NVIDIA launches Jetson Thor robotics computers for physical AI systems

Introduction & Market Context

WSP Global Inc. (TSX:WSP) presented its first quarter 2025 financial results on May 7, 2025, showcasing strong performance with double-digit growth across key metrics. The engineering and professional services firm reported significant revenue expansion and margin stability despite facing regional challenges, particularly in the Asia-Pacific market.

Following the earnings announcement, WSP’s stock initially rose 1.91%, though recent trading shows a 1% decline from its previous close of $278.69. The company currently trades at a premium to its fair value according to analyst estimates, with the stock delivering a 6.91% return over the past year.

Quarterly Performance Highlights

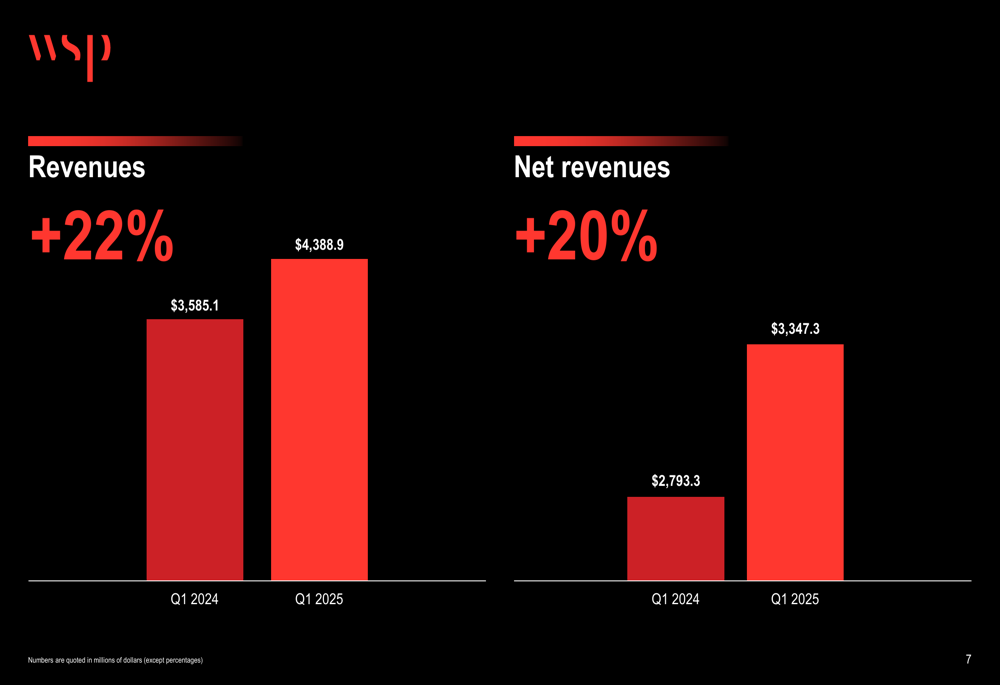

WSP reported robust financial results for Q1 2025, with net revenues reaching $3.35 billion, representing a 19.8% increase compared to the same period in 2024. The company achieved organic growth in net revenues of 3.7%, which adjusts to approximately 5.5% when normalized for fewer billable days in the US market.

As shown in the following chart of revenue and net revenue growth:

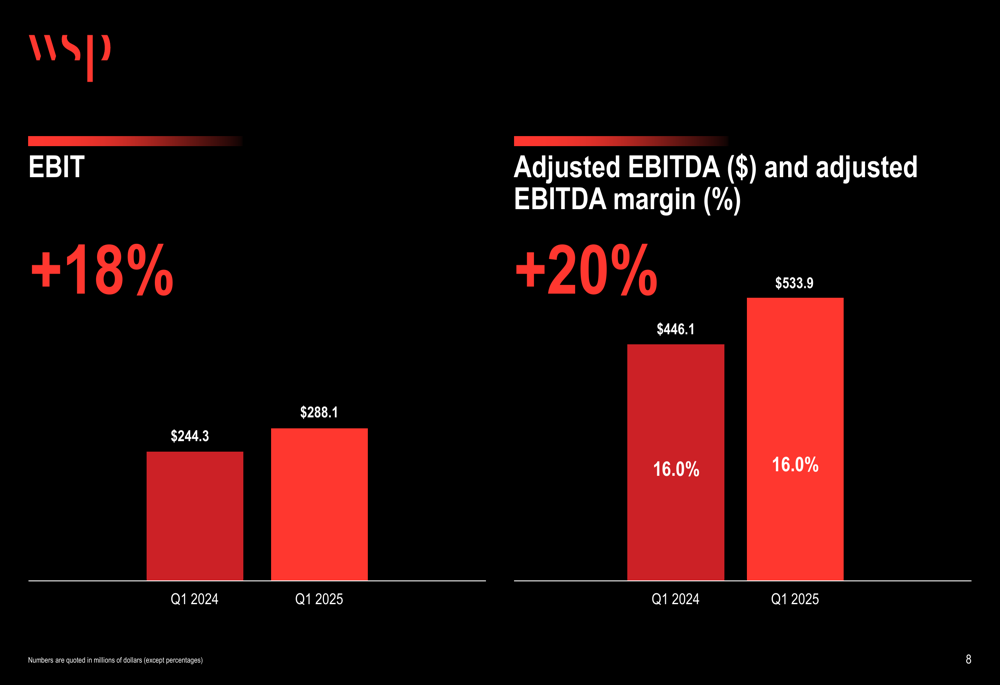

The company’s adjusted EBITDA grew by 19.7% year-over-year to $533.9 million, maintaining a stable margin of 16.0%. Earnings before interest and taxes (EBIT) increased by 17.9% to $288.1 million compared to Q1 2024.

The following chart illustrates the growth in EBIT and adjusted EBITDA:

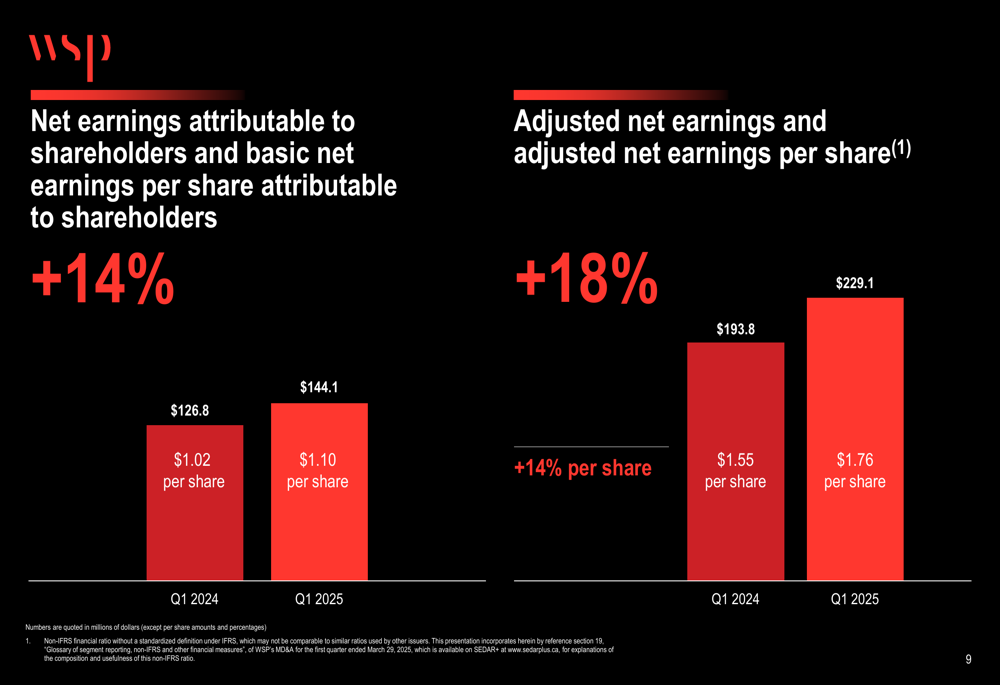

WSP’s adjusted net earnings rose 18.2% to $229.1 million, resulting in adjusted earnings per share of $1.76, up from $1.55 in the same quarter last year. Net earnings attributable to shareholders increased by 13.6% to $144.1 million ($1.10 per share).

The company’s earnings performance is detailed in this chart:

Detailed Financial Analysis

A key highlight of WSP’s Q1 2025 results was the significant improvement in free cash flow, which reached $115.9 million, representing an increase of $241.1 million compared to Q1 2024. This enhancement reflects the company’s focus on operational efficiency and working capital management.

The company’s backlog reached a record $16.6 billion, representing 11.3 months of revenues and a 16.6% increase over the twelve-month period. This robust backlog provides strong visibility for future revenue streams and indicates continued client confidence in WSP’s service offerings.

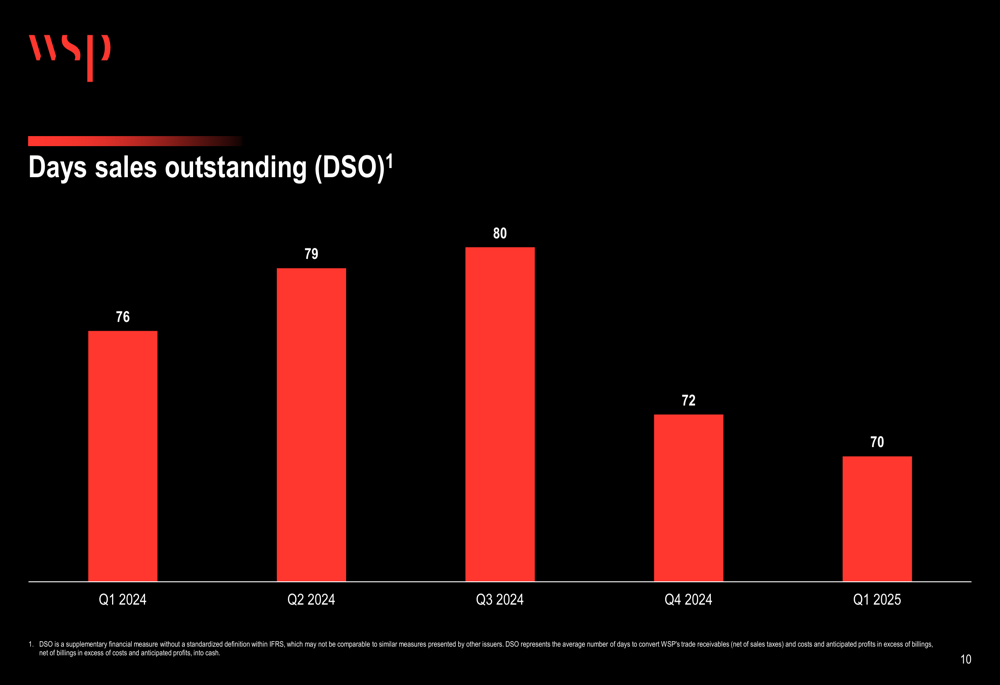

Days Sales Outstanding (DSO) improved to 70 days in Q1 2025, continuing a positive trend from 76 days in Q1 2024 and 72 days in Q4 2024. This improvement in collection efficiency contributes to the company’s stronger cash flow position.

WSP maintains a diversified business model across four core end-markets: Earth & Environment, Power & Energy, Transport & Infrastructure, and Property & Buildings. This diversification strategy has helped the company secure significant projects, including engineering consultant services for the reconstruction of the Francis Scott Key Bridge and the development of shore power systems at PortMiami.

The company’s diversified end-market exposure is illustrated in the following slide:

Regional Performance Analysis

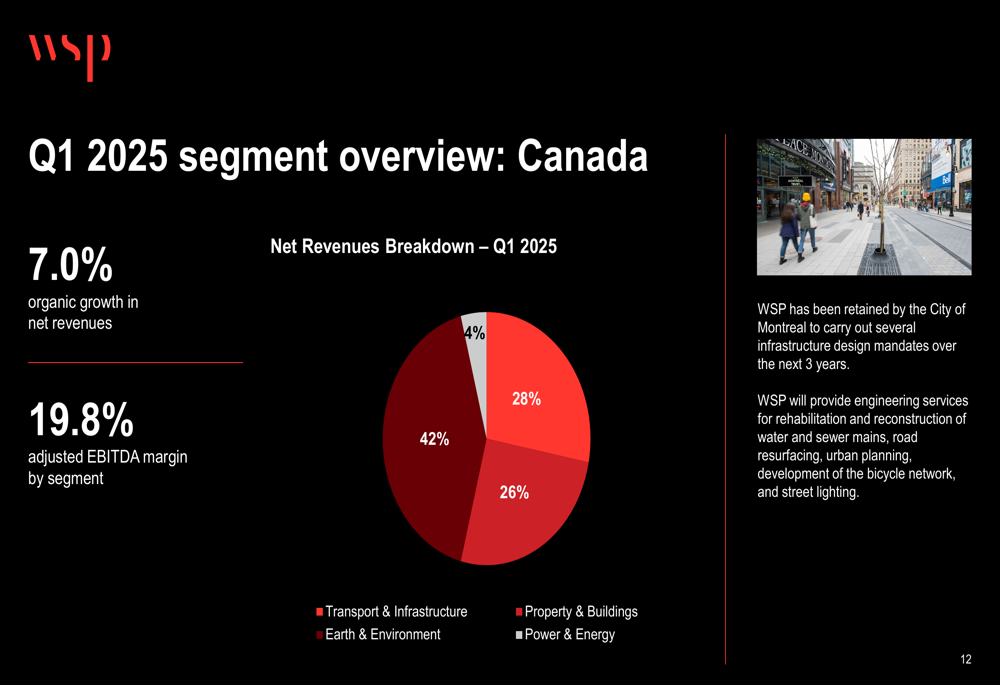

WSP’s performance varied significantly across its geographic segments in Q1 2025. The Canadian operations delivered strong organic growth of 7.0% with an adjusted EBITDA margin of 19.8%. The Canadian market shows a balanced revenue distribution with Transport & Infrastructure (42%) and Property & Buildings (28%) as the largest segments.

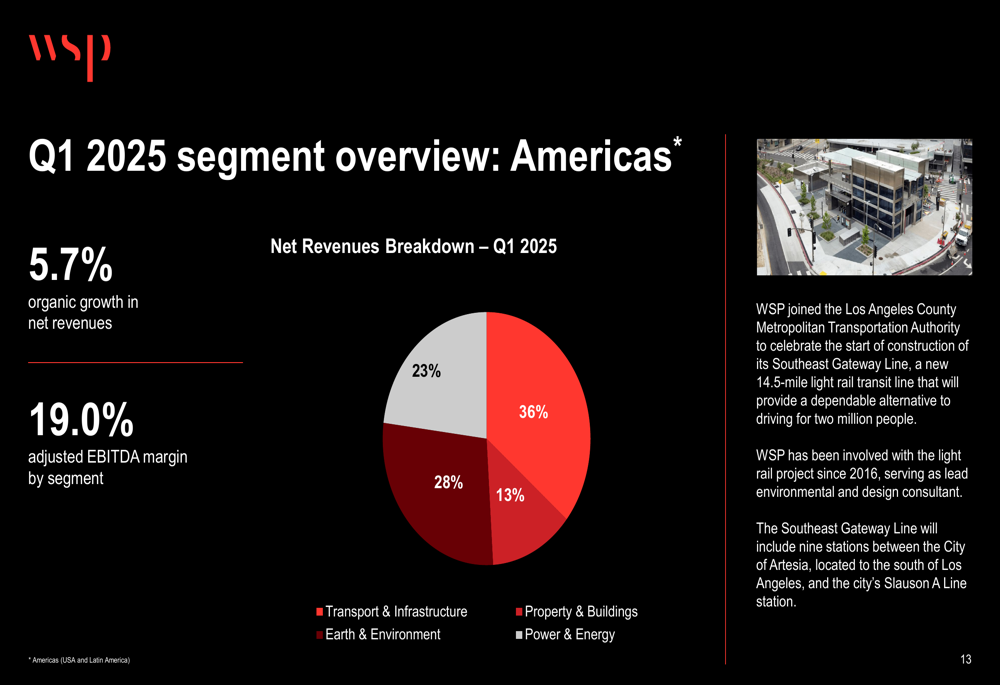

The Americas segment (USA and Latin America) also performed well with 5.7% organic growth and a 19.0% adjusted EBITDA margin. This region shows a different mix, with Property & Buildings (36%) and Transport & Infrastructure (28%) leading the revenue breakdown.

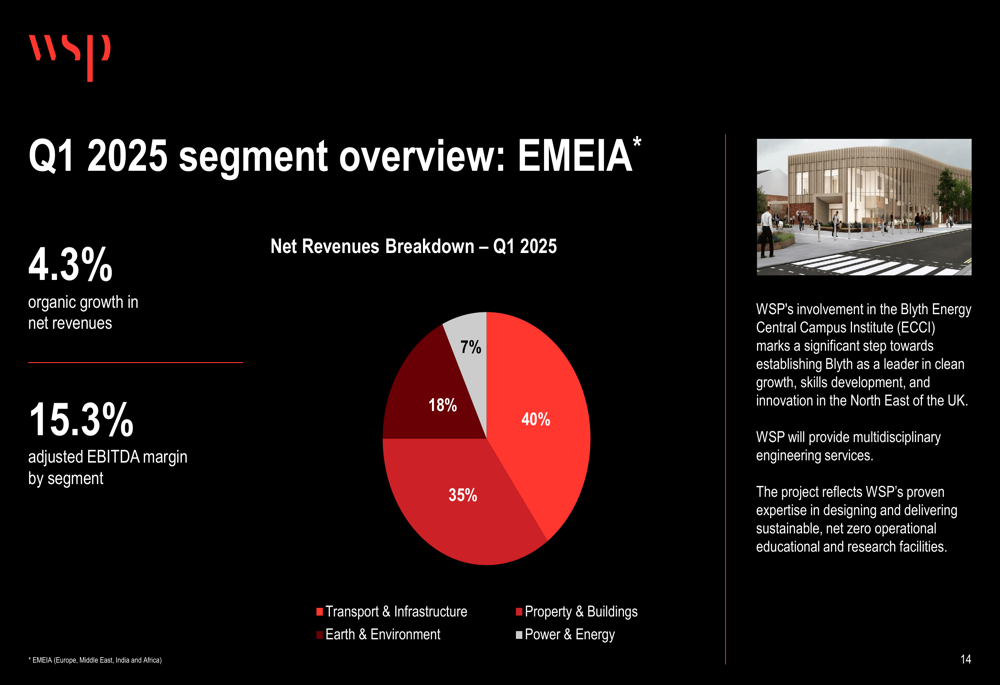

The EMEIA region (Europe, Middle East, India, and Africa) achieved 4.3% organic growth with a 15.3% adjusted EBITDA margin. Property & Buildings represents the largest sector at 40% of net revenues, followed by Transport & Infrastructure at 35%.

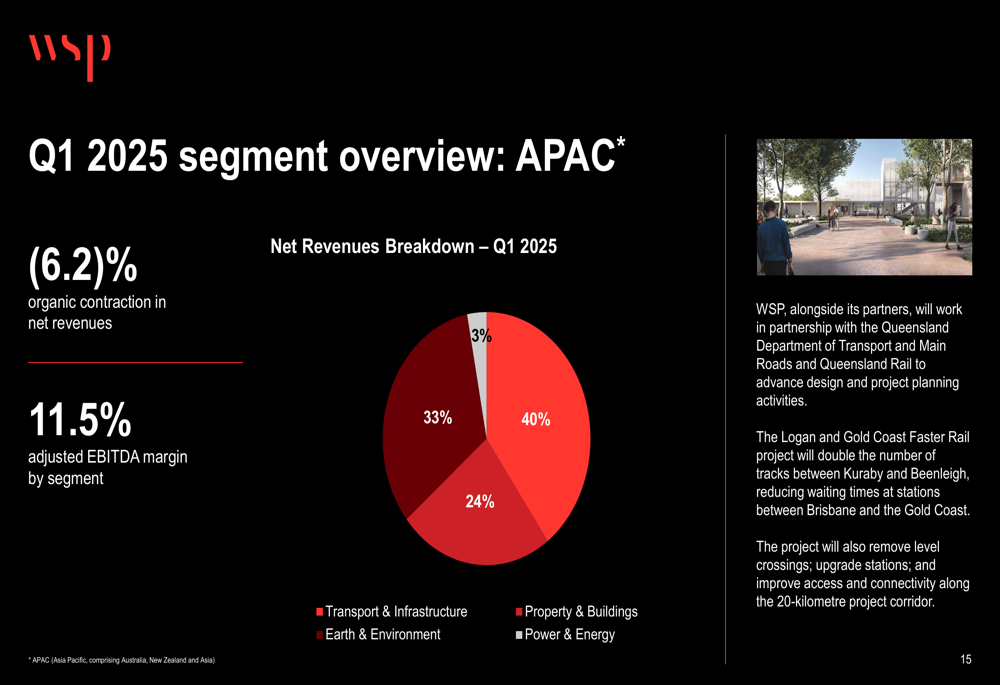

In contrast, the APAC region (Asia Pacific, Australia, New Zealand, and Asia) experienced an organic contraction of 6.2% with an adjusted EBITDA margin of 11.5%, significantly lower than other regions. This underperformance reflects ongoing challenges in the Asia-Pacific market that the company is addressing through operational adjustments.

Strategic Initiatives & Outlook

WSP has reaffirmed its full-year financial outlook despite the challenges in the APAC region, expressing cautious optimism about recovery in that market. The company continues to focus on high-growth areas and advisory services, leveraging its diversified platform to navigate regional variations in market conditions.

According to the earnings call, President and CEO Alexandre Roux emphasized the company’s proactive approach, stating, "We are being proactive and taking the appropriate steps where and when needed." He highlighted the resilience of WSP’s business model, noting that "The beauty of WSP model is one that is based on diversification."

While the company maintains a positive outlook, some analysts have revised their earnings expectations downward for upcoming periods, and there are projections of potential sales decline in the current year. Currency exposure, particularly in APAC and EMEA regions, remains a risk factor that could impact future financial results.

WSP’s strong cash flow improvement and record backlog, however, position the company well to weather these challenges while continuing to pursue strategic growth opportunities in its core markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.