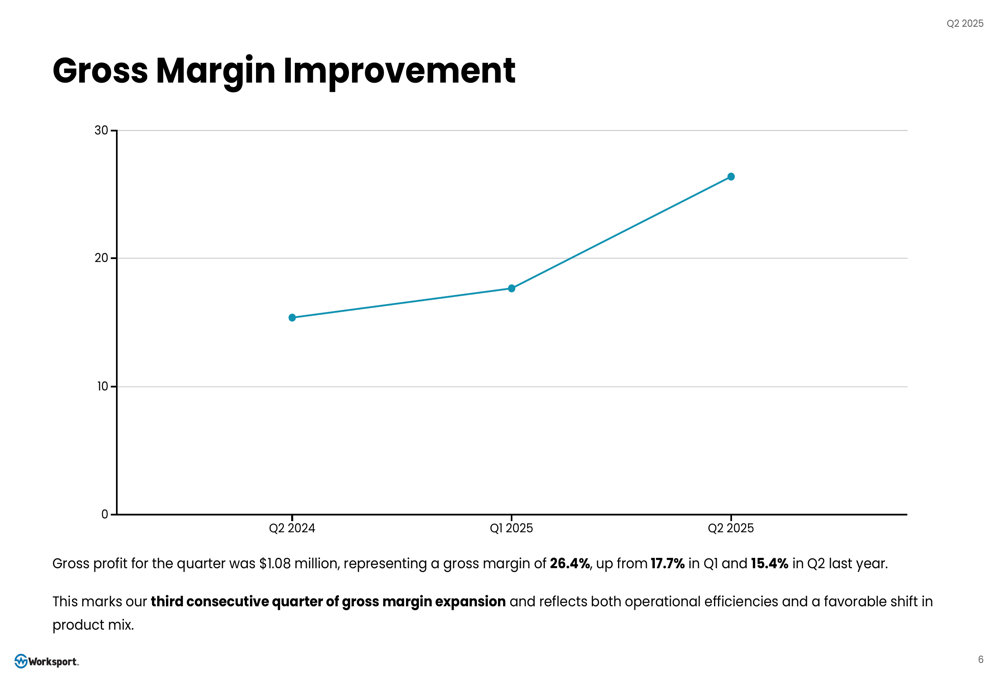

Gross profit for the quarter reached $1.08 million, representing a gross margin of 26.4%, up significantly from 17.7% in Q1 2025 and 15.4% in Q2 2024. This marks the third consecutive quarter of gross margin expansion and reflects both operational efficiencies and a favorable shift in product mix.

The margin improvement trajectory is illustrated in this chart:

Operating expenses were $4.70 million, up modestly from Q2 2024’s $4.21 million but essentially flat compared to Q1’s $4.65 million. The company reported a 15% improvement in operating loss to $(3.62) million, versus $(4.26) million in Q1, while R&D expenses decreased 71% year-over-year and G&A expenses declined 18% from the previous quarter.

Financial Position

Worksport ended the quarter with $1.39 million in cash and cash equivalents, down from $5.08 million at the end of March. However, the company reduced its cash burn by 19% to $(3.10) million from $(3.84) million in Q1, demonstrating progress toward operational efficiency.

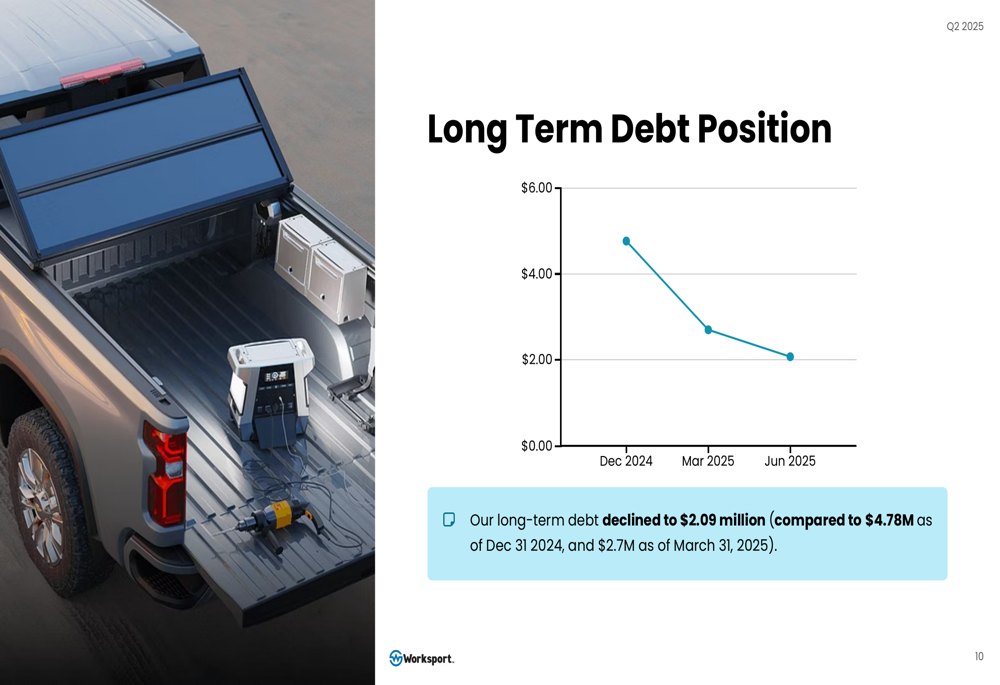

The company’s long-term debt position has improved significantly, declining to $2.09 million compared to $4.78 million at the end of December 2024 and $2.7 million at the end of March 2025, as shown in the following chart:

Inventory remained stable at $5.88 million, with a shift toward more raw materials and fewer finished goods, reflecting demand consistently outpacing production. The company noted that its inventory profile positions it to fulfill ongoing dealer and e-commerce demand without requiring significant near-term investment.

Operational Improvements

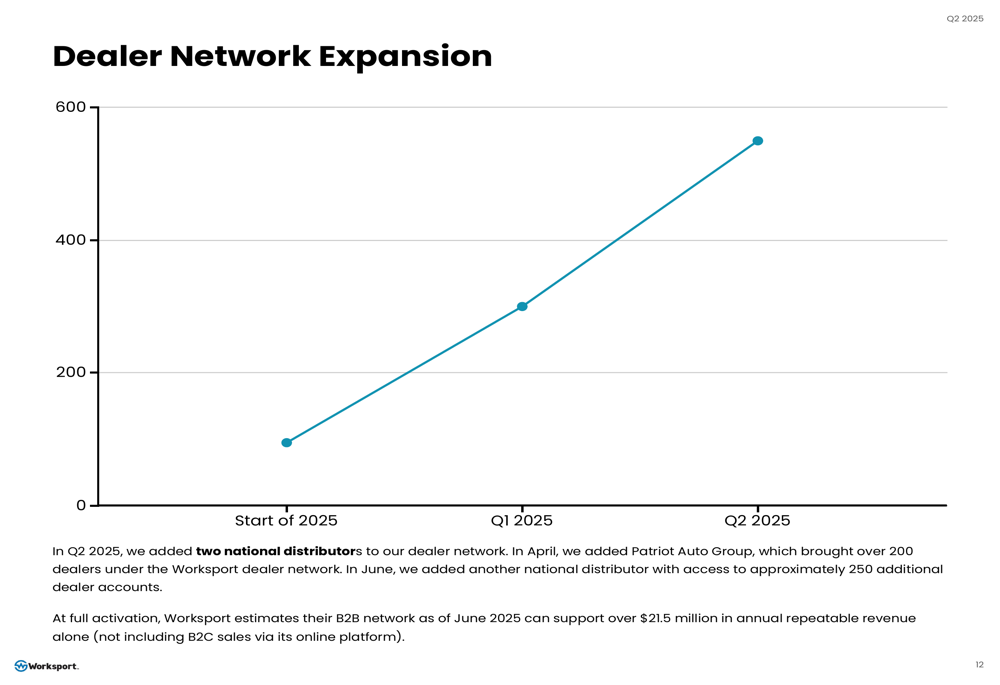

Worksport has made significant strides in expanding its dealer network, adding two national distributors in Q2 that brought over 450 additional dealers under the Worksport umbrella. At full activation, the company estimates its B2B network as of June 2025 can support over $21.5 million in annual repeatable revenue alone, not including direct-to-consumer sales.

The dealer network expansion is visualized in this graph:

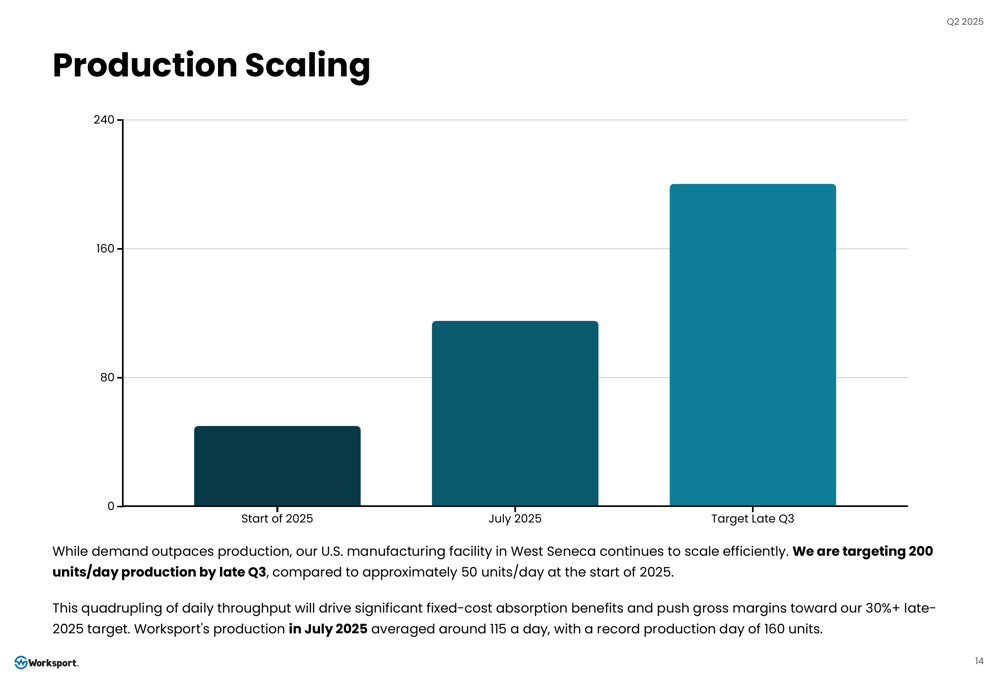

Production scaling has been a key focus, with the company targeting 200 units per day by late Q3 2025, compared to approximately 50 units per day at the start of the year. In July 2025, production averaged around 115 units per day, with a record day of 160 units. This quadrupling of daily throughput is expected to drive significant fixed-cost absorption benefits and push gross margins toward the company’s 30%+ late-2025 target.

The production scaling progress is illustrated here:

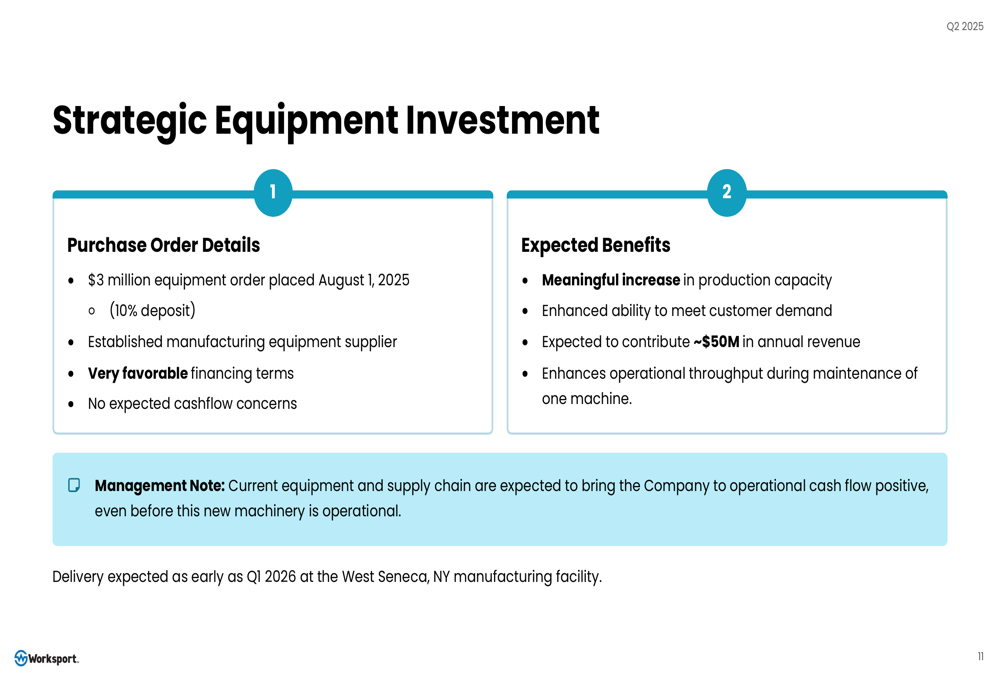

To support future growth, Worksport announced a strategic $3 million equipment order placed on August 1, 2025, with delivery expected as early as Q1 2026. The new equipment is expected to contribute approximately $50 million in annual revenue capacity once operational.

Innovation Pipeline

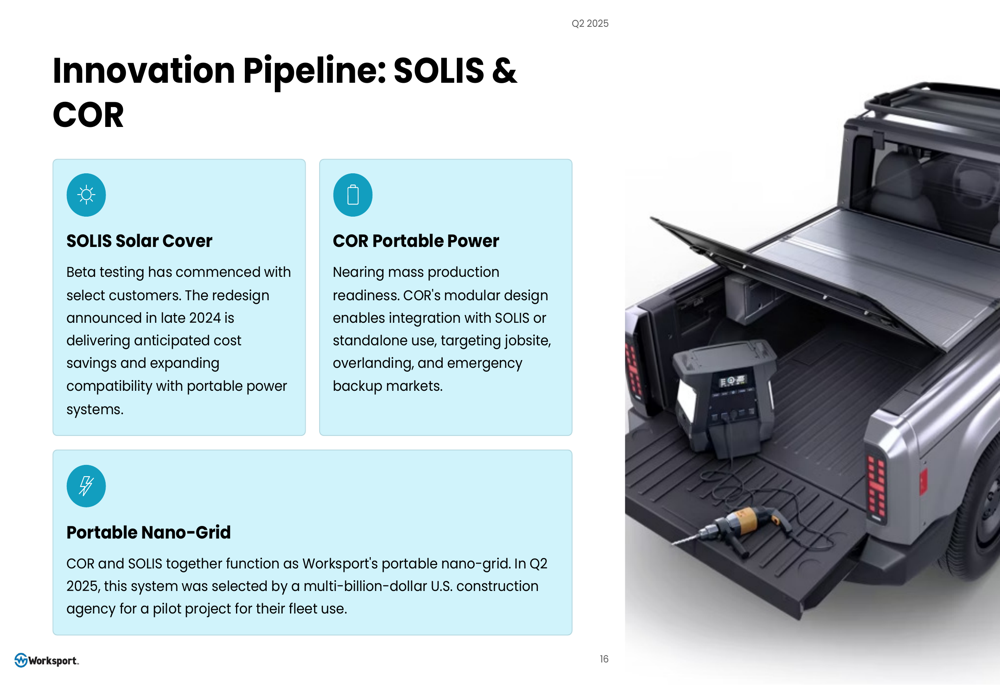

Worksport highlighted several new products in its innovation pipeline, including the HD3 Heavy-Duty Tonneau Cover scheduled for launch in Q3 2025. The company is also advancing its clean energy solutions, with beta testing commenced for the SOLIS Solar Cover and the COR Portable Power Station nearing mass production readiness.

The SOLIS and COR products are shown here:

In Q2 2025, the SOLIS and COR system was selected by a multi-billion-dollar U.S. construction agency for a pilot project for their fleet use, positioning Worksport within the fast-growing portable energy market.

Additionally, the company’s AetherLux heat pump technology, introduced in February 2025, has attracted significant interest. Management believes AetherLux could have a meaningful impact on Worksport’s 2026 balance sheet, supported by its position in the $123 billion global market.

Forward-Looking Guidance

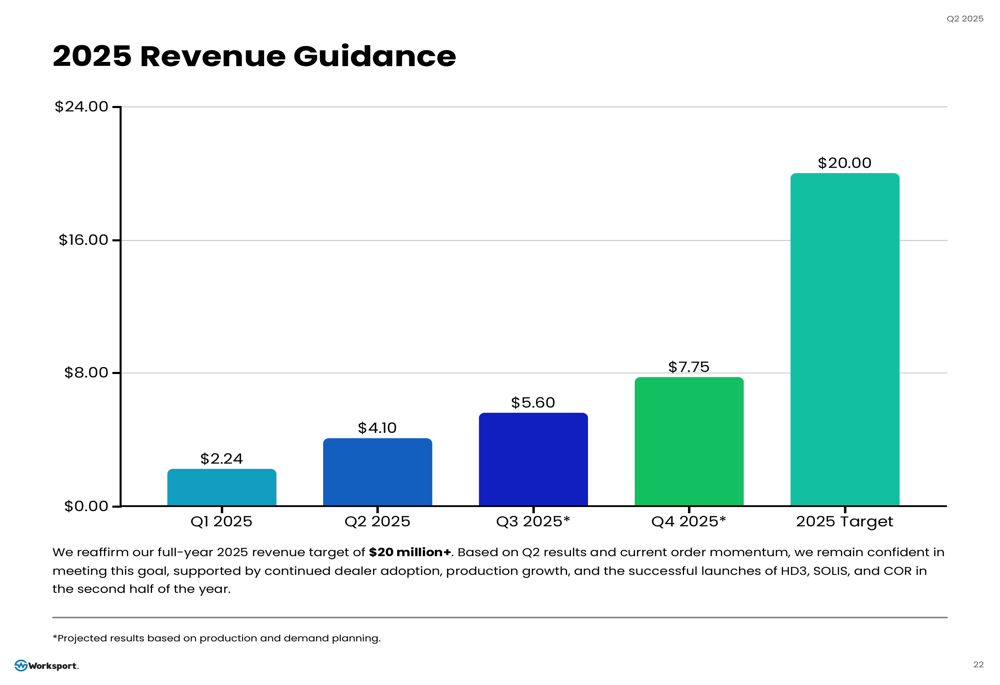

Worksport reaffirmed its full-year 2025 revenue target of over $20 million, with quarterly projections showing continued growth through the remainder of the year. The company expects Q3 2025 revenue of approximately $5.60 million and Q4 2025 revenue of $7.75 million.

The revenue guidance is outlined in this chart:

Gross margins are expected to reach 30%+ by year-end, with the company targeting breakeven by late Q4 2025 or early Q1 2026. Management identified three key profitability drivers for 2026: the core tonneau cover business, the COR & SOLIS energy products, and the AetherLux heat pump technology.

The company’s key achievements and priorities for the remainder of 2025 include:

Worksport’s management emphasized that while a successful launch of COR and SOLIS could accelerate profitability in 2026, they believe their core tonneau cover business alone can drive them into profitability next year. The company also noted its U.S. manufacturing advantage with 90% domestic parts, which helps mitigate tariff impacts that are affecting competitors more severely.

Despite the strong quarterly results and positive outlook, investors should note that Worksport’s stock declined significantly following the earnings announcement, suggesting market skepticism about the company’s ability to execute on its ambitious growth plans or concerns about broader economic conditions affecting the automotive accessories market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.