Street Calls of the Week

Xometry Inc (NASDAQ:XMTR) shares jumped 6.55% in premarket trading to $33.00 following the release of its Q2 2025 earnings presentation on August 5, 2025, which revealed accelerating marketplace growth and the company’s transition to positive adjusted EBITDA.

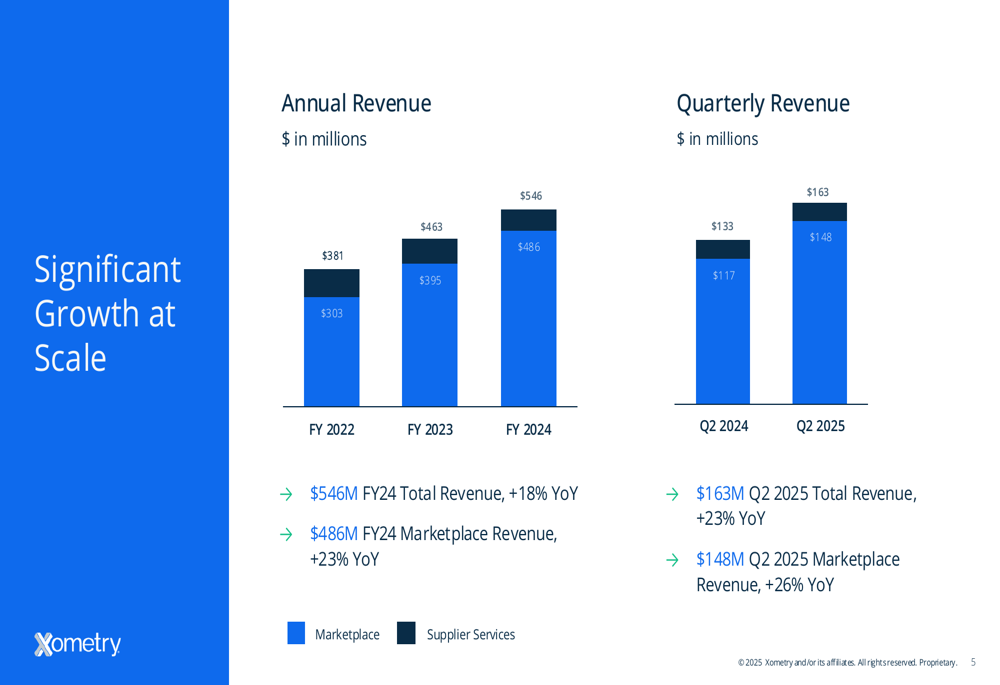

Quarterly Performance Highlights

The digital manufacturing marketplace reported Q2 2025 revenue of $163 million, representing a 23% year-over-year increase. Marketplace revenue, the company’s core business segment, grew even faster at 26% to reach $148 million, while gross profit increased 23% year-over-year to $65.2 million.

Notably, Xometry achieved positive adjusted EBITDA of $3.9 million in the quarter, a $6.6 million improvement compared to the same period last year. This marks a significant milestone in the company’s path to profitability.

As shown in the following chart of quarterly revenue growth:

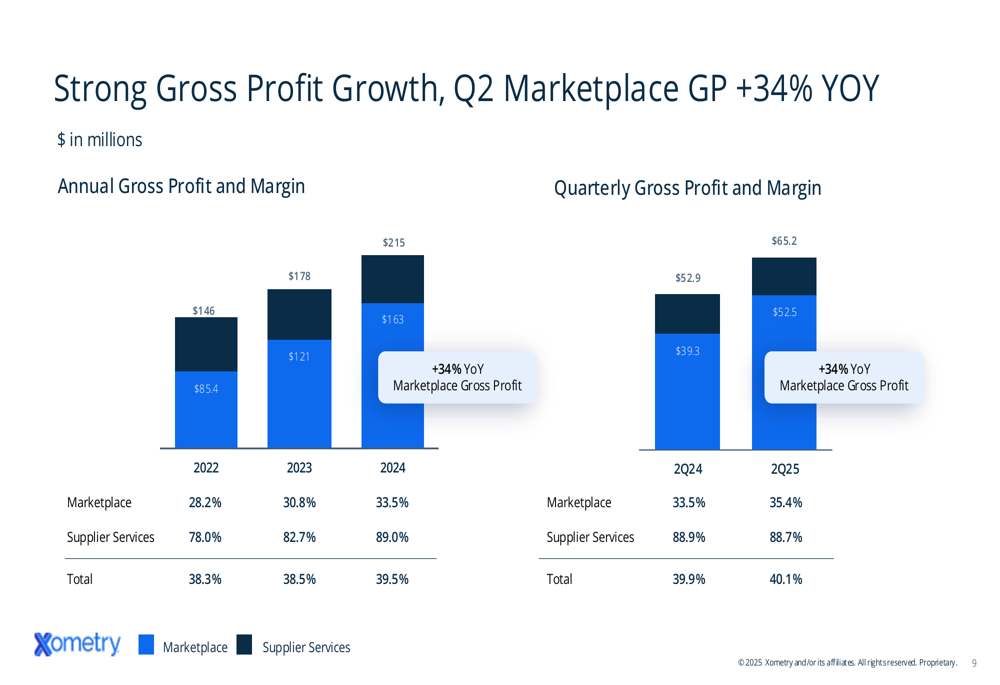

"We delivered strong Q2 2025 financial performance with record revenue of $163 million, representing 26% marketplace growth," the company stated in its presentation. Xometry’s marketplace gross margin expanded to 35.4%, an improvement of 190 basis points year-over-year, while supplier services maintained a robust gross margin of 88.7%.

The company’s gross profit growth has been particularly impressive in the marketplace segment:

Marketplace Expansion

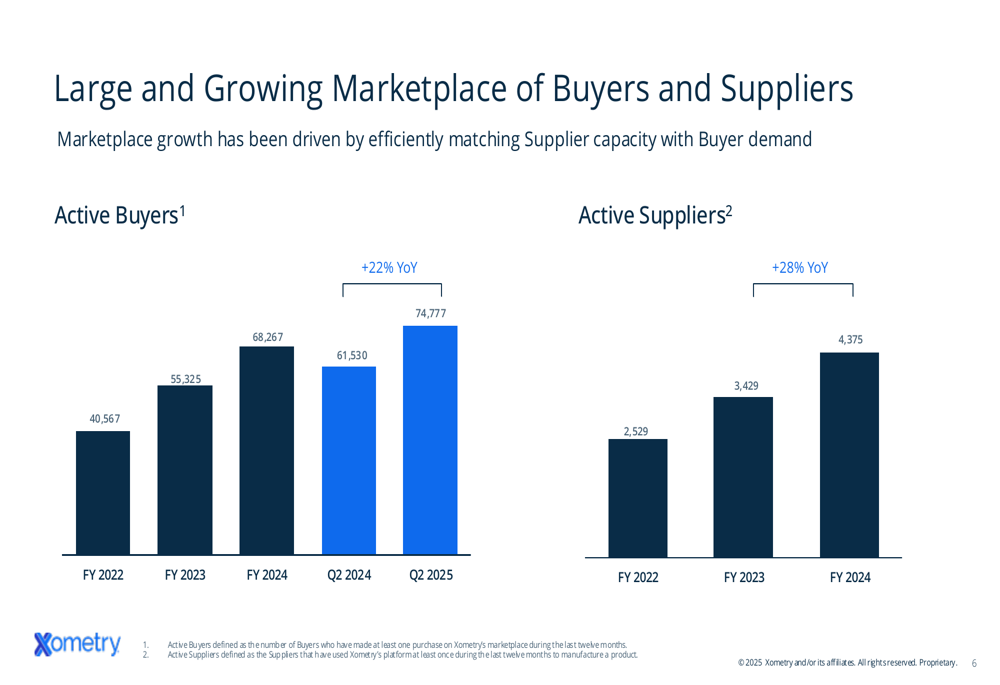

Xometry continues to expand its network of buyers and suppliers, with active buyers increasing 22% year-over-year to 74,777 in Q2 2025. The company’s supplier base grew 28% year-over-year to 4,375 as of Q4 2024.

The following chart illustrates this growth trajectory:

International expansion remains a key growth driver, with international revenue increasing 31% year-over-year to represent 18% of marketplace revenue. The company has established headquarters in Munich, Germany for Europe and Shanghai, China for Asia, and now supports 18 languages and 6 currencies. Xometry’s long-term target is for international business to represent 30-40% of marketplace revenue.

The company is also making significant inroads with enterprise customers. Accounts with last twelve months (LTM) spend of $50,000 or more increased 15% year-over-year to 1,653 in Q2 2025. More impressively, accounts with LTM spend exceeding $500,000 surpassed 100 and grew revenue by over 40% year-over-year. The company maintains exceptional customer retention, with 98% of Q2 2025 revenue coming from existing Xometry accounts.

Operational Efficiency

Xometry has made substantial progress in improving operational efficiency, with non-GAAP operating expenses declining to 37.8% of revenue in Q2 2025 compared to 42.0% in Q2 2024. All expense categories showed improvement as a percentage of revenue, with product development expenses showing the most significant reduction (from 4.5% to 3.6% of revenue).

The company’s advertising efficiency has also improved, with advertising spend as a percentage of marketplace revenue decreasing 130 basis points year-over-year to 5.6%.

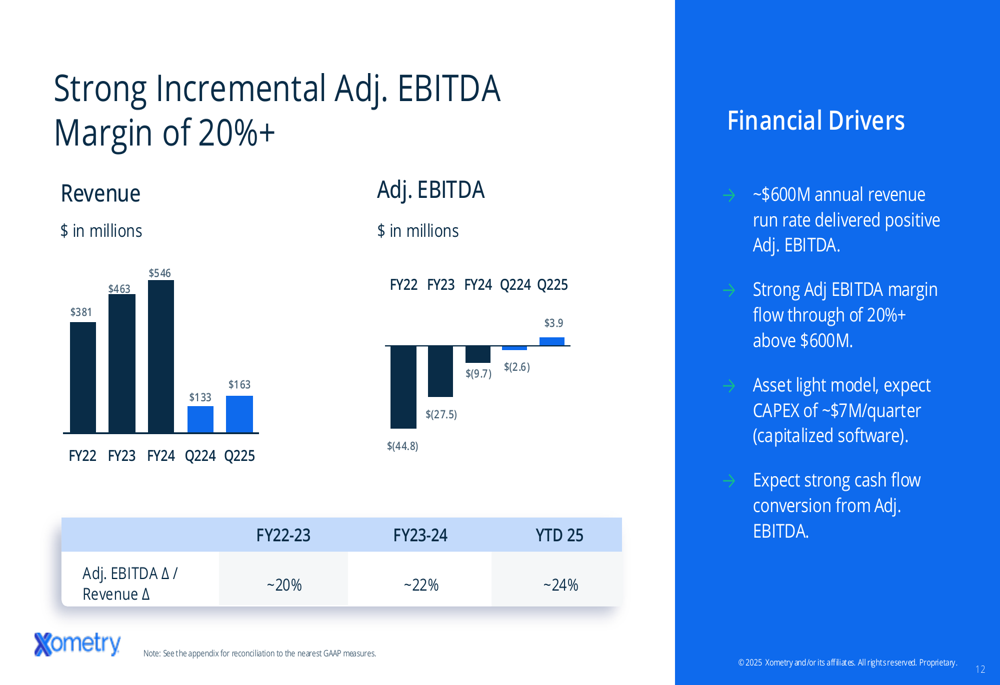

The following chart demonstrates Xometry’s improving adjusted EBITDA trajectory:

"Our asset-light model delivered strong adjusted EBITDA margin flow through of 20%+ above $600 million in annual revenue run rate," the company noted in its presentation. Xometry expects capital expenditures of approximately $7 million per quarter, primarily for capitalized software, and anticipates strong cash flow conversion from adjusted EBITDA.

Forward Guidance

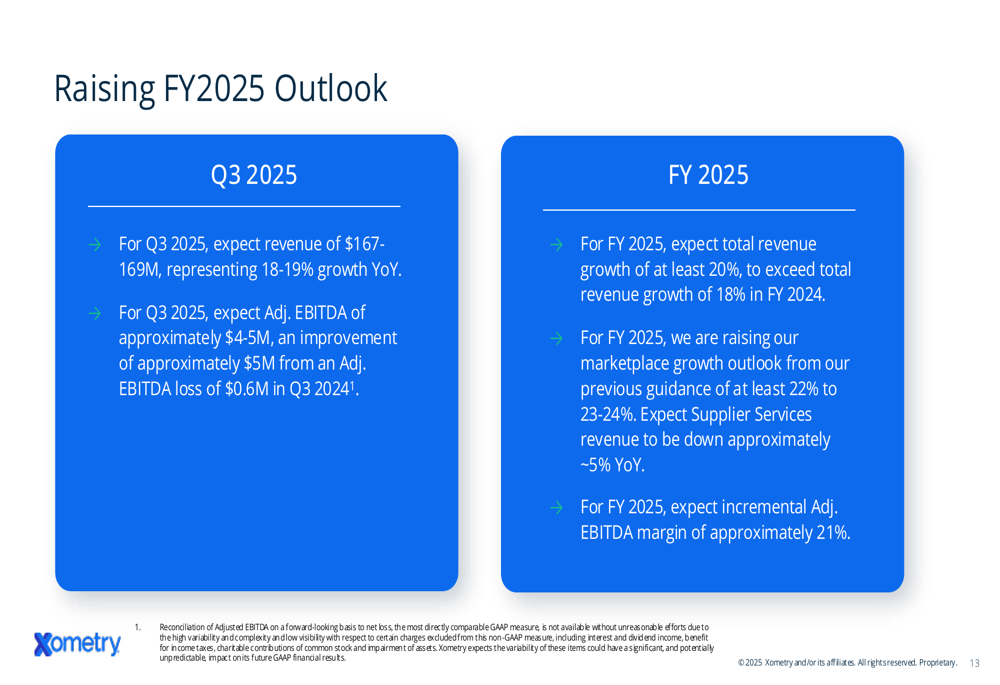

Based on its strong performance, Xometry has raised its outlook for fiscal year 2025. The company now expects:

For Q3 2025, Xometry projects revenue of $167-169 million, representing 18-19% growth year-over-year, with adjusted EBITDA of approximately $4-5 million.

For the full year 2025, the company now forecasts total revenue growth of at least 20%, with marketplace growth of at least 23-24%. Supplier services revenue is expected to decline approximately 5% year-over-year. Xometry anticipates an incremental adjusted EBITDA margin of approximately 21%.

This updated guidance builds on the momentum seen in Q1 2025, when the company reported revenue of $151 million (up 23% year-over-year) and first achieved positive adjusted EBITDA of $100,000.

The Q2 2025 results and raised guidance suggest Xometry is successfully executing its strategy of digitizing and transforming manufacturing while improving operational efficiency. With its marketplace model gaining traction both domestically and internationally, the company appears well-positioned for continued growth and improving profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.