Street Calls of the Week

Introduction & Market Context

Xerox (NASDAQ:XRX) Holdings Corporation (NYSE:XRX) presented its Q2 2025 earnings results on July 31, 2025, revealing widening losses and continued revenue challenges as the company doubles down on its transformation strategy. The stock reacted negatively to the results, with shares trading down 1.53% to $5.14 in premarket trading after closing at $5.22 the previous day, representing a 5.09% decline. The company’s stock has fallen significantly from its 52-week high of $11.42, hovering just above its 52-week low of $3.44.

The presentation comes at a critical juncture for Xerox, which recently completed its acquisition of Lexmark in July 2025, a move the company positions as central to its reinvention strategy and future growth prospects.

Quarterly Performance Highlights

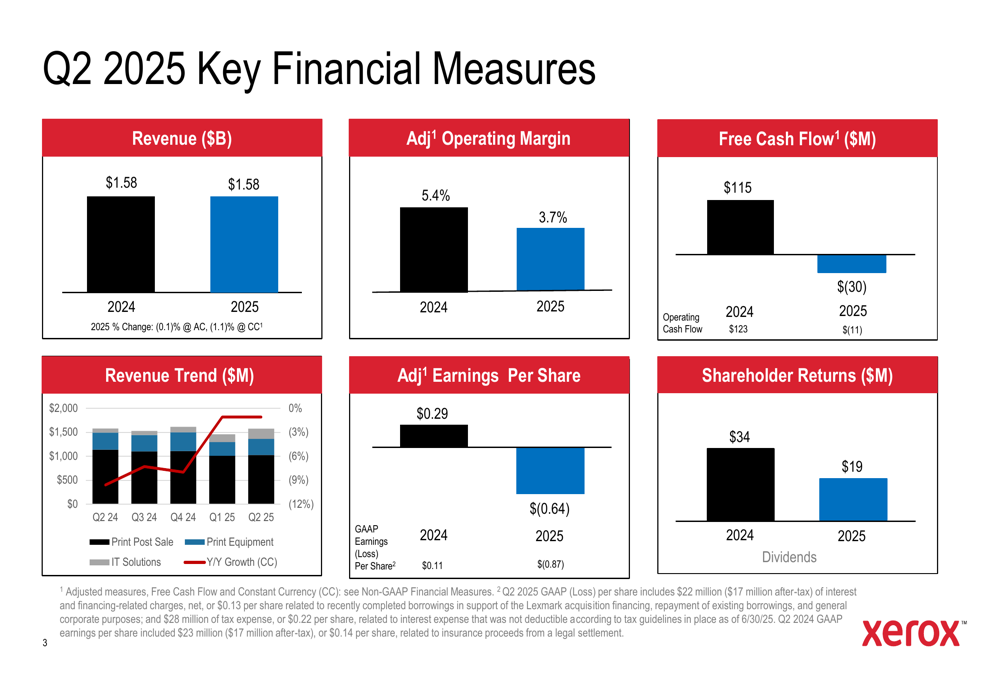

Xerox reported Q2 2025 revenue of $1.58 billion, essentially flat with a 0.1% decrease at actual currency and a 1.1% decrease at constant currency compared to Q2 2024. However, the company’s profitability metrics showed significant deterioration year-over-year.

As shown in the following financial summary from the presentation:

Adjusted operating margin fell to 3.7% from 5.4% in the prior year, while free cash flow plunged to negative $30 million compared to positive $115 million in Q2 2024. The company’s adjusted earnings per share dropped to negative $0.64 from positive $0.29 in the same quarter last year, while GAAP earnings per share declined to negative $0.87 from positive $0.11.

The revenue trend chart included in the presentation revealed a concerning year-over-year decline of approximately 12% at constant currency for Q2 2025, with weakness across print equipment, print post-sale, and IT solutions segments. Shareholder returns in the form of dividends also decreased to $19 million from $34 million in the prior year period.

These results continue a troubling trend seen in Q1 2025, when the company reported an adjusted loss per share of $0.06 and revenue of $1.46 billion, both below analyst expectations.

Strategic Initiatives

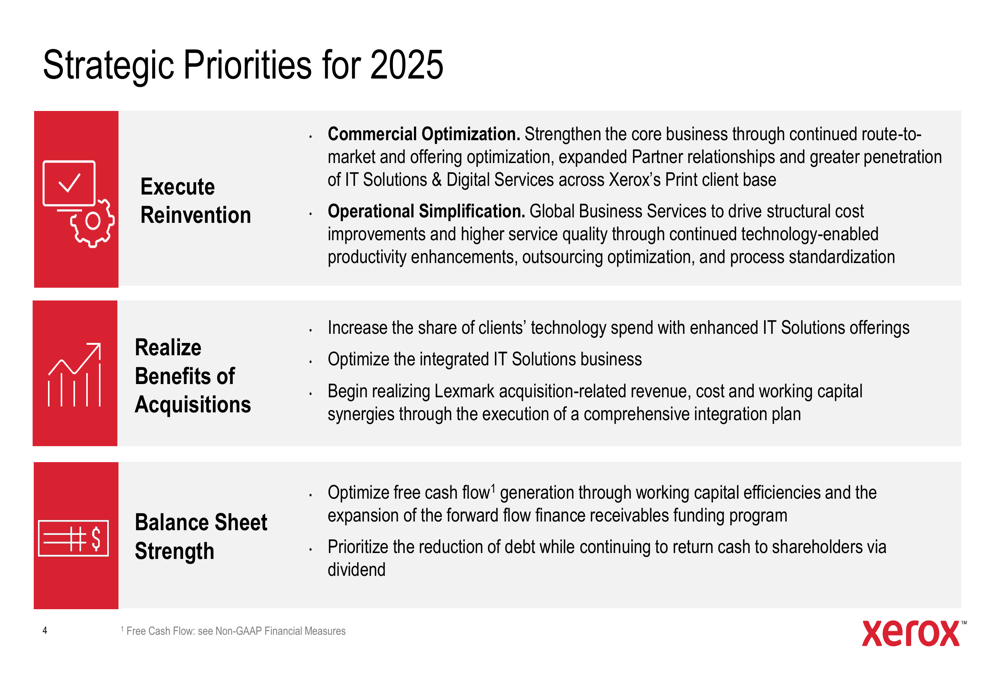

Xerox outlined three key strategic priorities for 2025, focusing on executing its reinvention plan, realizing benefits from acquisitions, and strengthening its balance sheet:

The company’s reinvention strategy encompasses commercial optimization to strengthen core business and operational simplification to drive structural cost improvements. Management highlighted progress across multiple phases of this plan, including non-core divestitures in 2023, organizational redesign in January 2024, the acquisition of ITsavvy in November 2024, and most recently, the acquisition of Lexmark in July 2025.

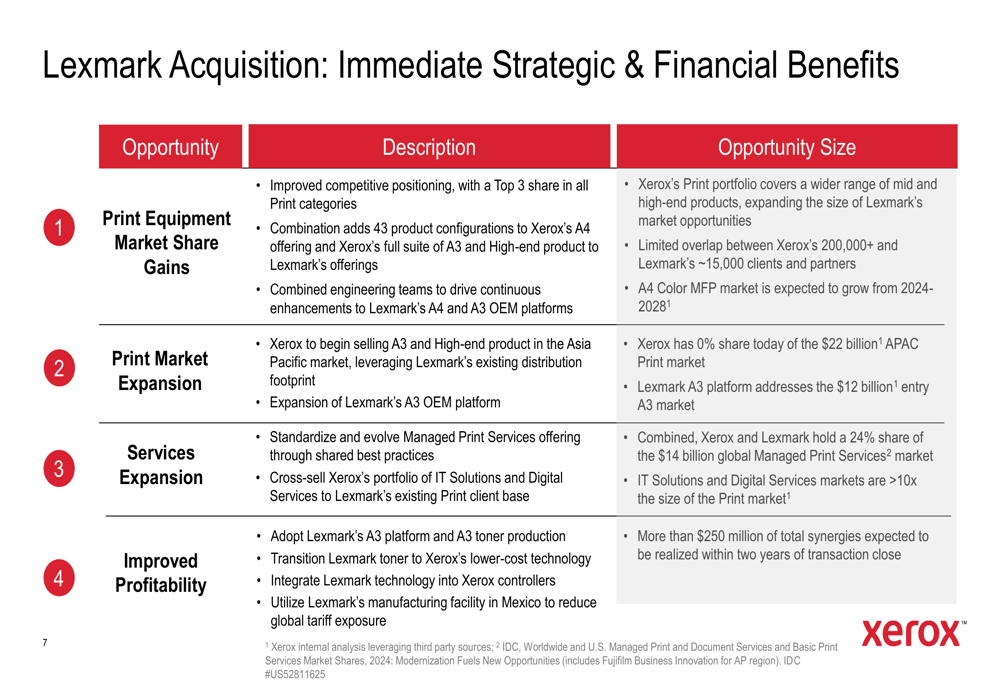

The Lexmark acquisition represents a cornerstone of Xerox’s transformation strategy, with the company expecting to derive significant strategic and financial benefits:

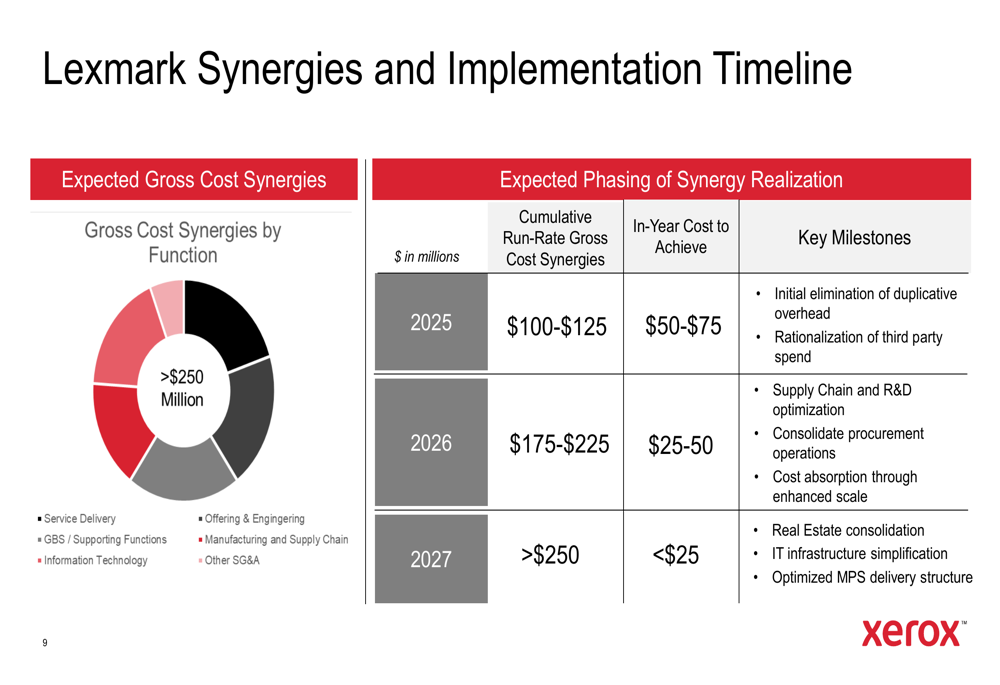

Xerox projects more than $250 million in synergies to be realized within two years of the transaction closing. These synergies are expected to come from print equipment market share gains, print market expansion into Asia Pacific, services expansion through standardized managed print services, and improved profitability through platform adoption and manufacturing optimization.

Forward-Looking Statements

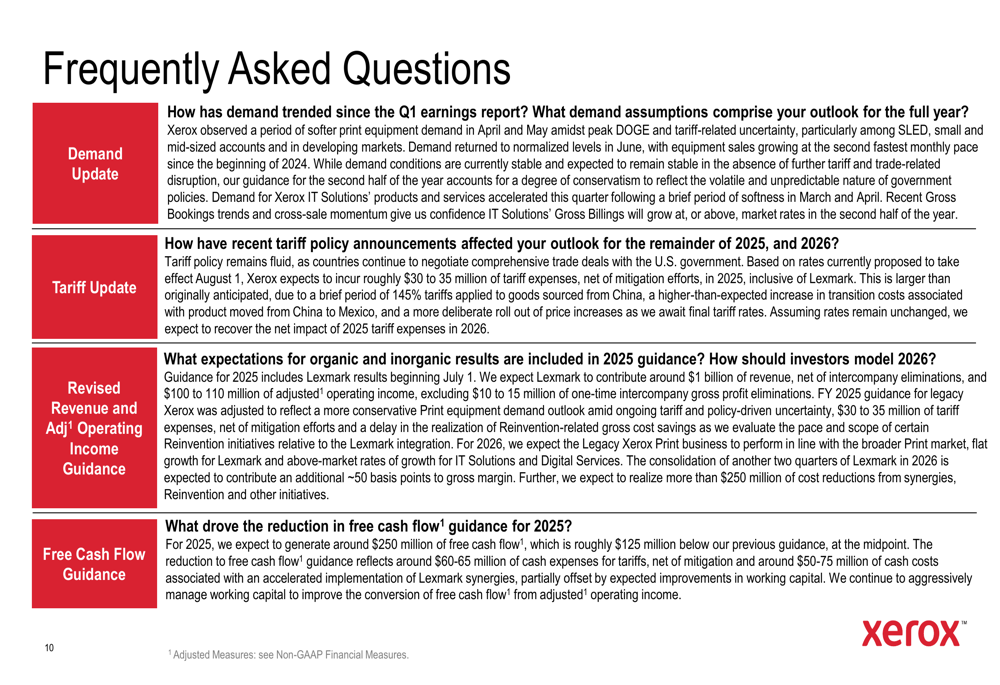

Xerox’s presentation addressed several key investor concerns in its FAQ section, including demand trends, tariff impacts, and revised guidance:

Management noted softer demand in April and May with a return to normalized levels in June. The company also addressed recent tariff policy announcements, estimating tariff expenses of $30-35 million in 2025. These tariffs, along with accelerated Lexmark synergy implementation costs, contributed to a reduction in free cash flow guidance for 2025.

The company provided a detailed timeline for realizing Lexmark synergies, projecting cumulative run-rate cost synergies of $100-125 million in 2025, $175-225 million in 2026, and over $250 million by 2027:

Implementation costs are expected to be front-loaded, with $50-75 million in 2025, $25-50 million in 2026, and less than $25 million in 2027. Key milestones include initial elimination of overhead, supply chain optimization, procurement consolidation, real estate consolidation, delivery structure optimization, and IT simplification.

Competitive Industry Position

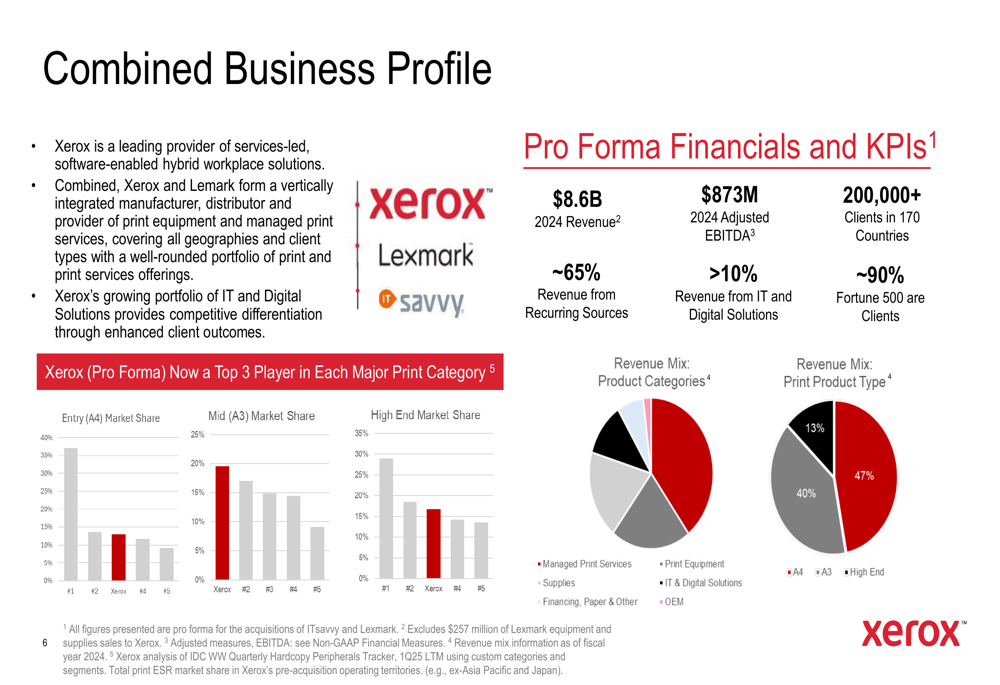

The presentation highlighted Xerox’s combined business profile following the Lexmark acquisition, positioning the company as a leading provider of services-led, software-enabled hybrid workplace solutions:

The pro forma business boasts impressive scale, with $8.6 billion in 2024 revenue, $873 million in 2024 adjusted EBITDA, approximately 65% of revenue coming from recurring sources, and more than 10% from IT and digital solutions. Xerox serves over 200,000 clients in 170 countries, including approximately 90% of Fortune 500 companies.

The combined entity is positioned as a top three player in Entry (A4), Mid (A3), and High-End Print Categories, with a diversified revenue mix across product categories and print product types. This enhanced market position is expected to help Xerox compete more effectively in the evolving print and digital solutions landscape.

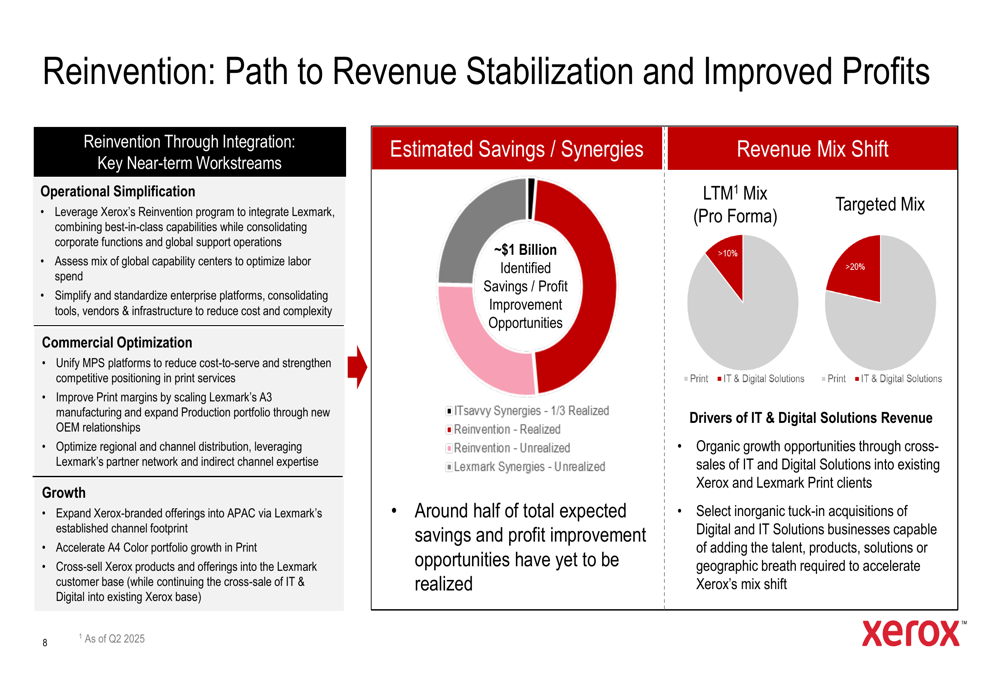

Looking ahead, Xerox aims to shift its revenue mix to increase the proportion of IT and digital solutions, which offer higher growth potential than traditional print businesses:

The company has identified approximately $1 billion in savings and profit improvement opportunities, with around half yet to be realized. These include ITsavvy synergies (one-third realized), reinvention initiatives (partially realized), and Lexmark synergies (newly identified).

Despite these ambitious plans, investors remain cautious as Xerox continues to face significant challenges in executing its transformation while navigating a difficult market environment. The company’s ability to successfully integrate Lexmark and deliver on promised synergies will be crucial to reversing its financial performance decline and rebuilding investor confidence in the quarters ahead.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.