SoFi stock falls after announcing $1.5B public offering of common stock

Introduction & Market Context

XL Axiata Tbk PT (EXCL) presented its Q1 2025 financial results on May 6, revealing a company navigating significant market challenges while implementing strategic changes. The Indonesian telecommunications provider reported modest revenue growth despite competitive pressures, with its stock closing down 2.27% at IDR 2,150 following the presentation.

The quarter marked a pivotal moment for the company, now operating under the XLSMART brand following its merger with First Media, which was completed on April 16, 2025. Management characterized the period as one of "navigating market headwinds" while focusing on operational discipline and merger integration.

Quarterly Performance Highlights

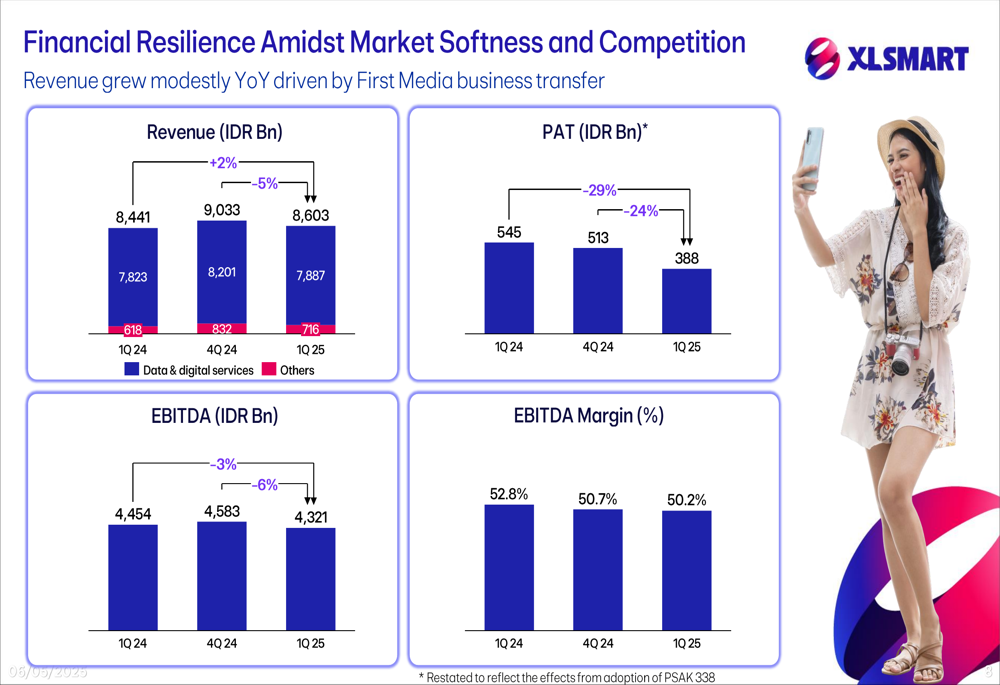

XLSMART delivered a mixed financial performance in Q1 2025. The company achieved 2% year-over-year revenue growth, reaching IDR 8,603 billion, though this represented a 5% decline from the previous quarter. The growth was primarily attributed to the First Media business transfer.

As shown in the following chart of quarterly financial metrics:

Despite the revenue increase, profitability metrics showed downward pressure. EBITDA declined 3% year-over-year to IDR 4,321 billion, with the EBITDA margin contracting to 50.2% from 52.8% in Q1 2024. More concerning was the 29% year-over-year drop in Profit After Tax (PAT) to IDR 388 billion, representing a 24% sequential decline from Q4 2024.

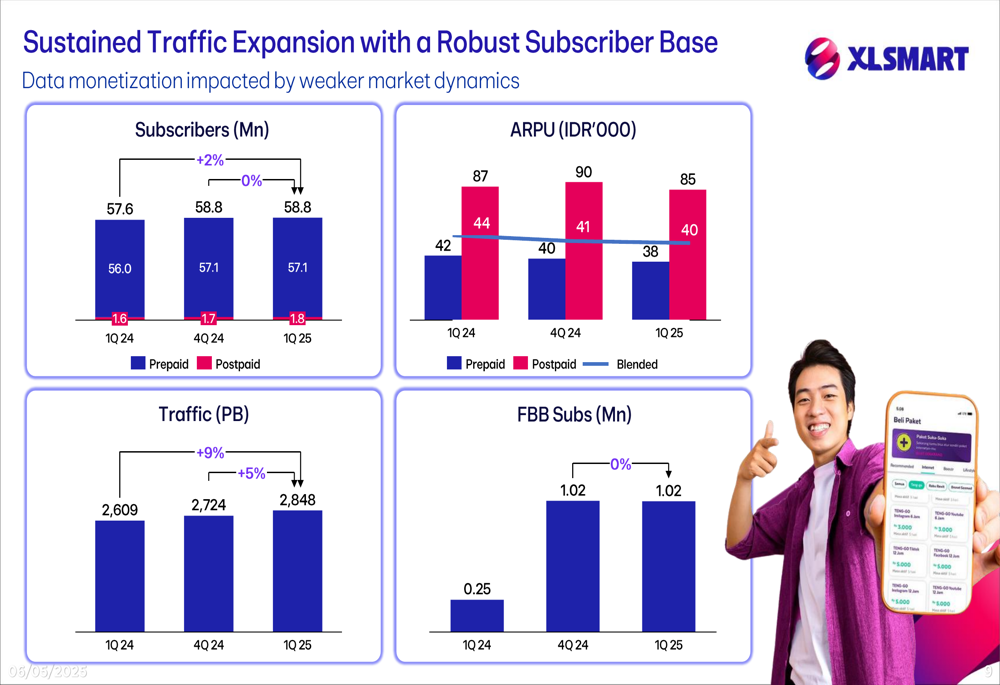

On the operational front, XLSMART maintained its subscriber base at 58.8 million, showing 2% growth year-over-year but flat quarter-over-quarter performance. The company’s traffic volume continued to grow, increasing 9% year-over-year and 5% quarter-over-quarter to 2,848 PB.

The following chart illustrates subscriber metrics and traffic growth:

Detailed Financial Analysis

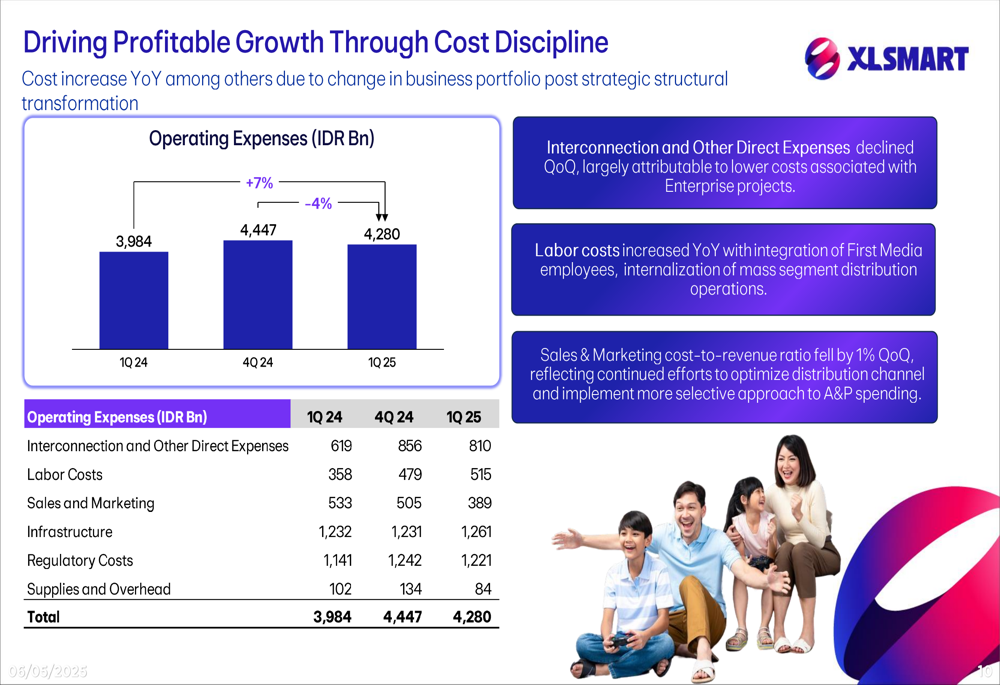

XLSMART’s cost management efforts showed mixed results in Q1 2025. Operating expenses increased 7% year-over-year to IDR 4,280 billion, though this represented a 4% decrease from the previous quarter. The company highlighted reductions in sales and marketing expenses, which fell to IDR 389 million from IDR 505 million in Q4 2024.

The breakdown of operating expenses reveals where cost pressures are occurring:

Labor costs increased significantly, rising to IDR 515 million from IDR 358 million in Q1 2024, likely reflecting integration costs following the merger. Infrastructure costs remained relatively stable at IDR 1,261 million.

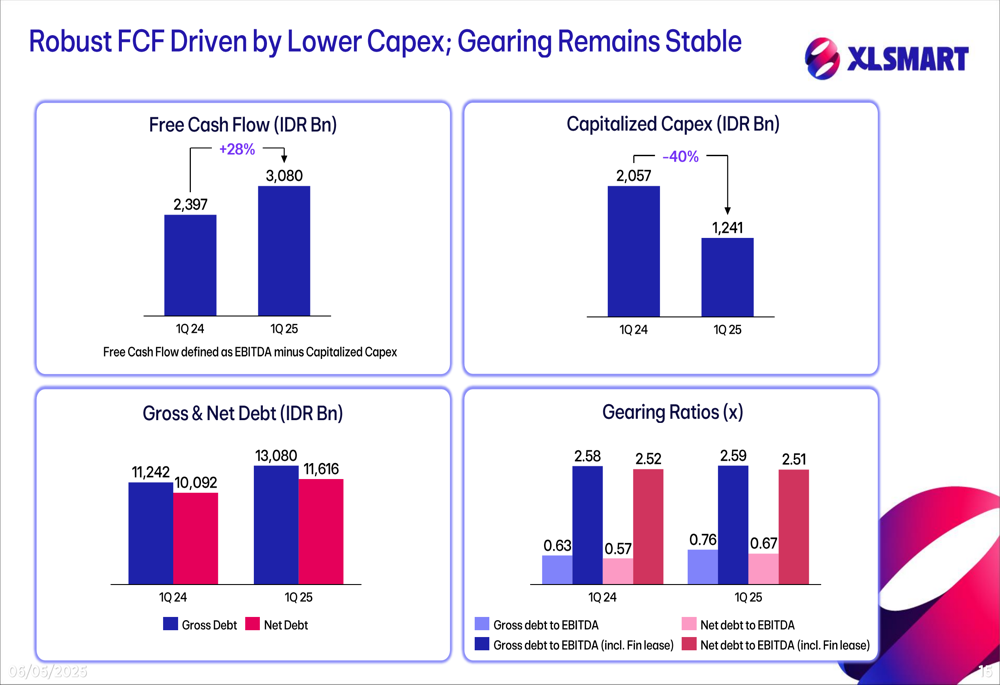

Despite profit challenges, XLSMART demonstrated strong cash flow management. Free Cash Flow increased 28% year-over-year to IDR 3,080 billion, driven primarily by a 40% reduction in capital expenditures, which fell to IDR 1,241 billion.

The following chart shows the company’s improved cash flow position:

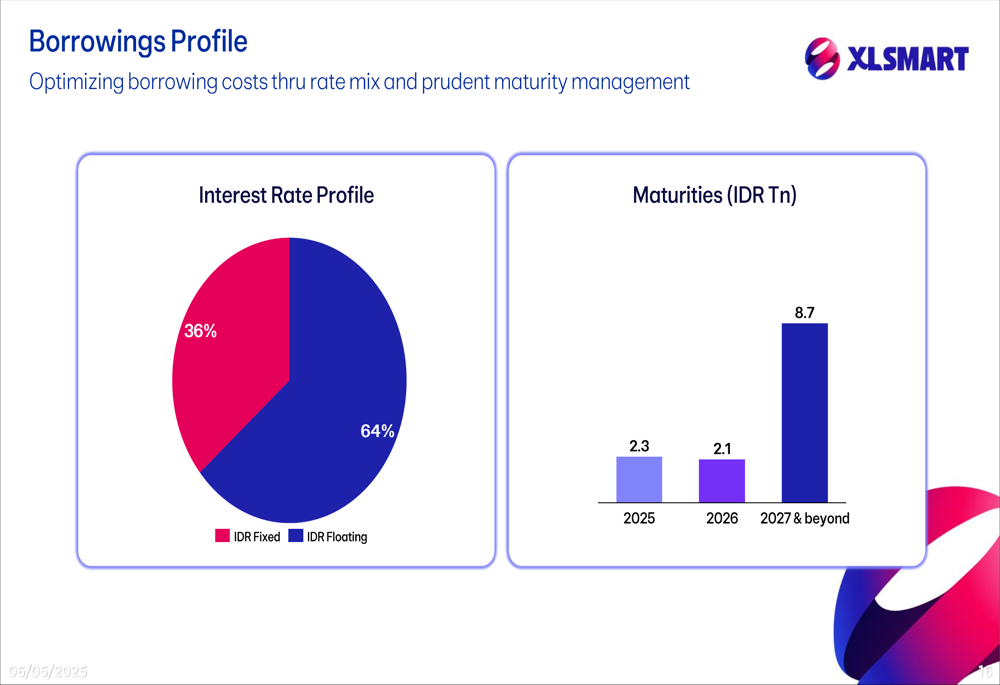

The company’s debt profile remained relatively stable, with gross debt to EBITDA at 2.59x, virtually unchanged from 2.58x in Q1 2024. Net debt increased to IDR 11,616 billion from IDR 10,092 billion a year earlier, with upcoming maturities of IDR 2.3 trillion in 2025 and IDR 2.1 trillion in 2026.

XLSMART’s borrowing profile shows a mix of fixed and floating rate debt:

Strategic Initiatives

XLSMART is pursuing several strategic initiatives to drive future growth. The company’s digital transformation efforts are showing positive results, with own app users increasing 18% year-over-year to 35.7 million. Revenue contribution from these apps grew 21% compared to Q1 2024.

The company’s digitalization metrics demonstrate growing customer engagement:

Network optimization continues to be a priority, with the company shutting down legacy 2G and 3G base stations while expanding its 4G footprint. The number of 4G base stations increased 7% year-over-year and 4% quarter-over-quarter to 115,493, with 63% of sites now fiberized.

The merger with First Media represents a strategic pivot toward a convergence play, combining mobile and fixed broadband services. Management highlighted ongoing integration efforts to improve customer retention and strengthen cross-selling opportunities.

As illustrated in the presentation, the merger opens a new chapter for the company:

Forward-Looking Statements

Looking ahead, XLSMART outlined three key objectives: becoming "the most loved company in Indonesia" by 2027, being the best place to work for employees, and becoming the most efficient service provider in the market.

The company acknowledged ongoing market challenges but expressed confidence in its ability to execute its convergence strategy. Management emphasized that the focus has now shifted from merger completion to synergy realization and integration, which will likely dominate the company’s strategic priorities in coming quarters.

While the presentation maintained an optimistic tone about future prospects, investors appear to be taking a more cautious view, as reflected in the stock’s negative performance following the results announcement. The declining profit metrics amid modest revenue growth suggest XLSMART faces significant challenges in translating its strategic initiatives into improved bottom-line performance in the near term.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.