Oil prices push higher amid worries over Russian supply disruptions

Xylem Inc (NYSE:XYL) presented its second quarter 2025 earnings results on July 31, showcasing accelerated growth across all business segments and raising its full-year guidance. The water technology company reported 6% organic revenue growth and a 16% increase in adjusted earnings per share, demonstrating strong execution amid tariff challenges.

Quarterly Performance Highlights

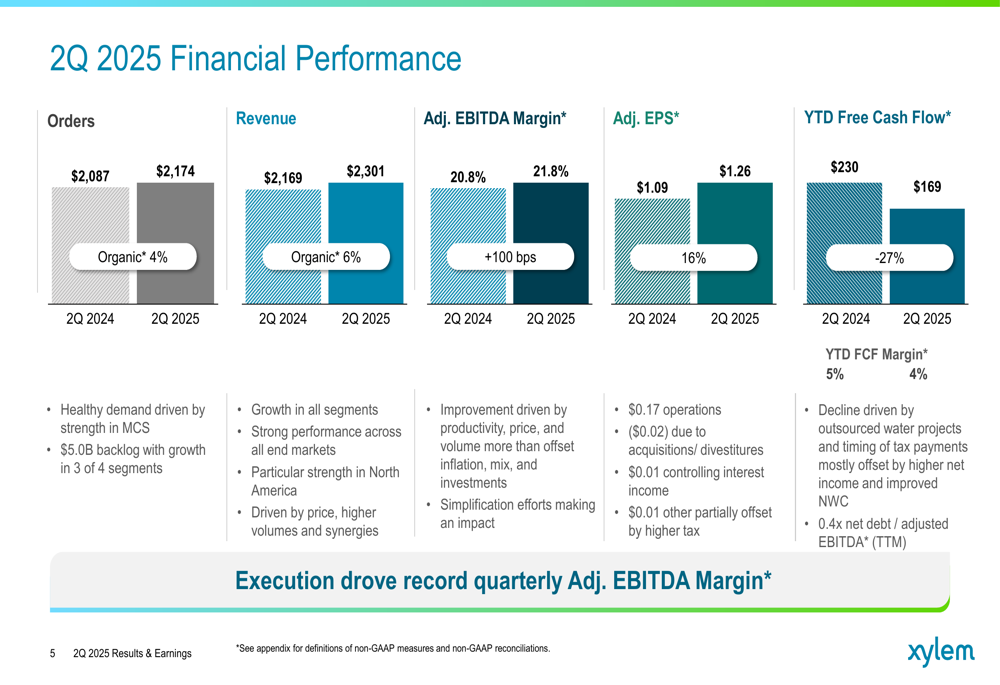

Xylem reported Q2 2025 revenue of $2.301 billion, representing 6% organic growth compared to the same period last year. Orders grew 4% organically to $2.174 billion, indicating continued healthy demand. The company achieved an adjusted EBITDA margin of 21.8%, expanding 100 basis points year-over-year, while adjusted earnings per share increased 16% to $1.26.

"We outperformed expectations on strong execution," stated the company in its presentation, highlighting order strength driven by developed markets and revenue growth across all segments.

As shown in the following chart of quarterly financial performance:

The company’s year-to-date free cash flow decreased 27% to $169 million, with a free cash flow margin of 4% compared to 5% in the prior year. However, Xylem maintained its net debt to adjusted EBITDA ratio at 1.5x, indicating a stable financial position.

Segment Performance Analysis

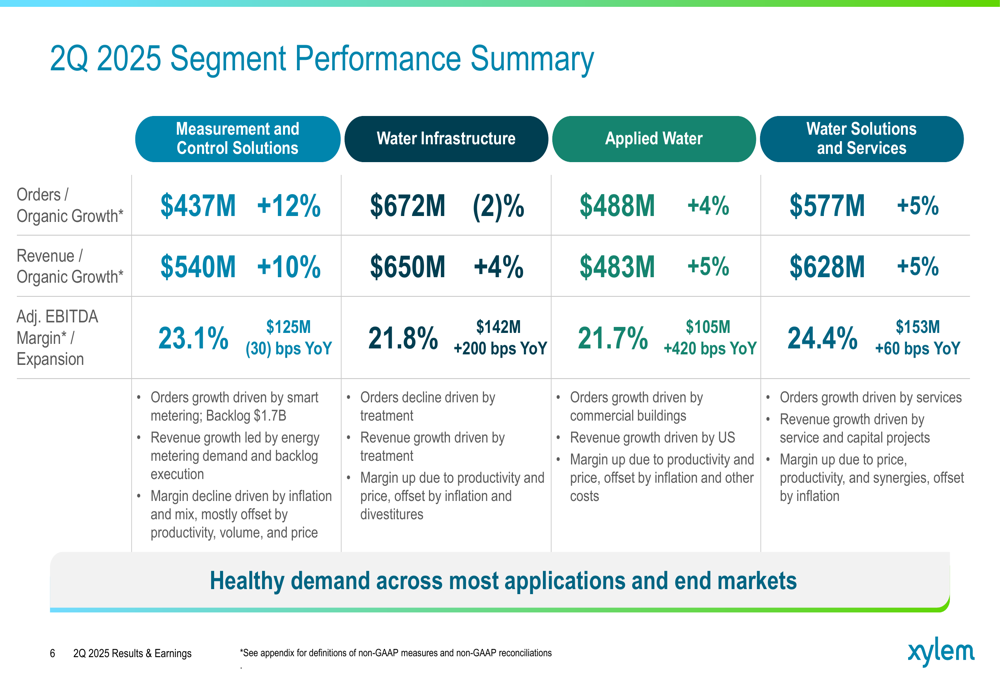

All four of Xylem’s business segments delivered organic revenue growth in the second quarter. The Measurement and Control Solutions segment led with 10% organic revenue growth and orders up 12%, driven by strong demand in test applications and smart metering. Water Infrastructure, Applied Water, and Water Solutions and Services each achieved 4-5% organic revenue growth.

The segment breakdown reveals margin expansion across the board, with Applied Water showing the most significant improvement at 420 basis points year-over-year:

"We’re seeing healthy demand across most applications and end markets," noted the company, with particularly strong performance in the utilities and industrial sectors. The Applied Water segment benefited from favorable price realization and productivity improvements, while Water Infrastructure saw continued strength in treatment and transport applications.

Tariff Impact Mitigation

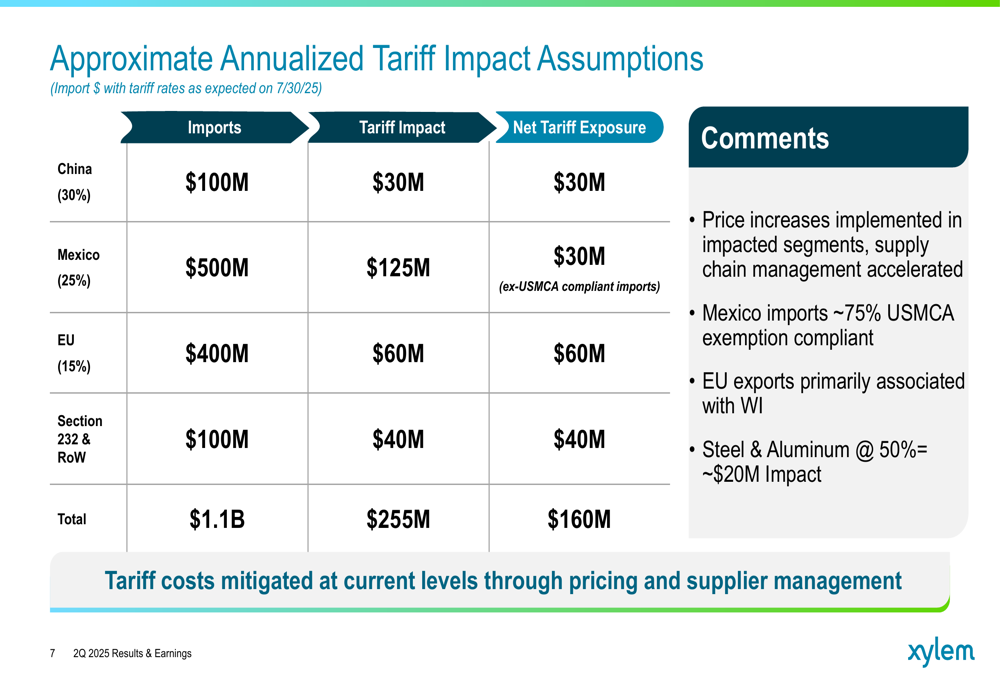

A key focus of the presentation was Xylem’s strategy for managing tariff impacts. The company faces approximately $255 million in annualized tariff impacts, primarily from Mexico ($125 million) and the EU ($60 million). However, through various mitigation strategies, Xylem has reduced its net tariff exposure to $160 million.

The following chart details the company’s tariff impact assumptions:

"Tariff costs mitigated at current levels through pricing and supplier management," the company stated, noting that about 75% of Mexico imports are USMCA exemption compliant. Xylem has implemented price increases in impacted segments and accelerated supply chain management initiatives to offset these challenges.

Updated Guidance

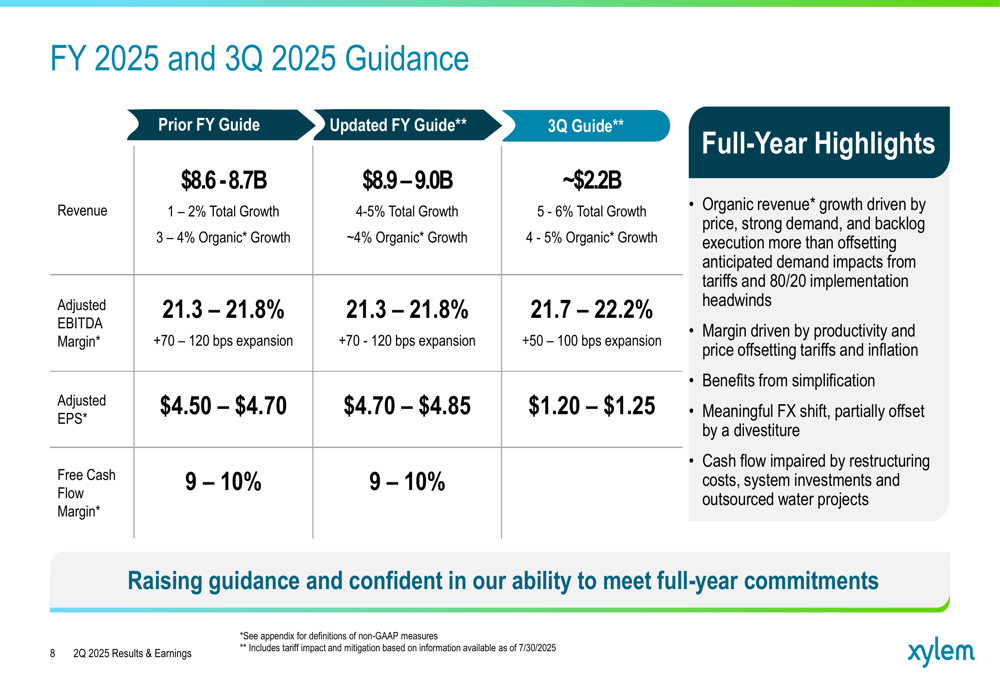

Based on strong first-half performance and a positive outlook for the remainder of the year, Xylem raised its full-year 2025 guidance. The company now expects:

- Revenue of $8.9-9.0 billion (4-5% total growth, ~4% organic growth), up from previous guidance of $8.6-8.7 billion

- Adjusted EBITDA margin of 21.3-21.8% (70-120 bps expansion)

- Adjusted EPS of $4.70-$4.85, increased from $4.50-$4.70 previously

For the third quarter of 2025, Xylem projects:

- Revenue of approximately $2.2 billion (5-6% total growth, 4-5% organic growth)

- Adjusted EBITDA margin of 21.7-22.2% (50-100 bps expansion)

- Adjusted EPS of $1.20-$1.25

The updated guidance is detailed in the following table:

This guidance raise represents a significant improvement from the company’s outlook presented in its Q1 2025 earnings, where Xylem maintained its full-year guidance rather than increasing it.

Strategic Initiatives & Outlook

Xylem’s presentation emphasized that its operating model transformation is driving profitable growth. The company highlighted that pricing and supply chain efforts are successfully offsetting tariff impacts and inflation, while benefits from simplification initiatives are improving customer experience.

"Self-help initiatives building foundation for long-term growth," the company noted among its key takeaways, along with an "aligned, customer-centric culture driving shareholder value creation."

Recent acquisitions are strengthening Xylem’s advanced treatment portfolio, enhancing its competitive position in the water technology market. The company’s diversified business model, addressing the full lifecycle of water, provides resilience against market fluctuations.

Xylem’s stock closed at $130.60 on July 30, 2025, down 1.03% ahead of the earnings presentation. The company’s shares have traded between $100.47 and $138.50 over the past 52 weeks, indicating investor confidence in its long-term strategy despite near-term challenges.

With its raised guidance and demonstrated ability to navigate tariff headwinds, Xylem appears well-positioned to maintain its growth trajectory through the remainder of 2025, supported by strong demand in its key markets and continued operational improvements.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.