NVIDIA launches Jetson Thor robotics computers for physical AI systems

Introduction & Market Context

XPLR Infrastructure LP (NYSE:XIFR) presented its first quarter 2025 results on May 8, 2025, outlining its strategic initiatives and financial performance amid ongoing challenges. The presentation comes after a disappointing fourth quarter 2024 that saw a significant earnings miss, with the company reporting an EPS of -$1.08 against forecasts of $0.71. Currently trading at $8.49, XIFR shares remain near their 52-week low of $7.53, significantly below their 52-week high of $29.03.

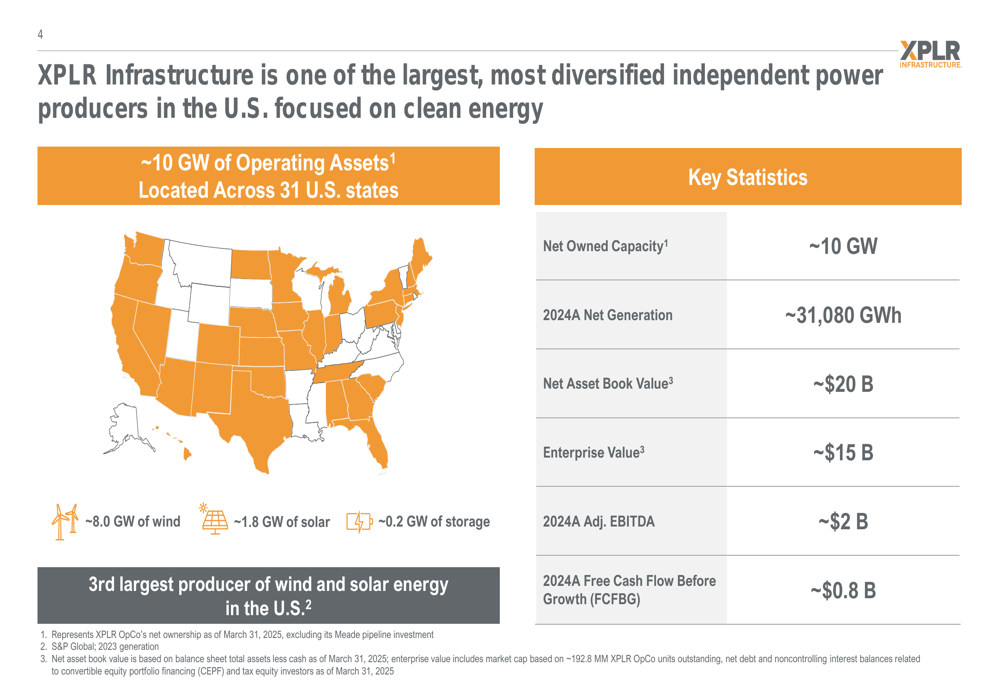

As one of the largest independent power producers in the U.S. focused on clean energy, XPLR Infrastructure operates approximately 10 GW of assets across 31 states, positioning itself as the third-largest producer of wind and solar energy in the country.

As shown in the following comprehensive overview of the company’s assets and financial metrics:

Q1 2025 Performance Highlights

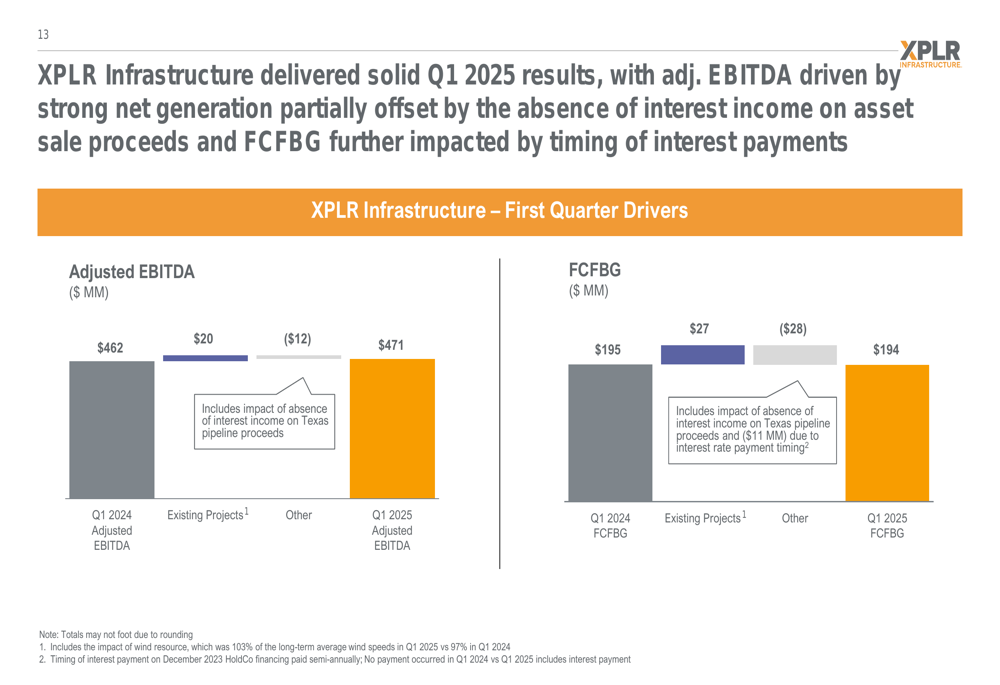

XPLR Infrastructure reported Q1 2025 Adjusted EBITDA of $471 million, a modest increase from $462 million in Q1 2024. This improvement was primarily driven by strong net generation from existing projects, which contributed an additional $20 million, partially offset by a $12 million decrease from other factors including the absence of interest income on asset sale proceeds.

Free Cash Flow Before Growth (FCFBG) for Q1 2025 was $194 million, slightly down from $195 million in the same period last year. While existing projects contributed positively with $27 million, this was more than offset by a $28 million decrease from other factors, including the timing of interest payments.

The following chart illustrates the drivers of Adjusted EBITDA and FCFBG for Q1 2025:

Portfolio Diversification and Stability

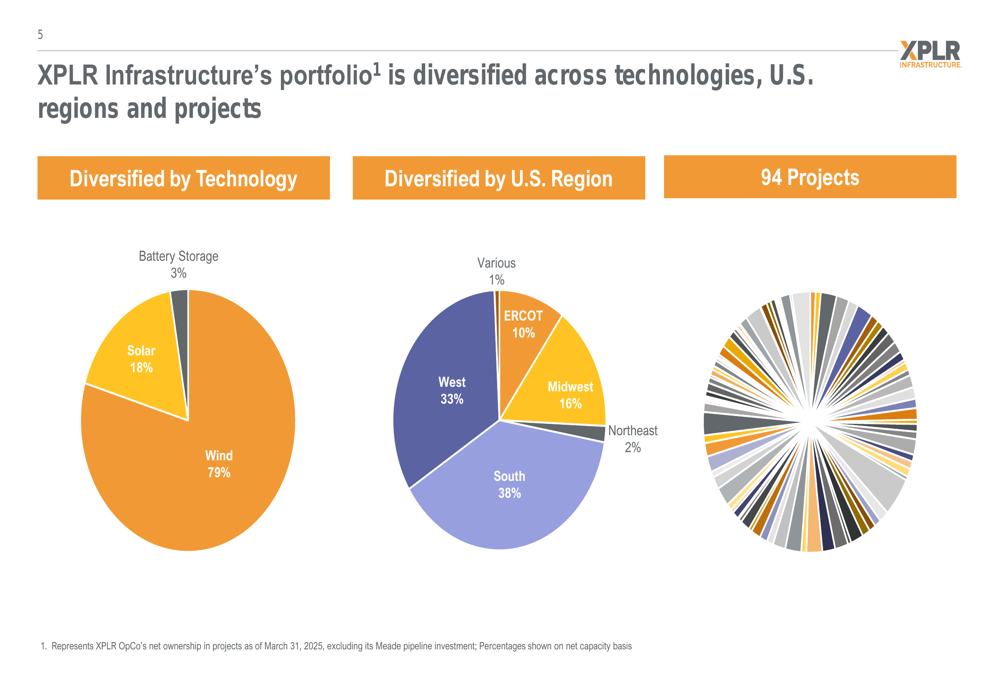

XPLR Infrastructure’s portfolio comprises 94 projects diversified across technologies and U.S. regions. Wind assets represent 79% of the portfolio, followed by solar at 18% and battery storage at 3%. Geographically, the portfolio is spread across the South (38%), West (33%), Midwest (16%), ERCOT (10%), Northeast (2%), and various other regions (1%).

The company’s portfolio diversification across technologies and regions is illustrated in the following chart:

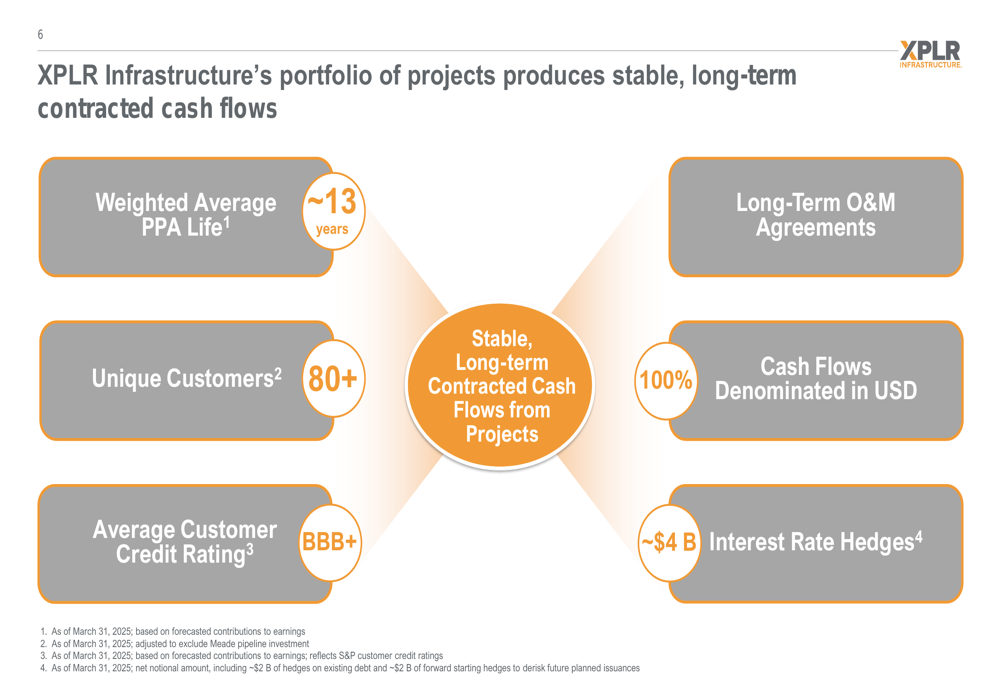

A key strength of XPLR’s business model is its stable, long-term contracted cash flows. The portfolio features a weighted average Power Purchase Agreement (PPA) life of approximately 13 years with over 80 unique customers having an average credit rating of BBB+. All cash flows are denominated in USD, and the company has interest rate hedges totaling approximately $4 billion.

The following slide highlights the characteristics contributing to XPLR’s stable cash flow profile:

Strategic Initiatives

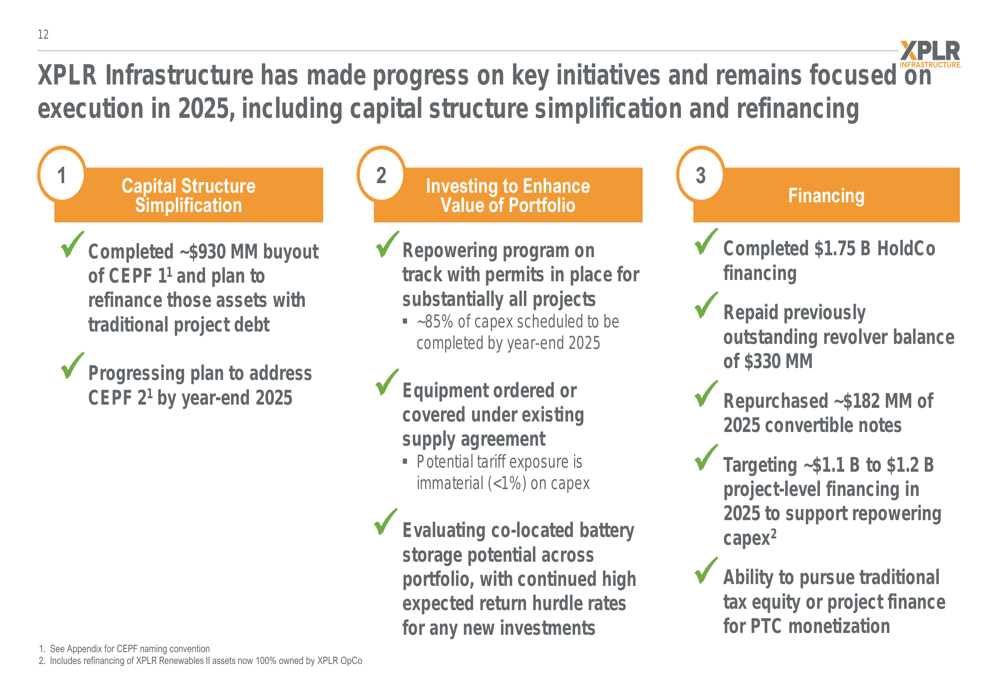

XPLR Infrastructure is focusing on several key strategic initiatives to enhance shareholder value and address recent financial challenges. The company’s capital allocation strategy prioritizes four areas: simplifying capital structure through buyout of selected Convertible Equity Portfolio Financings (CEPFs), investing in the existing portfolio, investments in clean energy assets, and returning capital to unitholders.

The company has made significant progress on these initiatives in Q1 2025, including:

1. Completing a ~$930 million buyout of CEPF 1 and planning to refinance those assets with traditional project debt

2. Advancing repowering programs with permits in place for substantially all projects

3. Completing a $1.75 billion HoldCo financing

4. Repaying a previously outstanding revolver balance of $330 million

5. Repurchasing ~$182 million of 2025 convertible notes

The following slide summarizes the progress on these key initiatives:

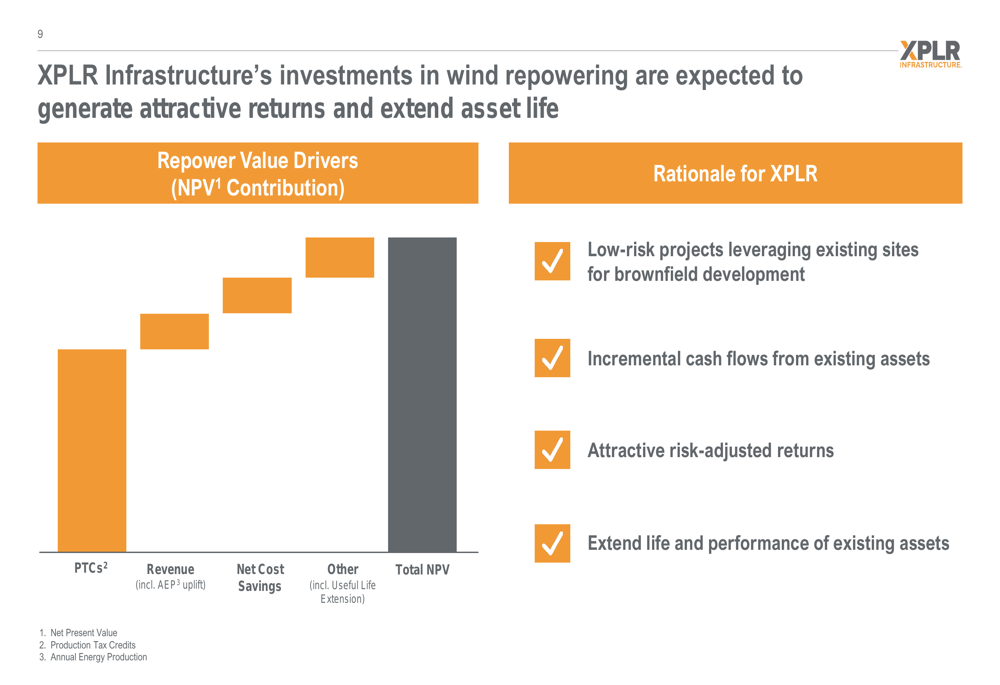

XPLR’s repowering investments are expected to generate attractive returns and extend asset life. The company is evaluating co-located battery storage potential across its portfolio while maintaining high expected return hurdle rates for any new investments.

The value drivers for repowering investments are illustrated in this chart:

Financial Outlook and Strategy

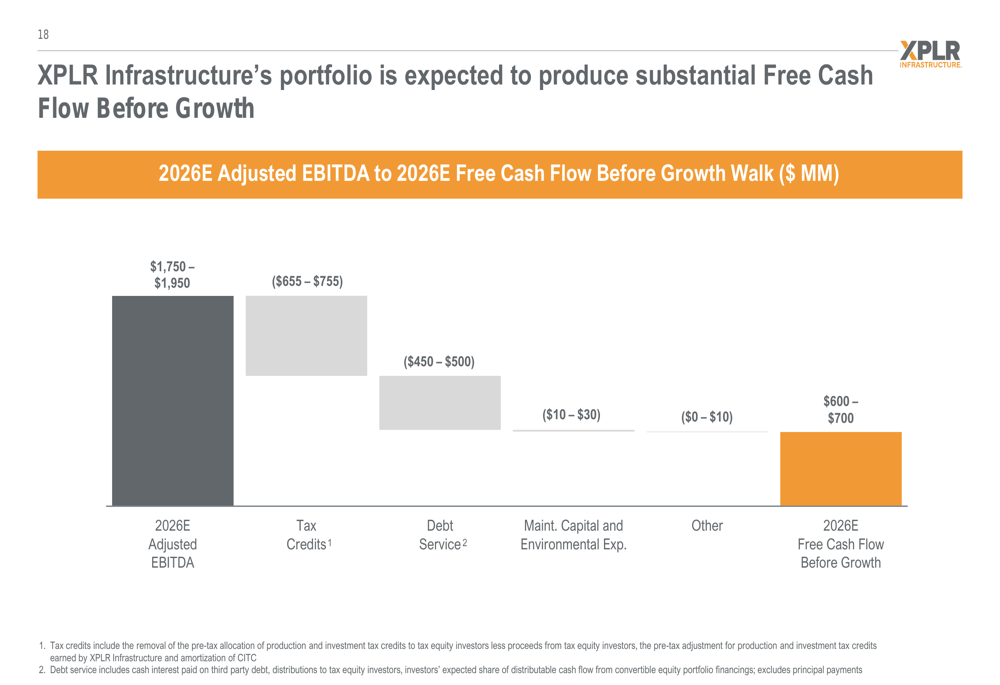

XPLR Infrastructure reaffirmed its financial expectations for 2025 and 2026. For 2025, the company expects Adjusted EBITDA of $1,850-$2,050 million. For 2026, Adjusted EBITDA is projected at $1,750-$1,950 million with FCFBG of $600-$700 million.

The company’s financial strategy focuses on prudently funding capital allocation priorities while maintaining balance sheet strength. XPLR’s 2025-2026 financial plan includes addressing legacy CEPF financings to simplify the capital structure and enhance long-term financing and strategic flexibility.

The following chart shows the expected walk from 2026E Adjusted EBITDA to Free Cash Flow Before Growth:

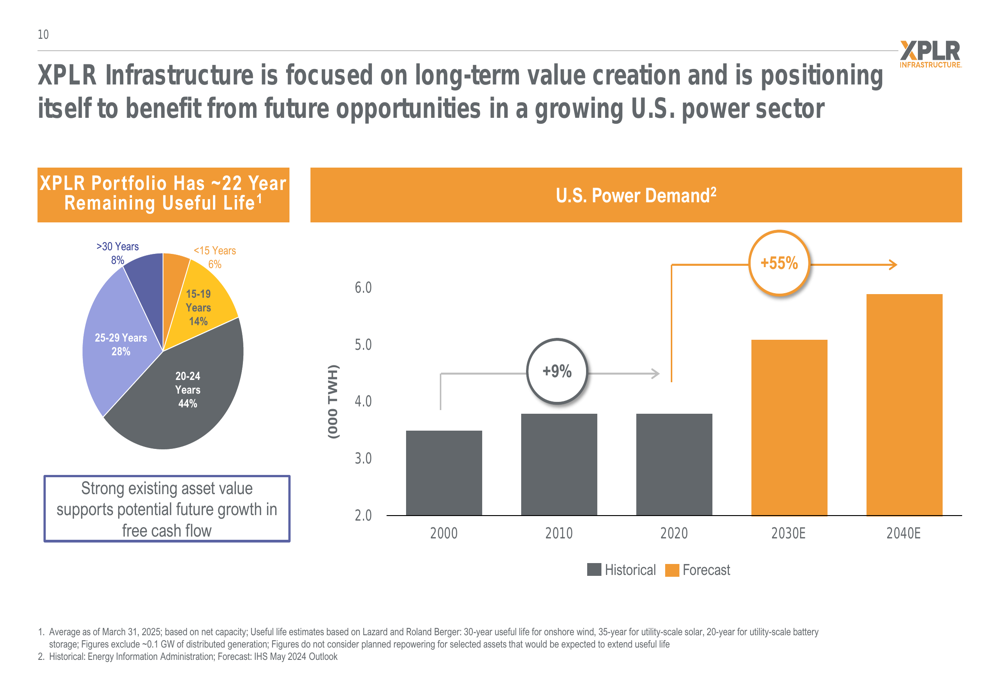

XPLR Infrastructure’s portfolio has approximately 22 years of remaining useful life, positioning the company to benefit from the projected growth in U.S. power demand, which is forecast to increase by 55% by 2040.

The long-term value creation potential is illustrated in this chart showing portfolio useful life and U.S. power demand forecast:

Investor Perspective

Despite the company’s positive long-term outlook, XPLR Infrastructure faces significant near-term challenges. The stock’s current trading price of $8.49 represents a substantial discount from its 52-week high of $29.03, reflecting investor concerns following the Q4 2024 earnings miss.

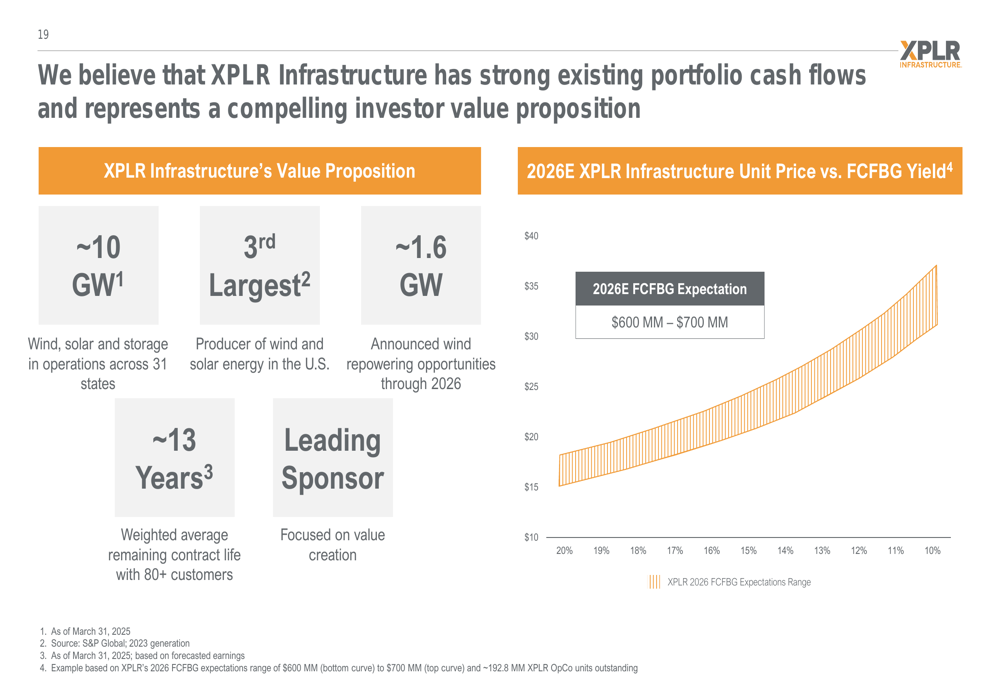

The company believes its strong existing portfolio cash flows represent a compelling investor value proposition, highlighting its 10 GW of wind, solar, and storage operations across 31 states, approximately 1.6 GW of announced wind repowering opportunities through 2026, and weighted average remaining contract life of 13 years with 80+ customers.

The following chart illustrates XPLR Infrastructure’s investor value proposition, showing the relationship between unit price and FCFBG yield:

However, investors should note the significant gap between the company’s presentation of its value proposition and its recent stock performance. While management focuses on long-term value creation through portfolio optimization and capital structure simplification, the market appears more concerned with near-term execution risks and financial stability following the disappointing Q4 2024 results.

As XPLR Infrastructure continues its efforts to stabilize and simplify its business model, investors will be closely monitoring the company’s progress on its strategic initiatives and its ability to deliver on its financial expectations for 2025 and 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.