Oklo stock tumbles as Financial Times scrutinizes valuation

Introduction & Market Context

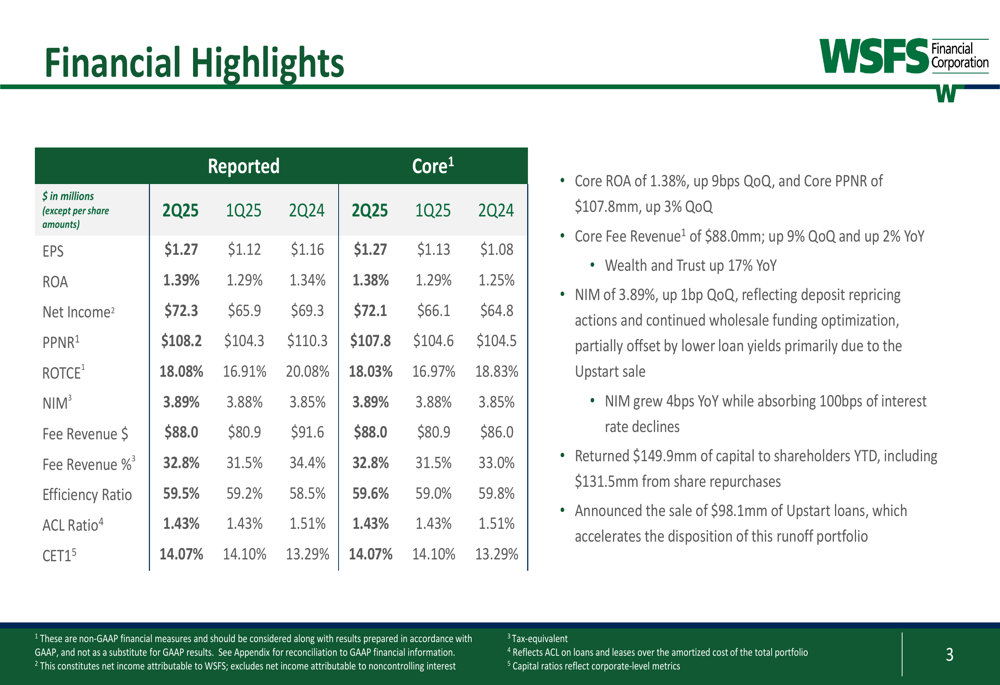

WSFS Financial Corporation (NASDAQ:WSFS) reported solid second-quarter 2025 results, demonstrating resilience in a challenging interest rate environment. The company posted core earnings per share of $1.27 and a core return on assets (ROA) of 1.38%, up 9 basis points quarter-over-quarter. Trading at approximately $53 per share, WSFS has shown a 2.68% increase following the earnings release, reflecting positive market reception to the company’s performance and outlook.

Quarterly Performance Highlights

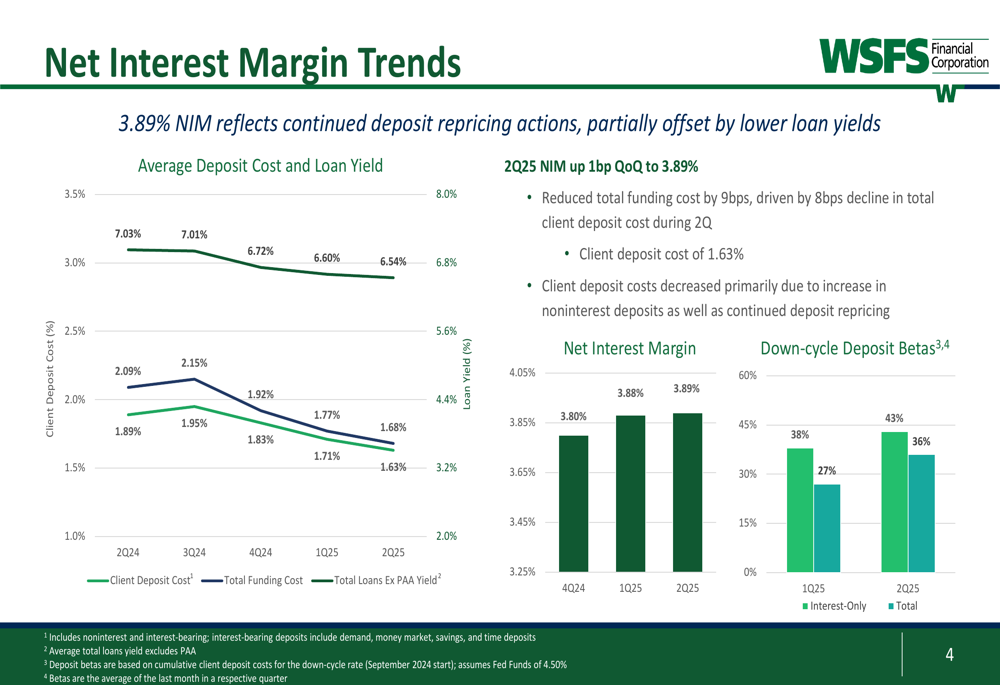

WSFS delivered strong financial performance across key metrics in the second quarter. Core ROA reached 1.38%, while core return on tangible common equity (ROTCE) stood at an impressive 18.03%. The company maintained a stable net interest margin (NIM) of 3.89%, up 1 basis point from the previous quarter, despite continued deposit repricing pressures.

As shown in the following financial highlights summary, the company’s performance remained solid across multiple metrics:

Fee revenue was particularly strong at $88.0 million, representing a 9% increase quarter-over-quarter and comprising 32.8% of total revenue. The efficiency ratio remained well-controlled at 59.5%, supporting overall profitability.

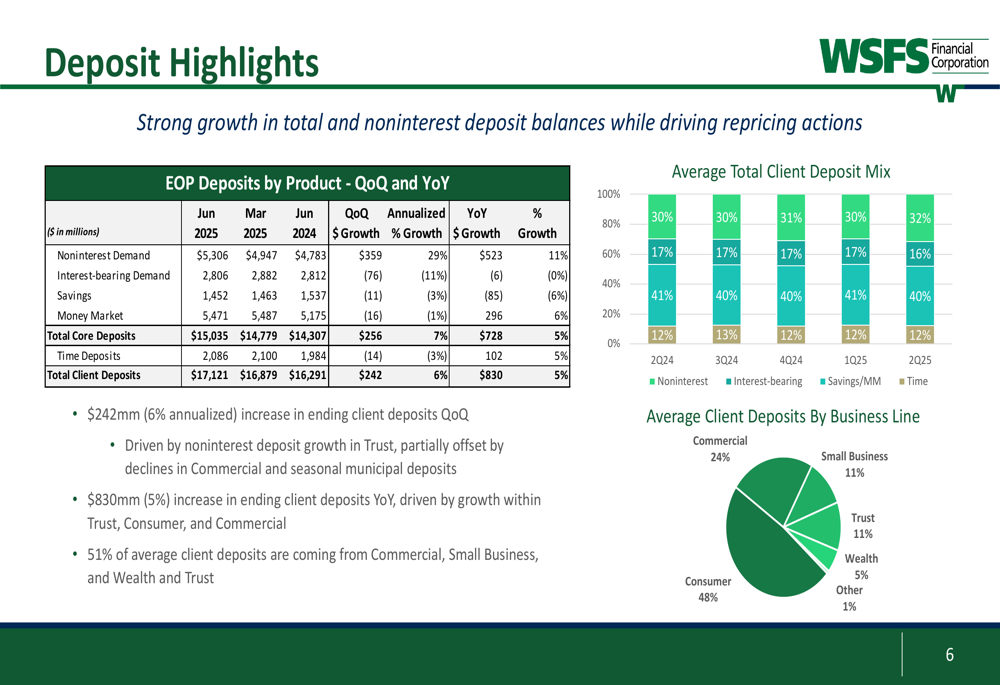

Deposit Growth and Funding

WSFS reported robust deposit growth, with total client deposits increasing by $242 million (6% annualized) quarter-over-quarter and $830 million (5%) year-over-year. Notably, noninterest demand deposits grew by $359 million quarter-over-quarter, representing a substantial 29% annualized growth rate.

The company’s deposit base remains well-diversified across business lines, with consumer deposits representing 48% of the total, followed by commercial (24%), small business (11%), and trust (11%).

As illustrated in the deposit trends chart below, WSFS has successfully grown its deposit base while managing deposit costs:

The net interest margin remained stable at 3.89%, supported by declining deposit costs. Client deposit costs decreased by 8 basis points quarter-over-quarter to 1.63%, while total funding costs fell by 9 basis points. The company’s down-cycle deposit beta of 27% (interest-only) and 36% (total) in Q2 2025 demonstrates effective cost management in a declining rate environment.

Loan Portfolio and Credit Quality

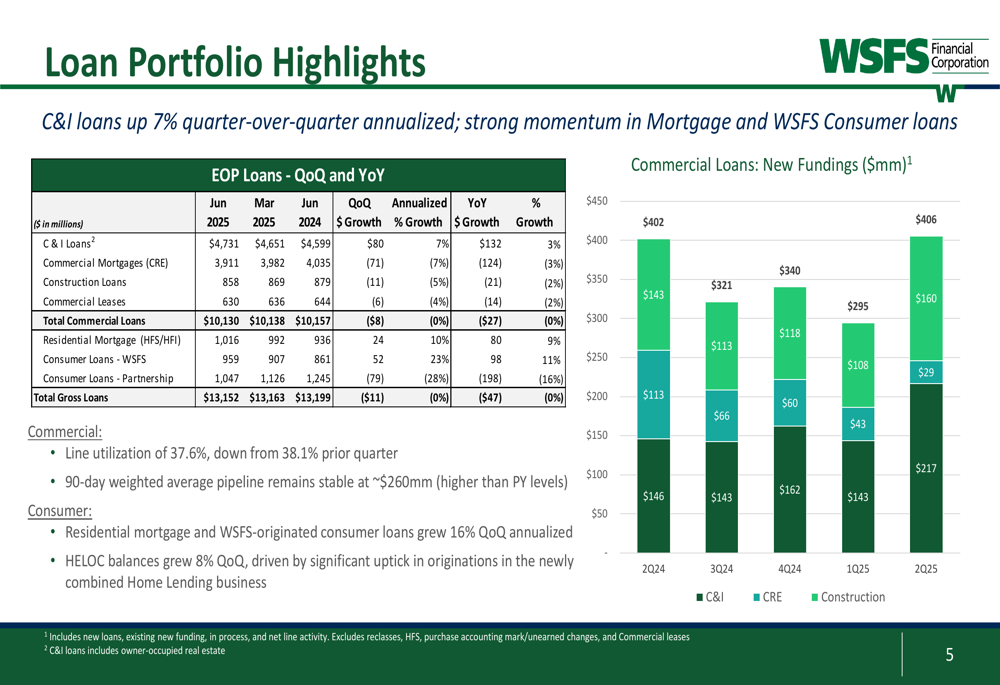

WSFS’s loan portfolio remained relatively flat overall, with total gross loans at $13.15 billion. However, there were notable shifts within the portfolio. Commercial and industrial (C&I) loans grew by 7% quarter-over-quarter annualized, while residential mortgage and WSFS consumer loans increased by 10% and 23% annualized, respectively.

The following chart illustrates the loan portfolio composition and growth trends:

Credit quality metrics remained stable. The allowance for credit losses (ACL) ratio stood at 1.43%, providing adequate coverage for potential loan losses. Nonperforming assets decreased by 6 basis points quarter-over-quarter to 0.51%, primarily driven by the payoff of a C&I loan without additional losses. Net charge-offs decreased significantly to 0.04% from 0.30% in the previous quarter.

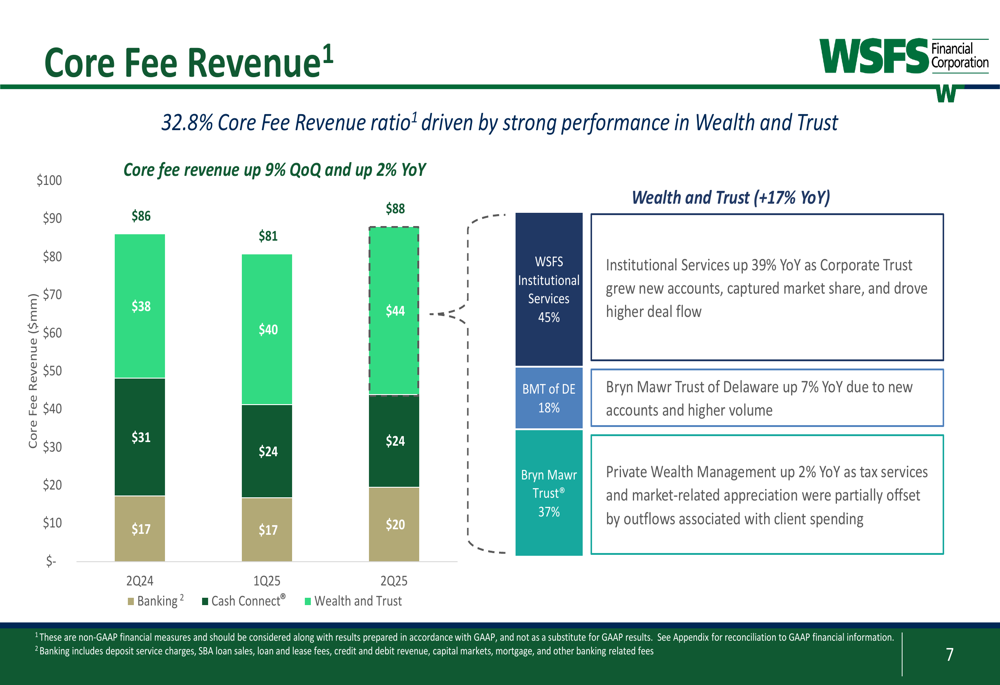

Fee Income and Wealth Management

A standout performer for WSFS was its fee-based business, particularly wealth management and trust services. These segments collectively accounted for 55% of core fee revenue, with Institutional Services growing by an impressive 39% year-over-year.

The following chart breaks down the company’s core fee revenue by business segment:

Wealth and Trust revenue increased to $44 million in Q2 2025, up from $40 million in the previous quarter and $38 million in Q2 2024. This growth was driven by new accounts, higher volume, and market-related appreciation, partially offset by outflows associated with client spending.

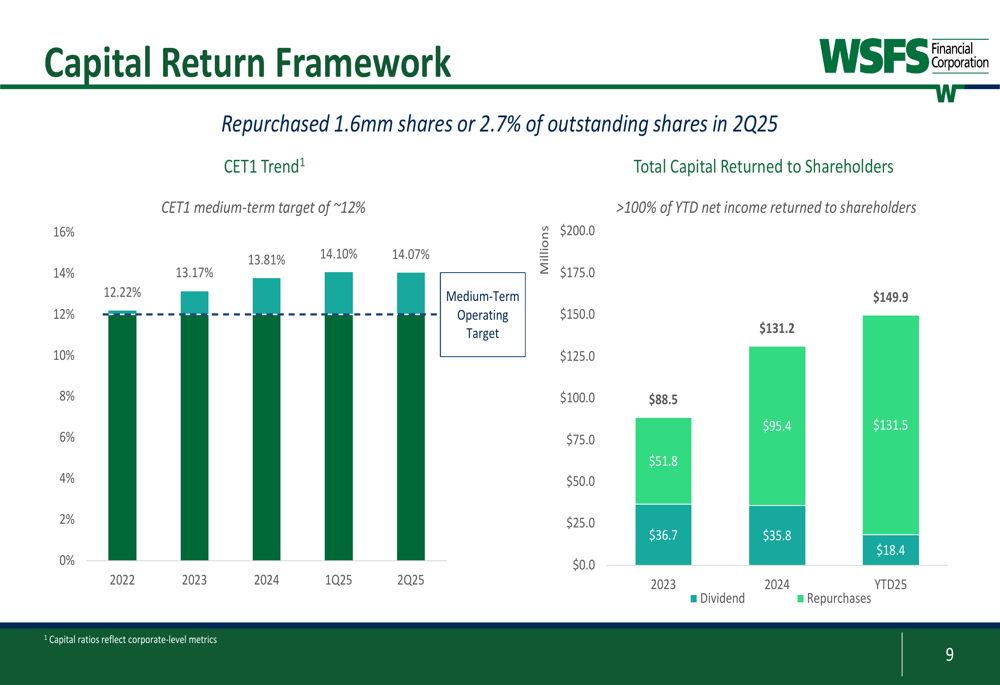

Capital Management and Shareholder Returns

WSFS maintained strong capital ratios, with Common Equity Tier 1 (CET1) at 14.07%, significantly above the "well-capitalized" threshold. This capital strength has enabled the company to continue its aggressive share repurchase program, buying back 1.6 million shares (2.7% of outstanding shares) in Q2 2025.

Year-to-date, WSFS has returned $149.9 million to shareholders through dividends ($18.4 million) and share repurchases ($131.5 million), representing more than 100% of year-to-date net income.

The company’s capital return framework is illustrated below:

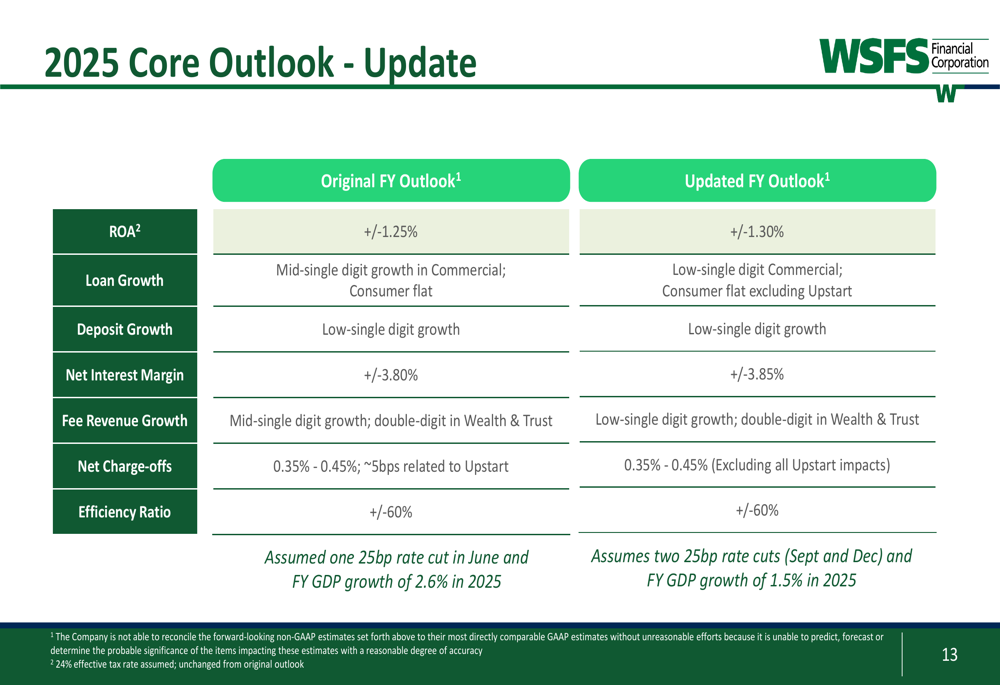

Updated 2025 Outlook

Based on the strong first-half performance, WSFS has raised its full-year 2025 guidance. The company now expects core ROA of approximately 1.30%, up from the previous guidance of approximately 1.25%. Net interest margin is projected to be around 3.85%, compared to the earlier estimate of 3.80%.

The updated outlook assumes two 25 basis point rate cuts (September and December) and full-year GDP growth of 1.5% in 2025, as shown in the following guidance table:

WSFS continues to expect low single-digit growth in its commercial portfolio, while the consumer portfolio is anticipated to remain flat, excluding Upstart. Fee revenue is projected to show low single-digit growth overall, with double-digit growth in Wealth and Trust segments.

Conclusion

WSFS Financial Corporation’s Q2 2025 results demonstrate the company’s ability to navigate a challenging interest rate environment while delivering solid financial performance. The combination of deposit growth, stable net interest margin, strong fee income growth, and aggressive capital return positions WSFS well for the remainder of 2025.

The company’s strategic focus on wealth management and trust services continues to pay dividends, providing a diversified revenue stream that complements its traditional banking operations. With an improved outlook for the full year and strong capital position, WSFS appears well-positioned to continue delivering value to shareholders despite potential economic headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.